Circular Packaging Market Overview- Recycled Content Mandates and Sustainable Innovation

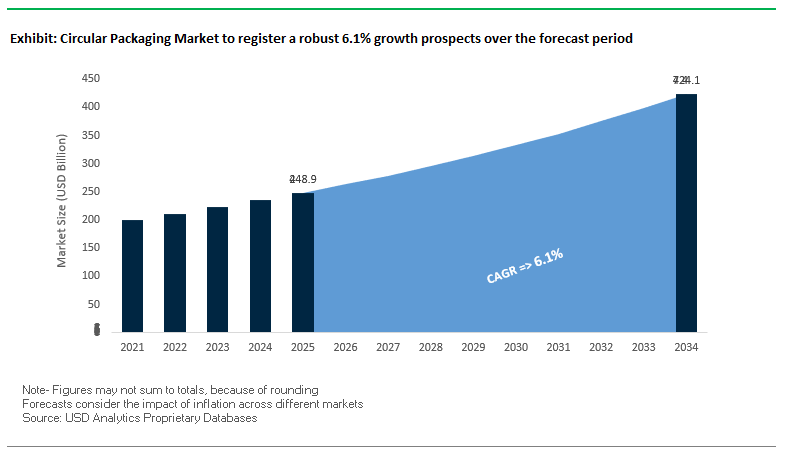

The global circular packaging market is projected to expand from USD 248.9 billion in 2025 to USD 424.1 billion by 2034, growing at a CAGR of 6.1%. This growth is primarily fueled by stringent regulatory mandates requiring recycled content, rising consumer preference for eco-friendly materials, and technological innovation in fiber-based and mono-material solutions. Circular packaging is no longer limited to traditional recycling; it integrates closed-loop systems, design for recyclability, and material efficiency as central pillars of growth.

Paper-based innovation is gaining traction as companies accelerate the “paperization” trend, developing fiber-based alternatives for applications ranging from laundry pods to beverage multipacks. At the same time, the infinite recyclability of aluminum and the improved recyclability of mono-material plastics highlight how material science advancements are shaping the future of packaging. For industry professionals, success depends on adapting portfolios to meet global policy shifts and aligning design with sustainability standards without compromising performance.

Key Insights for Professionals

- Recycled content mandates in EU & U.S. driving demand for rPET, recycled paper, and aluminum.

- Paperization trend replacing single-use plastics with fiber-based innovations.

- Closed-loop aluminum reduces energy demand by 95% compared to virgin production.

- Design for recyclability emerging as a key performance indicator for packaging success.

Market Analysis: Policies and Industry Developments Accelerate Transition to Circular Packaging

The circular packaging market is being reshaped by new regulations, mergers, and product launches that emphasize sustainability, recyclability, and innovation.

In August 2025, Mondi Group introduced FunctionalBarrier Paper Ultimate, a high-barrier paper-based solution that enhances recyclability while maintaining product protection, reflecting the strong momentum toward fiber-based replacements for plastics. In the same month, Graphic Packaging International launched a child-resistant paperboard pack for laundry pods, an innovation that highlights the versatility of paperboard in traditionally plastic-heavy applications. Also in August 2025, Smurfit Westrock, created from the merger of Smurfit Kappa and WestRock, announced its total voting rights, underscoring a major consolidation in the global packaging sector.

July 2025 marked significant regulatory and market shifts. Amcor launched its sustainable Hector CRC closure, made with up to 100% PCR plastic, strengthening the case for recyclable plastic innovation. In the same month, the Recycled Materials Association (ReMA) officially classified paper cups as a recyclable material, a key milestone for recycling infrastructure in the foodservice industry. Meanwhile, International Paper’s divestiture of five European corrugated plants reshaped its footprint following its acquisition of DS Smith, signaling continued consolidation in the fiber-based packaging sector.

Policy frameworks remain a defining growth driver. The EU Sustainable Textile Strategy (June 2025) is imposing stricter material-use and waste reduction targets, indirectly fueling demand for circular raw materials such as cellulose fibers. Furthermore, intellectual property rulings like the UK Court of Appeal’s July 2025 decision against Aldi for its Taurus cider packaging underscore the need for distinctive and defensible packaging designs in an increasingly competitive landscape.

