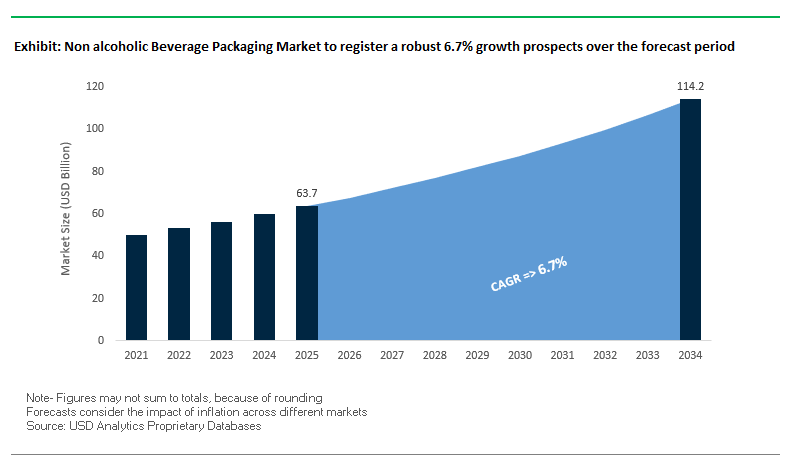

Non-Alcoholic Beverage Packaging Market to Reach $114.2 Billion by 2034 at 6.7% CAGR

The global non-alcoholic beverage packaging market is projected to grow from $63.7 billion in 2025 to $114.2 billion by 2034, reflecting a CAGR of 6.7%. This growth is fueled by rising demand for sustainable packaging materials, technological innovations in rigid and flexible packaging, and the integration of smart packaging solutions that enhance consumer engagement. Packaging companies are increasingly adopting recyclable plastics (rPET), paperboard cartons, and monomaterial solutions, aligning with global sustainability mandates and evolving consumer preferences.

Key Insights for Industry Professionals:

- Sustainable materials adoption: Increasing use of rPET bottles and paperboard cartons for juices, plant-based beverages, and functional drinks reduces environmental impact.

- Rigid packaging dominance: Bottles and cans remain the primary choice due to product protection, durability, and safe transportation.

- Flexible packaging growth: Lightweight bags and pouches are gaining traction, reducing transportation costs and carbon footprint.

- Smart packaging integration: QR codes, scannable features, and textured over-varnishes are driving consumer engagement, real-time product information, and brand loyalty.

- Circular economy alignment: Packaging innovations are increasingly designed for recyclability and monomaterial constructions, supporting regulatory compliance and sustainability goals.

Market Analysis: Recent Industry Developments Driving Non-Alcoholic Beverage Packaging Innovations

The non-alcoholic beverage packaging market has witnessed several strategic initiatives and technological advancements. In September 2025, Siegwerk participated in the 12th Specialty Films and Flexible Packaging Global Business Summit, showcasing circular packaging innovations and leveraging its expanded coating expertise following the Allinova acquisition. In August 2025, Mondi ramped up production of its FunctionalBarrier Paper Ultimate, offering an ultra-high barrier paper solution for food and beverage applications, while Graphic Packaging International launched the PaperSeal® Pressed MAP Tray, reducing plastic use by up to 85%.

Ball Corporation reported strong growth in non-alcoholic beverages in North America in August 2025, with global aluminum packaging shipments increasing 4.1% in Q2. The July 2025 debut of Smurfit WestRock on the New York and London Stock Exchanges marked the creation of a global leader capable of serving the non-alcoholic beverage market with innovative paper and fiber solutions.

Earlier developments include Amcor’s collaboration with Cofigeo in June 2025 to create a polypropylene (PP)-based monomaterial tray, Ball and Açaí Motion’s sustainable aluminum can launch in May 2025, and Amcor’s AmFiber Performance Paper stand-up pouch launch in April 2025, highlighting sustainable packaging trends. Constantia Flexibles’ acquisition of Aluflexpack in March 2025 expanded its flexible packaging portfolio, and Mondi and Proquimia’s paper-based pouch launch in February 2025 reinforced the industry’s commitment to eco-friendly alternatives.

Trends and Opportunities Transforming the Non-Alcoholic Beverage Packaging Market

Strategic Shift Towards 100% Recycled PET (rPET) in Major Bottling Operations

A defining trend in the non-alcoholic beverage packaging market is the rapid shift toward 100% rPET adoption by leading beverage companies. With mounting consumer demand for sustainable packaging, combined with corporate ESG goals and tightening regulatory frameworks, major bottlers are investing heavily to reduce reliance on virgin plastic.

