Blister Packaging Market Overview: Protection, Sustainability, and Cold-Forming Dominance

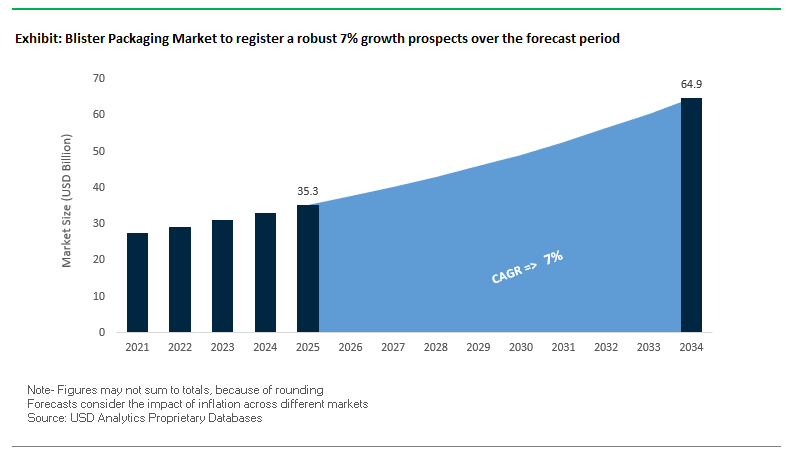

The Global Blister Packaging Market is forecasted to grow from $35.3 billion in 2025 to $64.9 billion by 2034, expanding at a CAGR of 7%. The growth trajectory reflects the critical role blister packaging plays in pharmaceuticals, healthcare, and nutraceuticals, where tamper-evident and unit-dose protection ensures product integrity and safety. Beyond its protective features, blister packaging is increasingly viewed as a medium for brand differentiation, especially in over-the-counter (OTC) and nutraceutical segments. The industry is undergoing a major shift toward sustainable materials, with innovations that reduce reliance on PVC and aluminum while enhancing recyclability.

Key Insights Driving Market Growth:

- Superior Protection: Blister packs offer tamper-evident features and unit-dose precision, reducing counterfeiting risks in pharma.

- Cold Forming’s Leadership: Cold-formed blisters dominate sensitive drug packaging due to their strong barrier protection against oxygen, light, and moisture.

- Sustainability Push: 67% of consumers prefer eco-friendly packaging, driving adoption of recyclable, bio-based, and PVC-free materials.

- Premium Branding: Nutraceuticals and OTC brands are increasingly investing in graphic-rich blister packs to elevate the unboxing and retail experience.

Market Analysis: Strategic Developments Driving the Blister Packaging Industry

Recent industry movements reflect the dual forces of sustainability innovation and strategic investments shaping the blister packaging landscape. In August 2025, Klöckner Pentaplast was recognized with the German Packaging Award for its kp 100% Tray2Tray® innovation, demonstrating leadership in circular economy materials. That same month, Constantia Flexibles announced a €100 million investment to strengthen its sustainable packaging portfolio, while Huhtamaki secured an EcoVadis gold medal for the fifth year in a row, underlining its corporate sustainability leadership.

Innovation momentum continued in July 2025, when Klöckner Pentaplast launched kp Elite® Nova, a next-generation MAP tray optimized for the food industry. Earlier, in April 2025, Pactiv Evergreen introduced its Recycleware® Reduced-Density Polypropylene (RDPP) trays, aligned with the Association of Plastic Recyclers’ standards. Additionally, Constantia Flexibles (March 2025) joined forces with Aluflexpack AG to reinforce its leadership in premium flexible and blister laminates.

Technology partnerships have also defined the market trajectory. Tekni-Plex Healthcare (January 2024), together with Alpek Polyester, developed the world’s first pharmaceutical-grade PET blister film with post-consumer recycled content, showcased at Pharmapack 2024. Meanwhile, Amcor (February 2025) collaborated with Flügger to introduce a container with 50% recycled content, highlighting cross-sector partnerships aimed at sustainability.

Key Market Trends and Emerging Opportunities Driving the Blister Packaging Industry

Mandated Adoption of Anti-Counterfeiting and Serialization Features

Global pharmaceutical regulations are compelling blister packaging manufacturers to integrate advanced anti-counterfeiting and serialization systems. The U.S. Drug Supply Chain Security Act (DSCSA) and the European Union’s Falsified Medicines Directive (FMD) require unique serial numbers on each unit, enabling end-to-end traceability. Blister packs now incorporate 2D Data Matrix codes containing GTIN, serial numbers, lot numbers, and expiration dates, ensuring products are verifiable throughout the supply chain. Compliance with these mandates involves significant investment in high-resolution cameras, precision lighting, and integrated vision systems for automated code verification, allowing manufacturers to prevent counterfeit medicines effectively. This trend is driving the adoption of advanced technologies in pharmaceutical packaging and positions serialized blister packs as critical tools for patient safety and regulatory adherence.