Key Trends and Emerging Opportunities Shaping the Circular Packaging Market

Implementation of Digital Product Passports (DPPs) for Full Material Traceability

The circular packaging market is increasingly adopting Digital Product Passports (DPPs) to provide a verifiable record of material composition, recycled content, and end-of-life instructions. This trend is driven by the European Union's Ecodesign for Sustainable Products Regulation (ESPR), which mandates digital tracking to enhance product durability, reusability, and recyclability. DPPs enable full supply chain transparency, accessible to manufacturers, recyclers, regulators, and consumers, reducing the risk of greenwashing. Industry collaboration, such as the HolyGrail 2.0 initiative involving over 160 companies, is leveraging digital watermarks as data carriers for DPPs, improving precision sorting at recycling facilities. The adoption of DPPs transforms the circular packaging value chain, creating opportunities for data-driven services that support recycling, supply chain transparency, and the broader circular economy.

Strategic Expansion of Reusable Packaging Pooling Systems for B2B and B2C

Another major trend is the expansion of reusable packaging pooling systems, which operate on deposit-return or subscription models. These systems extend the lifecycle of packaging, drastically reducing new material production and supporting circular economy principles. B2B systems like the Swedish Return System (SRS) for crates and pallets have proven economically viable and are now being adapted for B2C applications through partnerships with “packaging as a service” providers like Loop. According to the Ellen MacArthur Foundation, reusable containers often achieve a lower environmental impact than single-use containers after just a few cycles, even considering washing energy and water. This trend opens a growth avenue in logistics, cleaning, tracking services, and reusable packaging infrastructure, creating new revenue streams for brands and service providers.

Development of Advanced Monomaterial Flexible Packaging for Recyclability

There is a significant opportunity in monomaterial flexible packaging, particularly pouches and films made from a single polymer type (e.g., polyethylene or polypropylene). Unlike traditional multi-layer laminates, these packages are fully compatible with existing recycling streams. Advanced barrier coatings now allow all-PE or all-PP films to provide adequate protection against oxygen and moisture, addressing a key technical challenge. Brand owners are increasingly demanding recyclable flexible packaging, with market reports indicating faster growth for monomaterial formats compared to multi-material alternatives, especially in food and beverage sectors. Packaging companies are actively collaborating with brands to re-engineer structures, ensure performance on high-speed filling lines, and transition product lines to monomaterial formats, driving significant innovation in the circular packaging market.

Creation of Integrated Chemical Recycling Infrastructure for Food-Grade PCR

Mechanical recycling often produces lower-quality plastics unsuitable for food-contact applications, creating a critical need for chemical recycling (advanced recycling). This technology breaks down mixed plastic waste into monomers, enabling the production of virgin-quality recycled PET and polyolefins. Companies like Dow have developed REVOLOOP™ resins, certified for food contact in Europe, demonstrating the commercial viability of chemically recycled plastics. Investment in chemical recycling is projected to reach €8 billion by 2030, with a target output of 2.8 million tons of chemically recycled plastics. European case studies, such as the collaboration between Lactel and INEOS to produce the first chemically recycled milk bottle, illustrate practical applications. Developing a robust chemical recycling infrastructure not only solves the challenge of hard-to-recycle plastics but also creates a high-value, sustainable material supply for food and beverage packaging with strict safety requirements.

Competitive Landscape: Global Leaders Driving Circular Packaging with Material Innovation

The circular packaging industry is defined by global players that are scaling recycled content, advancing paperization, and innovating closed-loop systems.

Smurfit Westrock Merges to Form a Global Paper-Based Packaging Leader

Formed in August 2025 from Smurfit Kappa and WestRock, Smurfit Westrock is now a dominant force in corrugated and paperboard solutions. Its sustainability-first approach is backed by new hubs such as its Great Lakes corrugated operations facility in Wisconsin, supporting North American beverage and consumer goods markets.

Mondi Group Launches High-Barrier Paper to Replace Plastics

Mondi Group is accelerating paper-based innovation with its FunctionalBarrier Paper Ultimate (August 2025) and its FlexStudios hub (2024), enabling co-creation of sustainable flexible packaging. With 87% of its portfolio already recyclable, reusable, or compostable, Mondi is a frontrunner in advancing fiber-based circular solutions.

