Produce Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Produce Packaging Market Set to Grow to $55 Billion by 2034, Driven by Sustainability and Food Waste Reduction

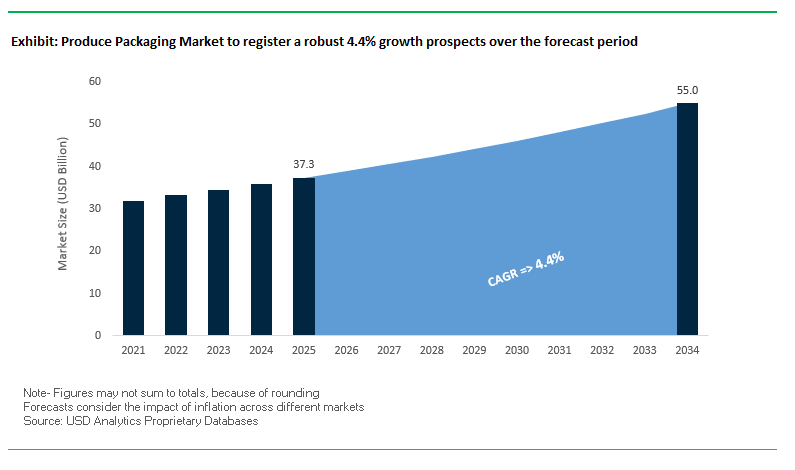

The global produce packaging market is projected to expand from $37.3 billion in 2025 to $55 billion by 2034, growing at a CAGR of 4.4%. Increasing consumer demand for freshness, convenience, and sustainability is shaping the industry. Packaging innovations are focused on extending shelf life, preventing damage during transport, and reducing food waste, a critical consideration as 30-40% of produce is lost between farm and table.

Key Insights for industry professionals and buyers:

- Food Waste Reduction is Central: Advanced packaging solutions preserve freshness and reduce losses.

- Corrugated Boxes Maintain Market Dominance: Their strength, durability, and recyclability make them ideal for bulk transport.

- Convenience and Portability Drive Innovation: Ready-to-eat salads, pre-cut vegetables, and single-serve fruits are influencing design trends.

- Sustainability Leads Design Choices: Eco-friendly materials like recycled paper, compostable films, and reusable plastics are increasingly prioritized by consumers and regulators.

- Adhesive and Material Innovations Are Emerging: Bio-based films and nanocoatings improve shelf life and efficiency, supporting a circular economy.

Market Analysis: Innovations in Produce Packaging Are Shaping Sustainability and Efficiency Standards

The produce packaging industry has recently witnessed breakthroughs in sustainable materials and smart solutions. In August 2025, scientists developed a clear and strong film from grapevine waste designed to biodegrade in days, providing a highly sustainable alternative to traditional films. The same month, Afera’s survey emphasized supply chain diversification and adhesive innovation, relevant to packaging for both film and corrugated boxes.

Material performance and shelf-life enhancement have also evolved. In April 2025, Amcor and Nfinite Nanotechnology partnered to validate nanocoating technologies that improve oxygen barriers, critical for maintaining produce freshness. Complementing this, March 2025 saw Cascades Inc. release recycled fiber produce baskets, offering sustainable, durable alternatives for fruit and vegetable transport.

Efficiency and food safety innovations are also gaining traction. In September 2024, the U.S. EPA approved antimicrobial packaging films to prevent bacterial and mold growth, extending produce shelf life. Earlier, in November 2024, a leading packaging company introduced faster-installing films for packaging machinery, allowing producers to optimize operations, reduce labor, and minimize costs.

Emerging Trends and Strategic Opportunities in the Produce Packaging Market

Strategic Shift to Reusable and Returnable Plastic Crates (RPCs) for Supply Chain Efficiency

The produce packaging market is experiencing a major transformation as reusable plastic crates (RPCs) replace traditional single-use packaging. Studies highlight that RPCs can dramatically reduce post-harvest food loss—such as an African study on tomato transport where damage fell from 41.12% in raffia baskets to only 4.92% with RPCs. This not only ensures better quality produce reaching consumers but also creates measurable value across the supply chain. From an environmental standpoint, a Fraunhofer IBP life cycle assessment confirmed RPCs emit 60% less CO₂ than single-use cardboard packaging when used repeatedly, with advantages compounding over their lifespan of up to 120 uses. Although initial costs are higher, financial modeling shows that RPCs pay back their investment within two years due to durability, reusability, and food waste reduction. For retailers and growers alike, RPCs align economic, operational, and sustainability priorities, making them a cornerstone of modern produce packaging strategies.

