PET Bottle Market Overview: Rising Adoption of rPET and Bio-PET Solutions

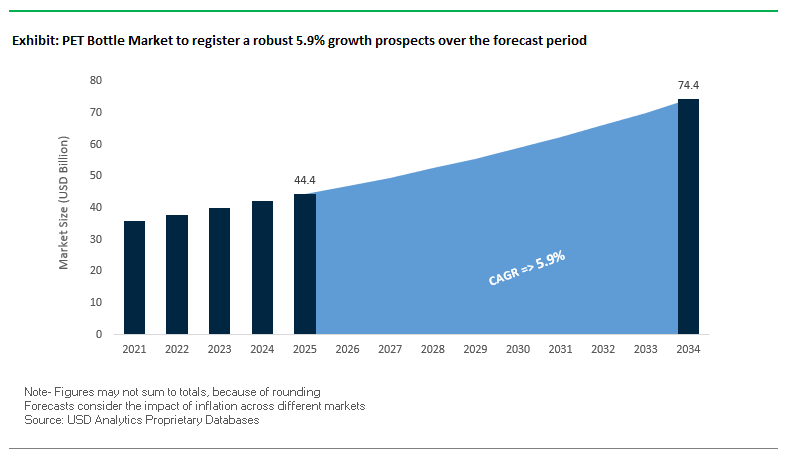

The Global PET Bottle Market is projected to grow from $44.4 billion in 2025 to $74.4 billion by 2034, registering a CAGR of 5.9%. PET (polyethylene terephthalate) remains the dominant packaging format for bottled water, carbonated soft drinks, and other beverages due to its clarity, durability, lightweight, and excellent barrier properties. Despite challenges in recycling infrastructure across several regions, the market is being reshaped by sustainability-driven innovations, including recycled PET (rPET) and bio-PET solutions.

A growing share of global consumers and brand owners are prioritizing eco-friendly packaging, even when it comes with higher production costs. For instance, India’s PET recycling efficiency reaches nearly 95%, setting benchmarks for global circular economy initiatives, while the U.S. and parts of Europe lag with much lower collection rates. The industry is also witnessing a surge in rPET adoption as brands integrate higher recycled content to strengthen their sustainability credentials. In parallel, bio-PET derived from plant feedstocks is emerging as a low-carbon alternative to fossil-based PET, aligning with ESG reporting frameworks and brand-level climate commitments.

Key Insights for Industry Professionals

- Clear, virgin PET dominates: Bottled water and soft drinks are the largest applications.

- Recycling gaps remain: India leads at ~95% efficiency, while U.S. and Europe trail behind.

- rPET adoption accelerating: Brands are using rPET to enhance sustainability even at higher costs.

- Bio-PET growing fast: Bio-based solutions are emerging as a critical low-carbon alternative.

Market Analysis: Recent Industry Developments in the Global PET Bottle Market

The PET bottle market is being shaped by sustainability commitments, M&A activity, and material innovations. In August 2025, PepsiCo announced a global goal to reduce its virgin plastic tonnage by 2% annually through 2030, supported by lightweighting initiatives and increased rPET integration. Similarly, in July 2025, Coca-Cola European Partners (CCEP) expanded its Southeast Asia footprint by acquiring Coca-Cola Beverages Philippines for $3.5 billion, signaling growth opportunities in emerging markets where PET bottle demand is accelerating.

Sustainability remains at the core of competitive differentiation. In May 2024, ALPLA introduced a recyclable PET wine bottle that lowers the carbon footprint by up to 50% compared to glass. In March 2025, Berry Global partnered with Mars, Incorporated to produce 100% recycled PET packaging for brands such as M&M’S and SKITTLES, reducing over 1,300 metric tons of virgin plastic annually. Likewise, Coca-Cola Singapore launched its first 100% rPET bottles in January 2025, advancing its “World Without Waste” strategy.

Other notable moves include Ball Corporation’s acquisition of Alucan in November 2024, diversifying into sustainable aluminum bottles, and Coca-Cola and ALPLA’s July 2024 collaboration to launch India’s first 100% rPET bottle for packaged drinking water. In August 2024, a U.S. Plastics Pact report highlighted the benefits of shifting from green PET to clear PET bottles, increasing the supply of food-grade rPET for circular economy applications. These developments illustrate a clear industry trajectory toward material innovation and regional scaling of recycling systems.

