Ceramic Matrix Composites Market Overview: High-Temperature CMCs Redefining Engine Efficiency

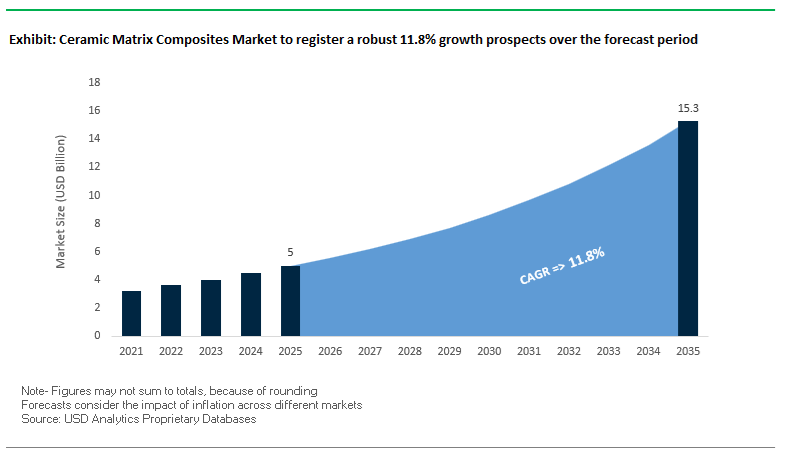

The global Ceramic Matrix Composites Market is projected to reach USD 5.0 billion in 2025, expanding at a robust CAGR of 11.8% between 2025 and 2035 to attain an estimated USD 15.3 billion by 2035. This growth is fundamentally driven by the replacement of nickel-based superalloys with SiC/SiC and C/SiC ceramic matrix composites in aero-engine hot-section components, industrial gas turbines, and high-performance braking systems. For manufacturers and material vendors, CMCs deliver a compelling combination of higher operating temperatures, dramatic weight reduction, reduced cooling air requirements, and superior creep and fatigue performance, making them a core enabler of next-generation propulsion and energy systems.

Engine OEMs are increasingly standardizing SiC fiber-reinforced SiC matrix (SiC/SiC) CMCs in turbine shrouds, combustor liners, and hot gas path parts to unlock higher thermal efficiency and lower fuel burn. At the same time, carbon fiber reinforced SiC (C/SiC) composites are becoming embedded in high-end braking systems and structural components that must withstand extreme cyclic loads with minimal degradation. As production volumes ramp up, the Ceramic Matrix Composites market is evolving from niche, demonstrator-level deployments to mass-production scale, compelling suppliers to invest heavily in fiber manufacturing, preform technologies, and environmental barrier coating (EBC) systems.

Key market insights for CMC manufacturers and vendors

- Ultra-high temperature capability: SiC/SiC CMC components enable jet engine parts such as turbine shrouds and combustor liners to operate at up to ~1,480°C (2,700°F), roughly 200–300°C higher than conventional nickel-based superalloys.

- Structural weight reduction: Replacing nickel superalloys with CMCs in engine hot sections typically delivers around 66% weight reduction (one-third the weight), directly improving thrust-to-weight ratio and fuel efficiency.

- Cooling air optimization: The superior high-temperature resistance of SiC/SiC CMC combustor liners can provide up to 60% reduction in cooling air requirements, allowing more air to be redirected to the core flow for higher thermal efficiency.

- Creep durability: Advanced CMC systems are engineered to maintain structural stability for over 1,000 hours at temperatures up to 1,200°C, meeting stringent creep resistance targets for long-life gas turbine applications.

- Fatigue performance: C/SiC composites deployed in braking systems and structural engine components have demonstrated survival of over 1,000,000 cycles at stresses near 90% of tensile strength, highlighting their damage-tolerant fatigue behavior for high-cycle applications.

Ceramic Matrix Composites Market Analysis: Aero Engine Programs and CMC Capacity Scale-Up

The Ceramic Matrix Composites Market is being shaped primarily by aero-engine and propulsion OEM roadmaps, where CMCs are indispensable to meeting aggressive fuel burn and emissions reduction targets. In November 2025, GE Aerospace announced an additional USD 105 million investment in its CMC production facility in Asheville, North Carolina, underpinning the rapid ramp-up of SiC/SiC components for LEAP and GE9X engines. This expansion is closely linked with job creation—131 new positions at Asheville and 15 more at West Jefferson—highlighting that CMC manufacturing is transitioning to true mass-production scale. In parallel, Arceon’s launch of Carbeon C/C-SiC CMCs in August 2024 for space, defense, and industrial furnace applications underscores the diversification of CMC demand beyond aviation into other extreme-temperature markets.