Strategic Shift Towards Recyclable Mono-material Polypropylene (PP) Blisters

Facing regulatory pressures from Extended Producer Responsibility (EPR) schemes and brand sustainability goals, the blister packaging market is rapidly transitioning from multi-material PVC/PVDC packs to recyclable mono-material polypropylene (PP) solutions. PVC-aluminum laminates, which account for roughly 70% of global pharmaceutical blister usage, are difficult to recycle due to their multi-layer composition. Innovative collaborations, including Etimex Primary Packaging, Perlen Packaging, and Faller Packaging, have developed mono-material PP blister packs that simplify recycling. European regulations, such as the Packaging and Packaging Waste Regulation (PPWR), further drive adoption, exemplified by SÜDPACK Medica’s NutriGuard solution. Concepts like the One-Material Blister (OMB), where both the bottom and lidding films use the same polymer, streamline the recycling process and reinforce circular economy initiatives, aligning with sustainability and corporate responsibility goals.

Development of High-Barrier, Compostable Polymer Blisters

A significant growth opportunity exists in creating fully compostable blister films that maintain critical moisture and oxygen barrier properties for pharmaceuticals and nutraceuticals. Existing biodegradable solutions often fail under real-world supply chain conditions, highlighting the need for high-performance compostable alternatives. Industry leaders and academic researchers are actively developing next-generation materials, such as paper-based compostable films and PLA sheets, which can withstand handling, transport, and storage while remaining environmentally friendly. The adoption of truly compostable blisters addresses mounting concerns over end-of-life pharmaceutical waste, particularly for nutraceutical products, and provides a sustainable alternative to conventional blister packs.

Integration of Smart Blister Packs for Enhanced Patient Adherence

The integration of smart technology into blister packs is transforming patient adherence monitoring and digital healthcare solutions. Embedded sensors, NFC tags, and other electronics allow real-time tracking of pill removal, offering accurate adherence data for clinical trials and healthcare providers. Studies show discrepancies between self-reported adherence and data captured by electronic smart blister packages, highlighting the importance of these innovations. Smart blister packs, such as those developed by Schreiner MediPharm, can transmit dosing data to mobile applications, providing patients with customized reminders, medication history tracking, and enhanced support. This integration of smart packaging not only improves patient care but also generates valuable insights for pharmaceutical companies and research institutions.

Competitive Landscape: Leading Companies in Global Blister Packaging

The blister packaging market is highly competitive, with global players leveraging material science, sustainability investments, and advanced manufacturing to retain market share.

Amcor plc advancing recycle-ready blister solutions

Amcor leads with innovative blister technologies such as AmSky, a PVC- and aluminum-free, recycle-ready polyethylene blister system. The company focuses on eliminating non-recyclable materials, aligning with its goal of making all packaging recyclable or reusable by 2025. With operations in 40+ countries, Amcor offers unmatched global-local integration for pharmaceutical and nutraceutical brands.

Klöckner Pentaplast Group pioneering recyclable rigid films

Klöckner Pentaplast (kp) specializes in rigid films for pharma blister packaging, with solutions like kpNext™ and PENTAPHARM® films. Its kpNext™ R1 film provides a recyclable, transparent alternative compatible with existing lines, enabling seamless adoption. The company’s German Packaging Award (August 2025) for kp 100% Tray2Tray® underlines its material innovation leadership.

Constantia Flexibles Group GmbH expanding cold-form foil sustainability

Constantia Flexibles delivers high-barrier laminates and foils critical for blister packaging. Its REGULA CIRC cold-form foil, launched as a PE-based recyclable solution, reduces reliance on PVC. Strategic expansions, including a March 2025 partnership with Aluflexpack AG, strengthen its premium flexible packaging leadership.

Huhtamaki Oyj innovating with mono-PET blister lids

Huhtamaki offers the Push Tab® blister lid, a 100% mono-PET, aluminum- and PVC-free innovation that is fully recyclable. Recognized with sustainability awards, Huhtamaki is positioning itself as the first-choice supplier for sustainable blister packaging solutions. Its global presence and EcoVadis gold recognition (July 2025) reaffirm its leadership in circular packaging systems.