Amcor PLC Strengthens Recyclable Plastic Portfolio with Hector CRC

Amcor remains a leader in flexible and rigid plastics with a strong push toward recyclable and PCR-based solutions. Its Hector CRC (July 2025) closure, made from up to 100% PCR plastic, balances safety and sustainability while meeting global regulatory standards. Amcor’s commitment to making all packaging recyclable or reusable by 2025 positions it at the forefront of circular plastic innovation.

DS Smith Plc Expands Fiber-Based Circular Design Principles

DS Smith is advancing circular design metrics to eliminate problem plastics, replacing 762 million plastic items since 2020. Its “Now & Next” strategy commits to a 46% CO₂ reduction by 2030 and net zero by 2050. Active R&D into seaweed and agri-waste fibers positions DS Smith as a pioneer in next-gen fiber innovation.

Ball Corporation Pushes Real Circularity in Aluminum Packaging

Ball Corporation leads in infinitely recyclable aluminum packaging and advocates for a 90% global recycling rate by 2030. With manufacturing from recycled aluminum requiring 20 times less energy, Ball’s expertise delivers low-carbon, closed-loop packaging solutions for the beverage sector, including cider, beer, and water.

International Paper Advances Circular Bioeconomy with Fiber Recovery

International Paper focuses on corrugated and fiber-based transport packaging. Its July 2025 divestiture of five European plants strengthens strategic alignment post-DS Smith acquisition. Using 5.2 million tons of recovered fiber annually, the company advances a circular bioeconomy model, ensuring its products remain 100% recyclable, reusable, or compostable.

Circular Packaging Market Share Insights

Food & Beverages Dominate Market Share by End-Use Industry in Circular Packaging

The food and beverages sector accounts for 40% of circular packaging demand, making it the undisputed volume driver of the industry. Its dominance is rooted in the sheer scale of packaging consumption in ready-to-eat meals, beverages, fresh produce, and quick-service restaurants. Regulatory bans on single-use plastics and Extended Producer Responsibility (EPR) frameworks have made F&B the primary testing ground for reusable systems, mono-material designs, and compostable substitutes. Multinationals like Nestlé, PepsiCo, and Unilever are committing to 100% recyclable, reusable, or compostable packaging by 2030, creating large-scale demand for circular solutions. In addition to compliance, F&B companies are using circular packaging as a brand differentiator, promoting PCR-content labeling and eco-branding to appeal to environmentally conscious consumers. This sector’s dominance ensures that innovation pipelines in bottles, pouches, cartons, and tubs are overwhelmingly directed toward food and beverage applications.

Personal Care & Cosmetics Accelerate Circular Packaging Adoption as a Premium Branding Tool

Personal care and cosmetics represent 22% of the circular packaging market, underscoring the sector’s proactive adoption of sustainable packaging as a brand-defining strategy. Unlike pharmaceuticals, where adoption is slowed by sterility requirements, cosmetics leverage circular materials to align with consumer expectations for “clean beauty” and eco-friendly branding. Glass jars, PCR PET bottles, and refillable packaging systems dominate this space, offering both sustainability and premium aesthetics. Brands like L’Oréal, Estée Lauder, and Procter & Gamble are aggressively piloting refill stations and reusable formats to capture sustainability-conscious consumers while maintaining luxury positioning. The integration of circular packaging is less about regulatory compliance and more about value creation and consumer perception, with higher price points justified by eco-labeling and sustainability claims. This premium-driven approach ensures cosmetics and personal care remain a high-value, fast-evolving end-user segment in circular packaging adoption.

United States Circular Packaging Market Accelerates with Reusable and Recyclable Innovations

The U.S. circular packaging market is heavily shaped by federal and state regulations, with the EPA’s “National Strategy to Prevent Plastic Pollution” released in November 2024 emphasizing source reduction and alternative materials. Multinational corporations are making strategic investments in line with sustainability goals, such as the U.S. Plastics Pact, which targets 100% reusable, recyclable, or compostable plastic packaging by 2025. This regulatory and corporate push is driving the adoption of advanced recycling technologies, including chemical and molecular recycling, to produce food-grade recycled content.