Technology programs are a core demand flywheel for CMC suppliers. CFM International’s RISE (Revolutionary Innovation for Sustainable Engines) program, which reported key technology milestones across May, June, and July 2025, explicitly centers on advanced core architectures that extensively leverage CMCs to deliver >20% fuel efficiency improvement over current engines. Similarly, Rolls-Royce’s ongoing 2025 test campaigns, including the Advance3 core and UltraFan demonstrator, are progressively incorporating CMC components into gas turbine cores to push the boundaries of operating temperature and cycle efficiency. Safran Aircraft Engines also reported a June 2025 milestone on composite fan blades for future engines, signaling that high-performance composites and CMCs will be jointly deployed across fan, compressor, combustor, and turbine architectures.

On the materials supply side, the Ceramic Matrix Composites Industry is experiencing pronounced supply chain tightening for SiC fibers and precursors. In late 2024 and early 2025, specialty SiC fiber and precursor producers (including suppliers of Nicalon and Tyranno fibers) reported heightened demand and mounting supply pressure due to the mass-production ramp-up of SiC/SiC CMCs for commercial aviation. This has intensified focus on integrated CMC–EBC systems, where ongoing 2025 R&D is directed at advanced Environmental Barrier Coatings capable of enabling SiC/SiC CMCs to operate at surface temperatures up to 2,700°F, while simultaneously reducing erosion rates and extending component life. As a result, the Ceramic Matrix Composites market is increasingly characterized by co-development between engine OEMs, fiber producers, and EBC formulators, consolidating CMCs as a critical enabling technology for sustainable aviation and next-generation high-temperature applications.

High-Temperature Capability, Oxidation Stability, and Ultra-High-Performance Design Driving Next-Generation CMC Adoption

Market Trend 1: Serial Production Scale-Up of SiC/SiC CMCs for Civil Aircraft Turbine Engines

A defining trend transforming the global Ceramic Matrix Composites Market is the industrialization of SiC/SiC CMCs for commercial aircraft turbine engines, driven by the need for higher thermal efficiency, reduced emissions, and weight reduction. SiC/SiC CMCs can withstand >1,500°C (2,732°F)—a temperature margin 200–300°C above the limits of advanced air-cooled nickel superalloys. This temperature headroom directly contributes to raising turbine inlet temperature (TIT), improving engine thermal efficiency by up to 15% in next-generation turbofans.

Weight reduction is a second crucial advantage. At ~3.2 g/cm³, SiC/SiC CMCs are 60–70% lighter than Ni-based alloys (~8.5 g/cm³), dramatically increasing the thrust-to-weight ratio and enabling new efficiency pathways across civil aviation platforms. Their structural superiority is further supported by non-brittle failure behavior, as SiC/SiC CMCs exhibit a fracture toughness (KIC) of 20–30 MPa·m½, compared to ~5 MPa·m½ for monolithic SiC. This improvement is enabled by meticulously engineered fiber–matrix interphases that promote crack deflection and controlled fiber pull-out. With aerospace OEMs scaling serial production of CMC turbine shrouds, vanes, and combustor liners, SiC/SiC is rapidly becoming the material foundation for hotter, lighter, and more fuel-efficient civil engines.

Market Trend 2: Adoption of Oxide/Oxide CMCs for Hydrogen-Compatible Industrial Gas Turbines

A parallel trend gaining traction is the deployment of Ox/Ox (oxide–oxide) CMCs in industrial gas turbines—particularly in hydrogen combustion environments where oxidation challenges are severe. Unlike SiC/SiC systems, Ox/Ox CMCs offer intrinsic oxidation and steam stability up to 1,150–1,250°C, eliminating the need for costly Environmental Barrier Coatings (EBCs). This property substantially reduces maintenance cycles, lifecycle costs, and coating-related failure risks.

