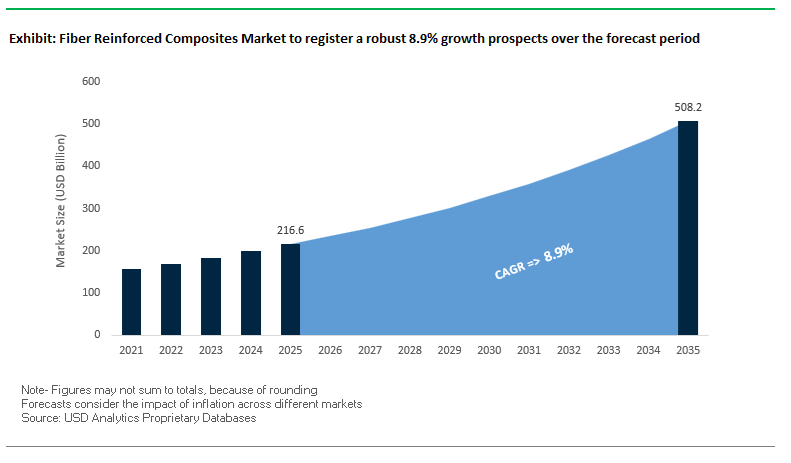

The Fiber Reinforced Composites Market, valued at USD 216.6 billion in 2025, is projected to reach USD 508.1 billion by 2035, expanding at a robust CAGR of 8.9%. The market’s strong outlook is driven by structural performance requirements in aerospace, rapid adoption in electric vehicles (EVs), advances in wind turbine design, accelerated implementation of automated manufacturing, and the increasing use of durable FRP solutions in large-scale construction.

The global Fiber Reinforced Composites Market is undergoing accelerated expansion driven by aerospace fleet modernization, EV lightweighting programs, industrial-scale renewable energy buildouts, and the adoption of automated manufacturing systems capable of reducing composite production costs. A major milestone occurred in January 2026, when the Japan Bank for International Cooperation (JBIC) co-signed a USD 180 million loan agreement with Toray Composite Materials America to expand carbon fiber manufacturing specifically for hydrogen-powered fuel cell vehicle (FCV) high-pressure tanks. The investment underscores the growing role of carbon fiber as a critical enabler of clean mobility and supply chain resilience for advanced propulsion systems.

Defense and space applications continued demonstrating robust demand. Hexcel reported a 13.3% sales increase in its Defense, Space & Other segment in November 2025, reflecting surging requirements for high-performance prepregs, honeycomb structures, and composite airframe components in global fighter aircraft and satellite platforms. In October 2025, Toray Industries confirmed an expansion of regular tow medium- and high-modulus carbon fiber capacity at its French subsidiary, increasing output from 5,000 to 6,000 metric tons, with production commencing in 2025. The expansion is directly aligned with rising European aerospace and industrial composite needs.

Structural efficiency and cost competitiveness also advanced in 2025 through major industry innovations. SGL Carbon successfully completed a major restructuring of its Carbon Fibers business unit in September 2025, achieving positive adjusted EBITDA after years of losses, signaling renewed financial health and improved capacity utilization. Automotive lightweighting gained momentum in August 2025, when a major European OEM partnered with a thermoplastic composite supplier to introduce a polypropylene-based GFRP rear cross-member achieving a 35% weight reduction compared to aluminum—highlighting fast-cycle thermoplastic composites as a key enabler for mass-market EVs. Sustainability was further strengthened in July 2025, with the UK’s Advanced Propulsion Centre funding a consortium to optimize CFRP recycling pathways, targeting a 20% lifecycle CO₂ reduction across aerospace and high-performance automotive industries.

Manufacturing innovation accelerated with Huntsman launching a fast-cure epoxy system in May 2025, reducing cure times in AFP and RTM processes by 40%, directly supporting next-generation airframe production rates. Complementing the, in March 2025, SGL Carbon showcased advanced carbon brush technologies for wind turbine generators at WindEurope 2025, demonstrating significantly enhanced service life and reduced wear, which strengthen the reliability and uptime of renewable energy assets.

