Advanced Composites Market Overview: High-Performance Materials, Rapid Scale-Up & Strategic Procurement Insights

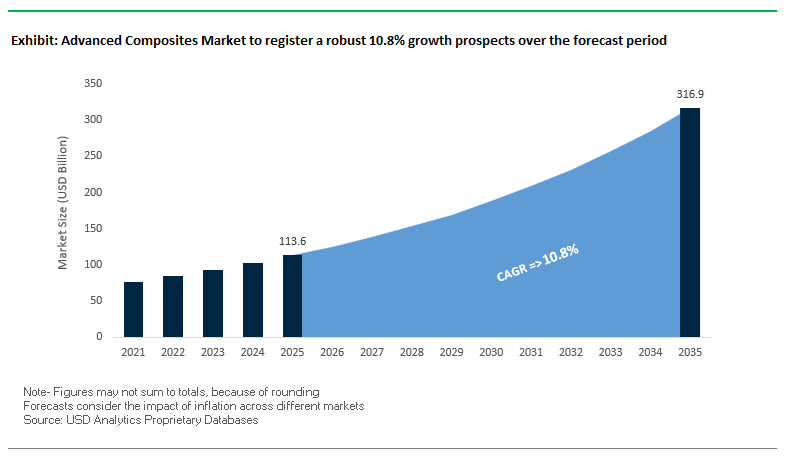

The Advanced Composites Industry, valued at USD 113.6 billion in 2025 and projected to reach USD 316.8 billion by 2035 at a strong 10.8% CAGR, is entering an accelerated growth phase driven by aerospace lightweighting mandates, utility-scale wind energy expansion, automotive electrification, and global defense modernization programs. As carbon fiber, glass fiber, and aramid fiber composites transition from niche engineering materials to mainstream structural solutions, industry leaders are prioritizing high-performance composites that deliver superior strength-to-weight ratios, fatigue resistance, environmental durability, and production efficiency.

Companies that pair material innovation with fast, automated production and robust recycling programs are set to capture the lion’s share of the market’s projected 10.8% CAGR. Strategic buyers and engineering teams increasingly evaluate composite suppliers across three mission-critical dimensions:

- Manufacturing speed, cure-cycle efficiency, and automation readiness to enable high-volume automotive and e-mobility applications;

- Material consistency, fatigue performance, and reliability required for long-service aerospace structures and next-generation 100+ meter wind blades;

- Recycling, circularity, and end-of-life solutions aligned with tightening sustainability regulations and OEM carbon-neutrality commitments.

Technology inflection points such as wide deployment of HP-RTM, compression molding, large-tow carbon fiber, thermoplastic composites, and ultra-fast-curing resin systems—are redefining production economics and expanding composites into markets previously dominated by metals. As a result, Advanced Composites are rapidly becoming the preferred structural alternative for industries seeking lightweighting, energy efficiency, thermal stability, corrosion resistance, and long-term durability, positioning the sector for transformative adoption through 2035.

Key Buyer Insights for Vendors

- Aerospace substitution trend: New-generation commercial aircraft now use >50% CFRP by structural weight, creating urgent demand for automated, high-speed composite manufacturing.

- Wind blade material demands: Offshore blades exceeding 115 m rely on large-tow carbon fiber and S-Glass for stiffness and fatigue resistance over 25+ year asset lives.

- Automotive cure-cycle revolution: Industry benchmark cure times have fallen from hours to <5 minutes via HP-RTM and compression molding, enabling CFRP use in higher-volume vehicle models.

- Defense penetration: Aramid and Ceramic Matrix Composites (CMCs) are specified across 70–80% of new defense platforms for ballistic and high-temperature roles.

- Recycling targets: Joint industry/OEM initiatives aim for an initial 25% aerospace CFRP recycling rate by 2030 via pyrolysis and solvolysis programs.