From a mechanical durability perspective, optimized Ox/Ox systems achieve creep rupture lives >100 hours at 1,200°C under 80 MPa, outperforming single-crystal Ni-based superalloys subjected to identical conditions. Even more compelling is their tensile strength retention, as many Ox/Ox systems show no measurable tensile strength degradation after 1,000 hours at 1,200°C, whereas superalloys typically lose 70–80% of their strength. Additionally, Ox/Ox CMCs benefit from lower-cost Al₂O₃ fibers, simplified slurry infiltration processes, and reduced factory complexity, making them financially attractive for large turbine OEMs planning hydrogen-co-firing upgrades.

Market Opportunity 1: Ultra-High Temperature CMCs (UHTCs) for Hypersonic Vehicles and Extreme Aerothermal Loads

Hypersonic systems present one of the largest emerging opportunities in the CMC sector, with Ultra-High Temperature Ceramics (UHTCs) positioned as indispensable materials for reusable leading edges, nose cones, and sharp vehicle geometries. UHTC materials—especially HfB₂ and ZrB₂ matrices—exhibit melting points >3,000°C, making them uniquely capable of withstanding 2,000–3,000°C surface temperatures generated during Mach 5+ flight.

Under extreme heat fluxes, such as 15.2 MW/m² for 60 seconds, ZrB₂–SiC UHTCs form a dense, protective oxide layer that resists ablation and preserves component geometry—performance unattainable with traditional carbon–carbon ablatives. Their 40 mm²/s thermal diffusivity offers superior thermal shock resistance during rapid temperature ramps, while their 23–28 GPa Vickers hardness provides exceptional erosion and plasma resistance. As hypersonic programs expand across defense, commercial point-to-point travel, and space access, UHTCs represent one of the most strategically important growth vectors for advanced CMC suppliers.

Market Opportunity 2: Recycled Carbon Fiber-Based CMCs for High-Performance Automotive Braking Systems

A second high-growth opportunity lies in developing a recycled carbon fiber (rCF)-reinforced C/SiC CMC supply chain for braking systems in premium automotive, motorsport, and next-generation EV platforms. C/SiC brake discs manufactured with CF—partially substitutable by rCF—demonstrate exceptional durability, supporting vehicle lifetimes of ~300,000 km, compared to ~70,000 km for conventional gray cast iron rotors.

With densities of 1.68–1.72 g/cm³, these discs reduce brake system weight by 65–75%, drastically improving handling, acceleration, and energy efficiency for EVs. Their stable coefficient of friction (0.4–0.8) ensures consistent braking across varied loads and speeds, outperforming metallic brakes in fade resistance. Importantly, substituting virgin carbon fiber (vCF) with recycled carbon fiber significantly reduces embodied energy and overall lifecycle costs—showing ~8% total cost reduction over a 200,000 km use phase. This positions rCF-based CMCs as a core enabler of lightweight, sustainable, and high-performance automotive systems.

Ceramic Matrix Composites Market Share Analysis

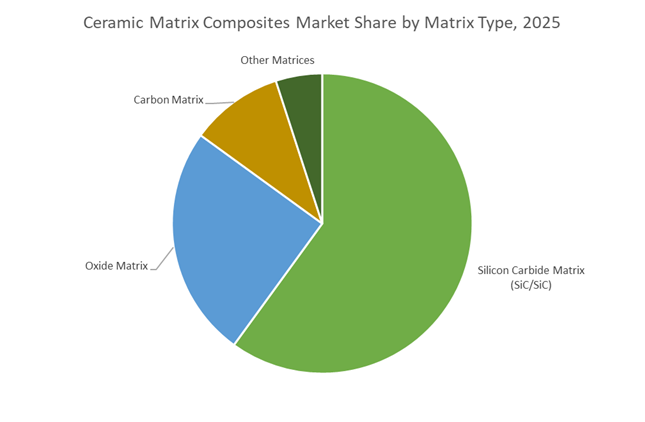

Market Share by Matrix Type: Silicon Carbide (SiC/SiC) Composites Lead Due to Superior High-Temperature Capability and Engine Efficiency Gains