PET Bottle Market: Emerging Trends and Strategic Opportunities

Accelerated Lightweighting and Resin Reduction Through Advanced Design

Lightweighting has become one of the most powerful trends reshaping the PET bottle market, with manufacturers adopting advanced computer-aided design and precision injection stretch blow molding to reduce material use without sacrificing durability or product protection. This transition is particularly significant as beverage companies face mounting cost pressures and consumer scrutiny over their environmental footprints. Partnerships such as ALPLA and Vöslauer have yielded bottles nearly 90% lighter than glass alternatives, reducing both transportation costs and lifecycle emissions. Lightweight PET bottles maintain essential performance characteristics such as barrier protection for carbonated drinks and structural integrity for long-haul shipping, ensuring that reduced plastic content does not compromise shelf life or consumer safety. For global brands, lightweighting is not only a technical achievement but also a measurable step toward corporate sustainability goals, enabling reductions in virgin plastic consumption while reinforcing commitments to a circular packaging economy.

Strategic Shift to 100% Recycled PET (rPET) Across Major Brands

The global PET bottle market is experiencing a strategic pivot as leading beverage producers transition toward 100% rPET usage to meet both regulatory mandates and corporate sustainability pledges. Coca-Cola’s rollout of fully recycled PET bottles in markets including the Philippines and the U.S., and PepsiCo’s pioneering of the first 100% rPET carbonated beverage bottle in Taiwan, signal how aggressively the industry is moving in this direction. This trend is reinforced by the EU’s Packaging and Packaging Waste Regulation, which sets escalating recycled content requirements, and state-level mandates in the U.S., such as California’s recycled plastic quotas. The shift has created a competitive race to secure reliable supplies of high-quality, food-grade rPET, fueling large-scale investments in recycling infrastructure. Indorama Ventures, for example, has surpassed 150 billion bottles recycled, showcasing how petrochemical and packaging companies are realigning operations to support circular production. As more brands make public commitments to rPET, the global demand for food-grade recycled PET will continue to outstrip current supply, intensifying the need for technological solutions and collaborative investment.

Development of Enhanced Barrier Technologies for rPET

The widespread adoption of rPET brings technical hurdles, particularly its higher oxygen permeability compared to virgin PET. This poses a challenge for oxygen-sensitive beverages such as juices, teas, and beer, where freshness and flavor stability are critical. The opportunity lies in developing advanced barrier technologies that can be integrated with rPET without hindering recyclability. Industry research is highlighting innovative additives and masterbatches capable of improving both oxygen and water vapor barrier performance while maintaining clarity and mechanical properties. These solutions are being designed to blend seamlessly with existing recycling streams, ensuring that rPET bottles can remain compatible with circular economy goals. For beverage producers, this innovation is essential to expand the application of rPET bottles into premium categories where product quality cannot be compromised, reinforcing brand trust and enabling greater reliance on recycled content.

Integration of Digital Watermarks for High-Speed Sorting

Another transformative opportunity for the PET bottle market comes from the integration of digital watermarking technologies such as the HolyGrail 2.0 initiative. Digital watermarks embedded directly into packaging enable material recovery facilities to achieve sorting accuracies above 90%, a dramatic improvement over conventional optical sorting. Industrial-scale trials in Germany demonstrated the system’s ability to process millions of items, with average daily detection rates exceeding 56,000 pieces, offering unprecedented efficiency and precision. By enabling clear separation of food-grade PET from non-food-grade materials, digital watermarking is unlocking the ability to produce higher-quality recyclates that meet stringent food-contact standards. This technology also accelerates recycling throughput and reduces contamination rates, making rPET production more economically viable and scalable. For brands and recyclers alike, the integration of digital watermarks represents a pathway to closing the loop on PET bottles, ensuring that circularity targets and regulatory demands can be met at industrial scale.

Competitive Landscape: Leading Companies in the PET Bottle Industry

The global PET bottle industry is characterized by sustainability-led innovation, brand-owner commitments, and recycling expansion. Major companies are focusing on rPET adoption, circular economy initiatives, and partnerships to enhance their competitive position.

Amcor plc: Innovating with AmPrima™ Recycle-Ready Solutions

Amcor is a global leader in rigid and flexible PET packaging, serving beverages, food, and personal care markets. Its AmPrima™ Recycle Ready portfolio offers high-barrier PET bottles designed for full recyclability, while the ASSET™ lifecycle assessment service helps brands reduce environmental impact. Amcor’s strategy centers on making 100% of its packaging recyclable or reusable by 2025, supported by seamless integration with existing customer equipment.

PepsiCo, Inc.: Accelerating rPET Adoption Across Beverage Lines

PepsiCo is not only a major PET bottle user but also a driver of circular packaging solutions. In August 2025, the company reinforced its commitment to reduce virgin plastic by 2% annually. It has launched its first 100% rPET carbonated beverage bottle in Taiwan and its first energy drink in India with an rPET bottle under the Sting brand. PepsiCo also promotes concentrates and powders to reduce dependence on single-use PET bottles, while targeting 40% recycled content by 2035 across its packaging portfolio.

