Composite Cans Market Overview: Expansion Toward $7.9 Billion by 2034

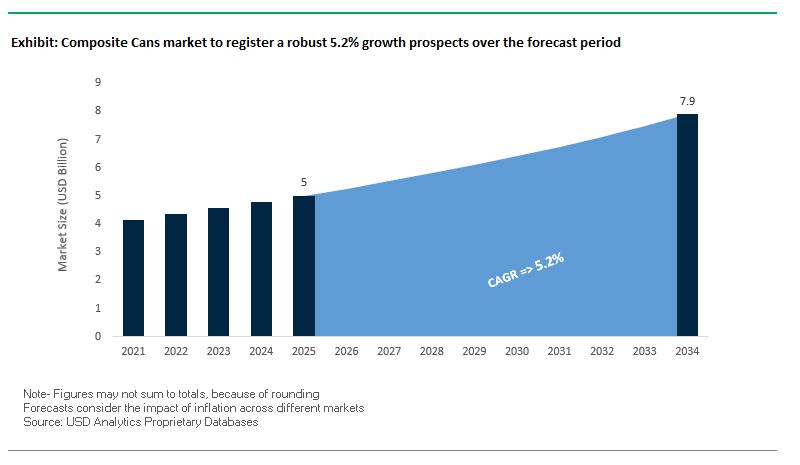

The global composite cans market is projected to grow from $5.0 billion in 2025 to $7.9 billion by 2034, registering a steady CAGR of 5.2%. Composite cans are becoming increasingly critical in packaging due to their high barrier protection, lightweight design, and sustainability advantages over traditional rigid containers. For industry professionals, the key considerations include: How will the demand for recyclable, paper-based cans evolve against metal and plastic formats? How will on-the-go consumption trends shape convenience-focused designs? And what cost and sustainability benefits will lightweighting unlock for global brands?

Key Insights include:

- Product Protection: Around 60% of composite can production is used for dry food packaging such as powdered beverages and snacks, where moisture, oxygen, and light protection are vital.

- Sustainability and Recyclability: The shift toward 100% paperboard composite cans is accelerating, aligning with consumer preference for eco-friendly packaging.

- Consumer Convenience: Over 80% of new snack and instant food launches now integrate easy-open caps, resealable lids, and ergonomic features in composite cans.

- Cost-Effectiveness: Spiral-wound designs and lightweight materials reduce both material usage and transportation costs, making composite cans a competitive alternative to glass and metal containers.

The rising global focus on circular economy, packaging convenience, and cost reduction ensures composite cans will remain a strategic growth area in the packaging industry throughout the next decade.

Market Analysis: Sustainability Investments and Strategic Moves in 2025

The composite cans industry is experiencing sustainability-driven investments, portfolio reshaping, and digital adoption across global supply chains.

In September 2025, a logistics summit emphasized the role of AI and predictive analytics in demand forecasting and inventory management, highlighting its value for composite can supply chains that require just-in-time delivery to brand owners. Earlier, in August 2025, Mondi Group invested in a new biomass power plant in Slovakia, pushing its energy self-sufficiency to 90% and reinforcing its commitment to low-carbon operations.

In July 2025, Greif announced the sale of its Containerboard business for $1.8 billion, a move to strengthen capital efficiency and concentrate on core packaging divisions, including composite cans. In June 2025, Sonoco expanded its U.S. facilities to produce rigid paper cans with paper bottoms, meeting snack food companies’ demand for recyclable alternatives. That same month, Mondi introduced the re/cycle PaperPlus Bag Advanced, showcasing high-barrier paper formats as substitutes for plastic packaging.

In May 2025, Sonoco divested its thermoformed and flexibles business to TOPPAN Holdings, sharpening focus on high-growth packaging solutions. Earlier, in March 2025, Constantia Flexibles merged with Aluflexpack, consolidating its leadership in innovation-driven flexible packaging. In January 2025, Constantia also won two WorldStar Global Packaging Awards for its EcoPeelCover and EcoLamHighPlus, underlining its success in sustainable materials development.