In January 2025, The Coca-Cola Company expanded its national rollout of 100% rPET bottles in the U.S. for its 20-oz formats, eliminating nearly 80 million pounds of virgin plastic annually. Globally, Coca-Cola India introduced its 250ml rPET bottles in June 2024, cutting the carbon footprint by 66% compared to conventional virgin PET. Similarly, PepsiCo has integrated 100% rPET into carbonated beverage bottles in Taiwan and launched rPET bottles for its energy drink brand in India, signaling an aggressive global strategy.

The demand for high-quality rPET has created intense competition across the value chain, prompting collaborations like the September 2025 Eastman–Doloop partnership unveiled at Drinktec 2025, which showcased a 100% rPET beverage bottle produced using chemical recycling. This innovation ensures recycled plastics match the quality of virgin resins, crucial for food-grade compliance. As rPET adoption accelerates, companies that secure supply and establish closed-loop systems will gain a sustainability and cost advantage in the non-alcoholic beverage packaging market.

Integration of Digital Technologies for Smart Packaging and Traceability

The industry is also witnessing rapid digitalization of packaging with the integration of QR codes and digital watermarks to address sustainability, traceability, and consumer engagement simultaneously. These technologies move beyond branding, delivering operational and environmental benefits.

The HolyGrail 2.0 initiative has demonstrated the commercial viability of this approach. Industrial trials conducted in Germany (Aug–Dec 2024) achieved a 90% detection efficiency with nearly 56,000 packaging items identified daily, ensuring high-purity recycling streams essential for circular PET bottle production.

At the consumer level, serialized QR codes embedded into bottles allow users to scan for product authenticity, trace sourcing, and access detailed nutritional or recycling instructions. A technical report highlights how such systems combat counterfeit beverages while simultaneously enhancing transparency. For brand owners, this trend represents a dual benefit—meeting recycling mandates and engaging consumers through interactive packaging.

Development of Paper-Based Barrier Bottles for Carbonated Drinks

One of the most groundbreaking opportunities lies in the commercialization of paper-based bottles for carbonated soft drinks—a segment that remains dominated by PET due to its barrier strength.

The Paper Bottle Company (Paboco), working alongside Coca-Cola and Carlsberg, is actively developing prototypes that integrate ultra-thin barrier coatings capable of maintaining carbonation. Current prototypes for still beverages have proven successful, but the CO₂ containment challenge continues to be the technical barrier for scaling into carbonated categories.

A breakthrough in this area would not only reduce dependence on PET but also represent a paradigm shift in sustainable packaging materials, unlocking a multibillion-dollar market segment. Paper-based carbonated beverage bottles would position brands at the forefront of bio-based innovation, offering consumers packaging that is recyclable, renewable, and aligned with climate-conscious lifestyles. With governments incentivizing alternative materials and consumers demanding plastic-free beverage solutions, successful R&D in this field represents a high-value growth avenue for packaging converters and beverage brands alike.

Standardization and Adoption of Refillable/Reusable Packaging Systems

The rejection of single-use formats is creating a significant opportunity for the scaling of standardized refillable and reusable packaging systems. Unlike isolated pilot programs, success in this area requires industry-wide collaboration, shared logistics, and harmonized regulatory support.

Leading corporations are setting ambitious reuse goals. The Coca-Cola Company targets 25% of global sales in refillable/reusable bottles by 2030, while PepsiCo plans to double its refillable share from 10% to 20% within the same timeframe. These commitments reflect a structural shift in packaging models.

Collaborative initiatives such as the NextGen Consortium—which includes McDonald’s, Starbucks, and Coca-Cola—are trialing scalable reusable cup systems, proving that shared infrastructure is commercially viable when supported by collective action. Regulatory frameworks are also propelling adoption. The EU’s Packaging and Packaging Waste Regulation (PPWR) mandates that by 2030, 10% of non-alcoholic beverage packaging must be reusable, further pushing brands toward investment in refillable systems. This creates a transformative growth opportunity: companies that pioneer scalable, standardized reuse models will not only reduce costs and meet compliance requirements but also enhance brand equity by positioning themselves as leaders in the circular packaging economy.