Market Analysis: Strategic Transactions, Capacity Expansions & Cross-Sector Partnerships

The Advanced Composites market registered a busy sequence of strategic moves that both expand supply capacity and accelerate technology qualification across aerospace, automotive, wind and space sectors. In December 2025, Cambium’s acquisition of SHD Holdings (advised by DLA Piper) materially increases manufacturing footprint across the US, UK and EU, strengthening supply options for aerospace and defense OEMs that require geographically diversified, certified composite suppliers. That consolidation complements Toray Advanced Composites’ NCAMP qualification (November 2025) of Cetex® LMPAEK™ TC1225/T300 thermoplastic composite - a key milestone that makes high-performance thermoplastic fabrics available in the NCAMP database and significantly shortens the certification timeline for certifiable aircraft structures, improving time-to-market for thermoplastic composite usage in primary structures.

Strategic industrial collaborations and long-term agreements show the industry is converging around mobility and space applications. October 2025 saw Hyundai Motor Group and Toray Group deepen cooperation to develop advanced materials for future mobility, directly targeting EV lightweighting and specialized-purpose vehicles. Earlier in July 2025, Toray secured a long-term supply agreement with Airborne Aerospace for space-grade composites to produce solar array substrates for mega-constellation satellites - a clear signal that composites are integral to NewSpace supply chains. Meanwhile, supply-chain circularity gained traction in June 2025 when Toray, Daher and TARMAC Aerosave launched an End-of-Life Aerospace Recycling Program (in collaboration with Airbus) to create closed-loop processing for thermoplastic composites, reflecting OEM pressure to build recycling pathways as production volumes scale.

Public funding and material innovation are also reshaping priorities: March 2025 DoE awards targeted advanced composite manufacturing and high-purity SiC components to secure domestic clean-energy supply chains, while May 2025 collaboration between Solvay and Origin Materials to develop carbon-negative materials points to rising investor interest in sustainable feedstocks. Collectively these developments - acquisitions expanding capacity, thermoplastic qualification accelerating certification, OEM-supplier partnerships for mobility and space, and public funding to onshore critical materials production - are converging to validate the industry’s projected high growth and to shift commercial focus from prototype to high-rate production and circularity.

Major Trends Redefining the Advanced Composites Market

Trend 1: Industrialization of Automated Composite Manufacturing to Enable High-Volume, Cost-Sensitive Applications

One of the most transformative shifts in the advanced composites market is the rapid industrialization of automated manufacturing technologies designed to break the cost barrier that historically limited composite adoption in high-volume sectors such as automotive, consumer goods, and industrial equipment. Traditional hand lay-up processes—long criticized for high labor dependency, slow throughput, and variability—are being replaced by robotic systems that enable consistent, rapid, and scalable production.

Automated Pick & Place systems for composite preforms are delivering 40%–50% reductions in recurring part costs, fundamentally reshaping the economics of carbon fiber reinforced polymer (CFRP) adoption for automotive OEMs. In aerospace and wind energy, Automated Fiber Placement (AFP) systems are achieving continuous deposition speeds of 800–1000 mm/s, allowing large aerodynamic structures and fuselage components to be manufactured at unprecedented throughput levels. Meanwhile, the automotive sector is accelerating the shift to thermoplastic composites such as D-LFT, where cycle times of 60 seconds or less now allow complex structural components to be produced with the volume cadence required for metal replacement.

Trend 2: Circular Material Design and End-of-Life Reform Drive Thermoplastic Adoption and Advanced Recycling Technologies

A second major trend reshaping the advanced composites market is the industry-wide focus on circularity—driven by escalating ESG requirements, EU waste regulations, and the looming disposal challenge as first-generation aircraft and wind turbine blades reach end-of-life. Manufacturers are now designing composite systems with recyclability in mind, developing thermoplastic matrices, recyclable resins, and scalable fiber recovery technologies that can reintegrate recovered materials into new value chains.

Public financing is accelerating this transition. The European Investment Bank’s €25 million funding approval (within a €69 million project) for FAIRMAT’s carbon fiber recycling expansion in France reflects growing institutional commitment to composite circularity. At the same time, pyrolysis-based reclamation technologies are achieving >90% fiber purity with mechanical properties approaching near-virgin performance, making recycled carbon fiber (rCF) competitive for automotive structures and industrial parts. Legislative actions strengthen the momentum: France has already moved to ban composite waste landfilling, and the proposed EU Landfill Directive is pushing the entire European market toward pyrolysis, solvolysis, and closed-loop reprocessing.

