Market Overview: Glass Bottles Market to Reach $70.5 Billion by 2034 on Premiumization and Circularity

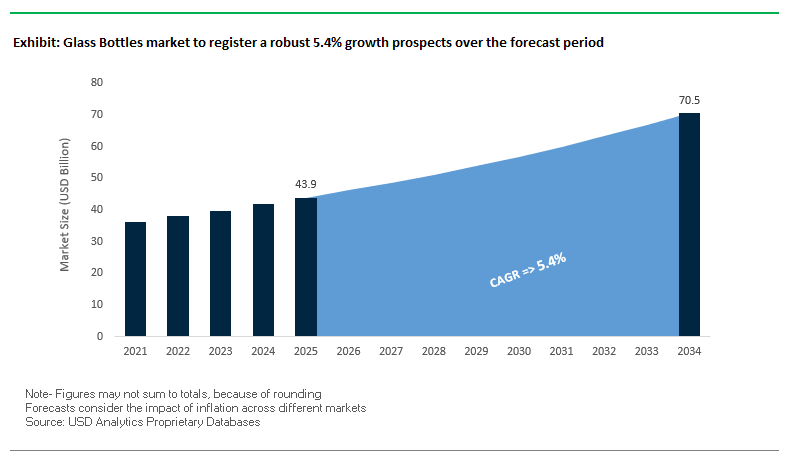

The global glass bottles market is valued at $43.9 billion in 2025 and is projected to reach $70.5 billion by 2034, growing at a CAGR of 5.4%. Glass remains the packaging of choice for wine, spirits, premium beverages, food, and pharma thanks to its chemical inertness, recyclability, and brand-building aesthetics. For industry buyers, the proposition is shifting from commodity containers to lightweighted, high-recycled-content glass that lowers logistics emissions while safeguarding product purity. Vendors are doubling down on closed-loop cullet sourcing, furnace efficiency, and decorative finishes that enhance shelf impact without compromising sustainability targets.

Key Insights for professionals

- Lightweighting as a cost & CO₂ lever: New 300g lightweight wine bottles (launched Jul 2025) cut glass mass and transport emissions while preserving strength.

- High recycled content (cullet) as a KPI: Strategic partnerships (e.g., CAP Glass in North America) secure quality cullet for consistent, circular supply.

- Premiumization drives mix: Wine/spirits brands prioritize glass to maximize brand value, clarity, and tactile cues.

- Non-reactive safety edge: Glass’ inertness underpins uptake in pharma vials, ampoules, and food where purity and shelf stability are non-negotiable.

Market Analysis: Recent Strategic Moves Reshape Capacity, Cost, and Sustainability

Industry momentum in 2024–2025 reflects a dual track of operational optimization and green investments. In September 2025, O-I Glass announced a production halt at Portland, Oregon, aligning with footprint optimization, while in August 2025 it reported Q2 strength with cost reductions and +4% sales volume in the Americas, demonstrating the payoff from modernization initiatives. Also in August 2025, Verallia signaled profitability recovery on higher volumes and cash generation, supported by financing actions that bolster its growth pipeline.

Brand-facing innovation kept pace. Ardagh Glass Packaging won Clear Choice Awards (May 2025) for sustainability-forward, design-led bottles, and in April 2025 switched its California plant to a new solar field, evidencing the sector’s renewable shift. Capacity is expanding in growth corridors: Vitro committed $70 million (Mar 2025) for a new furnace in Toluca to capture rising regional demand. Structurally, Verallia’s acquisition of Vidrala’s Italian business (Jul 2024, €230M) reinforced its footprint in a strategic European market. Meanwhile, Krones’ acquisition of Netstal (Jul 2025) strengthens adjacent PET ecosystems, nudging hybrid packaging portfolios and competitive dynamics for beverage customers.

On the product side, lightweighting accelerated with Ardagh Glass Packaging-Europe’s 300g wine bottle (Jul 2025) a tangible proof point that cost, carbon, and performance can be co-optimized. Concurrently, glass makers deepened cullet partnerships to stabilize recycled content quality at scale, a critical requirement for brand owners aiming to publicize circularity metrics on pack.

Trends and Opportunities Reshaping the Glass Bottles Market

Strategic Capital Investment in Furnace Modernization and Production Capacity

The glass bottles market is undergoing a wave of modernization, with leading manufacturers investing heavily in furnace upgrades and capacity expansions to strengthen supply chain resilience and meet growing global demand. For example, Gerresheimer invested nearly €100 million at its Lohr, Germany facility, installing a new oxy-hybrid melting furnace that can operate with up to 50% electricity. This innovation reduces carbon dioxide emissions by as much as 40% compared to conventional furnaces while increasing output for pharmaceutical and cosmetics packaging.