Competitive Landscape of Global Non-Alcoholic Beverage Packaging Market

The non-alcoholic beverage packaging market is highly competitive, with key players focusing on sustainable, innovative, and high-performance packaging solutions. Market leaders leverage rigid and flexible materials, monomaterial designs, and digital engagement features to cater to consumer preferences while complying with environmental regulations.

Amcor plc: Leading Sustainable and Monomaterial Packaging Solutions

Amcor offers a diverse portfolio of PET bottles, rigid containers, and pouches for juices, water, dairy alternatives, and functional drinks. In April 2025, it launched the AmFiber Performance Paper stand-up pouch, and in June 2025, collaborated with Cofigeo on a PP-based ready meal tray designed for recyclability. Amcor’s Catalyst™ program emphasizes sustainability, with a public goal to make all packaging recyclable or reusable by 2025, providing seamless integration into existing filling lines and supply chains.

Ball Corporation: Driving Circularity with Aluminum Packaging

Ball Corporation is the world’s largest aluminum beverage can manufacturer, serving energy drinks, soft drinks, and sparkling water. In August 2025, the company reported strong growth in North America, while May 2025 saw the launch of a sustainable aluminum can with Açaí Motion, certified by the Aluminium Stewardship Initiative. Ball focuses on sustainability and circularity, aiming for a 90% global aluminum recycling rate by 2030, while offering advanced graphics and textured over-varnishes to enhance brand visibility and consumer engagement.

Mondi Group: Innovating Paper-Based Barrier Packaging

Mondi provides paper-based flexible films, laminates, and sacks for non-alcoholic beverages. In August 2025, it ramped up production of FunctionalBarrier Paper Ultimate, a recyclable alternative to multi-layer plastics, and in September 2025, launched a mono-material pouch for liquid detergents. Mondi’s strategic focus is on sustainable, value-accretive growth, reinforcing a circular economy while expanding production capacity with a €400 million paper machine startup in May 2025.

Tetra Pak: Global Leader in Aseptic Carton Packaging

Tetra Pak offers carton packages for juices, milk, and plant-based beverages along with processing equipment. The company introduced a paper-based barrier in aseptic packaging and the Tetra Pak® E3/Speed Hyper filling machine, capable of 40,000 packages per hour using eBeam technology. Tetra Pak focuses on safe, renewable, and recyclable packaging with low carbon footprints, ensuring long-term preservation of perishable beverages.

SIG Combibloc Group AG: Pioneering Aluminum-Free Multi-Serve Cartons

SIG specializes in aseptic carton solutions, including juice and milk cartons. In May 2025, it launched the world’s first aluminum-layer-free full-barrier multi-serve carton, reducing the carbon footprint by 61%. The company aims to raise paper content to 90% by 2030 and sources 100% FSC™-certified paperboard, emphasizing renewable, sustainable, and high-performance packaging through its SIG Terra portfolio.

Non alcoholic Beverage Packaging Market Share Insights

Bottled Water Dominates Market Share by Product Type in the Non-Alcoholic Beverage Packaging Industry

Bottled water leads the global non-alcoholic beverage packaging market with 35% share in 2025, driven by its universal consumption and positioning as a healthier substitute for carbonated drinks. Packaging innovation in this segment is centered on lightweight rPET bottles, 100% recycled PET integration, and designs optimized for recyclability, such as crushable bottles that improve collection efficiency. Carbonated soft drinks follow closely with 30% share, relying heavily on pressure-resistant PET bottles and aluminum cans, with cans increasingly preferred due to their high recyclability and premium perception. Juices and nectars account for 15%, historically reliant on glass and carton formats, but now shifting towards barrier-enhanced PET and recyclable cans for portability and sustainability. Ready-to-drink (RTD) tea and coffee, at 12%, reflect a diverse packaging mix, with glass bottles in premium RTD coffee, PET bottles for tea, and a surge in aluminum cans for cold brew due to their superior light barrier. Functional beverages, including energy and sports drinks, make up 8% of share, where packaging is central to brand identity aluminum cans dominate energy drinks for their edgy appeal, while PET bottles with sport caps drive sports drinks through portability and performance-driven designs.

