Advanced Composite Materials Market Overview Anchored by High Strength-to-Weight Performance

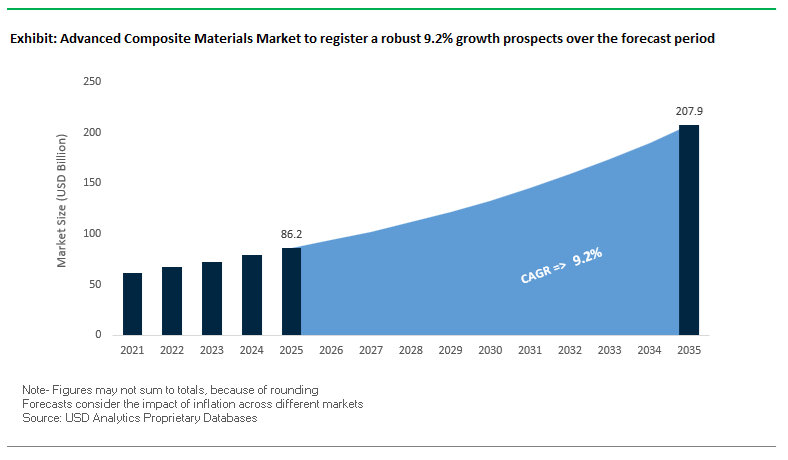

The global Advanced Composite Materials Market is projected to reach USD 86.2 billion in 2025 and is forecast to expand to USD 207.8 billion by 2035, registering a robust CAGR of 9.2% (2025–2035). This growth trajectory is underpinned by accelerating adoption of carbon fiber reinforced polymers (CFRP), glass fiber reinforced polymers (GFRP) and high-performance thermoset/thermoplastic composites in aerospace, wind energy, automotive, civil infrastructure and defense. For manufacturers and material vendors, the market is defined by a clear shift toward lightweighting, corrosion resistance, high strain-rate performance and tightly controlled curing parameters that maximize mechanical properties and laminate quality. OEMs are increasingly demanding integrated composite systems where fiber, resin, prepreg and process parameters are co-optimized to deliver higher fuel efficiency, extended service life and lower lifecycle costs.

Key insights for advanced composite materials manufacturers and vendors:

- Aerospace CFRP strength-to-weight advantage: Carbon fiber reinforced polymers (CFRP) used in commercial aerospace structures (e.g., Airbus A350, Boeing 787) deliver a specific tensile strength 3–5x higher than aluminum alloys while maintaining a density about 60% lower, driving significant fuel efficiency and payload capacity gains.

- GFRP rebars in harsh civil infrastructure: Glass fiber reinforced polymer (GFRP) rebars exhibit corrosion resistance up to 100× greater than steel, making them the preferred civil engineering composite solution for bridges, tunnels and marine structures exposed to chlorides and road salts.

- High-strain-rate performance for crash and defense: Unidirectional glass fiber composites demonstrate a 20–30% increase in dynamic tensile strength at high strain rates (≈40–200 s⁻¹), supporting their use in impact-tough, crash-worthy automotive structures and defense armor systems.

- Process-controlled autoclave curing for aerospace CFRP: Epoxy-based CFRP for aerospace typically requires autoclave curing around 140°C, 120 minutes, and 7 bar, underlining the importance of tightly controlled curing cycles to unlock optimal tensile strength, hardness and laminate integrity.

- System-level optimization imperative: The convergence of aerospace lightweighting, corrosion-free infrastructure, automotive safety, and wind blade upscaling is pushing suppliers to provide complete composite solutions—from fiber and resin chemistries to prepreg formats and automated processing routes.