Demand is particularly strong in the e-commerce and FMCG sectors, where right-sized and durable packaging solutions help reduce waste and shipping costs. Extended Producer Responsibility (EPR) bills in states like Washington and Maryland further incentivize the development of recyclable and reusable products. The rise of “reusable packaging as a service” models, such as Revino’s refillable glass bottle ecosystems, highlights a shift toward circular consumption. Strategic partnerships between businesses, non-profits, government agencies, and research institutions, coordinated through initiatives like the U.S. Plastics Pact, are accelerating the transition to a circular economy in packaging.

Germany Circular Packaging Market Leads Europe with Regulatory Compliance and R&D Innovation

Germany’s circular packaging market is strongly influenced by the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, mandating that all packaging be fully recyclable or reusable by 2030. The German Packaging Act (VerpackG) enforces producer responsibility for the entire lifecycle of packaging, encouraging the design of products compatible with recycling streams. The market is seeing significant technological innovation, including increased orders for beverage packaging machinery to efficiently handle sustainable materials.

Key applications include e-commerce and food and beverage sectors, with a growing focus on premium products in reusable and returnable packaging. Germany’s robust R&D ecosystem supports collaboration between companies and research institutions to develop lighter, stronger, and more sustainable packaging solutions. Trends such as digital product passports and watermarks are improving material transparency, while pilot projects like “Mehrweg Modell Stadt” in Mainz and Wiesbaden showcase innovative reusable cup infrastructures in the service sector, reinforcing Germany’s leadership in circular packaging practices.

China Circular Packaging Market Expands with Green Policies and Domestic Innovation

China’s circular packaging market is driven by the government’s “dual carbon” goal, which emphasizes low-carbon, green, and circular industrial growth. Regulatory reforms under the 14th Five-Year Plan and mandatory standards like the “Limit of Harmful Substances of Coatings” (GB 30981.1 2025) set strict safety and environmental thresholds, aligning domestic packaging with international standards. Automation, AI, and integration of “5G plus industrial internet” are transforming production processes, enhancing efficiency and flexible capacity for complex packaging designs.

Domestic manufacturing is being prioritized to substitute imported technology, and the rapid growth of e-commerce and the food and beverage sectors is driving demand for sustainable, circular packaging. The government’s initiatives to prevent over-packaging through a whole-chain administration system further reinforce the market’s focus on material efficiency. China’s active R&D ecosystem, characterized by high patent activity, supports continuous innovation in materials and production methods, positioning the country as a key player in circular packaging technology.

India Circular Packaging Market Gains Momentum with Strategic Collaborations and Sustainable Investments

India’s circular packaging market is supported by government initiatives such as “Make in India” and “Zero Effect Zero Defect,” alongside MoEFCC efforts to ban single-use plastics. Corporate investments, including LNJ GreenPET’s partnership with Sumitomo Corporation in September 2025, are creating a robust r-PET value chain to meet domestic and global sustainable packaging demand. Technological adoption in India is expanding, including automated systems and Braille embossing technologies for pharmaceutical packaging to comply with European market standards.

The domestic e-commerce, food and beverage, and pharmaceutical sectors are primary drivers for circular packaging adoption. Strategic partnerships, such as The CIRCLE Alliance launched by Unilever, USAID, and EY, committing USD 21 million to promote packaging circularity, demonstrate cross-sector collaboration. Key applications include ready-to-drink beverages and processed foods, where sustainable packaging enhances brand value while meeting regulatory and consumer expectations for environmental responsibility.

Brazil Circular Packaging Market Driven by Regulatory Reforms and Sustainability Initiatives

Brazil’s circular packaging market is shaped by the 2010 National Solid Waste Policy and new 2024 laws banning single-use disposable items. States like Paraiba and Pernambuco have introduced reverse logistics legislation, making producers responsible for the end-of-life of packaging. Technological advancements, including AI and robotics, enhance efficiency and quality control in packaging operations, supporting sophisticated sorting and defect detection.

