GF and GFRP Market Size To Grow To USD 51.3B By 2035 Driven By Lightweighting, Corrosion-Free Reinforcement & High-End Glass Fiber Mechanics

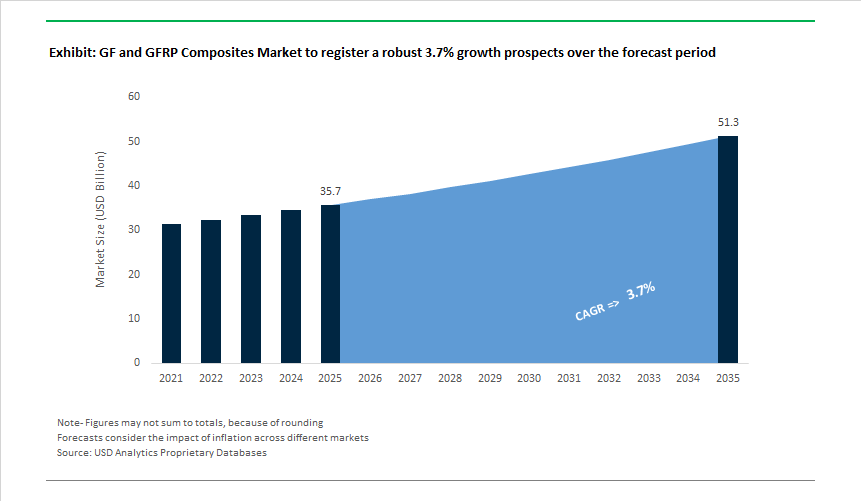

The Global Glass Fiber (GF) and Glass Fiber Reinforced Polymer (GFRP) Composites Market, valued at USD 35.7 billion in 2025, is on track to reach USD 51.3 billion by 2035 at a CAGR of 3.7%, driven by an industry-wide migration toward lightweight construction materials, corrosion-free reinforcement systems, and high-performance glass fiber mechanics. Demand is accelerating as OEMs and civil authorities prioritize materials that deliver longer service life, reduced maintenance burden, lower total cost of ownership, and improved structural efficiency. The rapid rise of S-2 glass fiber for modulus-critical aerospace, defense, and high-load energy systems further elevates the performance ceiling and expands the technical landscape of glass-based composites.

The market predominantly revolves around four high-impact technical decisions:

- Identifying GFRP formulations with the fatigue durability needed for wind blades and high-cycle civil structures, where extreme loading regimes demand the highest mechanical consistency.

- Understanding how GFRP rebar’s 80-100+ year service life in chloride-rich and marine environments outperforms steel’s typical 20-30 years, eliminating corrosion-driven failure modes and lifecycle repair costs.

- Determining when to specify S-2 glass instead of E-glass, particularly in applications where a 15% strength uplift and 25% modulus increase directly influence safety factors, deflection limits, or high-impact energy absorption.

- Quantifying the cost, logistics, and installation advantages arising from GFRP’s up to 75% weight reduction compared to steel, which reduces transportation requirements, accelerates on-site assembly, and enables more efficient prefabrication workflows.

As governments mandate corrosion-free infrastructure, wind energy OEMs optimize blade longevity, aerospace primes lighten high-precision components, and mobility sectors shift to composite-centric architectures, GFRP’s combination of mechanical reliability, chemical resistance, and lifespan superiority is reshaping global material selection across infrastructure, transportation, marine, electrical systems, EV components, and engineered aerospace structures.

Market Analysis: Capacity Expansion, Divestitures, Infrastructure Funding & High-Modulus Gfrp Innovations

The GF and GFRP Composites Market experienced notable restructuring and technology advancements, reshaping supply dynamics and accelerating adoption across infrastructure, automotive, electrical, and wind energy sectors. The period began with significant capacity expansion: China Jushi opened a major fiberglass production base in South Carolina in October 2024, reinforcing localized supply for North American OEMs while supporting technology transfer for wind, marine, and building composites. Also in September 2024, academic research demonstrated that recycled glass fibers incorporated into thermoset matrices reduce mechanical performance by only ~5%, a major milestone for sustainability initiatives in GFRP recycling.