Market Analysis: Portfolio Reshaping, Capacity Expansion and Sustainable Composite Innovation

The Advanced Composite Materials Industry is in a phase of strategic restructuring and capacity expansion, driven by aerospace, wind energy, automotive and defense applications. In October 2025, Hexcel Corporation announced an accelerated share repurchase (ASR) program of USD 350 million after securing an additional USD 600 million share repurchase authorization, signaling strong confidence in its defense and space composite backlog and its positioning in high-margin structural composites. Earlier, in September 2024, Toray Advanced Composites (TAC) initiated an expansion at its US carbon fiber prepreg facility to boost capacity for bismaleimide (BMI) and cyanate ester resin prepregs, directly aligned with rising demand for high-temperature composite materials in space launch vehicles and advanced aerospace platforms.

Product and process innovation are reshaping competitive dynamics across automotive, industrial and sustainable composites. In July 2025, a leading European prepreg manufacturer launched a thermoplastic composite prepreg line based on PEEK resin featuring a crystallization cycle shortened by 40%, targeting high-volume automotive and rapid-processing applications where cycle time and recyclability are critical. In February 2025, researchers developed a bio-based epoxy resin with tensile strength comparable to petrochemical epoxies and a bio-content exceeding 70%, reinforcing the trend toward sustainable composites without compromising performance. On the wind energy side, June 2024 saw a major blade manufacturer invest EUR 150 million in automated fiber placement (AFP) equipment tailored for large-tow carbon fiber, enabling longer blades, lower weight and higher rotor diameters for next-generation turbines.

Corporate portfolio realignment and policy-driven R&D funding are further shaping the advanced composite landscape. In May 2025, Owens Corning announced the expected closure of the sale of its Glass Reinforcements Business to Praana Group, a segment that generated about USD 1.1 billion in 2024, altering glass fiber market dynamics and allowing Owens Corning to refocus on its insulation, roofing and building materials core. In March 2025, SGL Carbon unveiled a major restructuring of its carbon fibers business unit, closing unprofitable activities to build a profitable core and targeting positive adjusted EBITDA for the segment. Government policy is also pivotal: in April 2025, the US Department of Defense (DoD) awarded multiple contracts totaling over USD 80 million for out-of-autoclave (OOA) prepreg systems to support rapid manufacture of military aircraft components, accelerating innovation in lower-cost, high-rate advanced composite manufacturing. Together, these developments highlight a market moving toward higher performance, lower emissions and faster manufacturing across all major composite value chains.

Breakthrough Production Technologies and Smart Composite Architectures Driving Next-Generation Opportunities

Market Trend 1: Industrialization of High-Rate Deposition (HRD) Technologies Transforming Aerospace Composite Manufacturing Efficiency

A transformative shift is underway as global aerospace OEMs accelerate the adoption of Automated Fiber Placement (AFP) and Automated Tape Laying (ATL) for primary aircraft structures. These technologies directly address the industry's ambition to reduce assembly cycle times, improve production repeatability, and meet rising build-rate requirements for next-generation commercial aircraft platforms. Studies show that AFP/ATL systems can reduce production time for large composite structures by up to 40%, substantially narrowing the gap between composites and metals in high-rate manufacturing environments. With deposition speeds reaching 800–1,000 mm/s, modern multi-tow AFP heads deposit a significantly higher volume of prepreg per hour than manual layup, dramatically boosting throughput for fuselage barrels, wing skins, spars, and control surfaces.

In parallel, AFP/ATL automation reduces recurring part costs by 40–50%, driven by lower labor intensity, tighter dimensional tolerances, and reduced material scrap. Advanced nesting algorithms and precision cutting enhance the buy-to-fly ratio, cutting material waste that has historically been a major cost driver in composite fabrication. As aerospace manufacturers pursue next-generation airframes with higher composite content—particularly for narrowbody aircraft—the industrialization of HRD platforms is becoming a central competitive differentiator. These process advances not only improve productivity but also strengthen quality assurance by eliminating defects associated with manual layup variability.

Market Trend 2: Qualification of Composite Overwrapped Pressure Vessels (COPVs) Enabling High-Pressure Hydrogen Storage in Heavy Mobility

A second major trend reshaping the market is the rapid qualification of Type IV Composite Overwrapped Pressure Vessels (COPVs) for hydrogen-based heavy transport applications, including fuel-cell trucks, buses, rail, mining, and aviation. These vessels, built around a polymer liner reinforced with carbon fiber–epoxy overwraps, must demonstrate exceptional structural integrity at extremely high pressures. For 700-bar systems, COPVs are required to withstand burst pressures of at least 1,575 bar (2.25× NWP) — a critical safety margin achieved through high-performance CFRP layers optimized for hoop strength.