Emerging Trends and Opportunities Reshaping the Composite Cans Market

Strategic Investment in Advanced Recycling Technologies

The composite cans market is undergoing a transformation as manufacturers address one of its most pressing challenges the recyclability of multi-material packaging. Traditionally, composite cans, made from layers of paperboard, foil, and plastic, have been difficult to recycle, resulting in criticism from regulators and sustainability advocates. However, industry leaders are now investing heavily in advanced recycling technologies to close this gap. In May 2024, Saperatec GmbH opened a new industrial-scale facility in Germany dedicated to recycling multi-material packaging waste, including composite films used in beverage cartons and cans. This plant represents a landmark investment, providing scalable solutions for recovering high-value materials from what was previously considered “unrecyclable.” At the same time, initiatives like HolyGrail 2.0, a collaboration involving over 160 global companies, are testing invisible digital watermarks that allow automated sorting of composite cans by material type. With detection rates above 95% in trials, these technologies are paving the way for a more viable recycling ecosystem. As regulations like the EU Packaging and Packaging Waste Regulation (PPWR) enforce recyclability standards by 2030, these innovations are critical for keeping composite cans competitive in sustainable packaging markets.

Material Science Innovation for PFAS Elimination

Another defining trend in the composite cans market is the elimination of PFAS (per- and polyfluoroalkyl substances) from barrier coatings. These so-called “forever chemicals” have long been used to provide grease and moisture resistance in food packaging but are facing mounting regulatory bans and consumer backlash. In February 2024, the U.S. FDA confirmed that PFAS-based grease-proofing agents were voluntarily withdrawn from the American market, following earlier restrictions in states like Washington and Maine. This regulatory pivot has accelerated R&D into safer alternatives, with companies like AGC Chemicals Americas commercializing FibraLAST, a PFAS-free additive that integrates into paper production and offers effective water and oil resistance. By leveraging these non-fluorinated coatings, composite can manufacturers can maintain high-performance barrier properties while meeting stringent food safety and sustainability standards. For food, beverage, and pet food brands seeking PFAS-free labeling, these innovations are rapidly becoming a market requirement rather than an option.

Expansion into Premium and Fresh Food Segments

With advances in barrier coatings and material science, composite cans are now positioned to move beyond traditional dry goods and capture high-value categories such as premium coffee, pet food, and ready-to-drink (RTD) beverages. The development of foil-lined and advanced polymer barrier liners allows composite cans to provide a near-hermetic seal, effectively blocking oxygen and moisture to preserve flavor, aroma, and nutrition. This capability is critical for premium coffee packaging, where freshness defines brand value, and for pet food, where nutrient retention is key for product differentiation. Several global food brands are already trialing composite cans in these segments, citing both sustainability advantages and superior branding potential through customizable labeling and designs. By competing directly with metal and rigid plastic formats, composite cans are opening up a profitable growth path in premium fresh food and beverage markets, where shelf life and brand perception carry significant weight.

Leveraging E-commerce Optimized Structural Design

The e-commerce boom is reshaping packaging priorities, and composite cans are particularly well-suited to thrive in this environment. Their inherent rigidity and lightweight structure make them an ideal e-commerce packaging format that balances product protection with cost efficiency. The ability of composite cans to function as Ships-in-Own-Container (SIOC) eliminates the need for extra corrugated boxes in certain product categories, reducing packaging material and streamlining logistics. This directly translates into lower shipping costs and reduced environmental impact, as lightweight cans consume less fuel during transit compared to glass or metal packaging. Additionally, their cylindrical shape and customizable printed labels enhance the unboxing experience, a crucial differentiator in direct-to-consumer (DTC) models. Studies on e-commerce packaging highlight that attractive, branded packaging elevates perceived product value, positioning composite cans as not only protective containers but also powerful marketing assets. With retailers and D2C brands prioritizing right-sized, efficient, and visually engaging packaging, composite cans stand out as a compelling solution for the digital retail era.

Competitive Landscape: Leading Players Shaping the Composite Cans Market

The composite cans sector brings together global packaging leaders and niche innovators, each leveraging sustainability, material science, and consumer-centric designs to strengthen market share.