The Coca-Cola Company: Leading with “World Without WasteCoca-Cola remains one of the largest users of PET bottles globally. Its “World Without Waste” initiative aims for 100% recyclable packaging by 2025 and at least 50% rPET integration by 2030. In January 2025, Coca-Cola Singapore launched its first 100% rPET bottles, a milestone in Southeast Asia. Coca-Cola’s switch of Sprite from green to clear PET bottles was another critical move, significantly increasing the supply of food-grade rPET for global recycling systems.

ALPLA Group: Pioneering 100% rPET Bottles in Emerging Markets

ALPLA is recognized for its innovation and recycling leadership in PET bottles and preforms. It partnered with Coca-Cola in July 2024 to launch India’s first 100% recycled PET bottle for packaged drinking water, marking a milestone in Asia’s sustainable packaging landscape. ALPLA also produces reusable PET bottles that can be refilled up to 25 times and made with up to 100% rPET, strengthening its role in advancing closed-loop plastic systems.

Berry Global, Inc.: Scaling Recycling for a Circular Economy

Berry Global offers PET bottles and closures across food, beverage, and personal care industries. In March 2025, it partnered with Mars to produce 100% rPET jars for confectionery brands, reducing reliance on virgin plastics. Berry’s B Circular Range highlights its circular economy strategy, and its expanded recycling capacity from 220 million pounds in 2020 to 350 million pounds in 2023 positions the company as a critical supplier for sustainability-focused brands.

PET Bottle Market Share Insights

Bottled Water Dominates Market Share by Application in PET Bottles

Bottled water accounts for 45% of the PET bottle market, making it both the largest volume driver and the fiercest sustainability battleground. Global beverage giants are under immense regulatory and consumer pressure to transition toward 100% rPET and lightweight bottles without compromising strength or clarity. This segment has triggered the most significant capital flows into closed-loop recycling systems, advanced washing technologies, and collection infrastructure to ensure availability of food-grade rPET. Bottled water also represents the category most vulnerable to substitution, as aluminum cans and refillable systems are increasingly positioned as eco-friendly alternatives. The segment’s dominance highlights its dual role: it is not just the largest user of PET but also the testing ground for innovations that will define the future of circular beverage packaging.

Food & Beverages Secure Market Share Leadership by End-Use in PET Bottles

Food and beverages hold an overwhelming 88% share of PET bottle consumption, underscoring the material’s entrenched role as the default container for global liquid packaging. From soft drinks to condiments, PET’s balance of clarity, lightweighting, shatter resistance, and regulatory compliance makes it indispensable for fast-moving consumer goods. The innovation cycle in PET bottles whether rPET integration, advanced barrier coatings for juices, or ergonomic designs for sauces is dictated by F&B brands’ aggressive sustainability pledges and supply chain efficiency targets. This dominance also stabilizes rPET demand, since beverage players set the benchmark for recycled content adoption. The segment’s share demonstrates how the PET bottle industry is strategically aligned with the packaging priorities of multinational F&B companies, making it the linchpin of the circular packaging economy.

United States: Rising Demand for Recycled PET and Lightweight Bottles

The U.S. PET bottle market is increasingly driven by consumer awareness of sustainability, leading to strong demand for bottles containing higher percentages of recycled PET (rPET). This trend spans the bottling of water, soft drinks, and juices, aligning with broader corporate sustainability initiatives. Technological advancements such as lightweighting technologies have reduced the average weight of a 0.5-liter PET bottle by 48% over the past decade, minimizing virgin material use and lowering transportation costs.

Sustainability remains central to the industry’s evolution. The National Association for PET Container Resources (NAPCOR) reported that the average post-consumer rPET content in U.S. bottles reached 16.2% in 2023, demonstrating a marked shift toward eco-conscious packaging. Corporate initiatives are further accelerating market growth; Coca-Cola has committed to 50% recycled material by 2030, while PepsiCo has introduced bottles made with 100% rPET in selected product lines. State-level regulations, including mandatory recycled content laws in California and Washington, along with a PET bottle collection rate of 33% in 2023 the highest since 1996 highlight the growing emphasis on recycling and circularity in U.S. PET packaging.

Germany: Circular Economy Leadership and Regulatory Excellence Driving PET Packaging

Germany’s PET bottle market is shaped by the EU Packaging and Packaging Waste Regulation (PPWR 2025), creating a strong demand for eco-friendly and fully recyclable bottles. The country’s deposit-return scheme (DRS), the largest and most efficient in the world, achieves a 98% return rate on single-use drink containers, providing a robust stream of recycled materials and reinforcing the circular economy.

Technological innovation supports market growth. Companies such as Vetropack Group have launched lightweight, tempered glass bottles that are 30% lighter than standard alternatives, demonstrating the industry’s focus on durability and sustainability. Governmental mandates, including a single-use plastics levy implemented in 2024, drive better resource utilization and influence packaging design. These developments, coupled with consumer preference for sustainable solutions, position Germany as a global leader in innovative and environmentally responsible PET packaging.