Tekni-Plex Healthcare first-to-market with recycled-content blister films

Tekni-Plex Healthcare focuses on thermoformable blister barrier films and lidding foils for pharmaceuticals. Its Teknilid Push, an all-polyester recyclable lidding, represents a breakthrough in recyclable pharma packaging. Collaborations like its PET blister film with PCR content (January 2024) highlight its commitment to pushing the boundaries of material science in healthcare packaging.

Blister Packaging Market Share Insights

Thermoform Blister Packaging Holds the Largest Market Share by Product Type

Thermoform blister packaging dominates the blister packaging industry with a commanding 70% share, underscoring its versatility and scalability. Its widespread use in the global pharmaceutical industry where over 80% of solid oral doses (pills, capsules, tablets) are blister packed in regions like Europe and Asia drives this dominance. Thermoforming allows manufacturers to tailor cavity design, combine plastics like PVC with barrier films such as PVDC, PCTFE, or Aclar®, and achieve an optimal balance of clarity, barrier protection, and cost efficiency. Beyond pharma, thermoformed blisters serve consumer goods and electronics, leveraging their tamper-evident design and peg-hole retail display adaptability. High production speeds, relatively low tooling costs, and compatibility with high-volume packaging lines consolidate their dominance, while ongoing innovations in recyclable PET-based blisters aim to mitigate sustainability criticisms.

Pharmaceuticals Secure the Largest Market Share by End-Use Industry in Blister Packaging

Pharmaceuticals account for 65% of blister packaging demand, making this end-use segment the indisputable driver of global market growth. Blisters deliver critical advantages that align directly with regulatory and patient compliance requirements: unit-dose convenience, tamper evidence, extended shelf life through superior moisture and oxygen barriers, and compatibility with serialization for global track-and-trace mandates. Regions like Europe, where over 85% of oral solid pharmaceuticals are dispensed in blister packs, anchor this dominance, with Asia-Pacific markets rapidly following suit due to growing generic drug production. Rising chronic disease prevalence and the surge in biologics and high-potency APIs further intensify the need for advanced blister formats, including cold-form aluminum blisters. Pharmaceutical companies also prefer blisters over bottles for supply chain optimization, as they reduce dispensing errors and enhance adherence, solidifying the pharmaceutical sector as the unrivaled engine of blister packaging growth.

United States: Sustainability and Regulatory Compliance Driving Advanced Blister Packaging

The U.S. blister packaging market is evolving rapidly under the influence of strict regulations, sustainability trends, and technological innovations. States like California are implementing laws such as the Plastic Pollution Prevention and Packaging Producer Responsibility Act (SB 54), promoting the adoption of recyclable and reusable blister packaging solutions. Industry leaders like Amcor plc are pioneering polyethylene-based thermoform systems that eliminate PVC and aluminum, providing environmentally sustainable alternatives.

Technological advancements are enhancing product security and traceability, with the U.S. Drug Supply Chain Security Act (DSCSA) driving the integration of barcodes and RFID tags to prevent counterfeiting. The pharmaceutical sector remains a key application area, particularly with the growing need for home-based chronic disease treatments, which require user-friendly, single-dose blister packs. Additionally, corporate initiatives such as Placon’s inert trays for food products highlight the trend toward transparent, functional, and regulatory-compliant blister packaging. FDA regulations on tamper-evident and child-resistant packaging further shape product design, emphasizing consumer safety and integrity.

Germany: Circular Economy Leadership and Technological Integration Enhancing Blister Packaging

Germany’s blister packaging market is shaped by a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR) effective February 2025. These regulations create a strong demand for eco-friendly, fully recyclable packaging. Germany’s Packaging Act (Verpackungsgesetz) emphasizes producer responsibility throughout the packaging lifecycle, reinforcing innovation in highly recyclable and sustainable materials.

Technological advancements are significant in the German market, with manufacturers embedding oxygen-barrier labels that integrate unique device identification (UDI) data to maintain drug stability and ensure compliance with the EU Medical Device Regulation (MDR). Sustainability initiatives are further highlighted by Gerresheimer AG, which launched a glass jar with bio-based forewood closure in February 2024, reflecting a growing focus on environmentally responsible packaging solutions for the pharmaceutical sector.

China: Green Policies and Automation Fuel Blister Packaging Market Expansion

China’s blister packaging market is benefiting from government initiatives aligned with the “dual carbon” goal, which encourages eco-friendly, reusable, and sustainable packaging materials. Policies restricting non-degradable plastics are spurring innovation in recyclable laminates. Chinese manufacturers are investing in automation and AI technologies, leveraging 5G and industrial internet integration to enhance production efficiency and flexible manufacturing.

