Market Overview: Expanding Beverage Containers Market Led by PET, Aluminum, and Glass

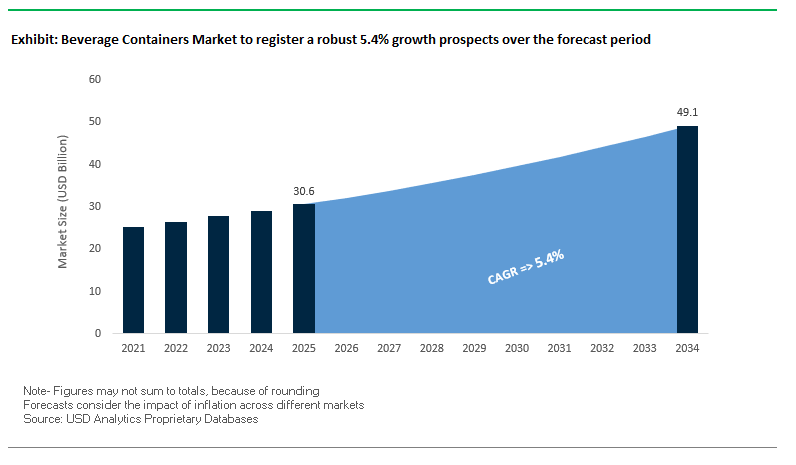

The Beverage Containers Market is valued at $30.6 billion in 2025 and is projected to reach $49.1 billion by 2034, registering a CAGR of 5.4%. Growth is being driven by the increasing consumption of packaged beverages, the shift toward sustainable packaging formats, and the premiumization of alcoholic and craft beverages. Industry professionals and buyers are seeking solutions that balance cost, durability, recyclability, and branding appeal, with packaging materials chosen to reflect both functionality and market positioning.

Polyethylene terephthalate (PET) bottles remain the most widely used packaging type for soft drinks and bottled water, valued for their lightweight, cost-effectiveness, and shatterproof safety. Aluminum cans are gaining momentum, especially for soft drinks and alcoholic beverages, due to their infinite recyclability with nearly 70% of aluminum ever produced still in circulation. Meanwhile, glass bottles remain central to premium beverages such as wine, spirits, and craft beers, where their inert properties ensure product purity and convey a high-end brand image.

Another fast-growing segment is aseptic cartons, widely used for shelf-stable milk, juices, and plant-based beverages. Their multi-layer structure protects against light and oxygen, enabling longer shelf life without refrigeration or chemical preservatives. Combined, these formats underline the market’s diversity and its evolution toward sustainability-driven innovation.

Key Insights for Industry Professionals

- PET dominates: Lightweight, cost-effective, and widely used for water and soft drinks.

- Aluminum’s recyclability advantage: 70% of aluminum ever produced remains in use today.

- Glass retains premium appeal: Preferred for wine, spirits, and craft beverages.

- Aseptic cartons grow rapidly: Shelf-stable liquids demand extended shelf life without additives.

Market Analysis: Recent Developments Strengthening Beverage Containers Industry

The beverage containers industry has seen a wave of strategic moves, portfolio restructuring, and sustainability-focused investments aimed at improving competitiveness and expanding capacity.

In August 2025, Ball Corporation streamlined its Middle East portfolio by selling 41% of its stake in Ball United Arab Can Manufacturing Company in Saudi Arabia to ORG Technology for $70 million, while retaining a strategic 10% share to ensure market access. That same month, Ardagh Group secured support from 99% of its senior secured noteholders for a restructuring plan, strengthening its financial position. In July 2025, O-I Glass announced a pivot away from its MAGMA platform, focusing instead on its “Best at Both” strategy to achieve premium output at lower capital intensity. In parallel, Ardagh introduced a 300g lightweight glass wine bottle in Europe, advancing sustainable premium packaging.