Durability is equally essential. Type IV hydrogen vessels must survive 11,000–22,000 pressure cycles without leakage or failure, meeting global standards such as EC 79 and SAE J2579. These vessels also deliver a service life of up to 30 years, double that of earlier steel-based designs, enabling broader adoption in commercial fleets. Lightweighting is central to hydrogen mobility economics, and carbon fiber composites enable significant gravimetric energy density improvements, helping manufacturers approach DOE targets of 1.8 kWh/kg. As hydrogen mobility gains global momentum, advanced composite materials emerge as foundational enablers for safe, efficient on-board hydrogen storage.

Market Opportunity 1: Commercialization of Reprocessable, Fully Recyclable Thermoset Composites Enabled by Vitrimer Chemistry

Sustainability pressures across aerospace, automotive, and wind energy sectors are opening a major opportunity for vitrimer-based recyclable thermoset composites, which address the historical non-recyclability of conventional epoxy systems. Vitrimers introduce dynamic covalent networks that maintain thermoset-like mechanical performance but become reprocessable at elevated temperatures. Importantly, vitrimer resins that have undergone chemical dissolution and re-crosslinking retain up to 95% of their original tensile strength, enabling closed-loop recycling of structural composites—long considered impractical for thermosets.

Virgin vitrimer systems offer tensile strengths around 50 MPa, squarely within the mechanical range of epoxy systems used in structural composites. Above the topology transition temperature (Tv), vitrimers exhibit rapid stress relaxation within ~3.6 minutes at 180°C, enabling reshaping, welding, repair, and reprocessing without degrading performance. With glass transition temperatures up to 130°C, high-performance vitrimer epoxies can meet the thermal demands of aerospace interiors, automotive structures, and electronic systems. These materials represent one of the most promising pathways toward achieving “zero-waste” composite manufacturing and end-of-life recycling at industrial scale.

Market Opportunity 2: Integration of Functionalized Fibers and Embedded SHM Sensors for Predictive Monitoring in Composite Infrastructure

A high-growth opportunity is emerging in the integration of functionalized reinforcing fibers and embedded sensor networks for predictive Structural Health Monitoring (SHM), especially in civil infrastructure and wind turbine blades. Fiber Bragg Grating (FBG) sensors, when integrated into composite laminates, deliver unparalleled diagnostic accuracy. Using deep learning–enhanced analytics, FBG networks can achieve >99% accuracy in detecting delamination, cracks, and impact damage—an essential capability for composites deployed in bridges, pipelines, aircraft interiors, and offshore structures.

FBG sensors measure strain with high fidelity, showing deviations of less than 6% compared to VIC3D optical systems in uniaxial tests. Their ability to operate at sampling rates up to 1,000 Hz enables real-time monitoring of dynamic loading, vibration, and fatigue-driven degradation. The sensitivity of FBGs allows detection of Barely Visible Impact Damage (BVID), a critical failure mode in fiber-reinforced laminates. As governments and asset owners increasingly deploy smart infrastructure technologies, the integration of SHM-ready composites offers massive potential to extend asset lifespans, reduce inspection costs, and support predictive maintenance models.