In March 2025, a leading wind turbine OEM signed a long-term supply agreement for chopped strand mat and direct roving, indicating sustained demand for GFRP-compatible materials in 100-meter+ blade production. April 2025 saw an automotive Tier 1 supplier unveil a new GFRP battery enclosure prototype enabling 15% weight reduction and improved fire containment-reinforcing composites’ expanding relevance in EV structural systems. June 2025 introduced a major catalyst for North American infrastructure adoption as the USDOT allocated federal grants to pilot GFRP rebar in bridge decks and tunnels, validating corrosion-free reinforcement for long-duration public infrastructure.

Industry consolidation and product innovation peaked in 2025. In February 2025, Owens Corning divested its $1.1B Global Glass Reinforcements business to India’s Praana Group for $755 million, streamlining OC’s focus on building materials while signaling growing strategic interest in the glass reinforcement sector. July 2025 featured the launch of a new line of fire-retardant GFRP profiles compliant with EN 45545 railway fire standards, supporting electrical and electronics applications. In November 2025, Jushi Group commenced operations at a high-performance fiberglass line producing its specialized E8 High-Modulus Glass Fiber, strengthening supply for wind energy and infrastructure customers.

GF and GFRP Composites Market: Trends and Opportunities

Closed-Loop Recycling Transitions GFRP from Downcycled Waste to Circular Structural Material

Glass fiber (GF) and GFRP composites are undergoing a structural shift from linear, end-of-life disposal models toward closed-loop recycling systems capable of preserving fiber value. Historically, most recycled composites were mechanically ground and reused as low-grade fillers, eroding mechanical performance and economic viability. That paradigm is now changing as pyrolysis and chemical recycling mature into industrial-scale solutions. In January 2025, Siemens Gamesa demonstrated this shift through the DecomBlades initiative, successfully processing 40 tons of reclaimed glass fiber via pyrolysis and reintegrating it into new 115-meter offshore wind turbine blades for the Greater Changhua project. This marked the first confirmed case of recycled GF being reused at full structural scale rather than secondary applications.

Strategic partnerships are accelerating adoption. In June 2025, Owens Corning formalized a collaboration with Composite Recycling to introduce reclaimed fibers directly into primary reinforcement lines, creating “circular-certified” GFRP targeted at automotive and marine OEMs. Regulatory pressure is amplifying this momentum. The EU’s proposed End-of-Life Vehicles Regulation (July 2025) introduces a digital circularity passport and mandates 85% recyclability by vehicle weight, forcing GFRP producers to demonstrate recyclability at the material-design stage. Pilot repurposing models are already emerging: in late 2024, Boralex and Université de Sherbrooke validated the reuse of turbine-derived GFRP in high-performance fiber-reinforced concrete, proving that alkaline-resistant glass fibers can be redeployed into infrastructure-grade applications rather than discarded.

GFRP Moves into Primary Automotive Structures as Lightweighting Pressure Intensifies

Automotive OEMs are rapidly elevating GFRP from semi-structural roles into Body-in-White (BIW) and chassis components, driven by EV range optimization and tightening efficiency regulations. Performance benchmarking published in 2025 showed that advanced GFRP hood structures delivered impact resistance of ~153 kJ/m², nearly double that of aluminum matrix alternatives, enabling thinner sections without compromising crash energy absorption. This mechanical advantage is becoming increasingly relevant as automakers work toward compliance with stringent fuel-efficiency and emissions mandates while offsetting battery mass.

Manufacturing innovation is removing historical cost barriers. Advancements in resin transfer molding (RTM), compression molding, and AI-assisted process control are reducing scrap rates to near zero, fundamentally changing the cost curve for high-volume GFRP production. Long glass fiber thermoplastics (LGFT) are now being specified for front-end modules and instrument panel carriers, delivering up to 25% weight reduction versus steel stampings. Safety-driven adoption is also expanding beneath the vehicle. Continuous filament mat (CFM) GFRP is increasingly used for under-body EV battery shields, where its non-conductive nature, debris-impact resistance, and thermal insulation outperform metallic plates. Collectively, these shifts position GFRP not as a substitute material, but as a system-level enabler of EV architecture efficiency.