As composite waste streams from aerospace and wind power accelerate, recyclable thermoplastics and next-generation resins will become essential for economic and regulatory compliance. Circular design is evolving from an ESG obligation to a structural requirement—and a key differentiator for composite manufacturers competing in global markets.

High-Value Opportunities Emerging in the Advanced Composites Market

Opportunity 1: Thermoplastic Composite Battery Enclosures for Lightweighting, Fire Safety, and EV Platform Scalability

Electrification is creating one of the strongest material innovation opportunities in the composites sector. Battery enclosures now require a unique combination of lightweighting, structural performance, dielectric insulation, and thermal runaway containment—criteria that advanced thermoplastic composites can meet more effectively than metals. Flame-retardant long-fiber reinforced thermoplastics such as LGF-PP and PC-LFT-D have demonstrated the ability to pass UL2596 thermal runaway tests and 1100°C bonfire testing for at least five minutes, even with thin-wall designs of 2–4 mm. This enables safer battery pack designs without resorting to heavy metallic barriers.

Thermoplastic composite trays and covers deliver >25% weight reduction compared to steel alternatives, extending vehicle range and improving energy efficiency—critical performance metrics for EV platforms. Beyond simple material substitution, leading suppliers such as SABIC and Trinseo are advancing halogen-free, intumescent thermoplastic FR systems that integrate electrical insulation, thermal insulation, and fire resistance into a single multifunctional material. This integrated design capability simplifies assembly, reduces part count, and accelerates OEM platform development.

As EV manufacturing scales globally, thermoplastic composites will become foundational to the next generation of battery enclosure architectures, offering OEMs a combination of safety compliance, mass reduction, and manufacturability that metals cannot achieve.

Opportunity 2: Next-Generation Composite Materials for High-Pressure Hydrogen Storage Vessels (Type IV & Type V Tanks)

Hydrogen mobility—spanning heavy-duty trucks, buses, trains, and future aviation concepts—is creating a high-value, high-growth opportunity for advanced composite manufacturers as the industry shifts toward lightweight, high-pressure storage technologies. Type IV vessels, featuring polymer liners fully wrapped in carbon fiber composites, represent the current commercial benchmark due to their exceptional weight efficiency and performance. These tanks achieve a gravimetric storage density of ~40 g/L at 700 bar, a figure approximately 160% higher than Type III metal-lined alternatives. This performance advantage is essential for enabling commercially viable hydrogen range in mobility applications.

The full composite overwrap in Type IV tanks allows safe storage at 700 bar, directly supporting the operating requirements of heavy-duty hydrogen vehicles. Even more transformative is the weight saving: carbon fiber reinforced Type IV tanks deliver up to 70% weight reduction compared to traditional all-metal Type I and Type II tanks. This magnitude of mass optimization is critical for hydrogen-powered trucks and buses, where payload and efficiency determine operating economics.

As mobility sectors accelerate hydrogen adoption and governments fund fueling infrastructure, demand for high-performance composite vessels will intensify. Future Type V (linerless) all-composite tanks, still in development, will push weight reduction even further—positioning carbon fiber composites as indispensable materials for the global hydrogen economy.