Industry professionals and buyers are primarily concerned with understanding how fiber composites—especially CFRP and GFRP—enable unprecedented weight reduction, operational efficiency, structural longevity, and sustainability benefits across mission-critical applications. As global industries transition to lightweight, corrosion-resistant, and fatigue-resistant materials, the demand for carbon and glass fiber composites continues to intensify across transportation, renewables, industrial systems, and advanced mobility platforms.

Performance benchmarks are rapidly evolving: next-generation aircraft structures exceed 50% CFRP composition, enabling major reductions in fuel burn and lifecycle emissions; EV OEMs routinely achieve 20–50% weight savings per substituted part using GFRP and CFRP; offshore wind turbines rely on 100+ meter blades requiring high-modulus carbon fiber spar caps; and automated fiber placement (AFP) processes are reducing production cycle times by up to 22%, directly addressing historical cost challenges for composite adoption. Meanwhile, FRP rebar is transforming infrastructure durability with 75–100 year service lifespans, eliminating corrosion issues in harsh environments and dramatically reducing long-term maintenance.

- CFRP accounts for >50% structural weight in next-generation wide-body aircraft, enabling major gains in fuel efficiency and payload capacity.

- GFRP and CFRP substitution provides 20–50% weight reductions in automotive components, essential for EV range optimization and emissions compliance.

- Offshore wind blades exceeding 100 meters require high-modulus carbon fiber spar caps, ensuring structural stiffness without excessive mass.

- Automated Fiber Placement (AFP) reduces production cycles by up to 22%, lowering manufacturing cost and enabling higher-volume composite production.

- FRP rebar provides 75–100 years of corrosion-free life, dramatically outperforming steel in bridges, tunnels, and coastal structures.

Automation-Led Manufacturing Shifts and Circular Material Innovations Shaping the Fiber Reinforced Composites Market

Trend 1 - Automated Fiber Placement (AFP) and Additive Manufacturing Transform Aerospace Composite Production

Aerospace OEMs are accelerating the shift toward Automated Fiber Placement (AFP) to industrialize composite manufacturing and reduce the historically high costs associated with large, complex primary structures. AFP automation directly supports the aerospace industry’s long-term productivity and cycle-time reduction objectives.

Aerospace material roadmaps identify 100 kg/h deposition rates as the target threshold for next-generation AFP systems-a step change compared to traditional hand layup. Achieving this throughput is essential for producing carbon fiber fuselage sections, wing skins, and spars at commercial aircraft volumes while maintaining structural quality and consistency.

AFP’s impact is amplified by the migration toward Out-of-Autoclave (OoA) processing. Advanced robot-mounted AFP systems paired with OoA resin systems eliminate the reliance on autoclaves, reducing energy consumption, shortening cure cycles, and increasing production flexibility. These OoA-compatible AFP workflows are reshaping the economics of primary aircraft structures and expanding automated composites adoption across Tier 1 suppliers.

Geometric processing capability is a critical differentiator. Narrow-tow AFP (e.g., 1/8-inch tow vs. 1/4-inch tow) provides superior fiber steering, enabling defect-free layups around curved contours and minimizing gaps and wrinkles. This precision improves the strength-to-weight ratio of wings, fuselage shells, and other load-bearing aerostructures.

The convergence of AFP with Additive Manufacturing (AM) introduces a new hybrid production paradigm. AM enables near-net-shape tooling and initial component architectures, which are subsequently reinforced through AFP with high-performance carbon fiber. This hybridization reduces material waste, accelerates development timelines, and supports customizable aerospace structures-key advantages as OEMs scale toward next-generation aircraft platforms.

Trend 2 - Recyclable Thermoset Resin Systems Gain Commercial Momentum in Wind Energy and Automotive Sectors

The global need to manage end-of-life composite waste-particularly from wind turbines-is accelerating commercial adoption of recyclable thermoset resin systems, marking a pivotal shift from traditional, non-recyclable epoxy-based composites.

A landmark example is the Siemens Gamesa–Swancor partnership, deploying recyclable blades built using Swancor’s EzCiclo resin and CleaVER chemistry. These blades are being installed in the North Sea’s 1.4 GW offshore wind project, marking the first full-scale industrial use of recyclable thermoset systems in a major offshore installation. This deployment showcases the commercial viability of recyclable resins for multi-decade operational environments.