Sonoco Products Company drives recyclable rigid paper cans

Sonoco leads in rigid paper containers with solutions like EnviroCan and EnviroSense, known for strong sealing and high barrier protection. In June 2025, the company invested in expanding U.S. facilities to produce recyclable paper-bottom cans, eliminating traditional metal closures. Sonoco’s “Better Packaging. Better Life.” strategy highlights its commitment to monomaterial designs and circular economy goals. Its focus on the North American snack sector positions it strongly in high-growth consumer categories.

Smurfit WestRock focuses on corrugated-based composite packaging

Following the merger of Smurfit Kappa and WestRock, the combined entity delivers paper-based composite packs that reduce reliance on single-use plastics. Its portfolio includes corrugated packaging solutions that replace shrink films and plastic rings in multipacks. With a vertically integrated supply chain from managed forests to final packaging the company ensures sustainability, consistency, and high performance. Smurfit WestRock’s solutions serve beverage, food, and industrial clients, with a strong emphasis on transit protection.

Amcor Plc enhances barrier performance in composite can components

Amcor specializes in supplying liners, peel membranes, and cardboard bases for composite can manufacturers. Its focus on barrier protection and aroma preservation ensures extended product shelf life for powdered beverages, snacks, and spices. Amcor is investing in recyclability-enhancing technologies, including materials compatible with polyolefin recycling streams. Its global footprint and integrated solutions make Amcor a key partner for brands seeking high-performance and sustainable composite can packaging.

Constantia Flexibles Group GmbH expands through acquisitions and innovation

Constantia Flexibles plays a critical role in flexible packaging components for composite cans, including high-barrier films and aluminum closures. In March 2025, it completed its merger with Aluflexpack, expanding its innovation pipeline and European market share. Constantia is recognized for award-winning sustainable solutions such as EcoPeelCover, and has invested in digital printing technologies for faster, more customized packaging. Its strategy emphasizes sustainability, quality, and speed-to-market as competitive differentiators.

Composite Cans Market Share Insights

Metal Ends Dominate Composite Cans Market Share by Closure Type

Metal ends lead the composite cans market with around 50% share in 2025, underscoring their importance as the industry’s gold standard for product integrity and barrier protection. Aluminum and steel ends provide hermetic sealing against moisture, oxygen, and light, which is essential for preserving freshness and extending the shelf life of sensitive food products such as powdered drinks, snack nuts, and infant formula. Their compatibility with high-speed filling and seaming equipment also makes them indispensable in large-scale food and beverage manufacturing. Plastic lids, with 45% share, represent the fast-growing segment, driven by consumer demand for resealability, convenience, and ease of opening. This closure type dominates categories like nutritional powders, protein supplements, and coffee, where products are consumed gradually. Advanced innovations in tamper-evidence and high-barrier plastics are further strengthening its market position. Paperboard ends remain a niche sustainable option, chosen for their recyclability appeal but limited by inferior strength and barrier performance, while specialty closures such as foil membranes and pull-tabs are reserved for premium food and personal care applications. Together, this segmentation highlights how composite can closures are evolving to balance preservation, consumer convenience, and sustainability.

Food & Beverage Drives Composite Cans Market Share by End-Use Industry

The food and beverage sector dominates the composite cans market with a commanding 70% share in 2025, making it the undisputed core application. Composite cans provide the perfect balance of protection, branding potential, and cost-effectiveness for sensitive dry food products like chips, powdered milk, baby formula, frozen juices, and coffee. The format’s ability to incorporate foil barriers while allowing premium printing and customization makes it a shelf-ready packaging solution for global brands. Personal care and cosmetics, accounting for around 15% share, represent a high-value growth area, as composite cans provide a premium natural feel aligned with sustainable and luxury branding. Products such as bath salts, loose powders, and skincare gift sets frequently adopt this packaging, often using plastic lids for resealability and differentiation. Industrial goods use composite cans as a protective workhorse, packaging motor oil, lubricants, adhesives, and abrasive powders that benefit from the cylindrical structure’s stacking strength and crush resistance. Agriculture represents a steady but smaller niche, using composite cans to store and distribute seeds, fertilizers, and pesticides with durability and moisture resistance. Across all segments, the food and beverage industry remains the anchor of global demand, while personal care and industrial applications are expanding composite cans into new premium and functional niches.