Capacity expansion remains a priority. In June 2025, Crown Holdings added a high-speed production line at its Brazil beverage can plant to meet regional demand. Meanwhile, Tetra Pak incorporated certified recycled polymers in its Indian packaging operations in March 2025, aligning with India’s Plastic Waste Management (Amendment) Rules 2022. Structural changes also continue: in February 2025, Smurfit Kappa and WestRock completed their merger, creating a paper-based packaging leader with applications across beverage sectors.

Earlier developments reflect similar momentum. In January 2025, Ardagh announced a long-term partnership with CAP Glass to expand recycling infrastructure in North America. The May 2025 merger of IPL and Schoeller Allibert also reshaped the reusable plastic packaging sector, influencing beverage logistics.

Emerging Trends and Opportunities Defining the Beverage Containers Market

Beverage Containers Market Transforming Through Reusability, Lightweighting, and Smart Recycling

The global beverage containers market is undergoing a structural transformation as producers shift from single-use packaging toward refillable, recyclable, and innovative alternatives. Driven by regulatory mandates, corporate sustainability targets, and consumer expectations, trends such as standardized refillable glass bottle systems and lightweight aluminum cans with higher recycled content are reshaping the industry. At the same time, breakthrough opportunities are arising from fiber-based bottle innovation and the integration of digital watermarks that enable more efficient recycling and supply chain transparency.

Strategic Shift Towards Universal, Refillable Glass Bottle Systems

Refillable glass bottles are gaining renewed prominence as beverage producers embrace circular economy models to address waste reduction and carbon footprint challenges. Unlike proprietary systems, universal bottle designs are being standardized to allow reuse across multiple brands and retailers. Coca-Cola’s commitment to package 25% of its beverages in reusable containers by 2030, supported by a €12 million investment in a new high-speed refillable glass bottling line in Austria, highlights the scale of this transition. Similarly, PepsiCo’s pledge to double refillable bottle sales by 2030 demonstrates industry-wide alignment toward reuse. The environmental impact is profound: the European Commission has reported that reusable glass bottles can reduce raw material demand by 40% and greenhouse gas emissions by 50% compared to single-use bottles. Collaborative initiatives such as Close the Glass Loop, which aims to achieve a 90% recycling rate for glass packaging in Europe by 2030, further underscore the importance of shared industry standards and partnerships. These developments are transforming refillable systems from niche offerings into scalable, mainstream solutions.

Accelerated Lightweighting and Increased Recycled Content in Aluminum Cans

Aluminum cans remain a dominant format in the beverage containers market, but manufacturers are under pressure to reduce their environmental footprint through lightweighting and greater use of post-consumer recycled (PCR) content. The energy savings are substantial: producing aluminum from recycled material consumes up to 95% less energy than using virgin aluminum. In the U.S., state-level mandates in California and Washington require increasing percentages of recycled content in beverage containers, forcing the industry to invest in closed-loop recycling systems. Consumer preferences also amplify this shift online searches for “eco-friendly” and “sustainable” packaging have grown by more than 70% over the past five years, creating a strong pull for PCR content. Beverage leaders are responding by targeting higher recycled material percentages in cans, with several announcing roadmaps to exceed 70% PCR content by 2030. Lightweighting complements this effort by reducing both material usage and Extended Producer Responsibility (EPR) fees while also lowering transport emissions. Together, these strategies ensure that aluminum cans maintain their competitive edge in a circular economy.

Development and Scaling of Fiber-Based Bottle and Can Alternatives

Fiber-based bottles and composite cans are emerging as high-potential alternatives to glass and aluminum, addressing regulatory demands for plastic reduction and corporate goals to cut carbon emissions. Major global brands are actively piloting solutions: Diageo and Pulpex have created a 90% paper-based bottle for Johnnie Walker, marking a milestone for spirits packaging, while Coca-Cola is trialing paper bottles for Adez smoothies. The technical challenge lies in achieving barrier protection against oxygen and moisture without compromising recyclability. Companies such as Paboco (The Paper Bottle Company) are advancing designs with bio-based barriers that separate cleanly during recycling, allowing fiber bottles to enter existing paper waste streams. Life cycle assessments show fiber bottles can cut carbon emissions by up to 90% compared to glass and 30% compared to PET, making them highly attractive for brands under pressure to meet net-zero goals. Commercializing these solutions at scale presents one of the most exciting innovation avenues in beverage packaging.