Silicon Carbide Matrix (SiC/SiC) ceramic matrix composites hold the dominant market share—approximately 60% in 2025—because they deliver the highest combination of temperature tolerance, structural strength, and weight reduction essential for modern aerospace propulsion systems. Unlike oxide or carbon-matrix CMCs, SiC/SiC maintains mechanical integrity at temperatures exceeding 1,400°C, enabling its use in the hottest zones of gas turbine engines where metallic superalloys reach their thermal limits. The material’s low density—roughly one-third that of nickel-based superalloys—translates into substantial reductions in engine mass, particularly in rotating components, which directly improves fuel economy, reduces emissions, and increases thrust-to-weight ratios. SiC/SiC also provides exceptional resistance to oxidation, corrosion, and thermal shock, supporting reliable performance during rapid throttle changes and prolonged exposure to high-velocity combustion gases. With major engine platforms already integrating SiC/SiC turbine shrouds, combustor liners, and other hot-section components, the technology has progressed from R&D into serial production, solidifying its leadership in the global CMCs market. As aerospace propulsion systems push toward hotter, lighter, and more efficient designs—including hydrogen-capable engines and hybrid-electric propulsion—SiC/SiC remains the preferred material for next-generation high-temperature components.

Market Share by End-Use Industry: Aerospace & Defense Dominates as CMCs Become Critical to Next-Generation Propulsion and Hypersonic Systems

The Aerospace & Defense sector accounts for nearly 65% of the global CMCs market, driven by the material’s unique ability to enable higher turbine inlet temperatures, improved thermal efficiency, and substantial weight savings in advanced propulsion systems. In commercial aviation, CMC components in LEAP, GE9X, and other next-generation engines allow hotter combustion, lower cooling air requirements, and reduced fuel burn—improvements that deliver both operational savings and compliance with increasingly strict emissions regulations. In military aviation and hypersonic systems, SiC-based CMCs are indispensable for thermal protection structures, propulsion liners, nozzles, and aerodynamic surfaces that must withstand extreme temperature spikes during high-Mach flight and atmospheric re-entry. These mission-critical environments demand materials capable of maintaining structural integrity under severe thermal gradients and corrosive exhaust gases, requirements that conventional metal alloys cannot meet. Strong investment from major OEMs—including GE Aerospace, Pratt & Whitney, and Rolls-Royce—continues to accelerate CMC adoption across turbines, engines, exhaust components, and thermal barriers. As defense modernization programs expand and commercial fleets transition to ultra-efficient propulsion architectures, aerospace and defense remain the largest and fastest-advancing end-use sector in the global CMCs market.

Country Analysis: Global Drivers in Ceramic Matrix Composites (CMCs)

United States: SiC CMC Supply Chain Leadership, Hypersonics Funding, and Engine Commercialization Driving Global Market Influence

The United States remains the undisputed leader in the Ceramic Matrix Composites (CMCs) Market, strengthened by its unique ability to scale SiC CMC component production for high-temperature aerospace applications. A defining achievement is GE Aerospace’s establishment of the world’s first fully integrated SiC CMC supply chain, with precursor fiber production in Huntsville, Alabama, and component fabrication in Asheville, North Carolina—representing a multi-billion-dollar, decade-long industrialization effort that reached operational maturity by 2025. This vertically integrated ecosystem supports advanced engine platforms such as the GE9X, which has expanded the use of SiC/SiC CMCs across up to five hot-section components. These CMC deployments significantly reduce engine weight, increase thermal efficiency, and validate long-term durability under extreme temperatures, setting a new global performance benchmark for commercial aviation.

Federal programs further accelerate the U.S. CMC trajectory. The DoD’s $1.5 billion investment (2023) targeting high-speed defense systems—including hypersonic glide vehicles and scramjet propulsion—solidifies CMCs as critical materials for thermal protection and structural integrity. Simultaneously, the DOE’s advanced manufacturing investments (~$8 billion) promote CMC integration into next-generation gas turbines, with the goal of achieving 15% higher turbine efficiency via elevated operating temperatures. Additional breakthroughs include successful U.S. testing of CMC rotating parts, representing a major R&D frontier with potential to reshape engine architectures. Together, these forces position the U.S. as the global epicenter of CMC innovation, engine commercialization, and strategic materials investment.

United Kingdom: UltraFan and Advance3 Programs Accelerating CMC Integration into Next-Generation Low-Emission Propulsion Systems

The United Kingdom’s leadership in the CMC landscape is anchored by its advanced aero-engine development programs, spearheaded by Rolls-Royce. The UK’s primary material breakthrough is the integration of CMC components into the UltraFan and Advance3 demonstrator engines, where ceramic matrix composites are applied in turbine shrouds, seal segments, and other high-temperature components. These CMC-enabled improvements directly support Rolls-Royce’s emissions-reduction strategy by enabling higher turbine inlet temperatures, improved thermal efficiency, and lower engine weight, all of which contribute to more fuel-efficient and lower-CO₂ propulsion systems expected to shape the next generation of wide-body aircraft.