Rapid Adoption of Perforated and Engineered Breathable Films for Modified Atmosphere Packaging (MAP)

Breathable film technology is redefining shelf-life management for fresh produce. Continuous, non-perforated films often fail to balance product respiration and gas exchange, leading to spoilage. However, engineered perforated films—developed through precision laser micro-perforation—enable controlled oxygen and carbon dioxide exchange, extending freshness for products like strawberries and leafy greens. These perforations, typically 50–60 µm in diameter, are customized to match respiration rates, ensuring optimal modified atmosphere conditions. In addition, advanced films now manage ethylene gas release, slowing premature ripening of highly perishable items such as cut flowers. Research confirms that this packaging innovation not only extends product life but also preserves visual and nutritional quality, aligning with consumer demand for fresher, longer-lasting produce. With food waste reduction becoming a global sustainability priority, perforated breathable films are quickly gaining traction among producers and retailers.

Development of High-Performance Bio-Based and Compostable Films for Fresh Produce

The push to eliminate petroleum-based plastics has unlocked significant opportunity in bio-based and compostable produce packaging. Materials derived from starch, cellulose, and seaweed are emerging as viable alternatives to conventional plastics, offering moisture resistance, clarity, and breathability while being fully compostable. Research into chitosan-based films, derived from crustacean shells, shows strong antimicrobial activity, extending shelf life by reducing microbial contamination—a crucial benefit for fresh produce. Academic studies further highlight that mechanical and barrier properties of bio-based films can be enhanced naturally or with minimal additives, ensuring they remain sustainable. The industry is moving toward developing films that rival conventional plastics in functionality while maintaining full biodegradability. For retailers under pressure to meet corporate sustainability targets and comply with single-use plastic bans, bio-based packaging presents both a regulatory-compliant and marketable solution.

Integration of Smart Labels for Real-Time Freshness and Traceability Monitoring

Smart labeling technologies represent one of the most disruptive opportunities in produce packaging. Time-temperature indicators (TTIs) are already gaining consumer acceptance in Europe, where studies show they enhance perceptions of freshness and foster greater trust in the supply chain. For retailers, the integration of TTIs and RFID-enabled smart labels allows dynamic inventory management, replacing static expiration dates with real-time shelf-life monitoring. This technology minimizes food waste, optimizes stock rotation, and ensures higher customer satisfaction. RFID tags also enable full supply chain visibility by automatically transmitting product condition and location data without the need for manual scanning. With food safety, transparency, and waste reduction becoming top priorities, smart packaging not only strengthens consumer confidence but also equips retailers and suppliers with actionable insights for operational efficiency. This positions smart labels as a critical innovation driving the next wave of digital transformation in produce packaging.

Competitive Landscape: Leading Produce Packaging Companies Focus on Sustainability, Customization, and Operational Efficiency

The global produce packaging market is dominated by companies leveraging sustainable materials, advanced coatings, and customized packaging solutions. Their strategies focus on reducing food waste, supporting the circular economy, and meeting consumer demand for convenience.

Amcor plc: Advancing Nanocoating and Sustainable Packaging for Extended Freshness

Amcor’s produce packaging solutions include films, trays, and bags designed to extend shelf life and improve product visibility. In April 2025, Amcor partnered with Nfinite Nanotechnology to validate nanocoating technologies for recyclable and compostable packaging. With a strong R&D network, Amcor collaborates with customers to integrate custom packaging solutions into production processes, enhancing efficiency and reducing waste.

WestRock Company: Delivering Fiber-Based Packaging Solutions Aligned with Consumer Trends

WestRock specializes in corrugated containers and folding cartons for fresh produce transport. The company collaborates with clients to create digitally printed, branded packaging for consumer convenience, such as custom meal boxes. Its emphasis on automation, smart packaging, and RFID integration positions WestRock as a forward-looking partner in the produce packaging sector.