Integration of Digital Watermarks for High-Speed Sorting and Recycling

Digital watermarking technologies, such as those pioneered under the HolyGrail 2.0 initiative, are creating a paradigm shift in packaging recycling. By embedding invisible digital codes into container artwork, sorting systems equipped with high-resolution cameras can identify material composition with detection rates as high as 99%. This innovation dramatically improves sorting accuracy at Material Recovery Facilities (MRFs), generating purer recycled streams and enabling more food-grade material recovery. The economic impact is equally compelling higher-quality bales of recycled PET or aluminum command premium prices, increasing recycling’s profitability. Digital watermarks also unlock new consumer engagement opportunities, with QR-like functionality enabling brands to share product origin, recycling instructions, and sustainability commitments directly with end users. With over 130 companies, including Nestlé, Unilever, and Procter & Gamble, participating in HolyGrail 2.0, this initiative is rapidly establishing itself as the next standard for circular packaging. Its deployment across beverage containers could redefine global recycling efficiency while simultaneously reinforcing consumer trust in brand sustainability.

Competitive Landscape: Leading Companies in Global Beverage Containers Industry

The global beverage containers market is consolidated around leading multinationals investing in recyclability, lightweighting, and advanced production capabilities. These players are competing on sustainability credentials, global reach, and capacity expansion.

Ball Corporation: Streamlining Portfolio While Championing Aluminum Sustainability

Ball Corporation is a leader in aluminum beverage cans, cups, and bottles. In August 2025, it sold 41% of its Saudi joint venture stake while retaining 10% ownership, reflecting a disciplined, returns-driven approach. Its sustainability agenda is centered on aluminum’s infinite recyclability, with strong investments in regional execution and partnerships such as ORG to maintain growth in high-demand markets.

Crown Holdings Inc.: Expanding Can Capacity in Latin America

Crown Holdings remains a top global player in beverage cans. In June 2025, it added a new high-speed production line in Brazil, underscoring strong demand for carbonated drinks and energy beverages in Latin America. Its “Built to Last” Sustainability Report highlights a sharp focus on recyclable solutions and reducing its carbon footprint. Crown’s strength lies in high-volume, high-quality can production, with expansion plans covering North America, Europe, and emerging markets.

Amcor plc: Diversifying with PET Bottles and Paper-Based Innovations

Amcor plays a major role in PET bottles, closures, and flexible beverage packaging. It is also diversifying with AmFiber™ Performance Paper, a recyclable, high-barrier paper alternative for high-end beverages. In August 2025, Amcor expanded its global network with a new warehouse in Costa Rica, strengthening supply chain capabilities. Its target of 100% recyclable or reusable packaging by 2025 positions it as a sustainability innovator in beverage containers.

Ardagh Group S.A.: Strengthening Glass and Aluminum with Recycling Partnerships

Ardagh supplies glass bottles and beverage cans for beer, wine, and spirits. In August 2025, it secured approval from 99% of noteholders for a recapitalization to improve financial flexibility. It also introduced a lightweight 300g wine bottle in July 2025 and partnered with CAP Glass in January 2025 to expand recycling infrastructure. Ardagh’s dual focus on premium glass innovation and sustainable aluminum cans keeps it central to both premium and mainstream beverage markets.

O-I Glass, Inc.: Focusing on Premium Output with Best at Both Strategy

O-I Glass specializes in glass bottles for alcoholic and non-alcoholic beverages. In July 2025, it announced the suspension of its MAGMA glass-making platform, redirecting efforts to its Best at Both operations strategy, which balances premium output with lower costs. O-I’s strength lies in glass’s premium appeal, recyclability, and brand differentiation value, making it a preferred supplier to global beverage companies seeking upscale positioning.