End-of-life materials represent an urgent challenge. WindEurope estimates that 25,000 tonnes of turbine blades will reach end-of-life annually by 2025 in mature markets, creating a significant volume of composite waste that cannot be landfilled under tightening EU regulations. This waste challenge is the primary catalyst for chemical recycling innovation targeting epoxy-based composites.

The CETEC initiative-led by Vestas, Olin, and global academic partners-has already demonstrated successful chemical depolymerization of epoxy resin, enabling full recovery of monomers and carbon/glass fibers from both legacy and newly manufactured blades. This breakthrough establishes a credible technical pathway to full circularity for thermoset composites.

Manufacturing adoption is strengthening. Aditya Birla Advanced Materials’ Recyclamine-enabled epoxy resin system is engineered as a drop-in replacement, compatible with existing turbine blade processes such as IntegralBlade manufacturing. This zero-capex-transition model removes adoption barriers for blade manufacturers and accelerates the shift toward recyclable resin chemistries across wind energy and automotive components.

Opportunity 1 - Commercial Scale-Up of Low-Cost Carbon Fiber for Mass-Volume Automotive Applications

Reducing the cost of carbon fiber remains the most influential factor for unlocking its widespread adoption across mainstream automotive platforms. High-strength Carbon Fiber Reinforced Polymers (CFRPs) offer transformative weight reduction, but their cost structure historically limits use to premium vehicles.

Material and energy suppliers-including Aramco-are targeting a 50% reduction in carbon fiber production costs, primarily through lower energy consumption during stabilization and carbonization. Achieving this threshold would dramatically expand CFRP penetration into high-volume vehicle architectures.

Processing innovation is equally critical. Teijin’s mass-production CFRP technology has successfully reduced molding cycle times for automotive cabin frames to under one minute, aligning with automotive production requirements that typically demand sub-five-minute cycles. This capability is essential to scaling CFRP from niche to mainstream applications.

Raw material cost reduction plays a decisive role. Carbon fiber manufacturing relies heavily on Polyacrylonitrile (PAN), whose price is influenced by the cost of acrylonitrile. Companies such as INEOS are investing in lower-cost acrylonitrile production methods to directly reduce PAN precursor pricing, which significantly affects final carbon fiber cost.

Hybrid material strategies are emerging to balance performance and affordability. Carbon Fiber Reinforced Thermoplastics (CFRTPs)-including long-fiber thermoplastic pellets for injection molding-enable rapid-cycle production of complex parts with high strength and geometric versatility. These materials support automotive OEMs in integrating CFRPs into structural and semi-structural mass-market applications at lower cost points.

Opportunity 2 - Embedded Structural Health Monitoring (SHM) Enables Predictive Maintenance and Longer Composite Lifespans

Embedding sensing technologies into composite structures presents a transformative opportunity to shift from scheduled, manual inspections to real-time, predictive structural health monitoring (SHM)-critical for aerospace, wind energy, infrastructure, and advanced pipelines.

Fiber Reinforced Composites integrated with Fiber Bragg Grating (FBG) sensors have demonstrated exceptional reliability. Composite pipeline studies show that FBG sensors combined with AI models such as Enhanced Convolutional Neural Networks (ECNN) can detect damage with 93.33% accuracy, enabling early intervention before catastrophic failure.

Impact damage-especially Barely Visible Impact Damage (BVID)-is a major concern for aerospace fuselage skins, rotor blades, and wind turbine structures. Embedded Piezoelectric Transducers (PZTs) provide both active and passive guided-wave SHM, enabling precise localization and imaging of impact zones that would otherwise remain undetected.

The materials industry is progressing toward self-sensing composite systems, reducing the need for external sensors. Strategies include integrating gold nanoparticle-coated yarns, designing piezoresistive fiber architectures, or leveraging the intrinsic conductivity of carbon fiber as an embedded electrode for resistance- or capacitance-based sensing.

Infrastructure operators are already adopting SHM for life-extension strategies. In pipeline systems, corrosion-related failures account for a substantial share of leaks and ruptures. Embedded fiber optic or piezoelectric sensors provide continuous structural integrity monitoring, reducing the cost of inspections and preventing unexpected downtime. These benefits strongly position SHM-enabled composites as a next-generation solution for safety-critical, long-lifespan structures.