United States: Driving Sustainability and Premium Food & Beverage Applications

The United States composite cans market is experiencing a significant shift toward sustainable and recyclable packaging solutions. A key innovation is the development of composite cans featuring fully recyclable paperboard bottoms, replacing traditional metal or plastic ends. This design ensures the entire can is recyclable within the paper stream, aligning with growing consumer demand for eco-friendly packaging and supporting corporate circular economy initiatives.

The adoption of composite cans is particularly strong in the food, beverage, and nutraceutical sectors, where superior barrier protection against oxygen and moisture is crucial for preserving freshness and extending shelf life. Manufacturers are investing in advanced production technologies to enhance barrier performance, improve efficiency, and produce durable packaging suitable for high-value items such as coffee, protein powders, and vitamins. This combination of sustainability, technology, and health-oriented applications is reinforcing the dominance of composite cans in the U.S. market.

China: Industrial Scale and Premium Packaging Driving Market Expansion

China’s composite cans market is propelled by its vast industrial base and expanding consumer class, driving strong demand across food, beverage, consumer goods, and industrial applications. The growth of the middle class is fueling demand for premium packaging solutions that enhance brand recognition and shelf appeal. Composite cans, with their excellent printability and design flexibility, have emerged as a preferred choice for high-quality, consumer-focused products.

The Chinese government’s focus on modernizing logistics and packaging standards is further encouraging adoption, while manufacturers are investing heavily in advanced automated production lines and innovative material formulations. These efforts not only meet rising quality standards but also enable large-scale production to efficiently serve both domestic and international markets.

Germany: EU Regulations and Circular Economy Catalyzing Innovation

Germany’s composite cans market is heavily shaped by European Union sustainability initiatives, including the European Green Deal and the Packaging and Packaging Waste Regulation (PPWR). These policies drive manufacturers to develop recyclable packaging solutions with a high percentage of recycled content, fostering innovation in paper-based composite cans that replace traditional metal or plastic ends and lids.

The country’s strong manufacturing base, particularly in the food, beverage, and industrial sectors, ensures steady demand for high-quality and durable composite cans. German companies are leading the way in creating eco-friendly, cost-efficient packaging while maintaining product protection, demonstrating the successful integration of circular economy principles into commercial applications.

India: Booming Packaged Food Market and Sustainable Packaging Adoption

India’s composite cans market is growing rapidly alongside the country’s packaged food and beverage sector, driven by urbanization, changing lifestyles, and increased demand for convenience and hygiene. Composite cans are increasingly preferred over traditional metal cans and plastic bottles due to their cost-effectiveness, durability, and sustainability.

Indian manufacturers are adopting advanced production technologies such as spiral winding to produce a wide variety of composite cans that meet diverse packaging needs. The focus on eco-friendly solutions combined with innovations in design and manufacturing is enabling the market to cater to both domestic consumers and export opportunities, establishing India as a high-growth region for composite cans.

Japan: Quality, Convenience, and Recycling Shaping Consumer Preferences

The Japanese composite cans market is characterized by a strong consumer preference for high-quality, compact, and aesthetically pleasing packaging. This is particularly evident in the health supplement and premium food segments, where maintaining product integrity and shelf appeal is critical.

Japanese manufacturers are investing in advanced composite materials that offer superior barrier protection to extend shelf life and ensure freshness. Additionally, Japan’s robust recycling infrastructure and national sustainability initiatives are driving the development of recyclable composite cans compatible with local systems, ensuring the packaging meets both environmental and consumer expectations.