GFRP Reinforcement Redefines Durability Economics in Public Infrastructure

Corrosion-induced degradation of steel reinforcement remains the leading cause of bridge and marine structure failure, creating a long-term opportunity for GFRP rebar and structural profiles. Unlike coated or cathodically protected steel, GFRP offers inherent corrosion resistance in chloride-rich and high-humidity environments. This advantage is now being reinforced by public funding. Under the U.S. Infrastructure Investment and Jobs Act, the Federal Highway Administration has obligated more than $14.5 billion by early 2025 toward grid and bridge resilience projects, many of which explicitly specify non-corrosive GFRP reinforcement.

Lifecycle data is validating the investment case. A 2025 review of GFRP-reinforced maritime decks reported service lives exceeding 50 years without the maintenance overhead associated with epoxy-coated steel. Comparative monitoring studies released by the U.S. Department of Transportation between 2024 and 2025 showed that GFRP-reinforced bridge decks maintained equivalent structural integrity to steel while exhibiting zero rust-related deterioration after four years of heavy traffic loading. Installation efficiency further strengthens adoption: GFRP’s low density—roughly one-quarter the weight of steel—has enabled ~30% reductions in onsite labor and faster deployment of precast elements in wharf and dock projects. These advantages position GFRP as a permanent reinforcement solution rather than a niche alternative.

High-Modulus Glass Fiber Enables the Next Generation of Ultra-Long Wind Blades

The offshore wind sector’s rapid shift toward 15 MW+ turbines is redefining material requirements for blade design, with length now exceeding 115 meters. This scale imposes extreme stiffness and fatigue demands that standard glass fiber struggles to meet, while carbon fiber remains cost-prohibitive for full substitution. The result is accelerating demand for high-modulus (HM) glass fibers that deliver near-carbon stiffness at a materially lower cost. Installation data underscores the urgency: the World Wind Energy Association reported a 64% year-on-year increase in global wind installations during the first half of 2025, placing unprecedented strain on advanced glass fiber supply chains.

Manufacturers are responding with capacity localization and hybrid material strategies. In September 2025, Vestas completed the acquisition of a blade factory in Poland from LM Wind Power, dedicating the site to large offshore platforms such as the V172 series. Above the 50-meter blade threshold, innovation is concentrated in hybrid glass-carbon spar caps and specialty fiber layups to manage bending moments and fatigue loads in the 115–130 meter class. Emerging markets are also entering the value chain. In June 2025, Sinoma Science & Technology announced a $25.2 million investment to establish a wind blade manufacturing facility in Uzbekistan, signaling that GF and GFRP composites are becoming strategically important materials for global renewable energy expansion rather than regionally confined inputs.

Glass Fiber and GFRP Composites Market Share Analysis

Market Share by Glass Fiber Type: E-Glass Fiber Anchors Volume Demand Through Cost-Performance Leadership