Advanced Composites Market Share Analysis

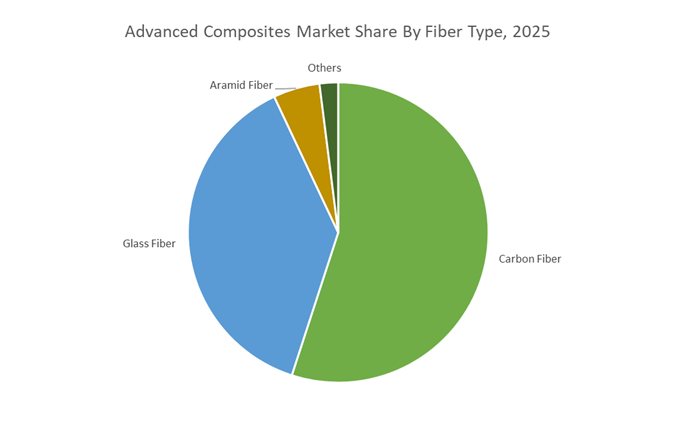

Market Share by Fiber Type: Carbon Fiber Leads with 55.8% Share

Carbon Fiber dominates the Advanced Composites Market with a commanding 55.8% share in 2025, reflecting its position as the industry’s highest-performance and highest-value reinforcement material. Its dominance is anchored in superior specific strength, stiffness, fatigue resistance, and lightweighting capability, making it indispensable for aerospace structures, EV platforms, high-performance sports equipment, industrial automation, and next-generation wind turbine blades. The segment’s strong market share is reinforced by two structural drivers: the industrialization and cost reduction of carbon fiber manufacturing, which is enabling adoption beyond aerospace, and the rapid acceleration of the renewable energy and EV transition, which depends on carbon-intensive composite architectures for efficiency gains. The broader fiber ecosystem highlights a bifurcated market landscape—glass fiber remains the volume leader for cost-sensitive, large-scale applications such as construction, transportation, and marine; aramid fibers hold a specialized, mission-critical niche in ballistic protection and defense systems; and hybrid and natural fibers contribute to sustainability and cost optimization in emerging applications. This segmentation reflects a clear trend in the composites industry: carbon fiber driving high-value innovation, while glass fiber anchors high-volume market expansion.

Market Share by Matrix Type: Thermoset PMCs Lead with 62.3% Share

Polymer Matrix Composites (PMC) based on thermoset resins command 62.3% of the market in 2025, underscoring their long-standing position as the structural backbone of composite manufacturing. Thermoset PMCs dominate due to decades of engineering validation, mature curing processes, superior mechanical performance, and widespread qualification across aerospace, automotive, wind, marine, and industrial sectors. Their chemical crosslinking provides exceptional dimensional stability, chemical resistance, and fatigue performance—properties that remain unmatched in many mission-critical applications. However, the matrix landscape is undergoing a transformative shift: thermoplastic PMCs are rapidly gaining momentum as the industry targets higher production rates, automated processing, weldability, and recyclability for mass-market automotive and consumer applications. Meanwhile, ceramic matrix composites (CMCs) represent the cutting-edge performance frontier, enabling ultra-high-temperature operation in turbine engines, hypersonic systems, and advanced propulsion technologies. Metal matrix composites (MMCs) also hold relevance for wear-resistant, high-stiffness applications. Collectively, the matrix evolution highlights a broader structural transition toward faster-cycle, greener, and extreme-environment composite systems, while thermoset PMCs retain their dominant share due to deep industrial integration and certified reliability.

Country Analysis: Global Advanced Composites Market Innovation Hubs

United States: Advancing Aerospace-Grade Composites, Defense Materials, and High-Rate Automated Manufacturing

The United States remains the global epicenter for high-performance composite materials, supported by federal programs, strong aerospace and defense demand, and increasing automation across composite manufacturing lines. The Department of Defense’s DPA Title III awards, totaling $33.5 million in late 2025, highlight an urgent national priority to expand the domestic solid rocket motor (SRM) industrial base. These programs rely heavily on carbon–carbon composites and structural composites essential for propulsion systems, hypersonic platforms, and next-generation defense technologies. Meanwhile, Hexcel Corporation’s expansion of its Americas aerospace distribution network demonstrates accelerating demand for carbon fiber, honeycomb core, and prepreg materials across commercial aviation, rotorcraft, and military aircraft production.