In Eastern Europe, Rubin Glass Factory completed a BGN 250 million modernization program at its Pleven site, installing a high-tech furnace described as one of the region’s largest industrial investments in decades. This project reflects the market’s push toward energy-efficient and high-capacity infrastructure to serve beverage and food companies. Meanwhile, in India, Şişecam allocated around USD 56 million to upgrade its Halol furnace, raising daily capacity to 650 tonnes and expanding its footprint in a high-growth region. These investments highlight how capacity growth, sustainability, and geographic diversification are converging as strategic imperatives in the glass packaging industry.

Accelerated Adoption of Post-Consumer Recycled (PCR) Content Driven by Legislation

Another defining trend is the rapid integration of post-consumer recycled (PCR) glass content into new bottles, spurred by both regulation and corporate sustainability targets. The EU Packaging and Packaging Waste Regulation (PPWR), effective since February 2025, mandates recyclability for all packaging by 2030 and promotes reduced virgin material use. Industry platforms such as Close the Glass Loop aim to achieve a 90% collection rate for glass recycling by the end of the decade, creating strong momentum across the value chain.

Complementing regulatory pressure, the Furnaces for the Future initiative seeks to deploy hybrid electric furnaces that can handle higher cullet ratios. Because cullet melts at lower temperatures, these furnaces significantly cut both energy use and CO₂ emissions, strengthening the environmental credentials of glass packaging. Beverage giants are also applying market pressure global brewers and food brands are setting ambitious circularity targets, forcing glass suppliers to expand recycled content integration. This combination of government mandates and corporate commitments ensures that PCR glass adoption will remain a central driver of market transformation.

Expansion into Premium Non-Alcoholic Beverages

One of the most promising opportunities lies in the premiumization of non-alcoholic beverages, where glass bottles are increasingly favored for their luxury appeal, inert material properties, and sustainability profile. Traditionally associated with alcoholic beverages like wine and spirits, glass packaging is now gaining traction in categories such as kombucha, cold-pressed juices, functional waters, and artisanal sodas. A financial industry report noted that the same consumer behaviors fueling premium liquor sales are spilling into the non-alcoholic sector, with packaging playing a crucial role in shaping perceptions of purity and quality.

Glass offers unique advantages in this space: it is chemically inert, preventing any interaction with sensitive ingredients such as probiotics, vitamins, or plant extracts. This ensures that functional beverages maintain their nutritional integrity and flavor profile throughout their shelf life. Moreover, custom bottle shapes, embossing, and specialty closures allow brands to visually communicate craftsmanship and exclusivity. For instance, a non-alcoholic startup recently launched a line in custom-shaped embossed glass bottles, using packaging as a brand differentiator in the crowded wellness beverage segment. As health-conscious and eco-aware consumers continue to drive demand, glass stands out as the premium packaging material of choice.

Strategic Partnerships for Closed-Loop Recycling Systems

With demand for recycled glass rising sharply, the industry faces a challenge in securing consistent cullet supply. This creates a major opportunity for closed-loop recycling partnerships between manufacturers, municipalities, and waste management firms. The acquisition of Strategic Materials, Inc. by Sibelco is a prime example, strengthening the company’s role as a global leader in cullet collection and processing. By integrating more tightly with local recycling ecosystems, glass producers can ensure high-quality material flows for their furnaces.

Collaborative initiatives such as Close the Glass Loop bring together producers, brands, recycling facilities, and governments to standardize collection systems and boost recycling rates across Europe. Similarly, in North America, the Closed Loop Foundation has partnered with companies like HEINEKEN USA to improve recycling infrastructure, signaling a shift from traditional supplier relationships to shared-investment models. These partnerships not only secure raw material supply but also build a powerful sustainability narrative, allowing brands to position their packaging as truly circular and climate-friendly.

Competitive Landscape: Scale Players Compete on Lightweighting, Cullet, and Energy

The glass bottles landscape is concentrated, with leading multinationals scaling lightweighting, recycled content, renewable energy, and decorative capability. Competition centers on footprint optimization, innovation velocity, and end-market depth across beverages, food, and pharma.

Global leaders are modernizing furnaces, integrating renewable energy, and building cullet pipelines to deliver low-carbon, premium glass bottles. Decorative services (embossing, coatings) and modular manufacturing raise agility for shorter SKU runs in wine and spirits, while pharma players add high-precision vials and device interfaces.

