Packaging Machinery Market Set to Reach $121.3 Billion by 2034, Driven by Automation and Digital Transformation

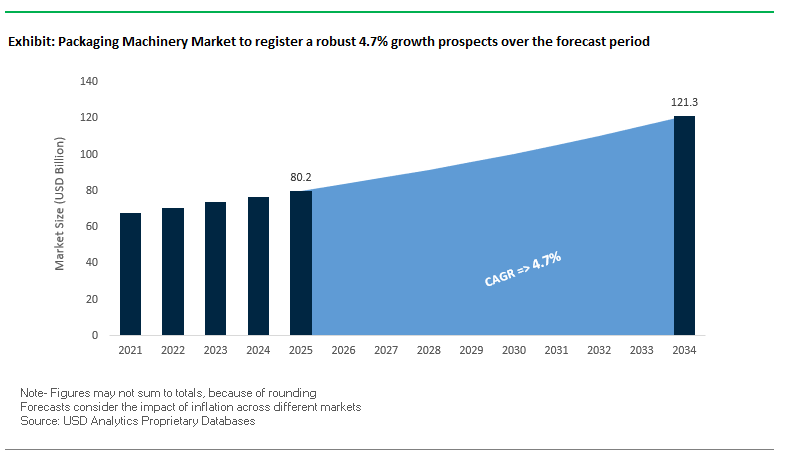

The Global Packaging Machinery Market is projected to grow from $80.2 billion in 2025 to $121.3 billion by 2034, at a CAGR of 4.7%. This growth reflects the industry’s pivotal role in modern manufacturing, enabling high-speed, efficient, and precise packaging across food, beverage, pharmaceutical, and consumer goods sectors. Packaging machinery ensures product safety, consistent quality, and operational efficiency, making it indispensable for companies seeking scalable and sustainable production.

Key Insights for Industry Stakeholders

- Automation and Robotics Integration: Increasing adoption of cobots, high-speed pick-and-place arms, and robotic handling systems to enhance efficiency, address labor shortages, and reduce operational errors.

- Digitalization and Smart Machinery: Use of AI, IoT, and machine learning for real-time monitoring, predictive maintenance, and process optimization, minimizing downtime and material waste.

- Flexible Machinery for Rapid Product Variation: Rising demand for machines adaptable to multiple formats, sizes, and materials, driven by e-commerce growth and consumer expectations for product variety.

- Sustainability and Resource Efficiency: Focus on eco-friendly packaging materials, energy-efficient machines, and waste reduction, aligning with global sustainability mandates.

- Regulatory and Compliance Alignment: Machines increasingly support environmental and safety regulations, enabling manufacturers to adopt recyclable and biodegradable packaging solutions.

The market is increasingly defined by technological sophistication, adaptability, and sustainable innovation, positioning it as a key enabler for global supply chain competitiveness.

Strategic Moves and Technological Innovations Driving Growth in Packaging Machinery

The Global Packaging Machinery Industry has experienced significant developments, driven by strategic mergers, technological innovation, and sustainability initiatives. In August 2025, Coesia acquired a majority stake in Autoware, a manufacturing software integrator, to enhance its digital transformation and smart manufacturing capabilities.

In July 2025, the all-stock combination of Amcor and Berry Global Group completed, influencing machinery demand for expanded product portfolios. June 2025 saw Tetra Pak open a new food technology center in Sweden, facilitating commercial scale-up of fermentation-derived foods and specialized packaging machinery. In May 2025, Krones AG reported robust profitability, highlighting resilience in a challenging macroeconomic environment.

Strategic consolidation continued with International Paper completing its $9.9 billion acquisition of DS Smith in April 2025, boosting demand for machinery compatible with paper-based solutions. In March 2025, Syntegon launched the MLD Advanced for ready-to-use nested syringes, integrating robotics with proven technologies to meet high pharmaceutical production demands. Earlier milestones include Smurfit Kappa’s acquisition of WestRock in November 2024 and Syntegon’s SVX Compact launch in September 2024, emphasizing ultra-compact, high-speed packaging capabilities.