Fiber Reinforced Composites Market Share Analysis

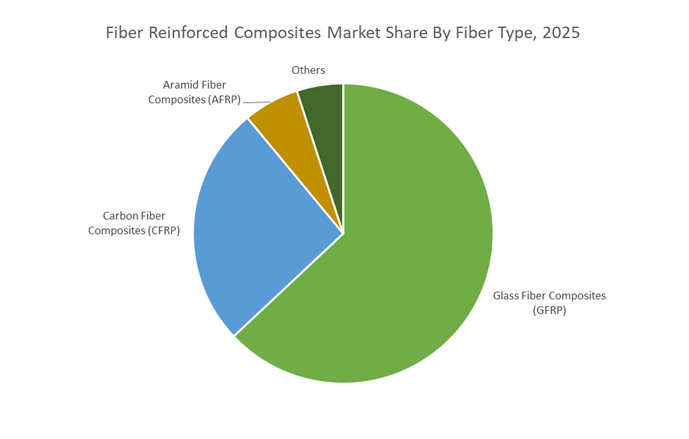

Market Share by Fiber Type: Glass Fiber Composites Lead Through Optimal Strength-Cost Balance and Broad Industrial Utility

Glass Fiber Composites (GFRP) hold the dominant 65% share within the Fiber Reinforced Composites Market, driven by their unmatched combination of mechanical performance, affordability, and manufacturing scalability. E-glass fiber—representing the bulk of global output—delivers a cost-to-performance ratio that far surpasses alternatives such as carbon fiber, which can be up to 10× more expensive. This stark cost differential makes GFRP the default choice for high-volume, large-format, or cost-sensitive composite applications where extreme stiffness is not a primary design requirement. Beyond economics, GFRP’s inherent corrosion resistance and chemical durability position it as the preferred material for structural components in marine, chemical processing, and water infrastructure sectors that demand long service life and minimal maintenance. The material’s strength-to-weight advantages remain compelling, with high-performance S-glass fibers reaching tensile strengths up to 4,890 MPa, enabling lightweight structures that often outperform steel in corrosive or fatigue-intensive environments. Additionally, GFRP is compatible with a wide range of fabrication methods—including pultrusion, filament winding, infusion, and compression molding—which accelerates adoption across industries seeking cost-effective composite production. Together, these characteristics reinforce GFRP’s leadership, ensuring it remains the most widely utilized reinforcement type in the global composites industry.

Market Share by End-Use Industry: Wind Energy Dominates as the Largest Consumer of High-Volume Composite Structures

Wind Energy leads the market with a 28% share, reflecting its status as the single largest consumer of fiber-reinforced composite materials worldwide. Modern wind turbine blades represent the largest composite structures manufactured at industrial scale, and their design geometry demands massive volumes of high-strength GFRP. Structural parts such as spar caps and aerodynamic shells typically incorporate up to 75% GFRP by weight, making turbine blade production one of the most material-intensive composite applications globally. As manufacturers push the boundaries of turbine efficiency, blade lengths now routinely exceed 80 meters, and because power generation increases with the square of blade length, the demand for stiffer, high-modulus glass fibers continues to surge. These long blades must balance low weight with structural rigidity while maintaining minimal deflection, a requirement that GFRP meets due to its favorable fatigue resistance—an essential property considering blades are subjected to over 300 million load cycles across their 20-plus-year operational life. This continuous cyclic stress environment places extraordinary emphasis on durability, and GFRP’s superior fatigue performance makes it indispensable. With global renewable energy capacity expanding rapidly and countries accelerating wind power investments, the Wind Energy sector is positioned to maintain its top share, driving long-term structural demand for advanced fiber-reinforced composites.

Country Analysis: Global Fiber Reinforced Composites Development Frontrunners

United States: Aerospace Dominance and Defense-Grade Carbon Fiber Reinforced Polymer (CFRP) Advancements

The United States leads global innovation in Carbon Fiber Reinforced Polymers (CFRP), driven by large-scale aerospace modernization, expanding defense programs, and advanced manufacturing capabilities for high-rate composite production. Major U.S. composite suppliers are scaling aggressively to meet the rising material intensity of commercial aviation, including next-generation single-aisle aircraft and the rapidly growing Urban Air Mobility (UAM) sector. Hexcel Corporation remains central to this leadership, actively expanding its high-rate composite manufacturing technologies and delivering specialized materials engineered for lighter, stronger aircraft structures. The company’s launch of HexForce® 1K reinforcement fabric in 2025 underscores the industry's shift toward ultra-lightweight, low-tow carbon fiber reinforcements required for high-performance, minimum-thickness composite systems.