O-I Glass: Execution on “Fit to Win” elevates cost and capacity

O-I is among the largest glass container manufacturers for beverage, food, and pharma. Its Fit to Win program targets modernization and footprint optimization; Q2 2025 showed +4% volume in the Americas despite softer Europe, evidencing competitiveness gains. O-I is a lightweighting leader, having commercialized an eco-designed 75cl bottle ~25% lighter than traditional 500g formats (Carbon Trust validated). With MAGMA modular technology and operations across 20+ countries, O-I blends scale with flexible, lower-carbon manufacturing.

Verallia: European scale with recycled content leadership

Verallia supplies wine, spirits, and food brands across Europe, emphasizing high-recycled-content “Verallia Green” lines. The Jul 2024 acquisition of Vidrala’s Italy business (€230M, two furnaces, ~225 kt/y) strengthened a key hub market. In Aug 2025 it reported improving profitability and cash generation, aided by volume recovery and financing actions. Verallia’s strategy fuses circularity metrics, lightweighting, and tailored design, aligning closely with premium beverage customers’ ESG agendas.

Ardagh Group: Design awards meet renewables execution

Ardagh delivers infinitely recyclable glass with award-winning ECO Series™ lightweight platforms. It secured multiple Clear Choice Awards (May 2025) and, in Apr 2025, energized its California facility with a solar field, cutting scope-2 emissions. Ardagh’s end-to-end offer design, manufacturing, and decoration helps brands unlock premium shelf presence while tracking toward science-aligned carbon reductions.

Gerresheimer: Pharma-grade precision with device synergies

Gerresheimer is a strategic partner to pharma/biotech, supplying vials, cartridges, ampoules, and primary packaging alongside delivery devices (inhalers, pens). In Aug 2025, it secured €200M in loans to prepay part of the bridge for Bormioli Pharma, increasing financial flexibility for growth. With capacity for 5B+ glass injection vials annually and expansion projects (including India), Gerresheimer leverages quality systems and regulatory know-how that general packaging players can’t easily replicate.

Vidrala: Focused European specialist in lightweight bottles

Vidrala specializes in lightweight glass for wine and spirits, optimizing energy use and furnace technology while pursuing carbon-neutral operations over time. The Jul 2024 divestment of its Italian operations to Verallia sharpened focus on core regions (Iberia, broader Europe). Its differentiation lies in agile production for premium SKUs, tight customer collaboration, and continuous lightweighting to reduce total cost of ownership for beverage brands.

Vitro: North American capacity expansion for demand capture

Vitro serves a broad set of food and beverage applications in North America. To meet rising demand, it committed $70M (Mar 2025) for a new furnace in Toluca, Mexico, incorporating advanced melting technology. Vitro’s strategy centers on capacity reliability, technology upgrades, and regional proximity, supporting fast-growing beverage categories that require consistent clarity, strength, and supply assurance.

Glass Bottles Market Share Insights

Bottles Secure the Largest Market Share by Product Type in Glass Bottles Industry

In 2025, bottles type dominate the glass bottles industry with 70% market share, making them the volume leader across global packaging. Their supremacy is rooted in the beverage sector, where glass is essential for premium beers, wines, spirits, and RTD beverages. The impermeability of glass ensures no flavor scalping, while its recyclability and premium aesthetics strengthen its appeal among sustainability-conscious consumers and high-end brands. Glass jars follow as the traditional food preservation format, widely used for baby food, gourmet condiments, and organic spreads. Vials and ampoules represent a precision-driven niche, catering to pharmaceutical injectables and cosmetic serums where sterility, dosing accuracy, and compatibility are non-negotiable. Other specialty formats contribute smaller shares but are critical for decorative or custom designs in luxury sectors. The breakdown highlights how bottles anchor high-volume demand, jars reinforce glass’s food legacy, and vials sustain its indispensable role in pharmaceutical and cosmetic safety.

Beverages Anchor Market Share by Application in Glass Bottles Industry

By application, beverages hold 60% of the glass bottles industry market share in 2025, reinforcing their role as the industry’s growth engine. Alcoholic beverages dominate this share, with wine, beer, and spirits relying heavily on glass for its premium identity and unmatched preservation of carbonation and flavor. Non-alcoholic drinks such as premium waters, specialty juices, and RTD cocktails further amplify demand, positioning beverages as the anchor application. Food packaging follows as a key driver, where glass protects organic sauces, dairy alternatives, and premium oils while reinforcing purity and safety. Pharmaceuticals depend on borosilicate bottles for sensitive liquid formulations, ensuring compliance with global drug safety standards. Cosmetics and perfumes leverage the luxury perception of glass, where finely crafted bottles elevate brand prestige and consumer loyalty. This application mix illustrates how beverages secure the largest share through tradition and premium branding, while food, pharma, and cosmetics sustain glass as a material of choice across value-added applications.