Trends and Opportunities Defining the Future of the Packaging Machinery Market

Strategic Reshoring Driving Investment in High-Speed, Automated Packaging Lines in North America

The packaging machinery market is being reshaped by the wave of reshoring and foreign direct investment (FDI) in North America, as manufacturers prioritize local-for-local strategies. In 2024, U.S. reshoring and FDI projects accounted for 244,000 announced jobs, making it the second-highest year on record. This momentum is fueled by policy incentives like the Inflation Reduction Act (IRA) and the CHIPS and Science Act, which are catalyzing large-scale investments in semiconductors, EV batteries, and clean energy. These new facilities require highly automated, high-speed packaging lines to ensure productivity and cost-competitiveness. Beyond policy, supply chain vulnerabilities exposed during the pandemic—ranging from ocean freight volatility to geopolitical disruptions—have accelerated the trend toward domestic production. Large corporations are leading the charge, with Taiwan Semiconductor Manufacturing Company (TSMC) investing nearly $150 billion in U.S. facilities over the past three years, creating a ripple effect for demand in advanced packaging and automation systems. As companies prioritize operational resilience and faster go-to-market timelines, automation-rich packaging machinery is becoming the backbone of North America’s manufacturing resurgence.

Integration of AI-Powered Machine Vision for Zero-Defect Packaging and Predictive Maintenance

The second key trend is the integration of AI and machine vision technologies into packaging machinery, transforming how quality and uptime are managed. Traditionally, machine vision was reactive—detecting defects post-production. Today, advanced AI-enabled systems proactively prevent defects by identifying process patterns and triggering real-time adjustments, moving manufacturers closer to the “zero-defect” benchmark. Predictive maintenance powered by IoT sensors and machine learning further reduces costly downtime, as demonstrated in academic studies where predictive models for film bag and paste packaging machines successfully forecasted malfunctions. AI also enables granular root cause analysis, correlating defects like seal failures with operational conditions such as ambient temperature or line speed. Additionally, AI systems now handle subjective quality assessments, such as fold straightness or logo placement, that once required human judgment. In sectors like consumer electronics, deep learning models are ensuring brand consistency at scale. Together, these innovations demonstrate that AI-driven packaging machinery is not only enhancing efficiency but also redefining quality assurance in global supply chains.

Development of Modular, Retrofittable Automation Solutions for Small and Medium Enterprises (SMEs)

One of the most compelling growth opportunities in the packaging machinery market lies in the development of modular, retrofittable automation systems tailored for SMEs. Unlike large corporations with fully automated lines, SMEs often face budgetary and technical barriers. Collaborative robots (cobots) are emerging as an entry point, enabling automation in tasks like carton erecting, pick-and-place, and palletizing without requiring complex infrastructure. Companies such as KUKA and Universal Robots highlight how cobots can be safely integrated into existing workflows, offering cost-effective automation. To lower adoption barriers, manufacturers are releasing “plug-and-play” systems like Schubert’s Lightline series, which are pre-configured for standard packaging functions and require minimal setup. Ease of programming is also a priority—many cobots now support manual “teach-by-demonstration” programming, allowing operators with no coding background to configure them. For SMEs handling high-mix, low-volume production, modular machines with quick-changeover capabilities provide the flexibility needed to remain competitive. This modularization trend positions SMEs to gradually scale their automation investments, making packaging machinery more accessible and adaptable across diverse industries.

Machinery for the Circular Economy: Automated Systems for Cleaning and Refilling Reusable Packaging

The transition toward a circular economy is unlocking new opportunities for automated machinery dedicated to cleaning, sanitizing, and refilling reusable packaging. Unlike conventional packaging equipment, these systems are designed for reverse logistics—processing returned containers for reuse. The Reusable Packaging Association (RPA) spotlighted this trend at PACK EXPO Las Vegas 2025, showcasing innovations that could underpin large-scale adoption of reuse models. Brand-level commitments are accelerating this opportunity: Unilever has piloted over 50 refill and reuse projects globally since 2018, including initiatives in Indonesia that tested manual refill stations serving thousands of customers. Insights from these pilots are informing the next generation of automated systems capable of scaling reuse models efficiently. The economic potential is equally strong—according to the United Nations Environment Programme (UNEP), shifting just 20% of single-use packaging to reusable systems could unlock $10 billion in economic value globally. Automated cleaning and refilling machinery is central to achieving this shift, enabling cost savings, sustainability gains, and enhanced consumer engagement with reuse ecosystems.

