Market Overview: Lightweight Materials Are Converting Mass Reduction into Energy, Cost, and Emissions Advantage at System Scale

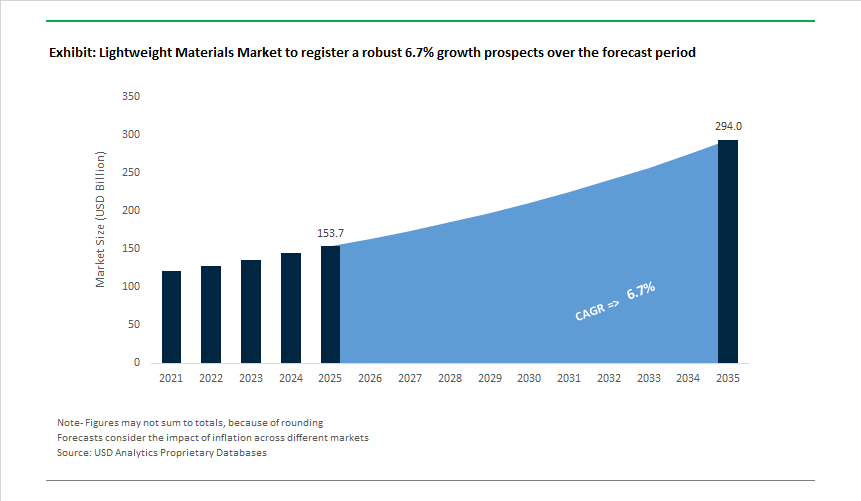

The Lightweight Materials Market reaches USD 153.7 billion in 2025 and is projected to expand to USD 294 billion by 2035, growing at a 6.7% CAGR as mass reduction becomes one of the most immediate and quantifiable levers for decarbonisation and performance improvement across transportation, aerospace, industrial equipment, and energy systems. Unlike longer-horizon fuel or chemistry transitions, lightweighting delivers instant benefits: lower energy demand, extended component life, and reduced operating cost - all without changing the underlying energy source.

The commercial logic is fundamentally arithmetic. In electric vehicles, a 10% reduction in vehicle mass delivers roughly a 13-14% improvement in driving range, allowing OEMs to either extend range without increasing battery size or reduce battery capacity while maintaining performance - both outcomes directly lowering cost and lifecycle emissions. As a result, lightweight materials are increasingly treated as battery enablers. Substituting steel with aluminum in closures such as doors, hoods, and tailgates can reduce component mass by up to 50%, offering a low-risk pathway to meaningful weight reduction on existing vehicle platforms without wholesale architectural redesign.

Material selection strategies are becoming more nuanced rather than purely substitutional. Ultra-high-strength steels (UHSS) now account for more than 60% of Body-in-White structures, as they allow thickness reductions of up to 40% while preserving crash performance and manufacturability within established stamping lines. In parallel, advanced polymers and fiber-reinforced composites are being deployed selectively in areas where stiffness-to-weight, corrosion resistance, or part integration provide outsized benefits. In aerospace, where weight penalties compound over decades of service, sustained adoption of carbon-fiber composites and lightweight alloys is structurally unavoidable as the industry works toward long-term targets requiring approximately 75% CO₂ reduction per passenger-kilometer by mid-century.

Circularity and embodied carbon are now shaping demand alongside mass reduction. Recycled aluminum has emerged as one of the most powerful decarbonisation tools in lightweighting strategies, requiring roughly 95% less energy and generating ~95% lower CO₂ emissions than primary aluminum production. This positions secondary aluminum as a strategic material aligned with OEM emissions reporting, regulatory compliance, and Scope 3 reduction commitments. As procurement teams increasingly evaluate materials on a lifecycle basis, lightweight solutions that combine mass reduction with low embodied carbon are gaining specification priority.

Market Analysis: Capacity Builds, Product Launches and Policy Nudges Shaping Demand

The last 18 months show converging supply-side investments, product innovation for additive manufacturing, and national policy nudges to shore up domestic capability. February 2025 saw Alleima launch a TD high-temperature alloy for aircraft components using metal additive manufacturing - a pointer to metal-AM enabling lightweight complex parts. June 2025 ArcelorMittal Nippon Steel India commissioned a new Continuous Galvanizing Line (CGL) at Hazira to produce Advanced High-Strength Steel (AHSS) up to 1180 MPa, expressly targeting automotive lightweighting requirements. Closely following that, July 2025 ArcelorMittal introduced a new UHSS product line in North America for EV safety and weight reduction programs.