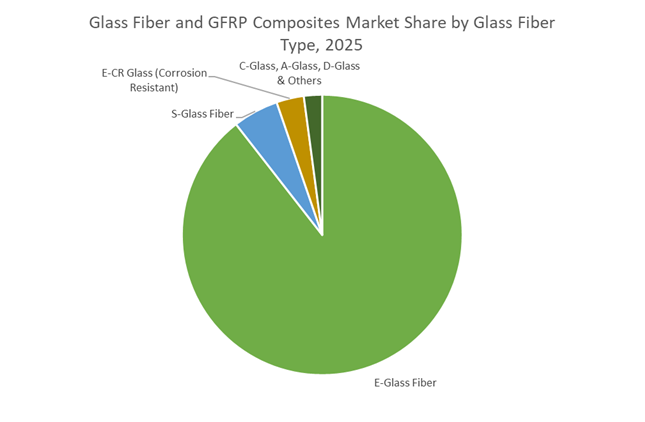

E-Glass fiber accounts for an estimated 85% share of the global Glass Fiber and GFRP Composites Market, underscoring its position as the undisputed volume material across structural and semi-structural composite applications. This dominance is fundamentally driven by E-Glass’s unmatched performance-to-cost ratio, which allows manufacturers to achieve high mechanical strength, chemical resistance, and processing reliability without the cost penalties associated with specialty fibers such as S-Glass or carbon fiber. Modern high-performance E-Glass grades deliver materially higher tensile strength and stiffness while retaining price competitiveness, enabling OEMs to meet increasingly aggressive lightweighting and durability targets at scale. Market share is further reinforced by E-Glass’s manufacturing versatility, as it is compatible with virtually all major resin systems and offers faster resin wet-out, directly reducing cycle times in high-volume production environments such as automotive panels, wind blades, and infrastructure components. From a sustainability perspective, the transition to boron-free and fluorine-free E-Glass formulations has strengthened its adoption among global manufacturers seeking compliance with tightening ESG and environmental regulations without redesigning existing composite systems. Structurally, E-Glass fibers deliver tensile strength levels that enable steel-equivalent performance at a fraction of the weight, making them indispensable in applications where cost discipline and scalability outweigh marginal performance gains. Collectively, these attributes explain why E-Glass continues to anchor the composite industry’s supply base and retains an overwhelming share of global glass fiber consumption.

Market Share by Application: Transportation Sector Drives GFRP Adoption Through Lightweighting Economics

The transportation segment commands approximately 30% of total demand in the Glass Fiber and GFRP Composites Market, positioning it as the largest application area and a primary growth engine for composite materials. This leadership is driven by the structural relationship between vehicle lightweighting, fuel efficiency, and emissions compliance, where even modest weight reductions translate into measurable gains in operating economics. GFRP has emerged as a preferred material in automotive, commercial trucking, and rail applications because it enables significant mass reduction without sacrificing corrosion resistance or structural durability. In electric vehicles, GFRP plays a critical role in offsetting battery pack weight, supporting longer driving ranges while maintaining underbody protection and crash safety. The segment’s market share is further strengthened by component-level substitutions, such as GFRP suspension elements and trailer panels, which deliver substantial weight savings while improving resistance to moisture, road salts, and chemical exposure. For fleet operators, these advantages translate into lower total cost of ownership, as GFRP components extend service life, reduce maintenance frequency, and prevent weight-related fuel penalties over time. As transportation OEMs and logistics providers face mounting regulatory and cost pressures, GFRP composites remain a strategically important material choice, sustaining the segment’s leading share in the global market.

Competitive Landscape: Global Leaders Advancing High-Modulus Fiberglass, Gfrp Reinforcement & Composite Integration

The GF and GFRP Composites competitive landscape is shaped by a combination of mega-scale fiberglass producers, specialty high-modulus fiber innovators, and vertically integrated composite solution providers. Market leadership is increasingly defined by melting-furnace efficiency, advanced fiber chemistries, precision-engineered sizing systems, regionalized manufacturing footprints, and conversion capabilities (rovings, chopped strands, mats, multiaxials, and preforms). These differentiators support rapid growth in structurally demanding markets such as wind energy, electric transportation, marine systems, oil & gas corrosion-resistant composites, and long-lifespan civil infrastructure. As the market shifts toward higher fatigue life, corrosion immunity, and weight-optimized structures, players are investing heavily in E8 and S-glass platforms, digital QC, low-energy melting technologies, and process-friendly sizings for RTM, pultrusion, SMC/LFT, and filament winding.