Advanced Composite Materials Market Share Analysis

Market Share by Fiber Type: Glass Fiber Composites Dominate Owing to Cost-Performance Advantage and High-Volume Structural Demand

Glass Fiber Composites (GFRP) hold the largest share of the global advanced composite materials market—approximately 50% in 2025—because they deliver the most cost-efficient balance of mechanical performance, durability, and scalability for large-scale industrial applications. As a fraction of the cost of carbon fiber, glass fibers enable mass adoption across sectors that require high-volume, structurally demanding components without incurring prohibitive material expenses. This is especially critical in wind energy, construction, marine, and automotive applications, where GFRP’s high strength-to-weight ratio, corrosion resistance, and excellent fatigue performance make it the default material solution. Mature, automated manufacturing methods—such as pultrusion, filament winding, vacuum infusion, and RTM—further reinforce glass fiber’s dominance by allowing continuous, repeatable, and low-cost production of large composite structures. Enhanced variants like ECR-glass improve chemical resistance and durability, broadening GFRP’s suitability for pipes, tanks, rebar alternatives, and marine components. As the global demand for lightweight, corrosion-resistant materials expands, particularly in renewable energy and infrastructure, GFRP’s unmatched cost-to-performance profile ensures it remains the cornerstone of the advanced composites market.

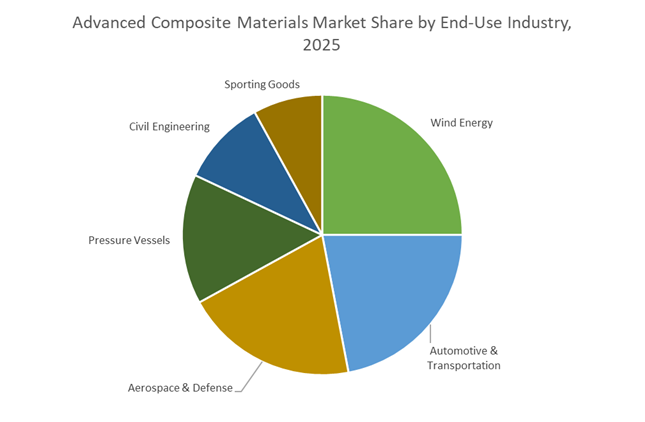

Market Share by End-Use Industry: Wind Energy Leads as Composites Become Essential for Modern, Large-Scale Turbine Blade Manufacturing

The Wind Energy sector accounts for roughly 25% of the global advanced composites market, solidifying its position as the single largest end-user due to the structural and performance-critical role composites play in turbine blade manufacturing. Modern wind turbine blades—often exceeding 70 to 100 meters in length for offshore deployments—must combine low weight, high stiffness, excellent fatigue resistance, and long-term environmental durability. Glass Fiber Reinforced Polymers (GFRP) meet these requirements at scale, making them indispensable for the bulk of the blade structure. As turbine capacities climb to 10–15 MW and blade lengths rise, composite consumption per turbine increases exponentially, intensifying material demand. While carbon fiber is selectively used in spar caps or root reinforcements for ultra-long blades, GFRP continues to dominate due to its economic viability and superior manufacturability in large layup structures. Aggressive global decarbonization efforts, accelerating offshore wind farm installations, and the shift toward larger, more efficient turbines further amplify composite usage. With blades representing up to 70% of a wind turbine’s total composite demand, the wind energy industry remains the driving force behind market expansion and the most influential application segment for advanced composite materials.

Country Analysis: Global Drivers in Advanced Composite Materials Development

United States: Defense-Grade Carbon Fiber, Next-Gen Propulsion Composites, and AFP Automation Expansion

The United States remains the world’s most influential hub for high-performance composite materials, supported by unmatched defense budgets, deep aerospace manufacturing capability, and pioneering investments in Automated Fiber Placement (AFP) and Ceramic Matrix Composites (CMCs). The U.S. Department of Defense continues to sustain long-term demand for specialty composite structures through large procurement cycles for platforms such as the F-35 fighter jet, whose airframe consists of roughly 40% composite content. This alone guarantees multi-year demand for high-modulus Carbon Fiber, advanced prepregs, and toughened epoxy systems engineered to meet stringent hot-wet performance standards. Complementing military demand, Boeing, Lockheed Martin, and Northrop Grumman are expanding AFP production lines—supported by AI-driven AFP systems deployed by Hexcel and Toray Advanced Composites—reducing layup times on large structures by up to 30%. These productivity gains strengthen the U.S. leadership position in wide-body, fighter jet, and rotorcraft composite manufacturing.