Retail Leads Market Share by End-Use Application in the Non-Alcoholic Beverage Packaging Industry

Retail channels dominate with 50% share in 2025, making them the largest end-use application for non-alcoholic beverage packaging. This segment thrives on multi-pack formats such as shrink-wrapped PET bottles, can cartons, and paperboard outer packaging, designed for cost efficiency, shelf optimization, and bulk purchasing. Convenience stores follow with 25% share, where single-serve PET bottles and cans play a pivotal role in on-the-go consumption, optimized for mobility, impulse buying, and high visibility on chilled display shelves. Food service accounts for 15%, driven by fast-food chains, cafes, and restaurants where packaging includes fountain dispensers, bottled water, and canned drinks, with an accelerating shift towards PLA-lined paper cups and recyclable options in line with sustainability mandates. E-commerce, while holding only 10% share, is the fastest-growing channel, driven by bulk purchasing and subscription models for soda, sparkling water, and functional beverages. Packaging innovation here is centered on e-commerce-optimized formats with stronger bottles, lightweight cans, and reduced secondary packaging to minimize damage and shipping costs while enhancing the consumer unboxing experience.

United States: Sustainability and Smart Packaging Drive Growth in RTD and Mocktail Segments

The United States non-alcoholic beverage packaging market is shaped by a complex regulatory landscape, with state-level Extended Producer Responsibility (EPR) laws in California and Maryland pushing the industry toward recyclable and high-recycled-content packaging solutions. These regulations are fostering innovation in sustainable beverage containers that meet environmental and consumer expectations.

Technological advancements are driving the adoption of bio-based plastics, paper-based cartons, and smart packaging solutions. The rising “sober curious” trend has accelerated demand for mocktails and ready-to-drink (RTD) beverages, prompting brands to invest in differentiated, visually appealing packaging formats, including cans and glass bottles. Corporate initiatives, such as Berry Global Inc.’s advanced micro tray packaging solution using bio-based polyethylene, highlight strategic investments that could extend to non-alcoholic beverage applications. The segment has grown from $6 billion in 2018 to $8.7 billion in 2024, making premium, functional, and sustainable packaging a key competitive advantage.

Germany: EU Regulations and Circular Economy Drive Innovation in Sustainable Beverage Packaging

Germany’s non-alcoholic beverage packaging market operates under the European Union Packaging and Packaging Waste Regulation (PPWR), effective early 2025. These regulations emphasize recyclability, recycled content, and mono-material designs, favoring returnable and eco-friendly packaging. Germany’s established deposit-return system further incentivizes the adoption of sustainable containers.

German manufacturers are pioneers in lightweight, high-performance films and containers, exploring ultra-thin and recyclable materials. The country’s circular economy infrastructure supports the growing popularity of beverage cans, particularly for energy drinks and soft drinks, with sales volume increasing 47% over five years. Consumers favor cans for their convenience, portability, and eco-friendly perception, making them a key driver of innovation in sustainable non-alcoholic beverage packaging.

China: Government Initiatives and E-Commerce Expansion Fuel Demand for Sustainable Packaging

China’s government actively supports the high-end manufacturing sector, emphasizing dual-carbon targets and sustainable production standards. Automation and AI-driven production systems are being implemented to boost efficiency and quality control. This focus is particularly strong in the food processing, e-commerce, and consumer goods sectors, enabling companies to scale production of high-quality, sustainable beverage packaging.

Consumer trends are shifting toward premium, functional, and visually appealing beverages, fueling demand for innovative paperboard cartons, PET bottles, and advanced flexible packaging. The rapidly expanding e-commerce landscape further enhances market accessibility, allowing brands to reach a larger, increasingly health-conscious audience. Government support and private sector investments signal a robust growth trajectory for nano-enabled and sustainable beverage packaging solutions in China.

India: Policy Support and Circular Economy Initiatives Accelerate Sustainable Packaging Adoption

India’s non-alcoholic beverage packaging market benefits from initiatives such as Make in India and the Production Linked Incentive (PLI) scheme, which encourage domestic manufacturing and investment in sustainable packaging technologies. Regulations like the 40% sugar-sweetened beverage tax influence product formulation and packaging strategies, driving brands toward eco-friendly containers.

Technological innovation is evident in 100% recyclable rPET bottles, such as those launched by PepsiCo India in collaboration with Varun Beverages and Srichakra Polyplast. Corporate investments, including the Huhtamaki Foundation’s CloseTheLoop recycling initiative, support post-consumer waste management. Key applications include juices, sports drinks, RTD teas, and coffees, with packaging playing a pivotal role in brand differentiation, product protection, and shelf appeal across retail and online channels.

Japan: Regulatory Shifts and Innovative Sustainable Packaging Propel Market Leadership

Japan has implemented new food container and packaging rules, effective June 2025, introducing a positive list of approved synthetic materials. These regulations encourage the use of eco-friendly, paper-based packaging with safe coatings, enhancing sustainability across the non-alcoholic beverage sector.