International Paper Company: Leading Sustainable Fiber-Based Packaging Solutions Globally

International Paper focuses on recyclable corrugated boxes and paper-based packaging that protect produce and facilitate global commerce. Following the sale of its cellulose fibers unit for $1.5 billion, the company has streamlined operations to focus on sustainable packaging solutions. Its commitment to forest stewardship, water conservation, and recycling enhances its reputation as an eco-conscious supplier.

Mondi Group: Pioneering Circular Economy Practices in Produce Packaging

Mondi offers flexible packaging, films, pouches, and paper-based containers for the produce industry. Recent collaborations, such as with Tesco for reduced-plastic multipacks, highlight Mondi’s strategy to reduce plastic while maintaining product integrity. The company prioritizes recyclable, biodegradable, and circular economy-compatible materials in its packaging solutions.

Berry Global Inc.: Providing Durable Plastic Packaging Solutions for Retail and Bulk Produce

Berry Global manufactures plastic containers, films, and trays for diverse produce applications. Its strategy emphasizes the circular plastics economy, using post-consumer recycled content (PCR) and innovative recycling technologies. The company works closely with customers to develop custom packaging solutions integrated with production processes, ensuring efficiency, sustainability, and adaptability.

Produce Packaging Market Share Insights, 2025-2034

Bags & Pouches Dominate Market Share by Product Type in the Produce Packaging Industry

Bags and pouches represent the leading product type in produce packaging, holding 28% of market share, driven by their material efficiency, cost-effectiveness, and versatility across both fruits and vegetables. The rise of high-barrier, breathable films in salad and fresh-cut packaging has made pouches critical for shelf-life extension and food waste reduction, while resealable formats cater to consumer convenience. Clamshells follow with 22% share, playing a premium role in protecting delicate, high-value produce such as berries and cherries, where damage prevention and visual appeal justify higher material use. Trays, with around 18% share, remain indispensable for heavier produce like tomatoes and mushrooms, particularly in combination with overwraps or lidding films. Films and wraps, although less visible at 15% share, are a technical enabler of shelf-life management, with micro-perforated designs tailored to the respiration rates of specific produce. Boxes, cartons, nets, and mesh bags collectively capture niche demand, primarily where sustainability, branding, or airflow are decisive factors. Overall, this segmentation underscores how bags and clamshells anchor volume, while films and trays drive functional innovation in extending freshness.

Fruits Packaging Holds the Largest Market Share by Application in the Produce Packaging Industry

Fruits dominate the produce packaging market with a 40% share, reflecting the sector’s diversity and high value. From clamshells for delicate berries to mesh bags for citrus and apples, fruit packaging is at the forefront of innovations in ethylene-absorbing liners, breathable films, and recyclable rPET clamshells, all aimed at preventing spoilage and extending shelf life. Vegetables follow with 35% share, where bulk packaging for items such as potatoes and onions coexists with value-added fresh-cut vegetables, increasingly adopting MAP pouches and trays for extended preservation. Salads and fresh-cut produce account for 20% share, representing the most technology-intensive segment of the market. Here, packaging is engineered as a preservation system, relying heavily on MAP films and trays to extend freshness from a few days to multiple weeks, enabling the booming meal kit and ready-to-eat sector. Horticulture packaging, while a smaller 5% niche, is driven by sustainability and functionality, with biodegradable pots and plantable trays emerging as eco-friendly solutions for nurseries and floriculture. Collectively, this segmentation highlights how fruits anchor volume, salads and fresh-cut lead in technology, and horticulture drives eco-innovation in produce packaging.

European Union: PPWR and Circular Economy Targets Transforming Produce Packaging

The European Union produce packaging market is undergoing sweeping changes under the Packaging and Packaging Waste Regulation (PPWR), which took effect in February 2025. This legislation replaces older directives and is one of the most comprehensive frameworks for packaging life-cycle management. It introduces ambitious goals to achieve a circular economy, directly impacting how fresh fruits and vegetables are packaged and sold. A landmark provision effective January 2030 bans single-use plastic packaging for fresh produce under 1.5 kg, pushing retailers and suppliers toward fiber-based trays, compostable films, and reusable solutions.