Competitive Landscape: Leading Players Advancing Automation, Sustainability, and Smart Packaging

The packaging machinery industry is driven by companies leveraging automation, digitalization, and innovation to provide high-performance, sustainable solutions. The following leaders are shaping market dynamics:

Krones AG: Enhancing High-Speed Filling and Labeling with Sustainable Solutions

Krones AG is a global leader in filling and packaging lines, particularly for the beverage and liquid food sectors. In H1 2025, it reported an EBITDA margin of 10.6% and maintained an order backlog of €4.29 billion, providing high visibility into 2026. Krones offers rinser-fillers, labelers, bottle washers, and inspection systems, including its Contiroll labeler and Dynafill filling technology, combining speed and precision. The company emphasizes resource-efficient machinery and integration with eco-friendly packaging materials.

Syntegon Technology GmbH: Delivering Integrated Automation for Pharmaceutical and Food Packaging

Syntegon provides complete packaging solutions with a focus on automation and digital services. In March 2025, it introduced the MLD Advanced for ready-to-use syringes, and in October 2024, it acquired Telstar to strengthen its vial filling portfolio. Its offerings include filling and dosing machines, robotic pick-and-place systems, and end-of-line case packers, enhancing production efficiency. Syntegon is committed to digitalization, predictive maintenance, and sustainable packaging innovations.

Coesia Group: Expanding Smart Manufacturing Capabilities Through Strategic Acquisitions

Coesia specializes in automated machinery across consumer goods, healthcare, and industrial sectors. In August 2025, it acquired a majority stake in Autoware, strengthening its digital transformation capabilities. Coesia offers machines for filling, cartoning, wrapping, and pouching, with brands like Acma and G.D renowned for specialized solutions. The company focuses on highly automated, tech-driven solutions that improve operational efficiency and sustainability.

Marchesini Group S.p.A.: Driving Innovation in Pharmaceutical and Cosmetic Packaging

Marchesini Group provides complete packaging lines for pharmaceutical and cosmetic products. It invests heavily in Industry 4.0 workforce development and R&D to create high-performance machines. Offerings include blister packaging, vial and ampoule filling, and serialization systems. Marchesini emphasizes customized solutions and global service, ensuring compliance with stringent pharmaceutical regulations.

Tetra Pak International S.A.: Integrating Food Processing and Sustainable Packaging Machinery

Tetra Pak is a pioneer in liquid food processing and packaging. In June 2025, it opened a new food technology center in Sweden, supporting the scale-up of fermentation-derived foods. Its machinery, such as the Tetra Pak E3/Speed Hyper, can produce up to 40,000 packages per hour, and the company is advancing paper-based barrier alternatives to aluminum foil for sustainable aseptic packaging. Tetra Pak’s strategy focuses on safe, environmentally responsible, and innovative packaging solutions.

Packaging Machinery Market Share Insights, 2025-2034

Automatic Machinery Dominates Market Share by Technology in the Packaging Machinery Industry

Automatic packaging machinery holds the commanding 65% share of the global packaging machinery market, underscoring the industry’s decisive pivot toward full automation. This dominance is fueled by manufacturers’ urgent need to achieve high-volume throughput, superior precision, and regulatory compliance while reducing operational costs. Automatic systems seamlessly integrate with Industry 4.0 platforms, IoT-enabled sensors, and predictive maintenance tools, allowing production facilities to optimize uptime and minimize defects. Their scalability makes them indispensable for high-capacity operations in food, pharmaceuticals, and consumer goods, where consistency, speed, and hygiene standards are critical. While semi-automatic machinery remains relevant for SMEs and pilot lines requiring flexibility, and manual systems persist only in artisanal or low-volume production, the future trajectory of the industry is anchored in robotics-integrated automation that ensures adaptability to changing product lines and sustainability requirements.

Food & Beverage Industry Leads Market Share by End-User in the Packaging Machinery Market

The food and beverage industry accounts for 45% of packaging machinery demand, making it the largest end-user by a wide margin. This leadership is driven by the enormous production scale, diverse packaging formats, and compliance with global food safety regulations. High-speed filling, capping, labeling, and palletizing machinery are vital to maintain efficiency in sectors ranging from dairy and beverages to frozen foods and ready-to-eat meals. Moreover, the rise of modified atmosphere packaging (MAP) and portion-controlled packs has amplified the need for advanced machinery capable of preserving freshness and extending shelf-life. Pharmaceutical and healthcare companies represent the next most value-intensive segment, demanding ultra-precise, sterile, and serialized packaging systems. Meanwhile, e-commerce logistics is emerging as the fastest-growing application area, requiring automated secondary and tertiary solutions such as case erectors, parcel sorters, and right-sized packaging equipment. Cosmetics and personal care industries further reinforce demand for flexible, aesthetically focused machinery, highlighting how food and beverage’s scale-driven dominance is complemented by innovation-led adoption across other sectors.