Jushi Group - Global Leader in High-Volume Fiberglass & E8 High-Modulus Fiber Platforms

Jushi Group maintains the world’s largest fiberglass production infrastructure, exceeding 2.6 million tons/year and powered by large-scale oxy-fuel and electric furnace technology optimized for energy efficiency and melt homogeneity. Its E8 High-Modulus Glass Fiber, designed for next-gen structural composites, delivers up to 17% higher modulus than E6 glass, supporting longer wind turbine blades, lightweight rail components, and GFRP rebars where stiffness and fatigue resistance are critical. Jushi’s global manufacturing footprint-spanning China, Egypt, and the United States (South Carolina)-provides supply-chain redundancy and localized delivery for Tier-1 wind OEMs, transportation suppliers, and construction material manufacturers. The company’s electronic-grade yarns remain essential in 5G PCB substrates, IC packaging, and high-frequency digital systems, reinforcing its diversification into information and communication materials.

Owens Corning - Strategic Pivot Toward Building Systems & High-Value Roofing Composites

Owens Corning’s February 2025 divestiture of its Global Glass Reinforcements business to Praana Group marks a major portfolio recalibration toward higher-margin building materials, insulation systems, and roofing composites. Retaining its vertically integrated glass nonwovens division strengthens OC’s leadership in shingle mat substrates, roofing reinforcement composites, and moisture-resistant construction laminates. With 85+ years of materials innovation, the company continues developing advanced fiber-sizing chemistries tailored for automotive SMC and LFT molding, Class-A surface panels, electrical housings, and lightweight structural components. OC remains influential in automotive and transportation composites by optimizing surface energies, fiber-matrix bonding, and durability performance-key requirements for enabling mass adoption of composite replacement parts.

China Fiberglass Co., Ltd. - High-Quality E-Glass Producer for Marine, Wind & Industrial Composites

China Fiberglass is a major global supplier of certified E-glass and high-silica fibers, meeting international accreditation standards such as DNV and Lloyd’s Register, which govern marine structures, wind blades, and offshore components. Its strong portfolio-including woven rovings, chopped strand mats, direct rovings, and stitched fabrics-supports a wide variety of manufacturing processes including hand lay-up, spray-up, infusion, RTM, and filament winding. The company’s focus on cost-efficient production enables widespread GFRP adoption in emerging markets for chemical-resistant piping, storage tanks, desalination systems, and wastewater treatment hardware. Continuous investments in high-speed winding systems, automated chopping lines, and melt-quality control have improved product consistency, filament uniformity, and laminate mechanical properties.

AGY Holding Corp. - S-2 Glass Specialist for Aerospace, Defense & High-Performance Composite Systems

AGY is globally recognized for its S-2 Glass® Fiber, engineered for extreme strength and energy absorption, offering 15% higher modulus and superior impact resistance compared to standard E-glass. This positions AGY as a material supplier of choice for aerospace rotor blades, missile structures, ballistic armor, rocket motor casings, and high-pressure filament-wound vessels. Its Zentron® high-performance rovings support precision filament winding, delivering the fiber alignment and tensile stability required in high-load propulsion and pressure containment systems. AGY’s advanced fiber-sizing systems are optimized for tough processing conditions-pultrusion, VARTM, and wet winding-ensuring excellent wet-out, improved interfacial adhesion, and enhanced fatigue performance in mission-critical applications. The company’s long-standing expertise in high-temperature glass chemistries solidifies its role as a premium supplier to aerospace, defense, and specialty industrial markets where mechanical resilience is non-negotiable.

China continues to anchor the global GF and GFRP composites market through unmatched production scale, while decisively shifting toward high-end, application-specific glass fiber reinforcements. The “Three-High” development framework-high quality, high efficiency, and high-end output-is reshaping China’s competitive posture away from commodity E-glass toward electronic-grade fibers, thermoplastic-compatible rovings, and high-modulus S-glass. Leading producers such as China Jushi are aligning capacity expansions with downstream demand from 5G infrastructure, AI-computing hardware, and large offshore wind turbine blades. At the same time, Chinese manufacturers are strategically localizing production overseas to mitigate trade barriers. Facilities such as Jushi Egypt have strengthened China’s indirect access to EU and U.S. markets, reinforcing export resilience despite tightening anti-dumping regimes. This dual-track approach-domestic upgrading and offshore localization-cements China’s role as both the volume backbone and an increasingly sophisticated technology supplier in the GF and GFRP ecosystem.