United States: Lightweighting and Premiumization Driving Glass Bottle Innovation

The U.S. glass bottles market is witnessing significant advancements driven by sustainability, premiumization, and smart packaging trends. Major players like O-I Glass are investing in lightweighting technologies to produce lighter glass bottles, reducing transportation costs and carbon emissions, which addresses environmental concerns while enhancing operational efficiency. The Glass Packaging Institute (GPI) is actively collaborating with governments and non-profits to expand recycling infrastructure, increasing the availability of recycled glass (cullet) and reducing energy consumption. The demand for premium beverages, particularly in the craft beer, wine, and spirits sectors, is driving innovation in aesthetically appealing, custom-designed glass bottles. Regulatory advantages, such as the FDA’s GRAS (generally recognized as safe) classification for glass, ensure chemical safety, making it a preferred choice for brands. Additionally, smart packaging integration, including QR codes for product origin, nutritional content, and recycling instructions, is emerging as a key application to enhance transparency and consumer engagement.

Germany: Circular Economy Leadership and High-Quality Pharmaceutical Glass Production

Germany’s glass bottles market is at the forefront of sustainable packaging practices, driven by the German Packaging Act (VerpackG) and preparations for the EU Packaging and Packaging Waste Regulation (PPWR). German manufacturers, including Stoelzle Glass Group, are leading in lightweighting technology, producing high-quality, low-weight glass for pharmaceutical, cosmetic, and spirits applications, which reduces carbon footprints. Germany is also a major hub for pharmaceutical glass exports, with Gerresheimer AG developing sustainable glass vials for injectable drugs to meet growing demand for safe, reliable packaging. Circular economy initiatives are central to the market, with manufacturers increasingly incorporating high percentages of recycled glass cullet, positioning Germany as a global leader in environmentally responsible glass bottle production.

China: Rising Domestic Demand and Governmental Push for Sustainable Glass Packaging

China’s glass bottles market is being propelled by rapid urbanization, rising disposable incomes, and increasing domestic demand, particularly in the alcoholic beverage sector with products like baijiu. A growing middle class has intensified demand for premium, high-end glass bottles, with advanced decoration techniques for cosmetics, perfumery, and spirits driving market differentiation. Government policies promoting sustainability, including plastic bans and waste management regulations, are motivating manufacturers to adopt eco-friendly and reusable glass alternatives. Chinese glass enterprises are also expanding internationally; for example, Tefu International launched a new production line in Tanzania in August 2024, enhancing local supply and regional market coverage.

India: “Make in India” Driving Investment and Specialty Glass Production

India’s glass bottles market is being strengthened by the “Make in India” initiative, attracting capital investments and enhancing domestic manufacturing capabilities. Key players such as AGI Greenpac have expanded production capacities to meet growing domestic demand. Technological upgrades and R&D investment are enabling the production of high-end specialty glass for cosmetic and perfumery sectors, with a strong focus on exports. Rising consumer awareness regarding health, hygiene, and quality is shifting preferences toward glass bottles, particularly for food and pharmaceutical applications. The alcoholic beverage segment, especially premium Indian Made Foreign Liquor (IMFL), is a key growth driver, with increased adoption of 100% glass packaging expected to support the segment’s expansion.

Brazil: Circular Economy and Regulatory Compliance Driving Sustainable Practices

While bioplastics are influencing the broader packaging sector in Brazil, the glass bottles market is aligning with sustainability and regulatory initiatives. Green polyethylene derived from sugarcane ethanol is reducing fossil fuel dependency, creating competitive pressures that encourage innovation in glass. Regulatory oversight by Anvisa ensures that glass bottles meet stringent food safety standards, promoting high-quality production. The Brazilian government is expected to implement decrees mandating recycling and restricting single-use items, further emphasizing sustainable practices. Initiatives like “eureciclo,” which award Packaging Recycling Certificates, are reinforcing circular economy practices and encouraging manufacturers to adopt environmentally responsible strategies.

Japan: Lightweighting, Recycling, and High-Quality Standards Ensuring Market Growth

Japan’s glass bottles market is driven by lightweighting innovations and high-quality production standards. Companies like Toyo Glass focus on eco-friendly, lightweight bottles, reducing energy consumption in production and transportation. The market is governed by the strict Japanese Sanitation Act, ensuring that glass bottles are hygienic, safe, and minimize contamination risks. Japan has also developed an extensive recycling infrastructure, with over 18 facilities converting glass bottles and containers into cullets and powder for new production. These initiatives strengthen sustainability, operational efficiency, and product safety, positioning Japan as a leading market for environmentally responsible glass bottle production.