Materials and sustainability announcements accelerated in late 2025. August 2025 Sandvik launched Osprey MAR 55 tool-steel powder for AM, improving precision and eco-efficiency in aerospace manufacturing. September 2025 Novelis published a 2025 Sustainability Report noting a 10% reduction in GHG intensity year-on-year and a target of 75% average recycled content by 2030, highlighting the aluminum circularity push. Also in September 2025, Hexcel and HyPerComp unveiled an Advanced Composite Pressure Vessel (CAMX 2025) aimed at hydrogen storage, showing composite lightweight materials moving into clean-energy storage. October 2025 Hexcel reported Q3 2025 sales of US$456.0 million with Defense, Space & Other up 13.3% YoY, underlining demand for composites in high-performance programs. Policy and incentive activity (e.g., November 2025 India PLI for Specialty Steel) further signal national strategies to localize advanced-material supply chains.

Lightweight Materials Market Trends and Opportunities

Multi-Material Integration for Battery Electric Vehicle (BEV) Platforms

Automotive OEMs are decisively moving away from monolithic steel body strategies toward hybrid lightweight architectures that integrate aluminum, advanced high-strength steel (AHSS), and composites. This transition is driven by the reality that large-format EV battery packs typically add 25–30% additional vehicle mass, creating an urgent need for compensatory lightweighting elsewhere in the platform.

According to technical assessments referenced by National Highway Traffic Safety Administration, advanced lightweight materials can deliver 20–50% weight reduction in Body-in-White (BiW) structures versus mild steel, while still meeting 5-star crashworthiness requirements. This capability has become essential as OEMs attempt to balance range, safety, and structural rigidity in skateboard EV architectures.

Aluminum is emerging as the backbone of this strategy. Data cited by European Aluminum indicates that average aluminum content in electric passenger vehicles is approaching 250–300 kg per unit, largely concentrated in battery enclosures, subframes, and crash management systems. Aluminum’s ~40% mass advantage over steel, combined with superior thermal conductivity, makes it particularly well suited for battery cooling and structural integration.

At the premium and performance end of the market, Carbon Fiber Reinforced Plastics (CFRP) are being deployed selectively to offset battery weight in passenger cells and structural pillars. Case studies from the BMW i-series architecture demonstrate 40–50% weight savings versus steel in targeted zones. Crucially, advances in Resin Transfer Molding (RTM) and automation are reducing cycle times, bringing CFRP-based hybrid designs closer to scalable EV production rather than niche luxury applications.

Qualification of TiAl and CMCs for Next-Generation Jet Engines

In aerospace, lightweight materials are no longer confined to secondary structures; they are now central to hot-section engine performance, where mass reduction directly translates into fuel efficiency and range. Engine OEMs are increasingly replacing nickel-based superalloys with Titanium Aluminides (TiAl) and Ceramic Matrix Composites (CMCs) to unlock higher operating temperatures and lower rotating mass.

CMCs such as SiC/SiC exhibit densities roughly one-third that of nickel superalloys, while tolerating sustained temperatures approaching 1,200 °C. Peer-reviewed aerospace studies from 2024–2025 confirm that these materials enable ~15% fuel burn reduction by supporting hotter, more efficient combustion cycles without excessive cooling air.

TiAl has already crossed the qualification threshold for commercial aviation. It is now standard in Low-Pressure Turbine (LPT) blades for engines such as GEnx and LEAP, cutting LPT module weight by approximately 50%. This mass reduction compounds system-level benefits by lowering centrifugal loads, enabling lighter shafts, bearings, and support structures throughout the engine.

Beyond commercial aviation, these materials are becoming indispensable for hypersonic platforms (Mach 5+), where conventional aluminum and steel lose structural integrity. Industry benchmarks indicate that advanced alloys and CMCs are among the few material classes capable of surviving the combined thermal, mechanical, and oxidative stresses encountered in next-generation high-speed flight systems.

Lightweighting Public Transit Under Federal Infrastructure Mandates

Public transit modernization is emerging as a high-volume opportunity for lightweight materials, driven by regulatory pressure and federal investment. The Bipartisan Infrastructure Law allocates $109 billion to public transit and $66 billion to passenger and freight rail through 2026, with $7.5 billion earmarked specifically for zero-emission buses.

