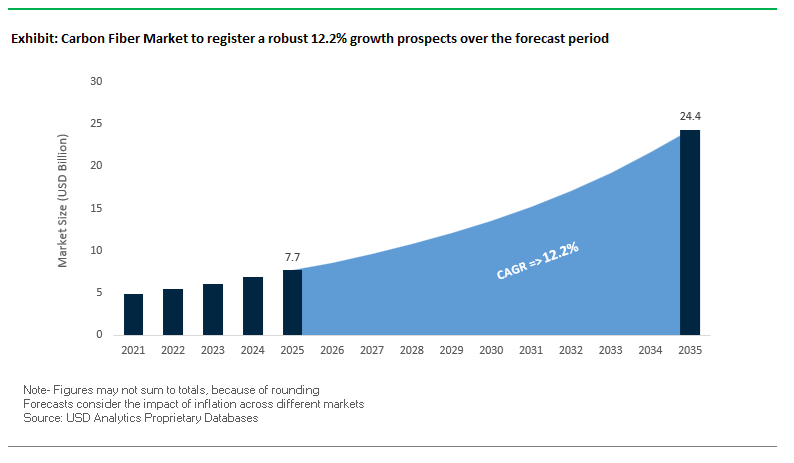

The global carbon fiber market is projected to grow from USD 7.7 billion in 2025 to USD 24.3 billion by 2035, reflecting a strong CAGR of 12.2% (2025–2035). The growth is anchored in PAN-based carbon fiber performance gains, aggressive capacity expansion in Europe and Asia, and fast-rising adoption in hydrogen mobility, commercial aerospace, wind energy and high-end automotive lightweighting.

The recent news flow in the global carbon fiber industry points to three dominant themes: circularity and recycling, capacity expansion and application diversification, and the institutionalization of a European industrial base. In November 2025, the European Composites Industry Association (EuCIA) launched Carbon Fiber Europe, a dedicated sector alliance aimed at strengthening industrial resilience, sustainability and circularity across the regional carbon fiber and composites ecosystem. The policy and advocacy layer complements technical advances including Toray’s October 2025 announcement of a chemical recycling technology capable of decomposing diverse CFRP waste from aircraft and wind turbines while retaining over 95% of original fiber strength—a step-change for carbon fiber recycling economics. In September 2025, Asahi Kasei further reinforced the circularity narrative by preparing to unveil a CFRP recycling technology for continuous carbon fibers from pressure vessels at K 2025, using electrolyzed sulfuric acid decomposition, directly aligning with hydrogen tank and pressure-vessel markets.

On the production and application side, the market narrative in 2025 is dominated by capacity expansions and new high-throughput product forms. Toray Industries announced in March 2025 a 20% carbon fiber capacity expansion at its French facility (Société des Fibres de Carbone S.A.), increasing medium- and high-modulus output to 6,000 tons/year by 2025, directly supporting aerospace and high-end automotive OEMs. In September 2025, the Brembo–SGL Carbon Ceramic Brakes (BSCCB) joint venture expanded carbon ceramic brake disc production capacity by 50% at its plants in Germany and Italy, underlining how high-performance automotive components are becoming a mainstream volume outlet for carbon fiber–based ceramics. Hexcel added more value-added capability in February 2025 with the launch of HexPly™ M949 cosmetic finish prepreg, engineered to deliver Class A interior and exterior carbon parts free of white spots and pinholes with a 150°C glass transition temperature, targeting the premium automotive exterior and interior trim segment.

Sustainability-driven innovation is also shaping the product roadmap and brand positioning of key suppliers. Teijin Carbon launched Tenax Next™ HTS45 E23 24K in March 2025, a sustainable carbon fiber filament yarn offering a 35% reduction in CO₂ emissions relative to conventional fibers, responding to OEM Scope 3 disclosure and low-carbon material requirements. In parallel, Teijin and A&P Technology introduced High-Performance BIMAX TPUD Braided Fabric in November 2025, a thermoplastic unidirectional (TPUD) braided fabric optimized for scalable composite manufacturing and faster cycle times in automotive and industrial applications, reinforcing the trend toward automation-friendly thermoplastic composites. Earlier, in January 2025, Hexcel and FIDAMC announced a strategic collaboration to accelerate R&D on next-generation composite materials and advanced manufacturing technologies for aerospace and industrial markets, matching material developments with process innovation. Finally, Toray’s October 2024 forecast that carbon fiber demand for Type IV hydrogen tanks will approach 40,000 tons by 2025, mainly from commercial fuel-cell truck OEMs, encapsulates the structural pull from the hydrogen mobility segment that is central to most long-term capacity plans.