Glass Bottles Market Report Scope

Glass Bottles market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$43.9 Billion

|

|

Market Size (2034)

|

$70.5 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Product Type (Bottles, Jars, Vials & Ampoules, Other Containers), By Color (Flint (Clear), Amber, Green, Other Colors), By Application (Beverages, Pharmaceuticals, Cosmetics & Perfumes, Food Packaging)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Owens-Illinois (O-I), Ardagh Group S.A., Verallia S.A., Gerresheimer AG, Vidrala S.A., Vitro S.A.B. de C.V., Stoelzle Glass Group, Hindustan National Glass & Industries Limited (HNG), AGI Greenpac, Saverglass S.A., PGP Glass Private Limited, Nihon Yamamura Glass Co., Ltd., Zignago Vetro S.p.A., Anchor Glass Container Corporation, Bormioli Rocco

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Glass Bottles Market Segmentation

By Product Type

- Bottles

- Jars

- Vials & Ampoules

- Other Containers

By Color

- Flint

- Clear

- Amber

- Green

- Other Colors

By Application

- Beverages

- Pharmaceuticals

- Cosmetics & Perfumes

- Food Packaging

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Glass Bottles Market

- Owens-Illinois (O-I)

- Ardagh Group S.A.

- Verallia S.A.

- Gerresheimer AG

- Vidrala S.A.

- Vitro S.A.B. de C.V.

- Stoelzle Glass Group

- Hindustan National Glass & Industries Limited (HNG)

- AGI Greenpac

- Saverglass S.A.

- PGP Glass Private Limited

- Nihon Yamamura Glass Co., Ltd.

- Zignago Vetro S.p.A.

- Anchor Glass Container Corporation

- Bormioli Rocco

*List not Exhaustive

Research Coverage

This USDAnalytics report investigates the dynamic global glass bottles market, providing a comprehensive analysis of recent breakthroughs in lightweighting, high-recycled-content integration, and premiumization strategies across beverages, pharmaceuticals, and cosmetic packaging. The analysis reviews evolving manufacturing trends, operational optimizations, and sustainability innovations, highlighting key market drivers such as furnace modernization, post-consumer recycled glass adoption, and closed-loop supply chain collaborations. This report is an essential resource for industry professionals seeking insights into capacity expansion, energy-efficient production, circular economy initiatives, and strategic corporate maneuvers shaping the competitive landscape. In addition, the report highlights transformative developments from leading market players including O-I Glass, Verallia, Ardagh Group, Gerresheimer, Vitro, and Vidrala, emphasizing the implications of strategic investments, acquisitions, and product innovations on global market trajectories. By integrating historic data from 2021 to 2024 with forward-looking projections to 2034, this report equips stakeholders with a 360-degree perspective on market evolution, sustainability-driven growth, and premium segment opportunities.

Scope Highlights:

- Segmentation: By Product Type (Bottles, Jars, Vials & Ampoules, Other Containers), By Color (Flint/Clear, Amber, Green, Other Colors), By Application (Beverages, Pharmaceuticals, Cosmetics & Perfumes, Food Packaging)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Data Coverage: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Company Coverage: Analysis and profiles of 15+ leading companies including O-I Glass, Ardagh Group S.A., Verallia S.A., Gerresheimer AG, Vitro S.A.B. de C.V., Vidrala S.A., Stoelzle Glass Group, Hindustan National Glass & Industries Limited, AGI Greenpac, Saverglass S.A., PGP Glass Private Limited, Nihon Yamamura Glass Co., Ltd., Zignago Vetro S.p.A., Anchor Glass Container Corporation, and Bormioli Rocco

Methodology

The USDAnalytics methodology integrates a robust combination of primary and secondary research, quantitative modeling, and expert validation to deliver precise, actionable insights on the global glass bottles market. The research begins with extensive data collection from industry reports, company filings, press releases, regulatory databases, and market trade journals. This is complemented by structured interviews with manufacturers, distributors, and packaging experts to capture qualitative trends such as premiumization preferences, sustainability adoption, and operational innovation. Collected data is rigorously validated, normalized, and triangulated to minimize bias and ensure reliability. Advanced forecasting models then project market growth from 2025 to 2034, accounting for factors including capacity expansion, raw material availability, regulatory mandates, and circular economy adoption. Geographic segmentation and product-level analysis are applied to evaluate market share, growth drivers, and investment opportunities, delivering an in-depth, professional-grade assessment that supports strategic decision-making for stakeholders across multiple sectors.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.