Silicon Carbide Fibers Market Overview: Ultra-High-Temperature SiC Composites Redefining Aerospace and Energy

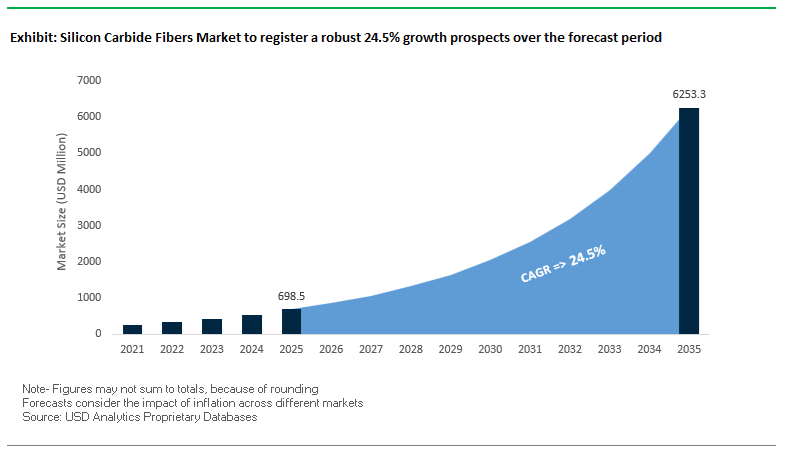

The Silicon Carbide Fibers Market is projected to grow from USD 698.5 million in 2025 to around USD 6,249.7 million by 2035, registering an exceptional CAGR of 24.5% (2025–2035). This explosive growth is driven by the shift from traditional superalloys to SiC fiber–reinforced ceramic matrix composites (SiC/SiC CMCs) in aerospace engines, nuclear reactors, and advanced energy systems, where ultra-high temperature stability, creep resistance, and density advantages directly translate into fuel savings, higher thrust, and lower CO₂ emissions. For manufacturers and vendors, the silicon carbide fibers industry is evolving from niche, defense-driven applications to scaled industrial adoption in commercial aviation and nuclear power, with procurement choices increasingly driven by temperature capability, oxidation resistance, and integration into qualified CMC systems rather than by fiber price alone.

Near-stoichiometric SiC fibers such as Tyranno SA and Hi-Nicalon Type-S, with oxygen content below 1.0%, can retain mechanical properties at temperatures above 1,500°C in aerobic environments, far beyond the limits of nickel-based superalloys. The creep-rupture-resistant grades, with crystallite sizes ≤200 nm, deliver long-term dimensional stability at 2,500°F (1,370°C) in gas turbine hot sections, supporting thousands of operating hours. With a tensile modulus between 380–420 GPa and a density of only ~3.10 g/cm³ (roughly one-third that of conventional superalloys), SiC fibers enable weight reductions and fuel-efficiency gains up to 15% in critical components such as turbine shrouds for LEAP-class engines.

Key insights for manufacturers and vendors in the Silicon Carbide Fibers Market:

- Ultra-high temperature stability: Near-stoichiometric SiC fibers with <1.0% oxygen content maintain strength beyond 1,500°C, unlocking new design envelopes for hot-section aerospace and nuclear components.

- Creep and fatigue performance: Optimized microstructures (SiC crystallites ≤200 nm) deliver outstanding creep resistance at 2,500°F (1,370°C) over thousands of hours, critical for long-life rotating turbine parts.

- High stiffness and structural efficiency: Tensile modulus of 380–420 GPa supports lightweight, high-stiffness SiC/SiC composites in reactor core structures, turbine shrouds, and advanced propulsion systems.

- Density advantage vs. superalloys: At ~3.10 g/cm³, SiC fiber-based CMCs are roughly one-third the density of nickel superalloys, enabling up to 15% fuel burn reduction in next-generation engine architectures.

- Cross-sector adoption: Beyond aviation, SiC fiber felts and fabrics are seeing increased uptake in fuel cells, advanced battery insulation and high-temperature energy systems, broadening the silicon carbide fibers industry demand base.