Beyond traditional CFRP, the U.S. is broadening its materials base with rapid integration of SiC-based CMCs into next-generation propulsion systems. GE’s GE9X and other demonstrator engines now leverage CMC turbine shrouds, combustor liners, and nozzles capable of operating at temperatures 20% higher than nickel superalloys, contributing to a 12% fuel efficiency improvement in commercial aviation. Meanwhile, U.S. hydrogen mobility initiatives are accelerating the deployment of Type IV composite pressure vessels for heavy-duty FCEVs, with companies like Hexagon Composites expanding U.S. capacity to support domestic clean-transportation adoption. Together, these trends reinforce the United States’ strategic dominance in the high-end Advanced Composite Materials Market across aerospace, defense, spaceflight, and hydrogen energy systems.

China: Wind Blade Megastructures, C919 Localization, and EV Lightweighting at Industrial Scale

China’s Advanced Composite Materials ecosystem is defined by unmatched production scale, strong policy backing, and a fast-evolving industrial base spanning wind energy, electric vehicles, and domestic aerospace. The country leads global wind turbine blade manufacturing, where 100-meter-plus GFRP blades are becoming standard in 2025. These massive structures require enormous volumes of E-Glass, biaxial and triaxial fabrics, hybrid reinforcements, and high-toughness epoxy systems—strengthening China’s position as the world’s largest single market for structural composite materials. In aerospace, China’s push to localize production for the COMAC C919 is accelerating domestic development of aerospace-grade CFRP prepregs, autoclave processing, and non-autoclave composite technologies, reducing reliance on foreign suppliers and building an indigenous composite supply chain.

China’s electric vehicle industry further amplifies composite demand through its rapid adoption of polymer composite battery boxes, underbody impact shields, and frontal crash structures. These components replace traditional steel/aluminum enclosures, delivering major weight reductions while meeting stringent flame-retardant and puncture-resistance performance requirements. Combined with aggressive EV export activity and gigafactory expansions, China continues to be a global powerhouse in high-volume composite materials, particularly for GFRP and automotive CFRP applications.

European Union (Germany/France/UK): Thermoplastic Composites, Circular Recycling, and High-Rate Industrial Manufacturing

Europe stands at the forefront of thermoplastic composite innovation and circularity-driven composite recycling technologies, guided by stringent EU sustainability mandates and an advanced aerospace ecosystem. German automakers are accelerating integration of PEEK- and PPS-based thermoplastic CFRP for crash structures, battery trays, and lightweight subframes to improve recyclability while achieving cycle times under 5 minutes—critical for mass-market automotive platforms. In aerospace, Europe’s leadership is anchored by Airbus, whose A350 uses CFRP for over 50% of its structural weight, driving sustained demand for high-performance prepregs from leaders like Hexcel and Solvay.

Equally important is Europe’s heavy investment in end-of-life composite recycling technologies. Multi-million Euro initiatives (2024–2025) are scaling industrial pyrolysis and solvolysis systems capable of recovering up to 95% of Carbon Fiber from decommissioned aerospace and wind turbine structures. EU R&D centers are also advancing high-pressure Resin Transfer Molding (RTM) and compression molding technologies, enabling large-volume production of structural CFRP components at competitive cost. Europe’s dual focus on thermoplastic composites and closed-loop recycling infrastructure positions the region as a global sustainability leader in Advanced Composite Materials.

Japan: Ultra-High-Modulus Carbon Fiber Leadership and Precision Composite Tooling Innovation

Japan remains the global benchmark for ultra-high-quality Carbon Fiber precursor production and high-modulus fiber performance, with Toray Industries retaining its position as the world leader. Toray’s continuous capital investment—surpassing $100 million across recent years—supports expanded production of PAN-based Carbon Fiber grades like T1100G, widely used in high-stress aerospace structures, defense equipment, and competitive sporting goods. Japan’s expertise in polymer chemistry and precursor stabilization gives its fibers superior tensile strength and consistency, making them indispensable in the elite segment of the global composite materials market.