The US is simultaneously reinforcing its leadership in next-generation composite engineering through DARPA-funded R&D programs aimed at strengthening the advanced manufacturing workforce and enhancing the digital infrastructure required for precision composite fabrication. Automation is rapidly scaling, with companies like Firefly Aerospace deploying advanced co-development and automated production lines for the Antares 330 and MLV launch vehicles. These facilities rely on proprietary lightweight composite structures, showcasing the shift toward high-rate composite manufacturing. Product innovation remains strong as Hexcel introduced the Flex-Core® HRH-302 mid-temperature honeycomb, a BMI-compatible core that improves thermal stability for new aerospace thermal-management architectures. This evolving ecosystem positions the US as a global leader in aerospace composites, defense materials engineering, and high-rate composite manufacturing technologies.

China: Expanding Domestic Composite Capacity Through Localization, Lightweighting, and Green Development

China’s advanced composites market is undergoing rapid expansion, driven by national directives for self-sufficiency in carbon fiber, thermoplastic composites, and high-strength lightweight materials. The 14th Five-Year Plan (FYP) is central to this transformation, emphasizing low-carbon industrial development and promoting extensive composite adoption across mobility, renewable energy, and infrastructure. Lightweight composites are becoming integral to the country’s decarbonization roadmap, particularly in transportation systems that must reduce emissions ahead of China’s 2030 carbon-peaking goal.

A major enabler is China’s $1.4 trillion digital infrastructure plan, accelerating the adoption of smart factories, 5G-enabled Industrial IoT systems, and automated composite manufacturing workflows. This digital shift is improving quality control, reducing scrap, and scaling throughput for thermoplastic composite components used in New Energy Vehicles (NEVs). As NEV manufacturers push for extended driving range and improved crash performance, demand is rising for CFRP battery enclosures, structural thermoplastics, and hybrid composite-metal assemblies. China’s investment in high-speed rail and bridge infrastructure is also expanding the use of GFRP reinforcements and pultruded structural composites, favored for their long-term durability and significantly reduced maintenance requirements. With aligned industrial policy, strong government funding, and enormous domestic market demand, China is rapidly positioning itself as a central hub for carbon fiber production, green composite technologies, and transportation lightweighting solutions.

European Union (Germany/UK/France): Clean Aviation and Sustainable Composite Materials Market

Europe—led by Germany, France, and the UK—continues to accelerate its transition toward sustainable composite materials aligned with the EU’s climate-neutral ambitions. The European Commission’s €2.9 billion Innovation Fund allocation to 61 net-zero technology projects in 2025 directly supports advanced composite recycling technologies, renewable feedstocks, and clean manufacturing pathways for lightweight materials used in aviation, automotive, and industrial applications. The Horizon Europe program, with a budget of €93.5 billion (2021–2027), fuels collaborative research across universities, OEMs, and material suppliers, including major “clean aviation” moonshot initiatives focused on next-generation composite airframes, ultra-efficient wings, and high-rate automated production lines.

Sustainability commitments are reshaping material production, demonstrated by Toray Carbon Fibers Europe’s mass balancing certification, which validates the use of recycled and biomass-derived precursors in carbon fiber manufacturing—a significant shift toward circular composites. Europe also retains global leadership in renewable energy composites, especially through large-scale offshore wind deployment requiring some of the world’s largest and most complex glass fiber and carbon-glass hybrid turbine blades. These megastructures necessitate heavy investment in infusion technologies, precision molding, and structural composite innovation. Collectively, Europe’s climate-driven funding, strong R&D networks, and industrial commitments position the region as a global leader in sustainable advanced composites and clean aviation materials.

South Korea: Leadership in Hydrogen Composite Pressure Vessels and Fuel-Cell Mobility Structures

South Korea’s advanced composites strategy is strongly aligned with its national hydrogen roadmap and leadership in next-generation automotive and fuel-cell technologies. The country is rapidly scaling production of Type IV composite pressure vessels, which rely on ultra-light CFRP liners for hydrogen storage at high pressures—critical for fuel-cell vehicles, hydrogen transport, and refueling infrastructure. South Korea aims for a substantial expansion in hydrogen-powered mobility and infrastructure by 2040, underpinning enormous long-term demand for high-strength composite tanks.