United States’ Strategic Specialization and Infrastructure-Led GFRP Demand

The United States GF and GFRP composites market is defined by portfolio rationalization and infrastructure-driven specialization rather than broad capacity growth. Major players are reallocating capital toward higher-margin building products, insulation systems, and corrosion-resistant infrastructure solutions. The strategic divestiture of glass reinforcement operations by Owens Corning reflects a wider industry shift toward integrated systems rather than standalone fiber supply. Concurrently, federal infrastructure funding is accelerating the adoption of GFRP rebar in coastal bridges and marine environments, where corrosion resistance delivers clear lifecycle cost advantages over steel. The increasing use of E-CR glass in U.S. public works projects highlights a structural demand trend tied to durability, resilience, and climate adaptation. As a result, the U.S. market is evolving into a demand-driven, specification-heavy environment favoring certified, performance-optimized GFRP solutions.

Germany’s Recyclable Composites Agenda and Hydrogen-Based Glassmaking

Germany stands at the forefront of Europe’s transition toward circular GF and GFRP composites, driven by regulatory pressure and advanced materials research. The launch of the “New Recyclable Composites” priority program has created a dedicated R&D pathway for soluble matrix systems that allow glass fiber recovery without mechanical degradation. This initiative directly addresses one of the industry’s most persistent challenges: end-of-life recycling of FRPs. In parallel, Germany’s expanded lightweighting strategy is incentivizing SMEs to develop bio-based and recyclable GFRP components for automotive and aerospace applications. On the production side, German manufacturers are piloting hydrogen-fueled furnaces in glass melting operations to comply with CBAM requirements and future-proof export competitiveness. Germany’s influence in the GF and GFRP market is therefore technological and regulatory, shaping global standards for recyclability and low-carbon composite manufacturing.

European Union Trade Defense and Strategic Autonomy in GFRP

At the regional level, the European Union is actively reshaping the competitive landscape through trade defense instruments and strategic autonomy policies. The imposition of definitive anti-dumping duties on glass fiber yarns and continuous filament GFR from China reflects a broader effort to stabilize domestic production capacity. By closing loopholes related to circumvention via third-country facilities, the EU is signaling a long-term commitment to protecting its composite supply chain. Simultaneously, the designation of GFRP as a critical material under the Clean Tech Supply Chain initiative elevates its importance for offshore wind, grid infrastructure, and green mobility projects. These measures collectively create a more predictable demand environment for European GF and GFRP producers while increasing compliance and cost pressures for import-dependent converters.

South Korea’s MPE 2030 Roadmap and High-Tech Composite Localization

South Korea’s GF and GFRP composites market is being rapidly transformed under the Materials, Parts, and Equipment (MPE) 2030 roadmap. National policy is explicitly targeting localization of high-performance composite substrates required for hydrogen storage systems, autonomous vehicle frames, and advanced battery housings. The creation of specialized industrial clusters is accelerating collaboration between fiber producers, resin formulators, and OEMs, shortening development cycles for next-generation GFRP components. Government-backed R&D into carbon-neutral glass fiber production further enhances South Korea’s export competitiveness in high-tech materials. This coordinated industrial approach positions South Korea as a fast-rising supplier of precision-engineered GFRP components rather than a commodity fiber producer.

Saudi Arabia’s Vision 2030 and Regional Glass Ecosystem Build-Out

Saudi Arabia is emerging as a strategic regional player in the GF and GFRP composites market by leveraging low energy costs, abundant silica resources, and strong state backing under Vision 2030. Large-scale glass manufacturing investments in Jubail Industrial City are laying the groundwork for a broader industrial glass and composite ecosystem. While current projects focus on flat and coated glass, the supporting infrastructure is directly relevant for future glass fiber and reinforcement capacity. In parallel, targeted investments under the National Industrial Development and Logistics Program are expanding pharmaceutical-grade glass and composite housings for medical devices, reducing import dependence and stimulating downstream composite demand. Saudi Arabia’s trajectory suggests a gradual but structurally important expansion into regional GF and GFRP supply chains.