Japanese manufacturers are also advancing precision composite tooling materials, supporting AFP, automated tape laying (ATL), and additive manufacturing workflows for next-generation aircraft. Innovations in low-expansion tooling prepregs, advanced autoclave tooling systems, and composite mold materials ensure precise curing conditions for large, complex geometries. These advancements bolster Japan’s status as a critical technology supplier across global aerospace, robotics, and electric vehicle composite supply chains.

India: Strategic Defense Indigenization and Emerging Aerospace Testing Infrastructure

India’s Advanced Composite Materials market is expanding rapidly under government-backed “Make in India” mandates targeting defense, aerospace, and strategic materials self-reliance. The Ministry of Defence has released multiple Positive Indigenisation Lists specifying domestic manufacturing requirements for critical composite-rich components, including aramid fiber armor panels, UAV airframes, lightweight composite structures for fighter jets, and next-gen ballistic protection systems. This policy shift is accelerating domestic production partnerships, technology transfer agreements, and local composite fabrication expertise.

India is also building a robust ecosystem for testing, validation, and qualification of advanced composites, supported by newly approved material testing facilities in regions like Uttar Pradesh. These centers focus on mechanical testing, fatigue analysis, thermal cycling, and destructive evaluation of Carbon Fiber, aramid-based composites, and hybrid materials to certify them for aerospace and defense applications. As indigenous aircraft programs (including AMCA, LCA Mk2, and various UAV platforms) advance toward production, India’s composite materials demand is expected to grow sharply across structural, armor, and propulsion-adjacent applications.

Competitive Landscape in Advanced Composite Materials: Global Leaders in CFRP, GFRP and Hybrid Systems

The competitive landscape of the Advanced Composite Materials Market is characterized by a mix of vertically integrated carbon fiber majors, specialty prepreg producers, glass reinforcement specialists and diversified polymer–composite groups. Companies such as Toray Industries and Hexcel anchor the aerospace and defense segment with high-performance CFRP and prepregs, while SGL Carbon is executing a focused transformation of its carbon fiber business. Owens Corning is reshaping its portfolio via divestiture of glass reinforcements, whereas Teijin and Mitsubishi Chemical Corporation (MCC) are leveraging polymer expertise and hybrid fiber systems to scale composites in automotive and industrial applications. Integration across fiber production, resin systems, prepregs, molding compounds and semi-finished products is emerging as a key differentiator in capturing long-term contracts with aerospace OEMs, wind blade manufacturers and Tier-1 automotive suppliers.

Toray Industries: Integrated Carbon Fiber and Prepreg Leader for Aerospace and Wind

Toray Industries, Inc. is a global heavyweight in carbon fiber and advanced composite materials, with a fully integrated value chain from precursor to carbon fiber and prepreg production. Its portfolio spans TORAYCA® carbon fiber, Toray Advanced Composites (TAC) prepregs, and ZOLTEK® large-tow carbon fiber, enabling it to serve both high-end aerospace platforms (e.g., Boeing 787) and cost-sensitive wind energy and automotive structures. Toray’s strategy emphasizes supply chain control and qualification for major aerospace programs, while the ZOLTEK arm focuses on low-cost, large-tow CF to drive high-volume industrial adoption, particularly in wind blades and structural automotive parts. This combination of premium and industrial CF positions Toray as a pivotal supplier in the global advanced composite materials industry.

Hexcel Corporation: High-Performance Aerospace and Defense Composites Specialist

Hexcel Corporation concentrates on premium structural composite materials with a strong focus on aerospace and defense markets. Its key products include HexTow® carbon fiber, HexPly® prepregs, HexMC® molding compounds and advanced honeycomb structures, widely used in programs such as the Airbus A350 and F-35. Commercial aerospace accounts for a substantial share of revenues, with around 65% of Q3 2025 sales tied to this segment, underscoring Hexcel’s reliance on aircraft build rates and fleet modernization. The company’s USD 203 million free cash flow in FY 2024 and the USD 350 million ASR program announced in October 2025 signal strong financial resilience and shareholder-friendly capital allocation, even amid supply chain volatility and evolving composite demand profiles.