Defense remains a critical and stable demand pillar. In 2024, the U.S. Army awarded major contracts under the FLRAA (Future Long Range Assault Aircraft) program, accelerating adoption of advanced carbon fiber systems to enhance rotorcraft maneuverability, survivability, and speed. Beyond aerospace and defense, the U.S. is integrating fiber-reinforced composites into national energy infrastructure, supported by the Department of Energy’s GRIP initiatives, using carbon fiber composite cores to increase grid reliability and transmission efficiency. Leading suppliers such as Toray Advanced Composites expanded their Continuous Fiber Reinforced Thermoplastic (CFRTP) capacity in late 2024 to meet demand for fast-cycle automotive and industrial applications. In parallel, sustainability efforts are growing—exemplified by Toray Composite Materials America's partnership with Elevated Materials, which repurposes aerospace-grade carbon fiber prepreg waste. These combined investments reinforce the U.S. as the highest-value market for advanced composites in aerospace, defense, and energy infrastructure.

China: Wind Energy Scale-Up and Strategic Localization of Carbon Fiber Production

China is undergoing rapid expansion in Fiber Reinforced Composites (FRC) consumption and manufacturing, fueled by its unmatched wind power installation rate, fast-growing EV market, and industrial policies aimed at localizing high-strength carbon fiber production. As the global leader in installed wind capacity, China consumes vast volumes of Glass Fiber Reinforced Polymers (GFRP) to produce increasingly larger and more durable wind turbine blades. The nation’s vertically integrated wind blade ecosystem, supported by state-owned enterprises, is aggressively reducing composite production costs while scaling manufacturing to support multi-gigawatt expansion. China’s infrastructure ambitions also extend to high-speed rail, where CFRP components in bogies and structural elements improve energy efficiency and reduce train weight, aligning with the country’s target of expanding its already world-leading rail network.

Localization is a central strategic pillar. Beijing’s industrial policy incentives continue to accelerate domestic R&D and large-scale production of T700 and T800 grade carbon fibers, reducing dependence on Japanese imports and strengthening national capabilities for aerospace, rail, and high-performance industrial applications. China’s booming EV industry—home to the largest EV market in the world—is increasing adoption of carbon fiber for brake discs, battery housings, and chassis components, supporting aggressive lightweighting targets for extended driving range. These trends, combined with heavy investment in upstream monomer and precursor capacity, position China as a global powerhouse shaping both current and next-wave composite material technologies.

Japan: High-Modulus Carbon Fiber Leadership and Thermoplastic Composite Specialization

Japan continues to dominate the upper end of the high-modulus carbon fiber and thermoplastic composite spectrum, driven by deep intellectual property leadership, advanced precursor technologies, and world-class materials science. Its leading composite manufacturer, Toray Industries, is expanding European capacity to increase production from 5,000 to 6,000 metric tons annually by 2025, particularly for regular tow medium- and high-modulus fibers used in aerospace and high-end automotive programs. Japan’s commitment to sustainability is also accelerating product innovation—evidenced by Toray’s development of a bio-circular carbon fiber, already commercialized through its adoption by HEAD in a next-generation sustainable tennis racquet in April 2025.

Japan is also advancing composites for emergent energy sectors. The Torayca™ Fuel Cell Material, honored by Honda in June 2025, highlights how carbon fibers are becoming integral to fuel cell stacks in next-generation FCVs—expanding the role of composites beyond structural applications. Circularity is being addressed through high-impact partnerships; in June 2025, Toray collaborated with Daher and Tarmac Aerosave to launch a dedicated End-of-Life Aircraft Recycling Program, tackling the significant challenge of thermoplastic composite recycling in aviation. Together, these initiatives reinforce Japan’s status as the global innovation engine for high-modulus carbon fiber, sustainable composite solutions, and advanced thermoplastic systems.