The regulation introduces a packaging recyclability grading system, requiring all packaging to be at least 70% recyclable (Grade C) by 2030, and progressing to Grade B (80%) or Grade A (95%) by 2038. New restrictions on PFAS in food-contact packaging (effective August 2026), mandatory harmonized recycling labels by 2028, and rules capping empty space in e-commerce packaging at 50% by 2030 further redefine design priorities. These requirements are driving innovation in eco-friendly produce trays, mono-material films, and intelligent labeling systems, ensuring compliance while meeting sustainability expectations.

United States: Smart Packaging and E-Commerce Driving Innovation in Fresh Produce Packaging

The United States produce packaging market is strongly influenced by consumer demand for longer shelf life and food waste reduction. Innovations such as Modified Atmosphere Packaging (MAP) and vacuum-sealed films are now widely used to preserve freshness in fruits and vegetables. Alongside performance, branding is a major trend—manufacturers are adopting advanced digital printing platforms with UV-curable and eco-solvent inks to create high-definition graphics, tamper-evident labels, and QR codes that improve traceability and consumer engagement.

The market is also seeing a surge in smart packaging adoption, where integrated sensors and digital codes provide real-time data on freshness, origin, and cold chain conditions. Industry collaboration through the U.S. Plastics Pact is fostering a shift toward a circular economy for plastics, while paper-based alternatives and molded fiber trays are gaining traction to reduce plastic use. The growth of online grocery and e-commerce food delivery is another critical driver, creating demand for robust and insulated produce packaging capable of protecting perishables during last-mile delivery.

China: National Standards and Food Safety Regulations Defining Produce Packaging

China’s produce packaging market is being shaped by strict government oversight aimed at reducing waste and improving food safety. The General Administration of Customs of China (GACC) requires a Product Expiration Date for all imported goods, influencing labeling requirements on produce packaging. In addition, national standards restricting excessive packaging for edible agricultural products impose strict limits on the interspace ratio, number of layers, and cost share of packaging relative to product value. These standards are designed to curb waste and promote affordability while maintaining quality.

Food-contact safety is governed by the Food Safety Law (FSL) and its interim measures for food-related products, which require packaging materials to be safe, stable, and not alter food organoleptic properties. Combined with sustainability policies from the NDRC and MEE, these frameworks are pushing manufacturers toward lightweight, recyclable, and compliant packaging materials. The result is a market balancing food safety, consumer trust, and reduced material intensity, with growth supported by e-commerce and domestic consumption trends.

India: Make in India and Bioplastic Innovations Supporting Sustainable Produce Packaging

India’s produce packaging market is expanding under the government’s Make in India initiative, which promotes local manufacturing of packaging materials. The Food Safety and Standards Authority of India (FSSAI) plays a central role by enforcing stricter food labeling standards and organic produce guidelines, which require packaging to include clear, traceable information. Meanwhile, the Central Pollution Control Board (CPCB) enforces the Plastic Waste Management Rules (2016, amended 2022), emphasizing Extended Producer Responsibility (EPR) for packaging waste collection and recycling.

Collaborative initiatives like the India Plastics Pact, led by the Confederation of Indian Industry (CII) and WWF India, aim for 100% of plastic packaging to be reusable or recyclable by 2030. Innovation is also notable, with patents for bioplastics derived from dairy and agricultural waste—including ghee residue-based bioplastics that degrade in water and soil—highlighting India’s potential as a hub for sustainable packaging solutions. Rising consumer demand for eco-friendly, affordable produce packaging is driving investments in biodegradable trays, films, and compostable bags, particularly for use in modern retail and e-commerce grocery delivery.

United Kingdom: Plastic Packaging Tax and Food Waste Reduction Regulations Driving Change

The United Kingdom produce packaging market is led by regulatory and fiscal measures, especially the Plastic Packaging Tax (PPT) introduced in April 2022, which applies to packaging with less than 30% recycled plastic. This has created a clear incentive for retailers and suppliers to transition to recycled-content and recyclable materials. The government is further promoting recycling through a proposed deposit return scheme for plastic bottles and investment initiatives like the £60 million Smart Sustainable Plastic Packaging (SSPP) Challenge, which supports projects reducing plastic waste and developing novel recycling technologies.

The Food Standards Agency (FSA) has also implemented stricter guidelines for food labeling, requiring transparent display of “use by” and “best before” dates to combat food waste. Producers are increasingly investing in single-material, recyclable packaging to simplify recycling processes while maintaining protection and shelf life. These developments position the UK as a regulation-driven market, balancing sustainability, food safety, and consumer information in its produce packaging sector.