Beyond industrial application, the UK sustains a robust ecosystem of academic and government-supported consortia dedicated to ceramic fiber weaving, environmental barrier coatings (EBCs), and oxidation-resistant CMC architectures. These national materials clusters ensure that the UK maintains a steady pipeline of innovation critical for protecting SiC-based CMCs from harsh steam-rich turbine environments. Collectively, the UK’s structured approach—combining engine integration, advanced materials research, and strategic collaboration—positions the nation as one of the leading global contributors to high-performance, low-emission CMC propulsion technologies.

China: Self-Sufficiency Strategy in SiC and C/SiC Composites for Commercial Aviation, Hypersonics, and Reusable Space Vehicles

China’s Ceramic Matrix Composites market is expanding at unprecedented speed, driven by commercial aviation ambitions, military modernization, and heavy state investment in strategic materials. Chinese manufacturers have begun supplying components for the CFM LEAP engine, which powers the domestically significant COMAC C919 aircraft—marking the early but meaningful adoption of CMC components within the country’s commercial aerospace ecosystem. This industrial foothold complements China’s long-term plan to reduce dependence on imported high-temperature aerospace materials.

State-owned enterprises and defense research institutions are directing substantial resources toward ultra-high temperature CMCs for hypersonic aircraft, reusable launch vehicles, and thermal protection systems. These R&D programs focus on achieving ablation resistance and structural stability under temperatures exceeding 2,000–3,000°C, recognizing that mastery of CMCs is central to advanced aerospace competitiveness. China is also accelerating the scale-up of PIP (Polymer Infiltration and Pyrolysis) and CVI (Chemical Vapor Infiltration) processing technologies to achieve domestic industrial control over microstructure refinement. This dual strategy—commercial adoption plus defense-driven materials science—positions China as a fast-rising global force in C/SiC and SiC-based CMC technology.

Germany: Energy-Sector CMCs, Oxide/Oxide Composite Adoption, and Circular Composites Strategy for Long-Term Sustainability

Germany’s contribution to the global CMC market extends beyond aerospace, with a major emphasis on integrating CMCs into Industrial Gas Turbines (IGTs) and energy systems undergoing modernization. German engineering firms and research institutions increasingly deploy Oxide/Oxide CMCs for gas turbine retrofits, capitalizing on their ability to withstand surface temperatures of up to 1,300°C with appropriate coatings. These materials support Germany’s flexible-grid renewable energy mandates, where turbines undergo frequent thermal cycling and require materials with exceptional thermal shock resistance.

The country’s innovation ecosystem—anchored by the Composites United network and Fraunhofer Institutes—drives national programs including EcoCeramic and hybrid CMC development. These initiatives explore hybrid material architectures, manufacturing scalability, and next-generation ceramic reinforcements for high-stress industrial environments. Germany is also a leading proponent of the circular composite economy, researching recycling pathways for complex fiber-reinforced composites, including end-of-life CMC components. This sustainability-driven approach strengthens Germany’s position as a global leader in industrial, renewable-energy, and circular-economy-driven CMC innovation.

Competitive Landscape of the Ceramic Matrix Composites Market: Engine OEMs and CMC Specialists

The Competitive Landscape of the Ceramic Matrix Composites Industry is dominated by a small group of engine OEMs and advanced materials specialists with deep expertise in SiC/SiC and C/SiC systems. GE Aerospace, Safran, Rolls-Royce, and Raytheon Technologies (Pratt & Whitney) are leading the adoption of CMCs in commercial and military engines, while Schunk Group is a key supplier of CMC braking and furnace systems. Across the value chain, these players are investing in vertical integration, process technologies such as CVI and PIP, and advanced EBCs, giving them strong control over performance, reliability, and long-term cost curves. The result is a Ceramic Matrix Composites market where technological know-how, process maturity, and supply chain integration are the primary competitive differentiators.