Electric buses and railcars face the same mass penalty challenges as EVs, but at a larger scale. Lightweight aluminum bodies, composite panels, and magnesium-rich components are increasingly specified to maximize driving range and passenger capacity without oversizing battery systems. Parallel regulatory pressure from the U.S. Environmental Protection Agency Phase 3 GHG standards requires heavy-duty vehicles to meet progressively tighter CO₂ limits through 2032, pushing OEMs toward aggressive lightweighting as a compliance strategy.

For freight and vocational vehicles, lightweighting has a direct economic impact: every kilogram saved in chassis or cabin mass translates to one additional kilogram of payload, improving the Levelized Cost of Transport (LCOT) for logistics operators. This is accelerating adoption of high-strength aluminum alloys and magnesium-lithium systems in delivery fleets, refuse vehicles, and intermodal transport platforms.

Materials for Reusable Launch Vehicle (RLV) Structures

The rapid expansion of commercial spaceflight is redefining material requirements for launch vehicles, where reusability has replaced one-time performance as the dominant design constraint. RLVs must survive extreme mechanical loads during launch and intense thermal cycling during atmospheric reentry—repeatedly.

Advanced aluminum-lithium (Al-Li) alloys have become foundational for cryogenic tanks and primary structures in reusable systems such as Falcon 9 and New Shepard. These alloys deliver ~10% weight reduction and up to 30% higher stiffness than conventional aluminum, improving tank integrity under pressurization while reducing inert mass.

Thermal protection is undergoing a similar transformation. Reusable heat shields based on carbon–carbon composites and CMCs are replacing ablative materials that erode with each flight. These lightweight systems can be reused across dozens of missions, contributing to 30–40% per-launch cost reductions by minimizing refurbishment.

Additive manufacturing is amplifying these gains. Programs supported by NASA are using 3D printing to consolidate complex brackets and engine components into single lightweight structures. In 2025, such designs are delivering 15–20% mass reduction while improving structural reliability—demonstrating that lightweighting in space is now as much about design freedom as material substitution.

Market Share Analysis: Lightweight Materials Market

Market Share by Material Type: Advanced Metals & Alloys as the Scalable Lightweighting Backbone

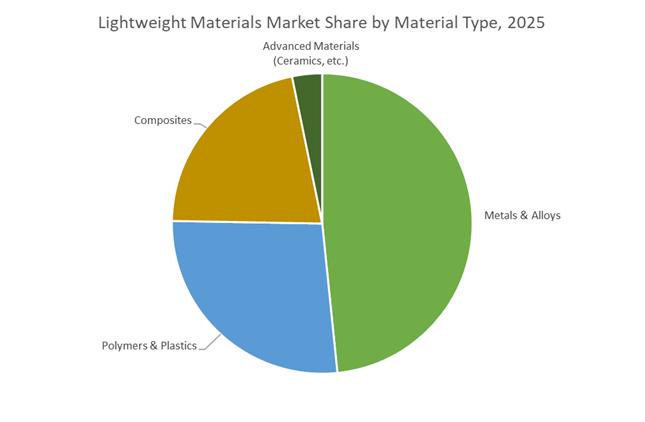

Metals and alloys command approximately 45% of the global lightweight materials market because they uniquely balance mass-reduction, crash performance, manufacturability, and cost discipline at automotive scale. Unlike composites, which require new tooling and slower cycle times, Advanced High-Strength Steel (AHSS) and 6XXX/7XXX series aluminum integrate seamlessly into existing stamping, extrusion, and joining lines, making them the fastest route to fleet-wide lightweighting. The steady rise toward 514 pounds of aluminum per vehicle by 2025–2026 reflects OEM preference for predictable performance gains without redesigning entire vehicle architectures. AHSS has further entrenched its share by enabling up to 50% gauge reduction versus mild steel while preserving energy absorption in crash zones—allowing body-in-white weight reductions of 25–30% at a cost multiple times lower than carbon fiber. In EV platforms, aluminum’s dominance has accelerated due to battery enclosure applications, where 30% mass savings versus steel translate directly into double-digit range extension. Critically, the market share of metals is no longer driven only by performance but by sustainability economics: 100% recycled aluminum alloys now deliver 95% energy savings and ~80% CO₂ reduction, turning lightweight metals into both a cost and ESG optimization lever. This combination of structural reliability, production scalability, and circular-economy alignment cements metals and alloys as the largest and most defensible material segment in the lightweight materials landscape.