For industry professionals and OEM buyers, the key strategic questions are shifting from “Can carbon fiber meet performance needs?” to “How fast can low-cost, circular, high-modulus carbon fiber scale for structural and energy applications without supply risk?”

R&D benchmarks including Toray’s 7.677 GPa tensile strength and 362 GPa modulus demonstrate how far PAN-based carbon fiber can push the performance envelope for next-generation aerospace and defense platforms. Further, European capacity expansion from 5,000 to 6,000 metric tons/year by 2025 shows that leading producers are preparing for sustained demand from commercial aircraft and premium automotive programs. On the cost side, the drop in Chinese industrial-grade carbon fiber prices from USD 33/kg in 2022 to USD 18/kg in 2023 is structurally changing project economics, enabling wider use in pressure vessels, infrastructure, sporting goods and industrial components. Parallel advances in CFRP recycling technology—including Toray’s process that recovers fiber with over 95% of virgin strength—are critical for meeting OEM circularity targets in wind turbine blades and aircraft component end-of-life strategies. Finally, Toray’s forecast that carbon fiber demand for Type IV hydrogen storage tanks could grow 42% per year to about 40,000 tons by 2025 confirms the explosive pull from the hydrogen mobility market, particularly commercial fuel-cell trucks.

- Performance ceiling: PAN-based carbon fiber has reached 7.677 GPa tensile strength / 362 GPa modulus in R&D, setting the reference benchmark for aerospace-grade and defense carbon fiber qualification.

- European supply resilience: Toray’s 1,000 metric ton/year expansion (to 6,000 tons/year by 2025) strengthens European high-modulus carbon fiber supply for aircraft and premium automotive programs.

- Circular CFRP economics: New chemical recycling routes recovering >95% of virgin fiber strength are making CFRP recycling viable for wind and aerospace end-of-life components.

- Industrial grade price reset: Domestic Chinese carbon fiber prices falling from USD 33/kg to USD 18/kg have intensified global carbon fiber USD/kg price competition, encouraging broader industrial adoption.

- Hydrogen storage pull: Carbon fiber demand for Type IV hydrogen tanks growing at 42% per year toward 40,000 tons underscores the strategic importance of hydrogen mobility pressure vessel composites.

Trends & Opportunities: Data-Driven Strategic Shifts Shaping the Global Carbon Fiber Market

Trend 1: Strategic, High-Volume Commitments by Legacy Automotive OEMs to Carbon Fiber for Structural BEV Components

Battery Electric Vehicle (BEV) platforms are now entering a lightweighting race, where carbon fiber transitions from niche applications in supercars to structural, safety-critical, and mass-manufactured components, such as structural battery enclosures (SBEs), cross-car beams, and body-in-white reinforcements. This evolution is backed by formalized manufacturing partnerships and long-term material procurement strategies.

Key industry-defining developments include:

- OEM–supplier strategic alliances, exemplified by Hyundai Motor Group’s cooperation with Toray Industries, which focuses on integrating advanced CFRP technologies into next-generation BEVs to improve energy efficiency, crashworthiness, and structural performance.

- Substantial weight reduction capabilities, with Carbon Fiber Reinforced Polymers (CFRPs) delivering approximately 20% lower weight than aluminum and titanium in automotive structures-directly improving BEV driving range and offsetting battery mass.

- Manufacturing breakthroughs such as Automated Fiber Placement (AFP) and Resin Transfer Molding (RTM), which have reduced CFRP cycle times by nearly 30%, making carbon fiber viable for high-volume automotive part production rather than limited-run premium vehicles.

- Superior crash safety, where CFRP’s high-impact energy absorption brings a measurable safety advantage, reinforcing OEM adoption for protective structures around battery packs and occupant cells.

This trend reflects carbon fiber’s evolution from a high-performance material to a mainstream structural enabler for mass-market BEVs.