SGL Carbon: Restructuring Carbon Fiber Business for Profitable Composite Growth

SGL Carbon SE operates across SIGRAFIL® carbon fibers, SIGRABOND® carbon composites and composite solutions components, with a presence in both high-tech graphite and automotive composite structures. In March 2025, SGL announced an extensive restructuring of its carbon fibers business unit, targeting closure of unprofitable activities and cost savings of around EUR 25 million to return the segment to profitability. This transformation aligns with its ambition to focus on profitable core applications, including EV battery structures and lightweight automotive parts that integrate carbon fiber, graphite, and composite solutions. With a diversified platform, SGL Carbon is repositioning itself as a leaner, more focused player in advanced composite materials, particularly where carbon fiber and graphite technologies converge.

Owens Corning: Composite Technology with Strategic Shift Toward Building Materials

Owens Corning has historically been a critical supplier of glass reinforcements and high-modulus glass fiber products, supporting a broad range of thermoset and thermoplastic composite applications. In May 2025, the company announced the expected sale of its Glass Reinforcements Business to Praana Group, a unit that generated about USD 1.1 billion in 2024, indicating a strategic shift toward its insulation and roofing building materials core. Despite this divestiture, Owens Corning retains patented composite fiber technologies and continues to innovate in sustainable, energy-efficient fiber solutions for construction, infrastructure and industrial markets. Its composite know-how remains central to enabling durable, thermally efficient and structurally robust building systems.

Teijin Limited: Multi-Material Carbon Fiber and Polymer Solutions for Mass-Market Mobility

Teijin Limited is a diversified materials group combining Tenax® carbon fiber, advanced thermoplastic resin products (PP, PC), and prepreg and fabric materials to deliver multi-material composite solutions. The company is strategically scaling mid- to large-volume carbon fiber production and intermediate materials, explicitly targeting automotive mass production with high-performance, short-cycle-time composite solutions. Teijin leverages synergies between its aramid fibers (Twaron, Technora) and polymer expertise to develop hybrid composite architectures that optimize impact resistance, stiffness and weight. This positions Teijin as a key enabler of lightweight, crash-worthy and cost-efficient composites for next-generation mobility platforms.

Mitsubishi Chemical Corporation: Industrial and Automotive Composites with Sustainable Emphasis

Mitsubishi Chemical Corporation (MCC) focuses on industrial and automotive composite materials built around its Pyrofil® carbon fiber, towpregs, carbon fiber sheet molding compounds (CF-SMC) and chopped strands. The company’s strategy centers on developing intermediate CF materials suited for fast, high-cycle-time processes such as SMC and pultrusion, which are crucial for scaling composite adoption in automotive, industrial equipment and infrastructure. MCC is also integrating bio-based resins and recycled carbon fiber into its product portfolio, aiming to deliver lower-embodied-carbon composites that align with OEM sustainability targets. This combination of processing speed, industrial scalability and sustainability focus reinforces MCC’s role within the broader advanced composite materials value chain.

Advanced Composite Materials Market Report Scope

Advanced Composite Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$86.2 Billion

|

|

Market Size (2035)

|

$207.8 Billion

|

|

Market Growth Rate

|

9.2%

|

|

Segments

|

By Fiber Type (Carbon Fiber Composites, Glass Fiber Composites, Aramid Fiber Composites, Hybrid Fiber Composites, Other Fibers), By Matrix Type (Polymer Matrix Composites, Thermoset PMCs, Thermoplastic PMCs, Ceramic Matrix Composites, Metal Matrix Composites), By Manufacturing Process (Prepreg Lay-Up/AFP/ATL, Resin Transfer Molding, Pultrusion & Filament Winding, Compression Molding, Additive Manufacturing), By End-Use Industry (Aerospace & Defense, Wind Energy, Automotive & Transportation, Pressure Vessels, Civil Engineering, Sporting Goods)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Toray Industries, Hexcel, Teijin, Solvay, SGL Carbon, Mitsubishi Chemical Group, Huntsman, Owens Corning, Formosa Plastics, Zoltek (Toray), Gurit, Hexagon Composites, Plasan Carbon Composites, Syensqo, Cytec (Solvay Group)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Advanced Composite Materials Market Segmentation