China: Sustainability Policies and Production Dominance Fuel PET Bottle Growth

China’s PET bottle industry is propelled by the government’s dual carbon objectives, aiming for carbon peak and carbon neutrality. Policies targeting eco-friendly, reduced, and reusable materials are accelerating innovation in the packaging sector. Additionally, the Plastic Pollution Control Action Plan (2021-2025) and bans on imported waste plastics have stimulated domestic recycling initiatives and the development of advanced technologies.

China dominates global PET bottle production, with a total capacity of 21.68 million tons, representing nearly 50% of global production. Chinese manufacturers are increasingly investing in automation, AI, and “5G plus industrial internet” integration, improving efficiency and enabling scalable production of PET bottle-grade chips. Coupled with growing sustainability awareness and supportive government policies, China remains a critical hub for high-quality and sustainable PET packaging solutions.

India: Regulatory Push and Infrastructure Investments Driving rPET Adoption

The Indian PET bottle market is witnessing rapid growth due to government initiatives promoting sustainable packaging, particularly the Plastic Waste Management (Amendment) Rules, which phase out certain single-use plastics. This has significantly increased the demand for eco-friendly and reusable PET bottles, especially in the beverage sector. Regulatory requirements mandating 30% recycled content by 2025, rising to 60% by 2030, are creating a robust market for B2B-grade rPET, projected to reach over ₹15,000 crore by 2030.

Investments in infrastructure are further strengthening the market. Ball Beverage and AGI Greenpac are expanding production facilities for aluminum cans and glass containers, indirectly supporting PET industry sustainability efforts. Corporate initiatives, such as PepsiCo India’s launch of 100% recyclable rPET Pepsi Black bottles, highlight the growing adoption of recycled materials across the supply chain. Together, regulatory mandates, corporate commitments, and infrastructural investments are positioning India as a rapidly emerging market for sustainable PET bottle solutions.

PET Bottle Market Report Scope

PET Bottle Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$44.4 Billion

|

|

Market Size (2034)

|

$74.4 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Material (Virgin PET, Recycled PET), By Application (Bottled Water, Carbonated Soft Drinks, Juices & Nectars, Edible Oils, Sauces & Condiments, Other Applications), By Neck Finish (PCO 1810, PCO 1881, 30/25, Other Neck Finishes), By End-Use Industry (Food & Beverages, Homecare & Personal Care, Pharmaceuticals)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Indorama Ventures Public Company Limited, ALPLA Group, Berry Global Inc., Resilux NV, Zijiang Group, SABIC, Crown Holdings, Inc., O-I Glass, Inc., Sidel (Tetra Laval Group), Graham Packaging Company Inc., Gerresheimer AG, Sonoco Products Company, Huhtamaki Oyj, Greiner Packaging International GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

PET Bottle Market Segmentation

By Material

By Application

- Bottled Water

- Carbonated Soft Drinks

- Juices & Nectars

- Edible Oils

- Sauces & Condiments

- Other Applications

By Neck Finish

- PCO 1810

- PCO 1881

- 30/25

- Other Neck Finishes

By End-Use Industry

- Food & Beverages

- Homecare & Personal Care

- Pharmaceuticals

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in PET Bottle Market

- Amcor plc

- Indorama Ventures Public Company Limited

- ALPLA Group

- Berry Global Inc.

- Resilux NV

- Zijiang Group

- SABIC

- Crown Holdings, Inc.

- O-I Glass, Inc.

- Sidel (Tetra Laval Group)

- Graham Packaging Company Inc.

- Gerresheimer AG

- Sonoco Products Company

- Huhtamaki Oyj

- Greiner Packaging International GmbH

* List Not Exhaustive

Methodology

USDAnalytics employed a rigorous research methodology to deliver an in-depth and actionable analysis of the global PET Bottle Market. Our approach combined primary research, including interviews with packaging manufacturers, beverage producers, sustainability officers, and regulatory authorities, with secondary research from company reports, press releases, industry journals, and government regulations. Market sizing and growth projections were derived from historical trends, adoption rates of rPET and bio-PET, lightweighting initiatives, barrier technology innovations, and regional recycling efficiencies. Segmentation analysis covered material types (virgin PET, recycled PET), applications (bottled water, carbonated drinks, juices, edible oils, and sauces), neck finishes, and end-use industries (food & beverages, homecare, pharmaceuticals). Qualitative insights focused on strategic developments, such as mergers and acquisitions, sustainability commitments, and digital watermarking for high-speed sorting. Competitive benchmarking highlighted key players including Amcor, PepsiCo, Coca-Cola, ALPLA, and Berry Global in advancing circular economy initiatives and high-performance PET packaging solutions. This methodology ensures USDAnalytics provides industry professionals with precise, forward-looking insights for investment decisions, production planning, and sustainability strategies.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.