Market Share by Application: Automotive as the Irreversible Demand Anchor

Automotive accounts for around 55% of total lightweight material demand, making it the undisputed volume and revenue engine of the market. This dominance is structurally linked to regulatory pressure and electrification economics rather than cyclical vehicle sales alone. Every major OEM faces tightening 2025–2030 emission thresholds, and weight reduction remains the most capital-efficient compliance strategy compared with powertrain redesigns. Industry benchmarks consistently show that each 10% reduction in vehicle mass yields a 6–8% improvement in fuel efficiency or EV driving range, a return profile unmatched by aerodynamics or drivetrain optimization alone. As a result, lightweight metals have become foundational across closures, subframes, crash structures, and battery housings. The rapid adoption of multi-material design (MMD)—using aluminum for outer skins and AHSS for safety-critical cages—has further expanded addressable volume by allowing OEMs to optimize weight without compromising crash ratings. Importantly, aluminum’s high thermal conductivity has elevated its role beyond weight reduction into EV safety, where structural aluminum components increasingly function as passive heat spreaders during battery thermal events. Despite moderate headline growth rates, automotive lightweighting remains a high-certainty, long-duration demand stream, underpinned by regulation, electrification, and platform standardization—securing automotive’s majority share and anchoring the long-term trajectory of the lightweight materials market.

Competitive Landscape: Five Leaders Scaling Alloys, Recycled Aluminum, Polymers and Composite Systems

The competitive field combines advanced-materials specialists, global steel/metal majors and polymer/composite groups. Leaders differentiate on product breadth (aluminum, UHSS, PEEK, carbon fiber), recycling capability, AM-ready alloys, and integration with OEM programs for EVs and aircraft.

Hexcel Corporation - Composite System Supplier Expanding Into Hydrogen Vessels and Optimising Financial Capacity For High-Rate Aerospace Demand

Hexcel is a leader in carbon-fiber, honeycomb cores and HexPly® prepregs; it reported Q3 2025 sales of US$456.0M with Defense & Space sales growing 13.3% YoY, reflecting elevated demand in fighter and space programs. Hexcel co-launched an Advanced Composite Pressure Vessel with HyPerComp (Sep 2025) for hydrogen storage and expanded its aerospace distribution network to support eVTOL/UAV markets (Sep 2025). Operationally, Hexcel has also executed balance-sheet actions (accelerated share repurchase) to support scale-up and shareholder value as it increases composite output for high-rate platforms.

Novelis Inc. - Global Aluminum Recycler and Rolled-Product Leader Driving Circular Lightweighting At Scale

Novelis is the world leader in aluminum rolling and recycling, achieving ~63% average recycled content across flat-rolled products (FY2025) and targeting 75% recycled content by 2030. The company reported a 10% reduction in GHG intensity in FY2025 and is central to OEM closed-loop initiatives that return production scrap for remelting - a pathway that uses ~95% less energy versus primary production and underpins low-carbon automotive lightweighting.

Arcelormittal - Advanced-Steel Innovator Expanding AHSS/UHSS Capacity For Automotive EV and BIW Lightweighting

ArcelorMittal is advancing UHSS and AHSS solutions: it commissioned a Hazira CGL (June 2025) capable of producing AHSS up to 1180 MPa, and launched a new UHSS line for the North American market (July 2025). These products enable >60% BIW penetration of UHSS and permit up to 40% thinner Sections for equivalent safety. ArcelorMittal is also investing in electrical-steel and EAF capacity to support electrification and reduce emissions intensity.

Solvay S.A. - High-Performance Polymer Platform Enabling Ultra-Light Components and Advanced Thermal/Chemical Resistance

Solvay offers ~1,500 HPP formulations (PEEK, PPSU etc.) and has committed US$85 million to expand PEEK capacity (Georgia & India) to exceed 2,500 tpa. Its HPPs (density ≈1.2-1.5 g/cm³) can be up to 50% lighter than aluminum, enabling up to ~20% fuel-efficiency gains in aircraft and EV components. Solvay’s SPM toolkit drives sustainable product development and positions the company to supply lightweight polymers for thermal- and chemically-demanding applications.