Trend 2: U.S. Qualification of Domestic, Non-Aerospace-Grade Carbon Fiber for Defense and Infrastructure Applications

In response to geopolitical and supply chain vulnerabilities, U.S. legislation is actively supporting the domestic manufacturing of commercial-grade carbon fiber, shifting away from reliance on aerospace suppliers and foreign sourcing. This shift creates a new tier of volume-driven carbon fiber demand across civil infrastructure, utility hardening, and non-critical defense structures.

Key policy- and performance-backed developments include:

- Defense Community Infrastructure Program (DCIP), which allocated ≈$396 million across 78 projects (FY 2020–2024) to enhance infrastructure resilience-projects where CFRP-based strengthening solutions are increasingly deployed.

- Infrastructure Investment and Jobs Act (IIJA) mandates state-level Carbon Reduction Strategies, creating new policy-aligned pathways for CFRP adoption in bridge rehabilitation, transportation networks, and load-bearing civil infrastructure.

- Heavy-tow carbon fiber material validation, where government studies confirm that textile-precursor-derived heavy-tow fibers outperform legacy commercial carbon fiber on a cost-specific-strength basis, supporting their use in non-aerospace applications.

- Domestic supply chain oversight, with agencies such as the Bureau of Industry and Security actively monitoring critical materials availability to secure long-term carbon fiber access for defense missions, grid modernization, and public infrastructure.

This trend highlights a rapid expansion of non-aerospace domestic carbon fiber use cases, driven by policy incentives and national security considerations.

Opportunity 1: Large-Tow, Cost-Efficient Carbon Fiber for Wind Turbine Blade Spar Caps

Wind turbine scale-up-where blade lengths routinely exceed 80 meters-is creating a significant commercial opportunity for large-tow, low-cost carbon fiber as the material of choice for spar caps, the single most structurally demanding blade element.

Industry-shaping performance and economic benchmarks include:

- Mass reduction of up to 25%, achieved when replacing fiberglass with carbon fiber in spar caps, reducing loads on turbine towers, nacelles, and foundations.

- Cost-performance superiority, as DOE analyses show blades using heavy-tow (e.g., 50K) large-tow carbon fiber reduce material costs by 40% versus baseline commercial carbon fiber while maintaining structural stiffness.

- Major energy production gains, with longer CFRP-reinforced blades (51–75 meters) delivering up to 25% higher Annual Energy Production (AEP) by reducing deflection and maximizing aerodynamic efficiency.

- Extended operational lifespan, with CFRP components achieving 20% longer service life and reducing maintenance costs by up to 25% in high-cycle wind environments.

This opportunity aligns with global wind turbine expansion and the trend toward multi-megawatt platforms (4.5 MW and above), positioning carbon fiber as a top-tier structural material for renewable infrastructure.

Opportunity 2: High-Conductivity, Continuous Carbon Fiber Composites for EV Battery Thermal Management and High-Voltage Platforms

As EVs shift to 800V architectures and faster charging rates, battery thermal control becomes a critical reliability and performance differentiator. This enables a new market segment for thermally conductive continuous carbon fiber composites, engineered not only for mechanical strength but also for enhanced heat dissipation.

Key research-backed performance metrics include:

- Breakthrough through-thickness thermal conductivity, where vertically oriented graphene nanoflakes (GNFs) boost CFRP thermal conductivity by 56%, solving a major bottleneck for composite battery enclosures.

- Battery efficiency improvements, with robust thermal management systems improving energy retention by 10–30% and boosting power density by 15–25%, enabling longer range and faster charging.

- Phase Change Material (PCM) hybridization, where adding carbon fibers to PCMs can reduce peak battery temperature rise by up to 45%, a major gain for thermal safety.

- Multifunctional composite casings, where CFRC panels infused with graphite-based resins maintain peak temperatures of only ≈68.3°C under 5V DC, combining thermal control, mechanical protection, and EMI shielding in a single component.