India: Localization of Wind Energy Composites and Strategic Defense-Grade CFRP Development

India is emerging as a competitive manufacturing hub for Glass Fiber Reinforced Polymer (GFRP) and high-performance composites due to its expanding renewable energy sector and rapidly advancing defense manufacturing ecosystem. The government’s push for self-reliance, driven by Make in India, is transforming wind energy supply chains. In 2025, the Ministry of New and Renewable Energy (MNRE) strengthened the Approved List of Models and Manufacturers (ALMM) Wind to mandate local supply chains and data centers for wind turbines, aiming to increase domestic capacity utilization to 70–80%. With a robust annual turbine manufacturing capability of 18,000 MW, India already hosts one of the world’s strongest fiberglass composite ecosystems, supplying blades, nacelles, and tower components for both domestic and export markets.

Financial incentives further bolster local manufacturing. The government’s Concessional Custom Duty Certificates (CCDCs) through March 2025 reduce costs for critical imported components, ensuring competitive domestic production of Wind Turbine Generators (WTGs). Beyond renewables, India’s defense sector is catalyzing demand for advanced CFRP and aramid fiber composites through collaborations between domestic manufacturers and the Defence Research and Development Organisation (DRDO). These partnerships focus on developing indigenous composite solutions for aerospace structures, protective armor, missile components, and UAV systems, enabling India to strengthen its strategic autonomy in high-performance materials.

Ireland / European Union: Sustainable Composite Breakthroughs and Circular Materials Innovation

The European Union, supported by strong academic and industrial partnerships, is leading global research into sustainable composites, recyclable resins, and low-energy manufacturing processes, closely aligned with the EU Green Deal and circular economy goals. Ireland has emerged as a standout innovator, with the University of Limerick’s CARBOWAVE project demonstrating a transformative method for carbon fiber production, using combined plasma and microwave heating to reduce energy consumption by up to 70% compared to conventional carbonization. This breakthrough represents a major step toward cost-effective, low-emission fiber production that could reshape global composite supply chains.

Regulatory drivers further accelerate Europe’s sustainable composite adoption. The European Commission’s proposed regulation on vehicle design and end-of-life management is set to mandate higher reusability, recyclability, and recoverability standards, significantly increasing demand for recyclable composite materials such as vitrimers and soluble, reprocessable thermosets. R&D across the EU is intensifying focus on bio-based fibers and renewable precursors. The Fraunhofer IAP is pioneering composite-grade carbon fiber precursors derived from cellulose and lignin, reducing reliance on petroleum-based PAN while boosting carbon yield for greener manufacturing. Together, these developments position the EU as a global frontrunner in next-generation sustainable fiber-reinforced composites and circular material innovation.

Competitive Landscape: Global Leaders Driving Carbon Fiber Expansion, Thermoplastic Composite Adoption, and High-Performance Resin Innovation

The competitive landscape of the Fiber Reinforced Composites Market is shaped by vertically integrated carbon fiber producers, advanced resin formulators, thermoplastic composite innovators, and glass fiber manufacturers serving infrastructure and automotive applications. Leading companies are investing in capacity expansion, thermoplastic composite processing, automation technologies, and circular economy initiatives to support high-volume aerospace, defense, EV, and renewable energy markets. Their strategies focus on improving material performance, strengthening supply chains, and lowering production costs across structured composite systems.

Toray remains the dominant player in premium carbon fiber and prepreg solutions, supplying TORAYCA™ fibers to major aircraft programs including Boeing 787 and Airbus A350. The company is expanding carbon fiber production in France starting in 2025 and securing major financing—initiated in August 2025 and reaffirmed in January 2026—for U.S. expansion supporting high-pressure FCV hydrogen tanks. Toray’s AP-G 2025 strategy prioritizes lightweighting technologies and climate-aligned material solutions, positioning it at the forefront of aerospace and clean mobility composite innovation.

Hexcel is a leading provider of carbon fiber prepregs, honeycomb materials, and engineered composite structures for commercial aerospace, space, and defense platforms. Its 13.3% YoY growth in Defense, Space & Other revenues reported in November 2025 underscores strong composite adoption in fighter jets, missile systems, and satellite structures. The company continues to refine its strategic focus by divesting non-core assets—including additive printing—to concentrate on advanced structural composites supporting future airframe production rate increases.