Beverage Containers Market Share Insights

Bottles Dominate Market Share by Product Type in Beverage Containers

Bottles hold the largest share of the beverage containers market, accounting for 45% of demand, reflecting their unmatched versatility across water, soft drinks, dairy, juices, and alcoholic beverages. PET bottles, in particular, remain the industry’s backbone due to their lightweight structure, clarity, and cost efficiency, while glass bottles continue to secure a stronghold in premium categories such as wine, spirits, and craft beverages. The dominance of bottles is not without challenges: sustainability pressures are forcing a transformation toward high rPET content, lightweighting technologies, and mono-material closures. Meanwhile, glass leverages its “infinite recyclability” and premium perception to preserve relevance in high-value segments. The enduring dominance of bottles illustrates their adaptability in balancing regulatory compliance, consumer convenience, and brand differentiation, even as aluminum cans and alternative formats gain momentum.

Bottled Water Maintains Leading Market Share by End-Use Industry in Beverage Containers

Bottled water represents the largest end-use industry in beverage containers, capturing 25% of the market and serving as the central battleground for packaging sustainability. As regulatory mandates and consumer sentiment challenge the environmental impact of single-use plastics, major global brands are aggressively investing in 100% rPET bottles, lightweight designs, and alternative packaging formats to protect market legitimacy. This category has also catalyzed the entry of aluminum cans into water packaging, positioning cans as a premium, recyclable alternative. The dominance of bottled water highlights the dual challenge for packaging producers: meeting unparalleled production scale and maintaining performance standards, while navigating one of the most scrutinized and politically sensitive packaging categories worldwide.

United States: Rising Sustainability and Smart Packaging Transform the Beverage Container Market

The U.S. beverage container industry is witnessing dynamic growth driven by increasing consumer awareness of sustainability and corporate environmental responsibility. Brands are prioritizing recyclable and reusable packaging solutions for bottled water, soft drinks, and alcoholic beverages to meet eco-conscious consumer demands. A key development in the market is the integration of smart packaging technologies, such as QR codes and NFC chips, allowing consumers to access information on sourcing, recycling instructions, and product authenticity. Major companies, including Diageo, are leveraging these innovations to enhance brand transparency and engagement.

Sustainability initiatives are also reshaping the market. Companies like PepsiCo have transitioned from plastic rings to paper-based packaging for multipacks in the U.S. and Canada, while Coca-Cola has experimented with label-free bottles to reduce carbon emissions. Corporate commitments are further driving adoption, with Coca-Cola pledging to achieve 50% recycled material use and 25% reusable packaging by 2030, highlighting the U.S. market’s focus on lightweight, mono-material, and environmentally friendly beverage containers.

Germany: Deposit-Return Systems and Circular Economy Accelerate Eco-Friendly Beverage Packaging

Germany’s beverage container market is strongly shaped by stringent regulations, including the EU Packaging and Packaging Waste Regulation (PPWR 2025), which mandates fully recyclable packaging by 2030 and sets reuse and refill targets. The country’s well-established circular economy practices include deposit-return schemes (DRS) for plastic bottles and aluminum cans, ensuring high return rates and providing a reliable source of recycled materials for manufacturers.

Technological innovation is a critical driver. For instance, Vetropack Group launched returnable glass bottles made from tempered lightweight glass, which are 30% lighter than standard bottles, enhancing both durability and sustainability. With a strong focus on eco-friendly packaging, German beverage brands are aligning with EU mandates while meeting the growing demand for sustainable and recyclable beverage containers, positioning Germany as a global leader in circular beverage packaging solutions.

China: Green Policies and E-Commerce Expansion Drive Sustainable Beverage Containers

China’s beverage container industry is being reshaped by government initiatives supporting the dual carbon goals of carbon peak and carbon neutrality. Policies restricting the use of non-degradable plastics in the express delivery sector by 2025 are accelerating the adoption of sustainable packaging solutions. Major brands, including Coca-Cola, are responding with label-free bottles, enhancing recyclability and reducing material consumption across the supply chain.