Composite Cans Market Report Scope

Composite Cans market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5 Billion

|

|

Market Size (2034)

|

$7.9 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Material (Paperboard, Plastic, Aluminum, Other Materials), By Diameter (Less than 50 mm, 50–100 mm, Above 100 mm), By Closure Type (Plastic Lids, Metal Ends, Paperboard Ends, Other Closure Types), By End-Use Industry (Food & Beverage, Industrial Goods, Personal Care & Cosmetics, Agriculture, Other Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Smurfit Kappa Group plc, Mondi Group, Sonoco Products Company, Greif Inc., Irwin Packaging Pty Limited, Halaspack Packaging Bt., Nagel Paper, Corex Group, Quality Container Company, Hangzhou Qunle Packaging Co., Ltd., PTS Manufacturing Co.Ltd., Heartland Products Group, LLC, CANFAB PACKAGING INC., Star Packaging Company, Zipform Packaging

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Composite Cans Market Segmentation

By Material

- Paperboard

- Plastic

- Aluminum

- Other Materials

By Diameter

- Less than 50 mm

- 50–100 mm

- Above 100 mm

By Closure Type

- Plastic Lids

- Metal Ends

- Paperboard Ends

- Other Closure Types

By End-Use Industry

- Food & Beverage

- Industrial Goods

- Personal Care & Cosmetics

- Agriculture

- Other Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Composite Cans Market

- Smurfit Kappa Group plc

- Mondi Group

- Sonoco Products Company

- Greif Inc.

- Irwin Packaging Pty Limited

- Halaspack Packaging Bt.

- Nagel Paper

- Corex Group

- Quality Container Company

- Hangzhou Qunle Packaging Co., Ltd.

- PTS Manufacturing Co.Ltd.

- Heartland Products Group, LLC

- CANFAB PACKAGING INC.

- Star Packaging Company

- Zipform Packaging

*List not Exhaustive

Research Coverage

This USDAnalytics report investigates the global composite cans market, highlighting recent breakthroughs in barrier technology, material innovation, and sustainable production practices. The analysis reviews historical trends from 2021 to 2024 and provides forward-looking forecasts from 2025 to 2034, emphasizing lightweighting strategies, recyclability advancements, and consumer-driven convenience features. The report highlights key developments in PFAS-free coatings, premium food and beverage adoption, and e-commerce optimized designs, offering actionable insights on cost efficiency, sustainability compliance, and branding potential. By profiling 15+ leading companies and analyzing their innovations in paperboard, aluminum, and plastic components, this report is an essential resource for packaging professionals, brand owners, converters, and investors seeking to understand competitive dynamics, regulatory impacts, and growth opportunities in composite cans. USDAnalytics ensures that decision-makers gain a deep understanding of evolving consumer preferences, circular economy initiatives, and advanced recycling technologies shaping the future of the composite cans market.

Scope Highlights:

- Segmentation: By Material (Paperboard, Plastic, Aluminum, Other Materials); By Diameter (Less than 50 mm, 50–100 mm, Above 100 mm); By Closure Type (Plastic Lids, Metal Ends, Paperboard Ends, Other Closure Types); By End-Use Industry (Food & Beverage, Industrial Goods, Personal Care & Cosmetics, Agriculture, Other Applications).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historical and Forecast Data: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Company Analysis: Detailed insights on 15+ companies, including Smurfit Kappa Group plc, Mondi Group, Sonoco Products Company, Greif Inc., Irwin Packaging Pty Limited, Halaspack Packaging Bt., Nagel Paper, Corex Group, Quality Container Company, Hangzhou Qunle Packaging Co., Ltd., PTS Manufacturing Co. Ltd., Heartland Products Group, LLC, CANFAB PACKAGING INC., Star Packaging Company, and Zipform Packaging.

Methodology

The study employs a comprehensive research methodology combining primary and secondary data collection to deliver accurate market insights. USDAnalytics conducted interviews with industry experts, including manufacturers, suppliers, and end-users, to validate trends in composite cans adoption, sustainability initiatives, and convenience-driven designs. Secondary research included regulatory reports, trade journals, financial statements, and market literature to identify historical growth patterns and strategic developments. Quantitative analysis encompassed market sizing, CAGR calculations, and detailed segmentation by material, diameter, closure type, and end-use industry. Forecasting incorporated scenario modeling that accounts for technological innovation, circular economy adoption, and regional regulations. Competitive intelligence was gathered from company profiles, product launches, mergers, and strategic partnerships, providing a comprehensive view of the global composite cans market landscape.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.