National Strategic Development Matrix: GF and GFRP Composites Market (2025)

GF and GFRP Composites Market Development Matrix by Country

|

Country / Region

|

Primary Strategic Driver

|

Key 2025 Development

|

Core GF & GFRP Application Focus

|

|

China

|

“Three-High” industrial upgrading

|

Electronic-grade and S-glass expansion

|

Wind energy, electronics, exports

|

|

United States

|

Infrastructure resilience

|

GFRP rebar in coastal bridges

|

Public works, building products

|

|

Germany

|

Circular economy leadership

|

Recyclable composites (SPP 2528)

|

Automotive, aerospace lightweighting

|

|

European Union

|

Trade defense & autonomy

|

Anti-dumping duties on GFR

|

Offshore wind, clean energy

|

|

South Korea

|

MPE 2030 localization

|

High-performance composite clusters

|

Hydrogen, autonomous vehicles

|

|

Saudi Arabia

|

Vision 2030 diversification

|

Industrial glass ecosystem build-out

|

Construction, MedTech composites

|

Glass Fiber and GFRP Composites Market Report Scope

Glass Fiber and GFRP Composites Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$35.7 Billion

|

|

Market Size (2035)

|

$51.3 Billion

|

|

Market Growth Rate

|

3.7%

|

|

Segments

|

By Glass Fiber Type (E-Glass, S-Glass, C-Glass, E-CR Glass, A-Glass, D-Glass), By Fiber Form (Roving, Chopped Strands, Mats, Woven Fabrics, Pultruded Profiles), By Resin Type (Polyester, Vinyl Ester, Epoxy, Phenolic, Thermoplastics), By Manufacturing Process (Pultrusion, Compression Molding, Injection Molding, Filament Winding, Resin Transfer Molding, Hand Lay-Up), By Application (Construction & Infrastructure, Transportation, Wind Energy, Aerospace & Defense, Electrical & Electronics, Pipes & Tanks)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Owens Corning, China Jushi Co., Ltd., Saint-Gobain S.A., Chongqing Polycomp International, Taishan Fiberglass, Johns Manville, AGY Holding Corp., Nippon Sheet Glass Co., Ltd., Gurit Holding AG, Mitsubishi Chemical Group, Strongwell Corporation, Asahi Kasei Corporation, PPG Industries Inc., Exel Composites Oyj, Taiwan Glass Ind. Corp.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Glass Fiber and GFRP Composites Market Segmentation

By Glass Fiber Type

- E-Glass Fiber

- S-Glass Fiber

- C-Glass Fiber

- E-CR Glass Fiber

- A-Glass Fiber

- D-Glass Fiber

By Fiber Form

- Roving

- Chopped Strands

- Chopped Strand Mat

- Continuous Filament Mat

- Woven Fabrics

- Pultruded Profiles

By Resin Type

- Polyester Resin

- Vinyl Ester Resin

- Epoxy Resin

- Phenolic Resin

- Polypropylene

- Polyamide

- Polyethylene Terephthalate

- Polyetheretherketone

By Manufacturing Process

- Pultrusion

- Compression Molding

- Injection Molding

- Filament Winding

- Resin Transfer Molding

- Hand Lay-Up

By Application

- Construction and Infrastructure

- Transportation

- Wind Energy

- Aerospace and Defense

- Electrical and Electronics

- Pipes and Tanks

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Glass Fiber and GFRP Composites Market

- Owens Corning

- China Jushi Co., Ltd.

- Saint-Gobain S.A.

- Chongqing Polycomp International Corp.

- Taishan Fiberglass Inc.

- Johns Manville

- AGY Holding Corp.

- Nippon Sheet Glass Co., Ltd.

- Gurit Holding AG

- Mitsubishi Chemical Group Corporation

- Strongwell Corporation

- Asahi Kasei Corporation

- PPG Industries, Inc.

- Exel Composites Oyj

- Taiwan Glass Ind. Corp.

*- List not Exhaustive