Carbon Fiber Market Share Analysis

Market Share by Product Form: Continuous Carbon Fiber Leads Due to Structural Performance Requirements in High-Load Applications

Continuous carbon fiber accounts for 48% of the market share, driven by its unmatched ability to convert carbon fiber’s inherent mechanical superiority into high-performance composite structures across wind energy, aerospace, automotive, sports equipment, and industrial applications. Unlike chopped or short fiber forms, continuous fibers maintain their structural integrity along the entire length of a component, enabling engineers to precisely control fiber orientation for anisotropic reinforcement, which is critical in applications requiring extreme stiffness and strength. This ability to align fibers with load paths allows continuous carbon fiber composites to achieve 10–20× higher tensile strength and significantly higher modulus values than discontinuous fiber composites, making them indispensable in safety-critical systems such as wind turbine spar caps, aerospace wing skins, fuselage panels, and pressure vessels. Their contribution to 25–60% weight reduction compared to traditional metal structures directly supports global lightweighting strategies that aim to improve fuel efficiency, structural efficiency, and energy generation performance. Continuous fibers also enable consistent load transfer, superior fatigue resistance, and reduced deflection in long-span components—performance requirements that chopped fibers cannot meet. As industries accelerate toward larger-scale, more efficient systems—particularly mega wind turbines and next-generation aircraft—the demand for continuous carbon fiber continues to climb, cementing its position as the dominant product form in the global carbon fiber market.

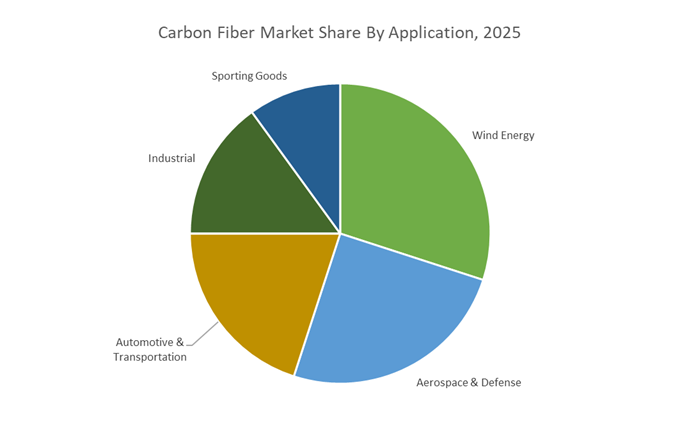

Market Share by Application: Wind Energy Dominates as Carbon Fiber Becomes a Structural Necessity for High-Capacity Turbines

Wind energy represents 30% of the total market share, making it the largest and fastest-growing application segment for carbon fiber due to the material’s direct impact on turbine efficiency, blade durability, and Levelized Cost of Electricity (LCOE). Modern wind turbine blades exceed 70–80 meters in length, and further scaling toward 100 meters in offshore turbines demands materials with exceptional stiffness-to-weight ratios—capabilities uniquely fulfilled by carbon fiber. In these massive blades, the spar cap is the primary load-bearing element, and carbon fiber’s superior modulus prevents excessive blade deflection, which could otherwise lead to catastrophic tower strikes in high-wind environments. The ability of carbon fiber to increase blade length without compromising structural integrity directly amplifies Annual Energy Production (AEP), as even a modest increase in blade length yields a disproportionately larger sweep area and electricity output. Additionally, offshore wind installations rely heavily on carbon fiber because it reduces the overall blade mass, lowering gravitational loads and improving fatigue life under harsh marine conditions. The sector’s rapid adoption trajectory—rising from ≈45% of blades incorporating carbon fiber in 2023 to an estimated 70% by 2028—illustrates a structural shift in turbine manufacturing strategies, where carbon fiber is no longer an optional high-performance upgrade but a core enabling material for meeting global renewable energy expansion targets.

Country Analysis: Global Carbon Fiber Production and Innovation Hubs

China – High-Performance Carbon Fiber Capacity Expansion and Domestic Substitution Strategy

China is rapidly solidifying its dominance in the global carbon fiber market, driven by extensive investments in high-performance carbon fiber technologies and an urgent national strategy to reduce reliance on imported aerospace-grade materials. A landmark example is Sinofibers Technology’s CNY 1.4 billion (USD 190 million) investment (June 2025) to construct a new facility in Changzhou capable of producing 2,000 tons per year of space-grade carbon fibers. This expansion directly supports China’s aerospace, aviation, and wind energy industries—sectors that require ultra-high-performance CFRPs and historically depended on foreign suppliers. The initiative marks an essential phase in strengthening China’s domestic advanced materials sovereignty.