South Korea is also strengthening its position in global hydrogen materials through strategic collaborations. Umoe Advanced Composites (UAC) showcased its hybrid Type IV cylinders at the World Hydrogen Expo 2025, highlighting the country’s growing ecosystem of hydrogen-centric composite technologies. Simultaneously, companies like Hyundai are accelerating development of fuel-cell trams, hydrogen buses, and advanced mobility platforms, each requiring lightweight, structurally efficient composite frames and enclosures. South Korea’s deep expertise in automotive engineering, combined with its aggressive hydrogen transition policies, is propelling the nation into a leadership role in hydrogen storage composites and advanced mobility materials.

Japan: High-Modulus Carbon Fiber Excellence and Composite Recycling Innovation

Japan continues to set global benchmarks in high-performance carbon fiber production, specialty prepregs, and composite lifecycle technologies. Toray Composite Materials America, utilizing its TORAYCA® high-modulus carbon fiber platform, remains a central supplier to aerospace OEMs seeking exceptional stiffness, fatigue resistance, and proven flight performance. Japan’s advanced composite manufacturers are deeply integrated into international commercial aviation and defense programs, maintaining stringent quality and performance standards across airframe, interior, and propulsion applications.

Sustainability is becoming a critical pillar of Japan’s materials strategy. Japanese suppliers are investing heavily in recycling technologies for CFRP waste, addressing rising environmental regulations and end-of-life vehicle (ELV) requirements. These initiatives focus on cost-effective pyrolysis processes, resin recovery systems, and bio-based resin platforms to enable circular composite economies. By combining world-leading carbon fiber production with technological innovation in recycling and reclaimed composite reprocessing, Japan is ensuring long-term competitiveness in both high-performance aerospace composites and sustainable material systems.

Competitive Landscape: Differentiation by Scale, Certification & Circular Capabilities

The Advanced Composites competitive field is defined by several structural axes: raw material control (carbon/aramid fiber supply), proprietary prepreg and resin chemistry, certification track record for aerospace and automotive, high-rate automation capabilities, and leadership in recycling or closed-loop programs. Market leaders combine broad R&D teams with global manufacturing footprints and strategic OEM partnerships that secure long-term offtake for high-value programs.

Toray Industries, Inc. - Market leader in carbon fiber and integrated composites with a clear push into future mobility

Toray dominates high-performance carbon fiber (Torayca®) and both thermoset and thermoplastic prepregs, supplying aerospace, wind and mobility sectors. The company is actively redirecting R&D and production capacity toward EV lightweighting, hydrogen storage tanks and UAM (urban air mobility) while leveraging a global R&D base of 3,500 personnel. Toray’s recent NCAMP qualification activities and participation in industry recycling initiatives demonstrate its dual focus on certification speed and circularity, solidifying its role as the tier-1 partner for large structural programs.

Hexcel Corporation - Structural composites specialist focused on aerospace, space & defense with lean product concentration

Hexcel concentrates on advanced structural composites - carbon fiber, honeycomb cores and prepregs - to serve commercial aerospace and defense prime contractors. Strategic corporate restructuring and focused R&D (notably consistent quarterly R&D investments) sharpen its product portfolio around high-value aircraft and space programs, and Hexcel’s materials remain integral to major airframe platforms where fatigue performance and certification pedigree are critical.

Teijin Limited - Multi-material systems provider combining carbon and aramid fibers for automotive and defense

Teijin distinguishes itself through a broad fiber portfolio (Tenax™ carbon fiber; Twaron/Technora aramids) and an emphasis on digital transformation (AI/ML in R&D) to accelerate multi-material solutions. The company’s push into sustainable automobiles and integration of high-speed curing prepregs supports its strategy to make composites viable for higher-volume automotive applications while retaining strong footholds in defense and industrial markets.

Solvay - Thermoplastics and renewable-carbon platforms targeting sustainable lightweighting

Solvay excels in thermoplastic composites and specialty polymers for aerospace and automotive customers. Its Renewable Materials & Biotechnology platform and commitment to scale renewable carbon share (65% sustainable solutions target by 2030) align Solvay with OEM decarbonization goals. Strategic partnerships with air mobility and sustainable aviation developers position Solvay as a materials-innovation partner for next-generation, low-carbon composite solutions.