United States Packaging Machinery Market Boosted by CHIPS Act Investments and AI Integration

The United States packaging machinery market is benefitting from major federal initiatives such as the National Advanced Packaging Manufacturing Program (NAPMP), part of the CHIPS for America program. With up to $1.6 billion allocated for R&D, this initiative is accelerating the development of high-tech semiconductor packaging, directly increasing demand for precision machinery capable of handling advanced processes. At the state level, supportive policies and sustainability regulations are further encouraging the adoption of machinery designed for recyclable and automation-ready packaging formats.

Technological progress is centered on automation and AI-enabled packaging lines, with rising demand for fully automatic systems that enhance speed, reduce labor costs, and improve consistency. AI-driven predictive maintenance and real-time quality control are helping manufacturers minimize downtime while maintaining compliance with stringent food and pharmaceutical safety standards. Companies such as BW Packaging Systems expanded U.S. operations in 2024 to meet growing demand, reflecting the industry’s shift toward advanced machinery solutions. Strong demand continues across e-commerce, food and beverage, and pharmaceuticals, with flexible and sterile packaging machinery essential for product safety, traceability, and efficient last-mile logistics.

Germany Packaging Machinery Market Strengthened by PPWR and Export Leadership

Germany’s packaging machinery market is shaped by the EU Packaging and Packaging Waste Regulation (PPWR) and the expanded German Packaging Act (VerpackG), both of which enforce ambitious targets for recyclability and reuse. These rules are driving innovation in machinery capable of processing sustainable materials and supporting circular economy packaging systems.

Germany continues to lead in engineering excellence, with machinery designed to be energy-efficient, modular, and capable of fast changeovers to accommodate diverse formats. This versatility ensures compliance with EU regulations while maintaining high productivity. Germany also remains a top global exporter of packaging machinery, particularly for food and beverage applications, reinforcing its role as a benchmark for quality and innovation. Strongest demand is seen for filling, labeling, and form-fill-seal (FFS) systems, where precision, hygiene, and traceability are essential for both domestic and international markets.

China Packaging Machinery Market Accelerated by Made in China 2025 and E-Commerce Growth

The packaging machinery market in China is advancing rapidly under the Made in China 2025 strategy, which prioritizes digital and intelligent manufacturing. Government backing, alongside heavy capital investment, is driving the country’s transition from low-end to mid- and high-end automated machinery, supporting higher efficiency, flexibility, and sustainability in packaging.

Chinese manufacturers are scaling production capacity and investing in R&D to deliver competitive, intelligent machinery, resulting in the country now holding approximately 35% of the global packaging machinery market. With domestic players leveraging economies of scale, China’s market is also expanding internationally. Demand is particularly high across consumer goods, e-commerce, and food and beverage sectors, with parcel volumes exceeding 175 billion units in 2024 fueling massive need for automation-ready machinery. This scale positions China as one of the fastest-growing hubs for high-speed packaging equipment globally.

India Packaging Machinery Market Supported by Make in India and Smart Packaging Growth

India’s packaging machinery market is being propelled by Make in India and the Production Linked Incentive (PLI) scheme, which encourage domestic manufacturing and self-reliance. These policies are spurring investments in advanced packaging lines and expanding India’s industrial base. The Ministry of Food Processing Industries (MoFPI) also supports packaging demand by funding the expansion and upgrading of food processing units, which depend on modern packaging machinery for compliance and safety.

The market is experiencing rapid adoption of automation, robotics, and AI-enabled packaging systems, designed to improve efficiency, reduce costs, and minimize human error. The demand is particularly high in food, beverage, and pharmaceutical packaging, with form-fill-seal (FFS) machines gaining traction for their ability to handle diverse materials and formats. With the growth of online retail and convenience packaging, India is emerging as a key regional hub for packaging machinery innovation and deployment.

Japan Packaging Machinery Market Advanced by Positive List Rules and IoT-Enabled Systems

Japan’s packaging machinery market is being reshaped by the introduction of the positive list system for food-contact materials in June 2025. This regulation is influencing machinery design, requiring equipment that can process compliant substrates and maintain safety standards for food and beverage packaging.