Teijin Limited - Aramid and Carbon-Fiber Supplier Powering Ballistic Protection and Hybrid Fabric Solutions For Mobility

Teijin is a global leader in para-aramid (Twaron®, Technora®) and carbon fiber (Tenax®). Para-aramids are up to 8× stronger than steel by weight and account for ~72.2% of the aramid market in 2025, reflecting dominance in ballistic and high-impact applications. Early-2025 partnerships to supply aramid for EV-specific tire systems demonstrate Teijin’s move to integrate lightweight aramid into mobility components, while its vertical capabilities support hybrid fabric solutions combining aramid and carbon for bespoke structural use-cases.

The United States lightweight materials market in 2025 is defined by federal reshoring, aerospace integration, and EV-grade aluminum scaling. The October 2025 United States–Japan Framework for securing critical minerals and rare earths directly targets the processing of magnesium and aluminum alloys vital for defense platforms and high-tech manufacturing, strengthening upstream security for lightweight components. In aerospace, domestic expansions by Hexcel Corporation and Alcoa Corporation are aligned with Boeing 737 MAX ramp-ups and new space launch systems; Hexcel’s Q3 2025 defense & space sales rose 13.3%, driven by carbon fiber, honeycomb, and foam cores.

EV policy reinforces demand pull-through. The Department of Energy (DOE) continues to deploy billion-dollar loan commitments to localize thermal barriers and aluminum-intensive frames, offsetting the mass of high-capacity battery packs. The result is a tightly coupled ecosystem where CFRP, AHSS, and high-strength aluminum converge to deliver range, safety, and manufacturability at scale.

China: New Materials Sovereignty, Giga Castings, and Circularity

China remains the world’s largest producer and consumer of lightweight materials, with 2025 strategy pivoting toward precision engineering and export governance. Effective April 2025, MOFCOM Announcement No.18 imposed export controls on samarium, gadolinium, and select rare-earth alloys, directly influencing global supply of lightweight magnetic components and high-strength alloys. On the demand side, EVs reached 50% of new car sales in H2 2024, and MIIT’s 2025 priorities emphasize aluminum “Giga Castings”—large, integrated structural parts that cut assembly complexity and vehicle mass.

Circularity complements scale. In early 2025, BASF operationalized loopamid® in Shanghai, enabling chemical recycling of nylon-based hybrid fabrics used in lightweight interiors. Together, export controls, giga casting adoption, and circular polymers reinforce China’s end-to-end leverage across aluminum, composites, and engineered polymers.

Germany: Clean Industrial Deal Drives PFAS-Free and Bio-Hybrid Lightweighting

Germany leads Europe’s sustainability-linked lightweighting under the Clean Industrial Deal. In November 2025, updated federal ordinances aligned with EU Regulation 2022/1616, tightening standards for recycled plastics and accelerating PFAS-free alternatives in food-contact and industrial components. Aviation R&D advanced through the Transnational Eureka Lightweighting call (May–October 2025), funding hybrid constructions that integrate smart sensors directly into composite airframes.

Automotive adoption validates the economics. Late-2025 announcements from BMW and Mercedes-Benz confirmed carbon/basalt hybrid yarns in interior panels, achieving ~40% cost reduction versus pure carbon while meeting fire-safety requirements. Germany’s focus on thermoplastic honeycombs, recycled TPU, and bio-hybrids positions it as the regulatory and engineering benchmark.

Japan: GX 2040 Catalyzes 6G-Ready and AAM-Grade Materials

Japan is leveraging leadership in carbon fiber and advanced polymers to pioneer ultra-gap lightweight materials for 6G and Advanced Air Mobility (AAM). The GX 2040 Vision (Cabinet-approved Jan 18, 2025) unlocks R&D subsidies for chemical recycling and low-energy recovery of high-purity monomers from end-of-life polymers. In parallel, METI’s fast-tracked eVTOL certification in 2025 is driving localized demand for ultralight aramid cores and low-dielectric polyimide foams.

Telecom applications add another layer. Japanese firms are piloting hybrid carbon/glass EMI shielding for 6G signal reflectors, balancing stiffness with controlled dielectric properties for smart-city infrastructure. Leadership from fiber majors such as Toray Industries underpins Japan’s materials-to-systems integration.