The market is expanding in the food and beverage, pharmaceutical, and personal care sectors, with sustainability as a central focus. Governmental targets for recycling 30% in 2025 and 50% by 2040 impact packaging design and materials. Companies are investing in advanced machinery to meet rising demand for sustainable, circular packaging solutions, ensuring alignment with both environmental regulations and industry-driven sustainability goals.

Japan Circular Packaging Market Pioneers Advanced Materials and Nanotechnology Solutions

Japan’s circular packaging market leverages precision manufacturing and next-generation materials. Oji Holdings’ March 2025 launch of cellulose nanofiber (CNF)-based flexible sheets exemplifies the country’s focus on high-performance, sustainable packaging. The “Plastic Resource Circulation Act” of April 2022 provides regulatory guidance for eco-friendly design and reduction of single-use plastics, supporting circular economy adoption.

Innovation in functionality emphasizes high dimensional stability, deformation resistance, and specialty applications, with companies like Toppan developing recyclable, lightweight, and biodegradable packaging solutions. Academic research is advancing biopolymers and natural agents for sustainable packaging, demonstrated by the award-winning 2023 Japan Packaging Contest entry a paper tray for confectionery that significantly reduces plastic use and simplifies recycling. Japan continues to lead in functional, eco-conscious, and nanotechnology-driven circular packaging solutions.

Circular Packaging Market Report Scope

Circular Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$248.9 Billion

|

|

Market Size (2034)

|

$424.1 Billion

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Packaging Type (Bottles & Jars, Bags & Pouches, Blister & Clamshells, Containers & Tubs, Cartons & Boxes, Others), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Household Chemicals, Personal Care & Cosmetics, Industrial, Others), By Material Type (Plastic, Paper & Paperboard, Glass, Metal, Others), By Technology (Advanced Recycling, Mechanical Recycling, Composting, Reusable Systems)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Ball Corporation, Berry Global Group, Inc., Smurfit Kappa Group, DS Smith Plc, Huhtamäki Oyj, International Paper Company, O-I Glass, Inc., WestRock Company, Graphic Packaging Holding Company, Tetra Pak International S.A., Greif, Inc., Crown Holdings Inc., Novolex

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Circular Packaging Market Segmentation

By Packaging Type

- Bottles & Jars

- Bags & Pouches

- Blister & Clamshells

- Containers & Tubs

- Cartons & Boxes

- Others

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Healthcare

- Household Chemicals

- Personal Care & Cosmetics

- Industrial

- Others

By Material Type

- Plastic

- Paper & Paperboard

- Glass

- Metal

- Others

By Technology

- Advanced Recycling

- Mechanical Recycling

- Composting

- Reusable Systems

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Circular Packaging Market

- Amcor plc

- Mondi Group

- Ball Corporation

- Berry Global Group, Inc.

- Smurfit Kappa Group

- DS Smith Plc

- Huhtamäki Oyj

- International Paper Company

- O-I Glass, Inc.

- WestRock Company

- Graphic Packaging Holding Company

- Tetra Pak International S.A.

- Greif, Inc.

- Crown Holdings Inc.

- Novolex

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive, research-driven methodology to analyze the global circular packaging market, integrating both primary and secondary data sources. Primary research involves consultations with packaging manufacturers, material suppliers, brand owners, regulatory authorities, and sustainability experts to gather first-hand insights on emerging trends, technological innovations, and regulatory compliance. Secondary research includes analysis of company reports, sustainability disclosures, patent filings, trade publications, and government policies across key regions, including the U.S., Europe, China, India, Brazil, and Japan. Market sizing and projections encompass packaging types (bottles, jars, pouches, cartons, containers), materials (plastic, paper & paperboard, glass, metal), and end-use industries (F&B, pharmaceuticals, personal care, household chemicals, industrial). USDAnalytics also evaluates innovations in advanced recycling, monomaterial solutions, reusable pooling systems, chemical recycling, and digital product passports to understand sustainability, operational efficiency, and circular economy impact. By combining regulatory trends, competitive landscape analysis, and technological advancements, USDAnalytics delivers actionable insights that guide industry professionals in portfolio optimization, strategic investments, and innovation in the circular packaging ecosystem.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.