Gurit Holding AG - End-to-end composite systems specialist for wind and marine with sustainable core materials

Gurit focuses on structural core materials, kitting and systems integration for wind blades and marine composites, investing in petrochemical-free core foams and recyclable blade solutions. Its end-to-end offering (materials, tooling, kitting) allows quick ramping of blade production lines and supports OEMs aiming for long-blade, low-lifecycle-cost installations in offshore wind projects.

Owens Corning - Glass-fiber reinforcement scale and infrastructure penetration for high-volume markets

Owens Corning provides high-performance glass fiber reinforcements and building materials that serve as cost-effective composite substitutes across infrastructure, automotive and industrial applications. Its strategic expansion of high-performance glass fiber lines and large-scale manufacturing footprint make it a reliable, lower-cost partner for commodity and engineered composites where glass fiber remains the preferred reinforcement for corrosion resistance and cost optimization.

Advanced Composites Market Report Scope

Advanced Composites Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$113.6 Billion

|

|

Market Size (2035)

|

$316.8 Billion

|

|

Market Growth Rate

|

10.8%

|

|

Segments

|

By Fiber Type (Carbon Fiber, Glass Fiber, Aramid Fiber, Boron Fiber, Natural/Bio-Fibers, Hybrid Fibers), By Matrix Type (Polymer Matrix Composites, Ceramic Matrix Composites, Metal Matrix Composites), By Product/Form (Prepregs, Composite Components, Filament, Bulk Molding Compound, Sheet Molding Compound, Core Materials), By Manufacturing Process (Automated Fiber Placement, Automated Tape Laying, Resin Transfer Molding, Vacuum Assisted Resin Transfer Molding, Pultrusion, Autoclave Curing, Compression Molding, Filament Winding, Additive Manufacturing), By End-Use Industry (Aerospace & Defense, Wind Energy, Automotive & Transportation, Marine, Construction & Infrastructure, Sports & Leisure, Pressure Vessels)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Toray Industries Inc., Hexcel Corporation, Teijin Limited, SGL Carbon, DuPont de Nemours Inc., Solvay SA, Owens Corning, Mitsubishi Chemical Group Corporation, BASF SE, Aerojet Rocketdyne, Gurit Holding AG, Huntsman Corporation, Plasan Carbon Composites, Spirit AeroSystems, Hexion Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Advanced Composites Market Segmentation

By Fiber Type

- Carbon Fiber

- Glass Fiber

- Aramid Fiber

- Boron Fiber

- Natural/Bio-Fibers

- Hybrid Fibers

By Matrix Type

- Polymer Matrix Composites (PMC): Thermoset

- Polymer Matrix Composites (PMC): Thermoplastic

- Ceramic Matrix Composites (CMC)

- Metal Matrix Composites (MMC)

By Product / Form

- Prepregs

- Composite Components

- Filament

- Bulk Molding Compound

- Sheet Molding Compound

- Core Materials

By Manufacturing Process

- Automated Fiber Placement

- Automated Tape Laying (ATL)

- Resin Transfer Molding (RTM)

- Vacuum Assisted Resin Transfer Molding (VARTM)

- Pultrusion

- Autoclave Curing

- Compression Molding

- Filament Winding

- Additive Manufacturing / 3D Printing

By End-Use Industry

- Aerospace & Defense

- Wind Energy

- Automotive & Transportation

- Marine

- Construction & Infrastructure

- Sports & Leisure

- Pressure Vessels

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Advanced Composites Market

- Toray Industries, Inc.

- Hexcel Corporation

- Teijin Limited

- SGL Carbon

- DuPont de Nemours, Inc

- Solvay SA

- Owens Corning

- Mitsubishi Chemical Group Corporation

- BASF SE

- Aerojet Rocketdyne

- Gurit Holding AG

- Huntsman Corporation

- Plasan Carbon Composites

- Spirit AeroSystems

- Hexion Inc.

*- List not Exhaustive