Silicon Carbide Fibers Market Analysis: Turbine, Nuclear and Defense Programs Scaling SiC/SiC Adoption

Recent developments in the global Silicon Carbide Fibers Market highlight a decisive transition from lab-scale validation to industrial-scale deployment across aerospace, nuclear, and energy applications. In Q4 2024, CFM International’s LEAP engine, which incorporates 18 SiC CMC turbine shrouds per engine, crossed a major flight-hour milestone, validating the long-term reliability of SiC fiber–reinforced CMCs in commercial narrow-body aircraft and strengthening the business case for further SiC fiber investments. Earlier, in January 2024, Chinese producer Ningxia Anteli Carbon Material Co. Ltd accelerated continuous SiC fiber production, signaling Asia-Pacific’s strategic push to localize high-temperature composite precursor supply and reduce dependence on imported fibers. In parallel, May 2024 saw industrial manufacturers expand the use of SiC fiber felts in new energy systems—such as hot-zone insulation for fuel cells and advanced battery systems—leveraging the material’s chemical inertness and thermal stability as the nanomaterials and electrification value chains converge.

On the technology and performance front, August 2025 academic reports confirmed that monazite coatings applied to SiC fibers (e.g., Tyranno SA and Sylramic) can significantly inhibit oxidation under dry conditions, extending fiber lifetime in aggressive gas turbine environments. In September 2025, research on SiC/SiC composites reinforced with high-purity fibers like Hi-Nicalon Type-S demonstrated that optimizing carbon interphase thickness (30–230 nm) can substantially enhance in-plane tensile strength—directly improving composite damage tolerance and reliability for engine hot-section parts. Meanwhile, the U.S. Department of Energy (DOE) continued, in February 2025, to channel funding into SiC fiber–reinforced CMCs as leading candidates for Accident Tolerant Fuel (ATF) cladding in nuclear reactors, underlining SiC’s strategic role in next-generation nuclear safety.

The defense and advanced propulsion ecosystem is also a major catalyst for the SiC fibers industry. In Q2 2025, the U.S. Air Force Research Lab extended support for Title III programs aimed at increasing domestic capability to produce next-generation SiC ceramic fibers rated for up to 2,400°F (1,315°C) in military propulsion systems, bolstering U.S. supply-chain resilience. On the downstream integration side, GE Aerospace announced in November 2025 a USD 14 million investment to expand its Pune, India manufacturing facility, further strengthening its ability to produce advanced engine components that rely heavily on SiC CMCs derived from high-performance SiC fibers. Alongside, broader new-energy and high-temperature process industries increasingly specify SiC fiber products for thermal management and insulation, confirming that the Silicon Carbide Fibers Market is structurally aligned with long-cycle megatrends in decarbonized aviation, nuclear energy, and defense propulsion.

High-Temperature Stoichiometric Fiber Expansion, Industrial-Grade Non-Stoichiometric Materials, Nuclear-Ready SiC Preforms, and MMC-Based Thermal Management Advancements

Market Trend 1: Rapid Scale-Up of Stoichiometric, High-Strength SiC Fibers for Extreme-Temperature Aerospace and Energy Systems

A defining transformation within the Silicon Carbide Fibers Market is the accelerated deployment of third-generation, near-stoichiometric SiC fibers such as Hi-Nicalon Type-S and Tyranno SA. These fibers are engineered to retain exceptional mechanical performance at temperatures at which earlier materials rapidly degrade. While first-generation SiC fibers lose tensile strength beyond 1200°C, new stoichiometric fibers can maintain ~2.0 GPa strength at 1600°C in inert conditions—positioning them as indispensable reinforcements in next-generation ceramic matrix composites (CMCs).

High-temperature creep resistance is another core differentiator. CMCs reinforced with Hi-Nicalon Type-S fibers have demonstrated <0.3% total creep strain after 100 hours under 138 MPa stress at 1315°C, confirming their suitability for turbine hot-section components, exhaust systems, and hypersonic platforms. Emerging developmental fibers further reinforce the market direction, retaining 97.2% tensile strength after annealing at 1900°C for one hour, demonstrating superior microstructural stability at ultrahigh temperatures. These performance benchmarks are central to global efforts to replace metallic alloys with lightweight, oxidation-resistant SiC composites across aerospace propulsion, thermal protection systems, and industrial ultra-heat applications.

Market Trend 2: Commercial Uptake of Cost-Optimized Non-Stoichiometric SiC Fibers for Mid-Temperature Industrial Applications

Parallel to the high-end aerospace segment, the market is witnessing accelerated adoption of non-stoichiometric SiC fibers (Tyranno Lox-M, Nicalon NL) that offer cost-effectiveness for industrial environments operating below 1000–1200°C. Unlike carbon fibers, which oxidize rapidly, SiC fibers exhibit superior oxidation resistance—highlighted by data showing SiC-coated carbon fibers gain an oxidation temperature margin of 140–320°C over uncoated variants.