India: Aatmanirbhar Defense, Rail Modernization, and EV Localization

India’s lightweight materials market is scaling rapidly through defense exports, rail modernization, and EV localization. In FY 2024–25, defense exports reached ₹23,622 crore, supported by indigenous airframes and components; the TATA Aircraft Complex (Vadodara)—inaugurated October 2024—is now at full production for C-295 aircraft. Policy support extends to textiles: under the ₹10,683 crore PLI for technical textiles, funding targets glass/carbon hybrid fabrics for Vande Bharat rail interiors and industrial filtration.

EV platforms are following suit. In 2025, Tata Motors and Mahindra deployed aluminum-intensive frames on “Born Electric” architectures, cutting curb weight by up to 15% to extend range without enlarging batteries—cementing aluminum, AHSS, and hybrids as core enablers.

South Korea: Gwangju Cluster Aligns Lightweight Materials with HBM4

South Korea’s lightweight materials strategy is tightly coupled to AI semiconductor packaging. In December 2025, the government committed ₩360.6 billion to advanced packaging, specifying ultra-thin polyimide-hybrid fabrics as dielectric layers for high-density chip stacking. The Gwangju Packaging Cluster anchors this push, aligning materials qualification with OSAT throughput.

Automotive synergies reinforce resilience. By 2025, Korean automakers achieved ~70% self-sufficiency in critical intermediates—PPS and long-chain polyamides—for high-voltage battery housings. Late-2025 integration of high-temperature polyimide films into HBM4 lines (withstanding 260 °C reflow) highlights how lightweight polymers now underpin both compute performance and EV safety.

2025 Strategic Matrix: Lightweight Materials Development by Country

Lightweight Materials Development Matrix

|

Country

|

Primary Technical Focus

|

2025 Strategic Milestone

|

Key Materials

|

|

United States

|

Aerospace & defense

|

Hexcel Q3 2025 defense growth

|

CFRP, honeycomb, aluminum

|

|

China

|

EV ecosystem & exports

|

Apr 2025 rare-earth controls

|

Aluminum giga castings, composites

|

|

Germany

|

Circular economy

|

EU 2022/1616 alignment

|

Bio-hybrids, recycled TPU

|

|

Japan

|

6G & AAM (eVTOL)

|

GX 2040 approval

|

Carbon fiber, aramid cores

|

|

India

|

Rail & defense

|

₹23k Cr defense export record

|

Glass/carbon hybrids, AHSS

|

|

South Korea

|

AI chip packaging

|

Gwangju cluster investment

|

Polyimides, LCP

|

Lightweight Materials Market Report Scope

Lightweight Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$153.7 Billion

|

|

Market Size (2035)

|

$294 Billion

|

|

Market Growth Rate

|

6.7%

|

|

Segments

|

By Material Type (Metals & Alloys, Composites, Polymers, Advanced Materials), By Product Form (Sheet & Plate, Extrusions & Profiles, Foams & Honeycombs, Castings & Forgings, Additive Manufacturing Filaments/Powders), By Application (Structural Components, Interior & Trim, Powertrain & Battery, External Body), By End-User Industry (Automotive, Aerospace & Defense, Renewable Energy, Electronics, Industrial)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Alcoa Corporation, Novelis Inc. / Hindalco, Toray Industries Inc., Hexcel Corporation, SGL Carbon SE, Teijin Limited, Solvay S.A. / Syensqo, ThyssenKrupp AG, Constellium N.V., Mitsubishi Chemical Group Corporation, SABIC, Rio Tinto Alcan Inc., Evonik Industries AG, LyondellBasell Industries N.V., ArcelorMittal

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Lightweight Materials Market Segmentation

By Material Type

- Metals & Alloys

- Composites

- Polymers

- Advanced Materials

By Product Form

- Sheet & Plate

- Extrusions & Profiles

- Foams & Honeycombs

- Castings & Forgings

- Additive Manufacturing Filaments/Powders

By End-User Industry

- Automotive

- Aerospace & Defense

- Renewable Energy

- Electronics

- Industrial

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Lightweight Materials Market

- Alcoa Corporation

- Novelis Inc. / Hindalco

- Toray Industries, Inc.

- Hexcel Corporation

- SGL Carbon SE

- Teijin Limited

- Solvay S.A. / Syensqo

- ThyssenKrupp AG

- Constellium N.V.

- Mitsubishi Chemical Group Corporation

- SABIC

- Rio Tinto Alcan Inc.

- Evonik Industries AG

- LyondellBasell Industries N.V.

- ArcelorMittal

*- List not Exhaustive