Japan is a global leader in precision packaging technologies, with innovation centered on robotics, IoT-enabled machinery, and advanced automation. These systems are designed to enhance safety, traceability, and real-time monitoring in packaging operations. With a strong emphasis on quality and R&D, Japanese packaging machinery is recognized worldwide for its precision and durability. Demand is concentrated in food, beverage, and pharmaceuticals, with sterile and accurate packaging increasingly important in the healthcare sector. Japan’s focus on automation and sustainability positions it at the forefront of the global packaging machinery landscape.

Brazil Packaging Machinery Market Driven by PNRS Recycling Mandates and Food Sector Demand

Brazil’s packaging machinery market is being shaped by the National Solid Waste Policy (PNRS), with 2025 regulations placing greater responsibility on manufacturers and consumers for sustainable end-of-life management. These rules are fueling demand for machinery that can process recyclable and reusable materials, ensuring compliance with national sustainability standards.

Technological advancements in Brazil are focused on equipment capable of handling sustainable packaging materials and meeting international food safety certifications. Corporate investments are being made to modernize facilities and adopt new machinery aligned with PNRS requirements. Demand is strongest in the food and beverage sector, where Brazil’s role as a major producer of canned and processed goods necessitates reliable filling, sealing, and labeling machinery. The push for both safety and sustainability is positioning Brazil as a rapidly evolving packaging machinery market in Latin America.

Packaging Machinery Market Report Scope

Packaging Machinery Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$80.2 Billion

|

|

Market Size (2034)

|

$121.3 Billion

|

|

Market Growth Rate

|

4.7%

|

|

Segments

|

By Machine Type (Filling, FFS, Labeling & Coding, Cartoning, Wrapping & Bundling, Palletizing & Case Packing, Others), By Technology (Automatic, Semi-automatic, Manual), By End-Use Industry (Food & Beverage, Pharmaceutical & Healthcare, Cosmetics & Personal Care, E-commerce & Logistics, Other Industrial Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Krones AG, Barry-Wehmiller Companies, Inc., Coesia S.p.A., Syntegon Technology GmbH, ProMach, Inc., Tetra Pak, KHS Group, Mondi Group, IMA S.p.A., Sidel Group, MULTIVAC Group, Marchesini Group S.p.A., Duravant LLC, Fuji Machinery Co., Ltd., Ishida Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Packaging Machinery Market Segmentation

By Machine Type

- Filling

- FFS

- Labeling & Coding

- Cartoning

- Wrapping & Bundling

- Palletizing & Case Packing

- Others

By Technology

- Automatic

- Semi-automatic

- Manual

By End-Use Industry

- Food & Beverage

- Pharmaceutical & Healthcare

- Cosmetics & Personal Care

- E-commerce & Logistics

- Other Industrial Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Packaging Machinery Market

- Krones AG

- Barry-Wehmiller Companies, Inc.

- Coesia S.p.A.

- Syntegon Technology GmbH

- ProMach, Inc.

- Tetra Pak

- KHS Group

- Mondi Group

- IMA S.p.A.

- Sidel Group

- MULTIVAC Group

- Marchesini Group S.p.A.

- Duravant LLC

- Fuji Machinery Co., Ltd.

- Ishida Co., Ltd.

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous and integrated research methodology to deliver comprehensive insights into the Global Packaging Machinery Market. Our approach combines primary research, including in-depth interviews with packaging machinery manufacturers, system integrators, technology providers, and end-users across food, beverage, pharmaceutical, e-commerce, and consumer goods sectors, with extensive secondary research using company reports, trade journals, patents, regulatory filings, and industry publications. Quantitative analysis is applied to calculate market size, growth projections, and CAGR from 2025 to 2034, incorporating factors such as machine type, automation level, and end-use demand. Our methodology evaluates technological trends including AI-powered machine vision, robotics, modular automation, digitalization, predictive maintenance, and circular economy-enabled machinery. Regional analysis spans North America, Europe, China, India, Japan, and Brazil, assessing policy drivers, regulatory compliance, sustainability mandates, and investment initiatives influencing market dynamics. USDAnalytics also examines competitive strategies, strategic mergers and acquisitions, and product innovation to provide actionable insights for strategic planning, operational optimization, and investment decisions. By synthesizing these elements, our research delivers an authoritative, market-ready perspective for industry professionals navigating technological transformation, automation adoption, and sustainability-driven packaging solutions.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.