These fibers also exhibit outstanding mechanical stability under oxidative stress. For example, a Tyranno ZMI-SiC/SiC composite retained 100% of its strength after oxidation at 1200°C for 100 hours, attributed to the development of a protective silica layer that prevents fiber degradation. This capability broadens the addressable market for SiC fibers, enabling their use in industrial burners, molten-metal handling systems, chemical reactors, and protective insulation components where temperatures exceed the safe limits of carbon fibers and stainless-steel reinforcements.

Market Opportunity 1: Engineering Nuclear-Grade SiC Fiber Preforms for Fusion and Fission Reactor Technologies

Nuclear power modernization—especially in fusion reactor development—is creating a high-value opportunity for SiC fiber preforms and SiC/SiC composites due to their unmatched resilience in extreme neutron radiation environments. Fusion reactors expose structural materials to high displacement damage rates of 45–105 dpa per effective full-power year, yet SiC maintains microstructural stability far better than metals, which suffer swelling, embrittlement, and phase decomposition at comparable damage levels.

In addition to displacement damage, fusion systems generate substantial helium through transmutation reactions. SiC materials experience 50–180 appm helium per dpa, yet their microstructure remains stable enough for long-term use, whereas metallic alloys typically blister or fracture under similar helium concentrations. One of the overarching safety and economic advantages is SiC’s low induced radioactivity, enabling potential classification as Class C low-level waste, which reduces disposal complexity. Mechanical performance is reinforced by the fibers’ contribution to damage tolerance, with SiC composites showing ~4.25 MPa·m1/2 fracture toughness, essential for containment structures, first walls, blankets, and control components in next-generation nuclear systems.

Market Opportunity 2: Commercialization of SiC Fiber-Reinforced Metal Matrix Composites (MMCs) for High-Efficiency Thermal Management

As semiconductor power densities escalate in aerospace electronics, EV power modules, radar systems, and satellite payloads, SiC fiber-reinforced metal matrix composites are emerging as a critical solution for high-performance thermal management. SiC-Al MMCs demonstrate 175–256 W/m·K thermal conductivity, surpassing pure aluminum (~237 W/m·K). This high heat-spreading capability is complemented by a low Coefficient of Thermal Expansion (CTE) of 3×10⁻⁶ to 8×10⁻⁶/°C, closely matching semiconductor materials and drastically reducing interfacial stresses in power electronics packaging.

Mechanical advantages reinforce their thermal value proposition. SiC MMCs deliver three times the specific stiffness of cast iron, enabling significant weight reduction without compromising structural performance. Their density is less than one-quarter that of copper, allowing designers to replace traditional heat spreaders with lightweight MMC alternatives—an essential requirement for aerospace avionics, UAVs, satellite electronics, and EV inverters where mass directly affects efficiency and performance.

Silicon Carbide Fibers Market Share Analysis

Market Share by Fiber Generation: First Generation SiC Fibers Retain Share Through Cost Efficiency and Established Use-Cases

First Generation Silicon Carbide (SiC) Fibers account for roughly 15% of the global SiC fibers market, retaining a meaningful share despite the shift toward higher-performance 2nd and 3rd generation fibers. Their continued relevance is driven by their mature production processes, favorable cost structure, and suitability for non-critical, mid-temperature applications, which collectively sustain steady industrial adoption. These early-generation fibers—typically represented by Nicalon—contain higher oxygen and excess carbon content, limiting their maximum service temperature to ~1200°C. However, this performance range remains sufficient for many aerospace secondary structures, thermal protection systems outside the engine hot zone, metal matrix composites, and polymer matrix composites used in lightweight defense structures and industrial equipment. Their lower price point relative to ultra-high-purity 3rd generation fibers makes them a practical choice for applications that do not require extreme thermomechanical stability or oxidation resistance. As OEMs and Tier-1 suppliers balance performance requirements with material cost, First Generation fibers continue to offer an accessible entry point for SiC-reinforced composite adoption, thereby sustaining their position in the overall market mix even as next-generation fibers gain prominence.