GE Aerospace: Scaling SiC/SiC CMC Production for LEAP and GE9X Engines

GE Aerospace is widely regarded as the pioneer in commercializing SiC/SiC CMCs for large-scale jet engines. The company has integrated CMC components into the CFM LEAP engine (turbine shrouds) and GE9X (combustor and high-pressure turbine components), setting benchmarks for fuel efficiency and operating temperature. In November 2025, GE Aerospace committed an additional USD 105 million investment into its North Carolina CMC facilities to address an anticipated tenfold increase in CMC demand over the coming decade. Supported by prior investments in SiC fiber and CMC tape plants in Huntsville, Alabama, GE’s vertical integration strategy ensures strong control over raw material quality and availability. Its use of CMC turbine shrouds in the LEAP engine has contributed to approximately 15% fuel efficiency improvement versus the CFM56, firmly positioning GE at the forefront of the Ceramic Matrix Composites market.

Safran: CMC Partner in the CFM RISE Program and Advanced Aero Engines

Safran, through CFM International (its 50/50 joint venture with GE), is a central player in the industrialization of CMCs for aero engines. The company co-develops and supplies CMC components for the CFM LEAP engine and is heavily invested in the CFM RISE program, which uses CMCs in advanced core components—compressor, combustor, and turbine—to tolerate higher operating temperatures that enable 20%+ reductions in fuel burn. Safran’s long-standing expertise in CERASEP® CMCs and high-temperature aerospace structures is underpinned by deep process capabilities in Chemical Vapor Infiltration (CVI) and Polymer Infiltration and Pyrolysis (PIP). Historically, Safran successfully tested CMCs in afterburner flame holders of the M88 engine, where CERASEP® CMCs endured 143 hours of operation at 1,180°C without failure, demonstrating the durability and reliability required for military propulsion and reinforcing Safran’s leadership in the CMC market.

Rolls-Royce: CMC Innovation for UltraFan and Next-Generation Gas Turbines

Rolls-Royce is a key innovator in oxide/oxide and SiC-based CMC systems targeting both civil and defense gas turbines. The company is actively developing and testing CMCs for UltraFan® and other next-generation engines, where weight reduction and enhanced thermal efficiency are critical competitive levers. Rolls-Royce has achieved notable success with self-sealing CMCs, such as SEPCARBINOX® A500 used in the F100 engine’s nozzle divergent seals, which exceeded full design life in ground engine tests. Its long-standing use of the PIP route, employing polyvinylsilane precursors to yield high-performance SiC materials, reflects a strong process-technology foundation. With a dedicated facility in Cypress, California, focused solely on CMC process development, Rolls-Royce is positioning CMCs as core elements in the engine core of future aircraft platforms, reinforcing its strategic stake in the Ceramic Matrix Composites Industry.

Raytheon Technologies (Pratt & Whitney): CMCs for Geared Turbofan and Defense Engines

Raytheon Technologies, through Pratt & Whitney, is a major developer and user of CMCs in both Geared Turbofan (GTF) and advanced military engines. Pratt & Whitney integrates CMCs into hot-section components of its commercial and defense portfolios, leveraging SiC/SiC materials to manage the extreme temperatures found in combustors and turbine stages. In the defense domain, it has been a leader in applying CMCs to engines such as the F135 powering the F-35 Joint Strike Fighter, where weight reduction translates directly into increased thrust and range. The company continues to invest in CMC coating technologies and Environmental Barrier Coatings to improve oxidation and steam-corrosion resistance at high pressures and temperatures. Collaborations with specialty fiber manufacturers to adopt next-generation ceramic fibers with superior creep and temperature stability further extend Raytheon’s competitive edge in high-performance CMC solutions.

Schunk Group: C/SiC and C/C CMC Solutions for Braking and High-Temperature Systems

Schunk Group is a major materials technology provider specializing in carbon and ceramic materials, including advanced carbon/carbon (C/C) and carbon/silicon carbide (C/SiC) Ceramic Matrix Composites. The company is a dominant supplier of C/C and C/SiC brake discs and pads for automotive and rail applications, where high friction coefficients, exceptional fade resistance, and stability at temperatures exceeding 1,000°C are critical performance metrics. Beyond mobility, Schunk supplies customized CMCs for high-temperature industrial applications, such as heating elements and kiln furniture, that exploit the material’s outstanding thermal shock resistance. The group’s strength lies in near-net-shape manufacturing of complex CMC geometries, using advanced 3D weaving and preform fabrication techniques to optimize fiber architecture for specific load paths. This combination of application know-how and process engineering makes Schunk a key non-aerospace pillar of the global Ceramic Matrix Composites Market.