SGL Carbon operates across the full value chain of carbon-based solutions, including SIGRAFIL™ carbon fibers, specialty graphites, and composite components. After implementing major restructuring completed in September 2025, SGL achieved positive adjusted EBITDA in its Carbon Fibers division, significantly improving competitiveness. The company’s advanced carbon brush solutions showcased in March 2025 highlight its contributions to wind turbine generator efficiency, reduced maintenance requirements, and longer operational lifetimes.

Teijin supplies TENAX™ carbon fibers, aramid fibers, and advanced thermoplastic composites aimed at high-volume automotive manufacturing. Its strategic focus is enabling rapid processing and recycling-friendly carbon fiber thermoplastic systems to support mass-market EV lightweighting. Teijin is also heavily investing in fiber recovery technologies to create circular composite solutions aligned with OEM sustainability targets and regulatory expectations.

Owens Corning dominates the glass fiber reinforcement segment, supplying GFRP materials for infrastructure, industrial systems, and automotive underbody components. The company plays a critical role in FRP rebar adoption across bridges, highways, and coastal structures where corrosion resistance and multi-decade durability are essential. Its ongoing optimization of energy consumption and sustainability in large-scale glass fiber operations reinforces its position as the preferred supplier for high-volume GFRP applications.

Huntsman provides advanced epoxy and polyurethane systems that serve as critical matrices for CFRP and GFRP structures across aerospace, wind energy, and industrial markets. The company’s fast-cure epoxy system introduced in May 2025 enables 40% shorter cure cycles, supporting AFP and RTM processing efficiency. Huntsman’s formulation expertise ensures compliance with stringent fire-smoke-toxicity (FST) and mechanical integrity requirements across aerospace and defense programs.

Fiber Reinforced Composites Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$216.6 Billion

|

|

Market Size (2035)

|

$508.1 Billion

|

|

Market Growth Rate

|

8.9%

|

|

Segments

|

By Fiber Type (Carbon Fiber Composites, Glass Fiber Composites, Aramid Fiber Composites, Natural Fiber Composites, Basalt Fiber Composites), By Matrix Resin Type (Thermoset Composites, Thermoplastic Composites, Ceramic Matrix Composites, Metal Matrix Composites), By Manufacturing Process (Prepreg Layup, Resin Transfer Molding, Compression Molding, Pultrusion, Filament Winding, Continuous Fiber Reinforcement 3D Printing), By End-Use Industry (Aerospace & Defense, Wind Energy, Automotive & Transportation, Construction & Infrastructure, Sports & Leisure, Pressure Vessels)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Toray Industries Inc., Hexcel Corporation, Teijin Limited, Solvay S.A., SGL Carbon SE, Mitsubishi Chemical Corporation, Owens Corning, Jushi Group Co. Ltd., Huntsman Corporation, SABIC, Gurit Holding AG, TPI Composites Inc., Cytec Industries (Solvay)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fiber Reinforced Composites Market Segmentation

By Fiber Type

- Carbon Fiber Composites (CFRP)

- Glass Fiber Composites (GFRP)

- Aramid Fiber Composites (AFRP)

- Natural Fiber Composites

- Basalt Fiber Composites

By Matrix Resin Type

By Manufacturing Process

- Prepreg Layup

- Resin Transfer Molding (RTM)

- Compression Molding

- Pultrusion

- Filament Winding

- Continuous Fiber Reinforcement 3D Printing

By End-Use Industry

- Aerospace & Defense (Airframes, Rotor Blades, Engine Components)

- Wind Energy (Turbine Blades, Nacelles)

- Automotive & Transportation (Lightweighting, EV Battery Housings, Chassis)

- Construction & Infrastructure (Rebar, Bridge Reinforcement)

- Sports & Leisure

- Pressure Vessels (Hydrogen Storage Tanks)

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies: Key Fiber Reinforced Composites Manufacturers

- Toray Industries, Inc.

- Hexcel Corporation

- Teijin Limited

- Solvay S.A.

- SGL Carbon SE

- Mitsubishi Chemical Corporation

- Owens Corning

- Jushi Group Co., Ltd.

- Huntsman Corporation

- Aramco (SABIC)

- Gurit Holding AG

- TPI Composites, Inc.

- Cytec Industries (Solvay)

*- List not Exhaustive