A major competitive strength for China is its aggressive movement toward upstream-to-downstream vertical integration, with Sinofibers expanding its Polyacrylonitrile (PAN) precursor capacity alongside downstream carbon fiber fabrics. This integrated expansion is fully aligned with the national Made in China 2025 roadmap, which identifies New Materials, Aerospace, and Aviation as strategic priority sectors. As a result, China is not only scaling its production capacity but is also actively positioning its local manufacturers as global competitors in high-performance CFRP applications and wind turbine structural components. The combination of scale, policy backing, and integrated manufacturing places China at the forefront of global carbon fiber capacity growth.

Japan – Technological Leadership, High-Coercivity Fiber Development, and Advanced CFRP Recycling

Japan continues to lead the global high-modulus and high-strength carbon fiber market, supported by decades of innovation in precursor chemistry, fiber tow technology, and the development of ultra-high-modulus pitch-based carbon fibers. Japan’s technological edge is further evident in its leadership in sustainable CFRP recycling, highlighted by Toray Industries’ breakthrough low-temperature chemical recycling process (October 2025). This technology recovers carbon fibers from diverse waste streams while retaining over 95% of the tensile strength of virgin fiber—an achievement that positions Japan as the world’s innovation center for circular carbon fiber technologies.

Japan’s recycling advancements extend directly into value-added products. Toray successfully converted the recovered fibers into a high-functionality nonwoven fabric, exhibiting properties suitable for radio frequency shielding and structural aesthetics, showcased in a concept vehicle by Mazda at the 2025 Japan Mobility Show. Japan’s scaling commitments are also expanding internationally: Toray’s $366 million investment (May 2024) to increase production capacity at its Gumi, South Korea plant from 4,700 tons to 8,000 tons annually underscores its role as a global supplier. Meanwhile, Japanese companies like Teijin and Showa Denko retain leadership in the specialized pitch-based carbon fiber segment, critical for satellites, robotics, and high-rigidity structural applications. This combination of recycling innovation, advanced fiber technology, and global capacity expansion ensures Japan’s continued influence across high-end aerospace and industrial carbon fiber markets.

United States – Aerospace-Grade Composite Leadership and Domestic Supply Chain Strengthening

The United States remains a core global hub for aerospace-grade carbon fiber composites, supported by its strong defense sector, commercial aviation ecosystem, and extensive federal initiatives aimed at securing an independent advanced materials supply chain. A key milestone was Tex Tech Industries’ acquisition of Fiber Materials Inc. (FMI) for USD 165 million (January 2025), strengthening the U.S. portfolio in thermal protection systems and high-performance composite structures for space, missile defense, and hypersonic applications. This acquisition reinforces the U.S. strategic objective of expanding domestic capabilities in mission-critical carbon fiber composites.

The U.S. is also accelerating innovation in manufacturing cost reduction and production efficiency. 4M Carbon Fiber’s plasma oxidation project (November 2024)—a 50-ton/year qualification line funded through a $4.5 million program—demonstrates a disruptive approach to reducing the energy-intensive precursor oxidation phase, which historically represents one of the highest cost components in carbon fiber manufacturing. Meanwhile, the U.S. maintains a strong pipeline of long-term aerospace contracts, such as Hexcel Corporation’s major supply agreement with Dassault for the Falcon 10X program, marking the first use of high-performance CFRPs in the jet’s main wing. Together, these developments position the U.S. as a leader in aerospace composites, domestic supply chain security, and next-generation carbon fiber production technologies.

Germany / Europe – Circular Carbon Fiber Economy and Automotive Lightweighting Acceleration

Europe is emerging as a leading force in circular carbon fiber recycling, advanced lightweighting for electric mobility, and sustainable composite manufacturing. The region’s policy-driven market is guided by stringent environmental regulations and EU circular economy goals. A flagship initiative is the LIFE CFCycle project, which aims to industrialize the recycling of at least 2,000 tonnes of CFRP scrap per year by 2027, collected from automotive parts, wind turbine blades, and aircraft structures. This initiative exemplifies Europe’s transition toward a closed-loop carbon fiber supply chain that limits waste while reducing dependence on virgin materials.

In high-performance automotive applications, Europe is advancing sustainable composite integration. Mercedes’ announcement (March 2025) that its W16 Formula 1 car will include sustainable carbon fiber composites marks a significant milestone for motorsports and future EV platforms. Additionally, Europe is expanding manufacturing capacity: Apply Carbon (France) invested heavily in a 16,500 m² facility capable of producing 2,500+ metric tons per year of recycled carbon and aramid fibers, positioning Europe as a top supplier in the recycled composites market. These developments reinforce Europe’s status as an innovation leader in sustainable carbon fiber materials for electric vehicles, wind power, and next-generation industrial applications.