Technological investments, including AI integration and 5G-enabled industrial internet, are optimizing production efficiency and enabling flexible manufacturing of high-quality beverage containers. Additionally, the rapid growth of e-commerce, especially in Tier 2 and 3 cities, is increasing demand for secure, tamper-proof, and recyclable packaging. Combined, these factors position China as a fast-growing market for innovative, environmentally friendly beverage containers.

India: Government Initiatives and Infrastructure Investments Accelerate Sustainable Beverage Packaging

India’s beverage container market is experiencing rapid growth, driven by the Make in India initiative and regulatory support from bodies like the Food Safety and Standards Authority of India (FSSAI). These initiatives encourage local manufacturing, sustainable practices, and innovative packaging solutions. Significant infrastructure investments, such as Ball Beverage’s ₹700 crore aluminum can plant in Telangana and AGI Greenpac’s ₹700 crore container glass facility in Madhya Pradesh, are expanding production capacity and creating direct employment opportunities.

Sustainability remains a critical growth driver. The Plastic Waste Management (Amendment) Rules have fueled demand for eco-friendly and reusable packaging alternatives. In alignment with these goals, PepsiCo India, in collaboration with Varun Beverages and Srichakra Polyplast, launched the country’s first 100% recyclable rPET Pepsi Black bottles, marking a milestone in the adoption of sustainable beverage containers. These developments highlight India’s emergence as a key hub for recyclable, sustainable, and innovative beverage packaging solutions.

Beverage Containers Market Report Scope

Beverage Containers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$30.6 Billion

|

|

Market Size (2034)

|

$49.1 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Material Type (Glass, Plastic, Metal, Paper & Paperboard, Other Materials), By Product Type (Bottles, Cans, Cartons, Pouches, Cups, Other Types), By End-Use Industry (Alcoholic Beverages, Carbonated Soft Drinks, Bottled Water, Juices & Nectars, Dairy Beverages, Other Beverages)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Ardagh Group, Ball Corporation, Tetra Pak, Crown Holdings, Inc., O-I Glass, Inc., Mondi Group, Smurfit Kappa Group, DS Smith plc, WestRock Company, BillerudKorsnäs AB, Canpack Group, Greif, Inc., AGI Greenpac Limited, Elopak ASA

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Beverage Containers Market Segmentation

By Material Type

- Glass

- Plastic

- Metal

- Paper & Paperboard

- Other Materials

By Product Type

- Bottles

- Cans

- Cartons

- Pouches

- Cups

- Other Types

By End-Use Industry

- Alcoholic Beverages

- Carbonated Soft Drinks

- Bottled Water

- Juices & Nectars

- Dairy Beverages

- Other Beverages

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Beverage Containers Market

- Amcor plc

- Ardagh Group

- Ball Corporation

- Tetra Pak

- Crown Holdings, Inc.

- O-I Glass, Inc.

- Mondi Group

- Smurfit Kappa Group

- DS Smith plc

- WestRock Company

- BillerudKorsnäs AB

- Canpack Group

- Greif, Inc.

- AGI Greenpac Limited

- Elopak ASA

* List Not Exhaustive

Methodology

USDAnalytics employed a comprehensive research methodology combining primary interviews, secondary research, and quantitative modeling to deliver a detailed assessment of the global Beverage Containers Market. Primary research involved discussions with key stakeholders, including beverage manufacturers, packaging designers, sustainability specialists, and regulatory experts, to capture current trends, technological innovations, and consumer preferences. Secondary research drew insights from company reports, press releases, trade journals, and regulatory documents, ensuring validation of market dynamics, mergers, acquisitions, and sustainability initiatives. Market sizing and forecasts were derived from historical data, production volumes, consumption patterns, and regional adoption trends across PET, aluminum, glass, aseptic cartons, and emerging fiber-based containers. Segmentation analysis covered material types, product formats, and end-use industries, while qualitative insights focused on premiumization, lightweighting, recyclability, refillable systems, and smart packaging technologies. This methodology emphasizes both sustainability and innovation, providing industry professionals with a precise, data-driven understanding of opportunities, competitive landscapes, and strategic growth drivers through 2034.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.