Ceramic Matrix Composites Market Report Scope

Ceramic Matrix Composites Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5 Billion

|

|

Market Size (2035)

|

$15.3 Billion

|

|

Market Growth Rate

|

11.8%

|

|

Segments

|

By Matrix Type (Silicon Carbide Matrix, Oxide Matrix, Carbon Matrix, Other Matrices), By Fiber Reinforcement Type (Continuous Fiber, Woven Fiber, Short/Chopped Fiber, Other Reinforcements), By Fiber Material (Silicon Carbide Fiber, Alumina Fiber, Carbon Fiber, Other Fibers), By End-Use Industry (Aerospace & Defense, Energy & Power, Automotive, Industrial Equipment)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

GE Aerospace, Rolls-Royce, SGL Carbon, Kyocera, CoorsTek, Mitsubishi Chemical Group, Lancer Systems, Axiom Materials, Safran, Boeing, DuPont/Solvay, Ultramet, 3M Company, Spirit AeroSystems, COIC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ceramic Matrix Composites (CMCs) Market Segmentation

By Matrix Type

- Silicon Carbide Matrix (SiC)

- Oxide Matrix

- Carbon Matrix

- Other Matrices

By Fiber Reinforcement Type

- Continuous Fiber

- Woven Fiber

- Short / Chopped Fiber

- Other Reinforcements

By Fiber Material

- Silicon Carbide Fiber

- Alumina Fiber

- Carbon Fiber

- Other Fibers

By End-Use Industry

- Aerospace & Defense

- Energy & Power

- Automotive

- Industrial Equipment

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Ceramic Matrix Composites (CMCs) Market

- GE Aerospace

- Rolls-Royce

- SGL Carbon

- Kyocera

- CoorsTek

- Mitsubishi Chemical Group

- Lancer Systems

- Axiom Materials

- Safran

- Boeing

- DuPont / Solvay

- Ultramet

- 3M Company

- Spirit AeroSystems

- COIC

*- List not Exhaustive

Research Coverage

This Ceramic Matrix Composites (CMCs) Market study from USDAnalytics delivers a rigorously engineered assessment of how SiC/SiC, C/SiC, Ox/Ox, and other advanced CMC systems are transforming aero-engines, industrial gas turbines, automotive braking, and high-temperature industrial equipment. Building on quantitative demand modelling to 2035, this report investigates the shift from nickel-based superalloys to lightweight, ultra-high-temperature CMC architectures, examines supply-chain constraints in SiC fibers and precursors, and tracks technology programs such as LEAP, GE9X, UltraFan, and CFM RISE that are scaling CMCs into serial production. The analysis reviews emerging breakthroughs in environmental barrier coatings (EBCs), oxide/oxide CMCs for hydrogen-ready turbines, ultra-high-temperature ceramic (UHTC) CMCs for hypersonics, and recycled carbon fiber–based C/SiC for next-generation braking systems, while mapping how regional industrial policies in the United States, United Kingdom, China, and Germany are reshaping competitive dynamics. It highlights matrix and fiber innovations, process routes such as CVI and PIP, and OEM–material supplier partnerships that are redefining engine efficiency, weight reduction, and lifecycle cost structures. Designed for strategy, R&D, procurement, and investment teams, this report is an essential resource for stakeholders seeking data-backed insight into CMC deployment roadmaps, qualification timelines, and value-creation opportunities across aerospace & defense, energy & power, automotive, and industrial equipment supply chains.

Scope Highlights

- Segmentation

- By Matrix Type: Silicon Carbide Matrix (SiC), Oxide Matrix, Carbon Matrix, Other Matrices

- By Fiber Reinforcement Type: Continuous Fiber, Woven Fiber, Short / Chopped Fiber, Other Reinforcements

- By Fiber Material: Silicon Carbide Fiber, Alumina Fiber, Carbon Fiber, Other Fibers

- By End-Use Industry: Aerospace & Defense, Energy & Power, Automotive, Industrial Equipment

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data from 2021 to 2025 and detailed forecasts from 2026 to 2034.

- Companies: In-depth analysis and profiles of 15+ leading CMC and propulsion players, including engine OEMs, fiber suppliers, and specialist CMC fabricators.