Competitive Landscape: Global Leaders Scale High-Performance, Sustainable and Hydrogen-Ready Carbon Fiber

The global carbon fiber market is dominated by a concentrated group of technology-intensive producers—Toray Industries, Hexcel Corporation, Teijin Limited, SGL Carbon SE, and Mitsubishi Chemical Group—that control critical IP, precursor capacity, and downstream composite know-how. Their competitive edge comes from high-strength PAN- and pitch-based carbon fiber portfolios, deep integration into aerospace, defense, hydrogen storage, wind energy and automotive programs, and growing investments in recycling, low-CO₂ fibers and thermoplastic composite technologies. For OEMs, selecting partners among these leaders is increasingly about aligning with hydrogen mobility roadmaps, regional supply security, and circularity targets, in addition to traditional metrics including tensile strength, modulus and cost.

Toray remains the benchmark for high-performance PAN-based carbon fiber in the global market. The company’s flagship T1100G fiber delivers a guaranteed tensile strength of 7.0 GPa, while its R&D capabilities have pushed the performance ceiling to 7.677 GPa, setting the standard for aerospace-grade carbon fiber in next-generation aircraft and defense systems. Strategically, Toray is heavily focused on hydrogen mobility, projecting 42% annual growth in carbon fiber demand for Type IV hydrogen storage tanks, with demand expected to reach around 40,000 tons by 2025 as commercial fuel-cell truck platforms scale. To support the, Toray is executing a European high-modulus expansion plan, increasing medium- and high-modulus capacity in France by 1,000 tons/year to 6,000 tons/year by 2025, enhancing supply security for European OEMs. The company also leads on circularity, having developed chemical recycling technology that recovers fibers from CFRP waste with more than 95% of virgin strength, positioning Toray as a preferred partner for sustainable carbon fiber and CFRP recycling solutions.

Hexcel is a core structural composites supplier to the commercial aerospace and defense sectors and a pivotal player in the global carbon fiber market. The company estimates that its backlog with Airbus and Boeing programs (A350, 787) equates to around USD 10 billion in future commercial aerospace sales, underscoring long-term demand visibility for its carbon fiber prepregs and structures. From a strategic perspective, Hexcel is strengthening defense resilience, reporting 7.6% year-over-year sales growth in its Defense, Space & Other segment in Q2 2025, with exposure to more than 100 defense programs, including advanced aircraft and space systems. On the product front, Hexcel’s HexPly™ M949 cosmetic finish prepreg—launched in February 2025—provides Class A automotive interior and exterior carbon parts with a 150°C glass transition temperature and defect-free visual appearance, expanding its footprint in premium automotive composites. The company is also committed to sustainability, targeting 75% of its R&T projects to deliver measurable sustainability benefits by 2030, whether through low-impact materials, recycling processes, or energy-efficient manufacturing.

Teijin is a key competitor in the high-tensile strength (HTS) and intermediate modulus (IMS) carbon fiber segments with its Tenax™ portfolio. Products including Tenax™ HTS40 (around 4.0 GPa strength) and Tenax™ IMS (about 5.5 GPa strength) are widely used in aircraft structures and wind energy applications, making Teijin a critical supplier to OEMs seeking high fatigue resistance and stiffness. In March 2025, Teijin expanded its sustainable product offering with the launch of Tenax Next™ HTS45, a filament yarn delivering roughly 35% lower CO₂ emissions than conventional alternatives through the use of circular feedstock, aligning with decarbonization targets. The company also advances thermoplastic composite technology, partnering with A&P Technology to launch BIMAX TPUD Braided Fabric in November 2025, a thermoplastic unidirectional braided material tailored for high-volume, automation-friendly composite part manufacturing in automotive and industrial markets. Teijin’s commitment to the aerospace supply chain is reinforced by achieving Nadcap certification for its carbon fiber production in July 2025, confirming compliance with stringent global aerospace quality assurance standards.