The rapid growth of domestic e-commerce platforms is creating strong demand for secure, tamper-proof, and durable blister packaging, particularly in electronics, medical supplies, and pharmaceutical sectors. Regulatory reforms by the National Medical Products Administration (NMPA), including updated Good Manufacturing Practices (GMP) for Drugs issued in June 2025, are driving manufacturers to maintain comprehensive quality management systems, ensuring product safety, compliance, and reliability in the Chinese market.

India: Government Support and Pharmaceutical Demand Driving Blister Packaging Adoption

India’s blister packaging market is witnessing strong growth due to government programs like “Make in India” and “Zero Effect Zero Defect”, which encourage high-quality domestic production. The Production Linked Incentive (PLI) Scheme, with an outlay of INR 10,900 crore, is fostering enhanced manufacturing capabilities, driving the production of standardized, high-quality blister packaging solutions.

Rising disposable incomes and urbanization are shifting consumer preferences toward convenient, single-serve, and on-the-go products, boosting the adoption of blister packs. India’s pharmaceutical and healthcare sectors are expanding, driven by an aging population and increasing chronic disease prevalence, creating strong demand for secure, tamper-evident, and child-resistant blister packaging. Additionally, eco-friendly alternatives are gaining traction due to Plastic Waste Management (Amendment) Rules, reinforcing the market’s focus on sustainability and regulatory compliance.

Blister Packaging Market Report Scope

Blister Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$35.3 Billion

|

|

Market Size (2034)

|

$64.9 Billion

|

|

Market Growth Rate

|

7%

|

|

Segments

|

By Product Type (Thermoform Blister Packaging, Cold Form Blister Packaging, Clamshell Packaging), By Material Type (Plastic Films, Aluminum, Paper & Paperboard, Bioplastics), By Technology (Thermoforming, Cold Forming), By End-Use Industry (Pharmaceuticals, Consumer Goods, Food & Confectionery, Medical Devices, Industrial Goods)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, WestRock Company, Constantia Flexibles, Klöckner Pentaplast, Sonoco Products Company, Huhtamaki Oyj, Tekni-Plex, Inc., Honeywell International Inc., Sealed Air Corporation, DNP (Dai Nippon Printing Co., Ltd.), Bilcare Ltd., ACG, Uhlmann Pac-Systeme GmbH & Co. KG, Romaco Group, Gerresheimer AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Blister Packaging Market Segmentation

By Product Type

By Material Type

- Plastic Films

- Aluminum

- Paper & Paperboard

- Bioplastics

By Technology

- Thermoforming

- Cold Forming

By End-Use Industry

- Pharmaceuticals

- Consumer Goods

- Food & Confectionery

- Medical Devices

- Industrial Goods

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Blister Packaging Market

- Amcor plc

- WestRock Company

- Constantia Flexibles

- Klöckner Pentaplast

- Sonoco Products Company

- Huhtamaki Oyj

- Tekni-Plex, Inc.

- Honeywell International Inc.

- Sealed Air Corporation

- DNP (Dai Nippon Printing Co., Ltd.)

- Bilcare Ltd.

- ACG

- Uhlmann Pac-Systeme GmbH & Co. KG

- Romaco Group

- Gerresheimer AG

* List Not Exhaustive

Methodology

USDAnalytics conducted a comprehensive study of the global Blister Packaging Market by combining primary and secondary research to deliver actionable insights for industry professionals. The methodology included interviews with packaging manufacturers, pharmaceutical and nutraceutical companies, and supply chain experts, alongside analysis of company reports, regulatory publications, sustainability frameworks, and industry news. Market sizing and growth projections were determined using historical trends, innovations in thermoform and cold-form blister technologies, and the increasing adoption of recyclable, mono-material, and compostable solutions. Segmentation was analyzed by product type, material, technology, and end-use industry, while competitive intelligence assessed strategic investments, partnerships, M&A activity, and technological developments by leading companies such as Amcor, Klöckner Pentaplast, Constantia Flexibles, Huhtamaki, and Tekni-Plex. Special attention was given to anti-counterfeiting, serialization, patient adherence solutions, and sustainability initiatives, ensuring the analysis captures evolving regulatory frameworks, circular economy strategies, and premium branding opportunities, providing a holistic view of market dynamics and emerging growth avenues.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.