Brazil: Export Sensitivity and MAP Packaging Adoption Strengthening Market

Brazil is a leading global exporter of fresh produce, making its packaging sector highly sensitive to international trade agreements and phytosanitary regulations. Packaging plays a critical role in ensuring product quality during long-distance exports, leading to strong adoption of MAP and vacuum-sealed trays and films that extend shelf life and preserve freshness during transit. The country’s National Solid Waste Policy further pushes the industry toward recyclable and sustainable packaging options.

At the same time, the government is investing in improved waste reduction and recycling infrastructure to support compliance with global trade standards. While much of Brazil’s packaging innovation is linked to exports, rising domestic demand is also driving the use of eco-friendly and performance-oriented packaging in retail channels. However, challenges such as avian influenza outbreaks in the poultry sector have underscored the need for strict biosecurity and resilience across Brazil’s broader agri-food packaging industry. These dynamics establish Brazil as both a key exporter and sustainability-focused adopter of modern produce packaging solutions.

Produce Packaging Market Report Scope

Produce Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$37.3 Billion

|

|

Market Size (2034)

|

$55 Billion

|

|

Market Growth Rate

|

4.4%

|

|

Segments

|

By Material (Plastic, Paper & Paperboard, Molded Fiber, Bioplastics, Others), By Product Type (Trays, Bags & Pouches, Clamshells, Boxes & Cartons, Films & Wraps, Nets & Mesh Bags), By Application (Fruits, Vegetables, Salads & Fresh-Cut Produce, Horticulture), By Packaging Technique (MAP, Vacuum, Active & Intelligent, Protective Packaging)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Sealed Air Corporation, Smurfit Kappa Group Plc, Graphic Packaging Holding Company, DS Smith Plc, Sonoco Products Company, WestRock Company, Huhtamaki Oyj, International Paper Co., Pactiv Evergreen Inc., Uflex Ltd., Greif, Inc., Silgan Holdings Inc., Berry Global, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Produce Packaging Market Segmentation

By Material

- Plastic

- Paper & Paperboard

- Molded Fiber

- Bioplastics

- Others

By Product Type

- Trays

- Bags & Pouches

- Clamshells

- Boxes & Cartons

- Films & Wraps

- Nets & Mesh Bags

By Application

- Fruits

- Vegetables

- Salads & Fresh-Cut Produce

- Horticulture

By Packaging Technique

- MAP

- Vacuum

- Active & Intelligent

- Protective Packaging

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Produce Packaging Market

- Amcor plc

- Mondi Group

- Sealed Air Corporation

- Smurfit Kappa Group Plc

- Graphic Packaging Holding Company

- DS Smith Plc

- Sonoco Products Company

- WestRock Company

- Huhtamaki Oyj

- International Paper Co.

- Pactiv Evergreen Inc.

- Uflex Ltd.

- Greif, Inc.

- Silgan Holdings Inc.

- Berry Global, Inc.

* List Not Exhaustive

Methodology

The research methodology for the Produce Packaging Market leverages a comprehensive approach combining both primary and secondary research techniques to provide actionable insights for industry professionals. Primary research included structured interviews and consultations with key stakeholders, such as packaging manufacturers, logistics managers, retail and e-commerce operators, material scientists, sustainability experts, and regulatory authorities across North America, Europe, Asia-Pacific, and emerging markets. Secondary research involved detailed analysis of company reports, investor presentations, industry journals, trade publications, patents, and verified market studies, with a focus on sustainable materials, Modified Atmosphere Packaging (MAP), smart labeling, reusable crates, and bio-based films. USDAnalytics employed triangulation techniques to validate market sizing, CAGR forecasts, and segment distribution, integrating macroeconomic factors, regulatory frameworks, technological advancements, and supply chain dynamics. Both top-down and bottom-up approaches were utilized to cross-verify regional and global market projections. Competitive benchmarking and company profiling captured innovation pipelines, strategic collaborations, and operational efficiencies, ensuring a professional-grade and reliable market intelligence report for stakeholders seeking insights on produce packaging trends, sustainability initiatives, and emerging growth opportunities.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.