SGL Carbon has carved out a strong position as a high-rate carbon fiber component manufacturer for the automotive industry, while also diversifying into energy storage and industrial applications. A flagship example is its production of 500,000 composite leaf springs annually for Volvo 60 and 90 series models, where parts are approximately 65% lighter than steel and demonstrate the scalability of automated carbon fiber component manufacturing. Through its Brembo SGL Carbon Ceramic Brakes (BSCCB) joint venture, SGL expanded carbon ceramic brake disc production capacity by 50% in September 2025 at sites in Germany and Italy, reinforcing its leadership in high-performance automotive brake systems. In June 2025, SGL broadened its portfolio by launching a carbon fiber battery felt for redox flow batteries, signaling a strategic move beyond structural composites into advanced energy storage materials. The company’s quality credentials are underlined by receiving the Ford Q1 award in May 2025, recognizing SGL as a top-tier supplier of automotive composite components and validating its manufacturing and quality systems for global OEMs.

Mitsubishi Chemical Group differentiates itself through leadership in pitch-based carbon fibers and advanced composite processing technologies. Its DIALEAD™ pitch-based fiber range offers ultra-high modulus grades exceeding 500 GPa and high thermal conductivity variants, making it the material of choice for satellite structures, precision instruments and thermal management applications in aerospace and electronics. In December 2025, the group showcased Kyron™ ULTRA thermoplastic carbon fiber composite prepreg, designed for high-speed manufacturing of e-mobility structures, supporting OEM demand for lightweight yet mass-producible EV components. Mitsubishi also promotes Fusion Core Molding (FCM) technology, which enables the manufacture of complex 3D hollow carbon fiber parts, supporting lightweighting in sports goods, industrial equipment and mobility structures without compromising mechanical integrity. From an environmental standpoint, the company is actively developing bio-resin composites, including plant-derived epoxy resin/carbon fiber materials, and spotlighted both these and its CFRP recycling technology at SAMPE Japan 2025, aligning the DIALEAD and thermoplastic platforms with the global shift toward low-carbon and recyclable composite systems.

Carbon Fiber Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.7 Billion

|

|

Market Size (2035)

|

$24.3 Billion

|

|

Market Growth Rate

|

12.2%

|

|

Segments

|

By Precursor Type (PAN-Based Carbon Fiber, Pitch-Based Carbon Fiber, Rayon-Based Carbon Fiber), By Tow Size (Small Tow, Large Tow), By Modulus Type (Standard Modulus, Intermediate Modulus, High Modulus, Ultra-High Modulus), By Product Form (Continuous Carbon Fiber, Chopped/Milled Carbon Fiber, Carbon Fiber Fabric/Nonwoven, Carbon Fiber Prepreg), By Application (Aerospace & Defense, Wind Energy, Automotive & Transportation, Industrial, Sporting Goods), By Fiber Type (Virgin Carbon Fiber, Recycled Carbon Fiber)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Toray Industries Inc., Hexcel Corporation, Teijin Limited, Mitsubishi Chemical Group, SGL Carbon SE, Solvay S.A., ZOLTEK Corporation, Hyosung Advanced Materials Corp., DowAksa, Formosa Plastics Corporation, China National Bluestar Group, Sinofibers Technology Co. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Carbon Fiber Market Segmentation

By Precursor Type

- PAN-based Carbon Fiber

- Pitch-based Carbon Fiber

- Rayon-based Carbon Fiber

By Tow Size

- Small Tow (< 24K filaments)

- Large Tow (> 48K filaments)

By Modulus Type

- Standard Modulus (SM)

- Intermediate Modulus (IM)

- High Modulus (HM)

- Ultra-High Modulus (UHM)

By Product Form

- Continuous Carbon Fiber

- Chopped/Milled Carbon Fiber

- Carbon Fiber Fabric/Nonwoven

- Carbon Fiber Prepreg

By Application

- Aerospace & Defense

- Wind Energy

- Automotive & Transportation

- Industrial

- Sporting Goods

By Fiber Type

- Virgin Carbon Fiber

- Recycled Carbon Fiber (rCF)

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies: Key Carbon Fiber Producers and Integrators

- Toray Industries, Inc.

- Hexcel Corporation

- TEIJIN LIMITED

- Mitsubishi Chemical Group

- SGL Carbon SE

- Solvay S.A.

- ZOLTEK Corporation

- Hyosung Advanced Materials Corp.

- DowAksa

- Formosa Plastics Corporation

- China National Bluestar (Group) Co., Ltd.

- Sinofibers Technology Co., Ltd.

*- List not Exhaustive