By Fiber Type

- Carbon Fiber Composites

- Glass Fiber Composites

- Aramid Fiber Composites

- Hybrid Fiber Composites

- Other Fibers

By Matrix Type

- Polymer Matrix Composites (PMCs)

- Thermoset PMCs

- Thermoplastic PMCs

- Ceramic Matrix Composites (CMCs)

- Metal Matrix Composites (MMCs)

By Manufacturing Process

- Prepreg Lay-Up / AFP / ATL

- Resin Transfer Molding (RTM)

- Pultrusion & Filament Winding

- Compression Molding

- Additive Manufacturing

By End-Use Industry

- Aerospace & Defense

- Wind Energy

- Automotive & Transportation

- Pressure Vessels

- Civil Engineering

- Sporting Goods

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Advanced Composite Materials Market

- Toray Industries

- Hexcel

- Teijin

- Solvay

- SGL Carbon

- Mitsubishi Chemical Group

- Huntsman

- Owens Corning

- Formosa Plastics

- Zoltek (Toray)

- Gurit

- Hexagon Composites

- Plasan Carbon Composites

- Syensqo

- Cytec Solvay Group.

*- List not Exhaustive

Research Coverage: Advanced Composite Materials Market

The USDAnalytics Advanced Composite Materials Market study provides a rigorous, data-backed roadmap for decision-makers as this report investigates how CFRP, GFRP, aramid, hybrid and next-generation composite systems are reshaping aerospace, wind, automotive, hydrogen pressure vessels and civil infrastructure value chains. It highlights key demand inflection points such as high-rate AFP/ATL deposition, qualification of Type IV COPVs for 700-bar hydrogen storage, vitrimer-based recyclable thermosets, and SHM-enabled “smart” laminates, while our analysis reviews portfolio restructuring, capex commitments and policy-driven funding that are redefining competitive positioning across regions. The research tracks breakthroughs in high-temperature CMC integration, thermoplastic composite adoption, and circular recycling pathways, connecting material-level advances with build-rate, cost and sustainability metrics at OEM and Tier-1 levels. Covering technology roadmaps, regulatory tailwinds, end-use intensity and supplier strategies, this report is an essential resource for composites manufacturers, fiber producers, resin formulators, part fabricators, investors and policymakers seeking to benchmark their positioning and calibrate growth strategies in the global Advanced Composite Materials Market, with USDAnalytics providing actionable insights at the intersection of performance, manufacturability and lifecycle economics.

Scope Highlights

- Segmentation:

By Fiber Type: Carbon Fiber Composites, Glass Fiber Composites, Aramid Fiber Composites, Hybrid Fiber Composites, Other Fibers

By Matrix Type: Polymer Matrix Composites (PMCs), Thermoset PMCs, Thermoplastic PMCs, Ceramic Matrix Composites (CMCs), Metal Matrix Composites (MMCs)

By Manufacturing Process: Prepreg Lay-Up / AFP / ATL, Resin Transfer Molding (RTM), Pultrusion & Filament Winding, Compression Molding, Additive Manufacturing

By End-Use Industry: Aerospace & Defense, Wind Energy, Automotive & Transportation, Pressure Vessels, Civil Engineering, Sporting Goods

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data from 2021 to 2025 and forecast data from 2026 to 2034.

- Companies Covered: Includes analysis and profiles of 15+ leading players such as Toray Industries, Hexcel, Teijin, Solvay, SGL Carbon, Mitsubishi Chemical Group, Huntsman, Owens Corning, Formosa Plastics, Zoltek (Toray), Gurit, Hexagon Composites, Plasan Carbon Composites, Syensqo and Cytec Solvay Group.