Japanese companies focus on high-quality, functional, and environmentally responsible packaging, exemplified by Suntory Group’s “2R+B (Reduce, Recycle + Bio)” strategy to achieve 100% sustainable PET bottles by 2030. Innovations such as FtoP direct recycling technology and ultra-lightweight PET bottles (15g) reduce CO2 emissions. Key applications include ready-to-drink tea, coffee, and mineral water, where durable, lightweight, and visually appealing packaging supports consumer convenience and premium brand perception.

Brazil: Regulatory Push and Aluminum Cans Fuel Growth in Functional and Non-Alcoholic Beverages

Brazil’s non-alcoholic beverage packaging market is influenced by Law No. 15,088 (2025), amending the National Solid Waste Policy to ban solid waste imports and promote recycling. This legislation, combined with government initiatives for a circular economy, encourages eco-conscious beverage packaging solutions.

Technological innovation is evident in Ambev’s canned water launch, leveraging the high recyclability of aluminum cans. Functional beverages are the fastest-growing segment, driving demand for packaging that preserves quality and product integrity. The market remains dominated by carbonated soft drinks, but premium and health-oriented beverages are shaping the future, emphasizing sustainable, innovative, and convenient packaging formats.

Non alcoholic Beverage Packaging Market Report Scope

Non alcoholic Beverage Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$63.7 Billion

|

|

Market Size (2034)

|

$114.2 Billion

|

|

Market Growth Rate

|

6.7%

|

|

Segments

|

By Material (Plastic, Glass, Metal, Paper & Paperboard), By Product Type (Carbonated Soft Drinks, Bottled Water, Juices & Nectars, RTD Tea & Coffee, Functional Beverages), By Packaging Format (Bottles, Cans, Cartons, Pouches & Sachets), By End-Use Application (Food Service, Retail, Convenience Stores, E-commerce)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, WestRock Company, Ball Corporation, Crown Holdings, Inc., Sonoco Products Company, International Paper Company, DS Smith Plc, Oji Holdings Corporation, Huhtamaki Oyj, Ardagh Group S.A., Graphic Packaging Holding Company, Tetra Pak International S.A., Billerud AB, Mondi Group, Greiner Packaging International GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Non alcoholic Beverage Packaging Market Segmentation

By Material

- Plastic

- Glass

- Metal

- Paper & Paperboard

By Product Type

- Carbonated Soft Drinks

- Bottled Water

- Juices & Nectars

- RTD Tea & Coffee

- Functional Beverages

By Packaging Format

- Bottles

- Cans

- Cartons

- Pouches & Sachets

By End-Use Application

- Food Service

- Retail

- Convenience Stores

- E-commerce

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Non alcoholic Beverage Packaging Market

- Amcor plc

- WestRock Company

- Ball Corporation

- Crown Holdings, Inc.

- Sonoco Products Company

- International Paper Company

- DS Smith Plc

- Oji Holdings Corporation

- Huhtamaki Oyj

- Ardagh Group S.A.

- Graphic Packaging Holding Company

- Tetra Pak International S.A.

- Billerud AB

- Mondi Group

- Greiner Packaging International GmbH

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive, multi-layered research methodology to deliver actionable insights into the global non-alcoholic beverage packaging market. Our approach integrates primary research, including interviews with packaging engineers, sustainability experts, and supply chain managers, with secondary research sourced from industry reports, regulatory documents, patent filings, and corporate disclosures. Market sizing and forecasting are based on historical trends, adoption rates of sustainable materials such as rPET, paperboard cartons, monomaterial plastics, and aluminum, along with innovations in flexible packaging, smart labeling, and digital engagement technologies like QR codes and serialized watermarks. We evaluate the impact of regulatory frameworks, including the EU Packaging and Packaging Waste Regulation (PPWR), U.S. Extended Producer Responsibility (EPR) laws, and country-specific environmental initiatives, while assessing corporate sustainability commitments. Competitive intelligence examines strategic mergers, product launches, and technological advancements by key players including Amcor, Ball Corporation, Mondi Group, Tetra Pak, and SIG Combibloc, highlighting their initiatives in recyclable, reusable, and high-performance packaging solutions. This methodology ensures USDAnalytics delivers professional-grade insights that help industry stakeholders navigate market dynamics, capitalize on sustainability trends, and drive innovation in non-alcoholic beverage packaging.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.