Market Share by End-Use Industry: Aerospace & Defense Dominates Due to Mission-Critical Demand for High-Temperature CMCs

The Aerospace & Defense sector, holding approximately 65% of the global SiC fibers market, is the unequivocal growth engine and highest-value segment due to its stringent performance requirements and rapid adoption of SiC/SiC Ceramic Matrix Composites (CMCs) in next-generation propulsion and thermal management systems. SiC fibers enable step-change improvements in engine efficiency and durability because SiC CMCs operate at temperatures up to 1650°C, far surpassing nickel-based superalloys limited to roughly 1100°C. Their extreme heat tolerance, coupled with a weight reduction of up to 70%, directly translates into major benefits for jet engines, including improved thrust-to-weight ratios, reduced cooling air requirements, and fuel consumption reductions in the range of 10–15%, as demonstrated in advanced commercial engines like GE’s LEAP. These performance gains align with aviation’s core imperatives: lowering emissions, increasing fuel efficiency, and reducing maintenance intervals. Additionally, defense applications—including thermal protection systems, hypersonic vehicles, missile propulsion components, and lightweight armor—depend heavily on SiC fibers’ stability under extreme stress and temperature. Because aerospace applications involve stringent qualification cycles and extremely high reliability requirements, SiC fibers used in this sector command premium prices—often ranging from $1,400 to $9,000 per kilogram—cementing Aerospace & Defense as the market’s highest revenue contributor. This entrenched reliance on SiC CMCs ensures that the segment will continue to dominate SiC fiber consumption over the next decade.

Fibers Market Share by End-Use Industry, 2025.png)

Country Analysis: Global Silicon Carbide Fibers Hotspots and Strategic Material Development

United States: Defense-Driven Silicon Carbide Fiber Industrialization and Domestic CMC Supply Chain Expansion

The United States remains a strategic center for Silicon Carbide (SiC) fibers due to its government-backed push for domestic production and aerospace-grade material independence. A major milestone occurred in December 2024, when General Atomics (GA-EMS) secured a DOE contract supporting the deployment of SiC-based Ceramic Matrix Composites (CMCs) for structural components in fusion power systems. This effort builds on decades of U.S. investment into SiC fiber applications for nuclear fuel cladding, reinforcing the material’s relevance for high-temperature, radiation-resistant energy technologies.

Beyond energy, the U.S. defense and aerospace sectors are heavily mobilizing to strengthen domestic SiC fiber manufacturing capacity. A multistakeholder consortium—comprising COI Ceramics, Honeywell, Rolls-Royce, Pratt & Whitney, and Oak Ridge National Laboratory—is executing a national initiative to establish a Continuous Scalable Process for Domestic SiC Fiber Production. This program directly addresses supply chain vulnerabilities caused by historical dependence on Japanese imports and aims to deliver cost-competitive fibers for next-generation CMCs. The momentum is also visible in jet engine manufacturing: Pratt & Whitney is increasing the incorporation of SiC-reinforced CMCs in hot-section components of engines such as the F135, enabling reductions in weight, fuel burn, and thermal loads compared to nickel-based superalloys. Together, these efforts position the U.S. as a rising force in high-performance SiC fiber adoption, especially in defense propulsion and extreme-environment engineering.

Japan: Global Technology Leader in Polymer Precursor SiC Fibers and Next-Generation High-Purity Filament Innovation

Japan maintains an undisputed leadership position in Silicon Carbide fiber technology through decades of innovation in the Polymer Precursor Method, widely known as the Yajima Process. Companies such as Nippon Carbon and UBE Corporation hold foundational patents and continue to produce globally recognized continuous SiC filaments including Nicalon, Tyranno, and Sylramic, which are essential for high-stress, long-duration environments across aerospace, energy, and industrial gas turbines. Japan’s dominance lies in the precision synthesis of fibers that consistently achieve exceptional tensile strength, controlled microstructure, and long-term oxidative stability.

Recent Japanese R&D emphasizes the commercialization of third-generation, near-stoichiometric SiC fibers, which exhibit dramatically improved creep resistance and stability at temperatures exceeding 1,800°C. These ultra-high-purity fibers are pivotal for future industrial gas turbine engines, hydrogen-fueled turbine systems, and hypersonic propulsion. As global aerospace OEMs explore hotter, more efficient engines, Japan’s SiC fibers remain the benchmark, and its material science leadership ensures it will continue to define performance standards for continuous SiC filaments worldwide.

China: Rapid Scale-Up of Second-Generation Silicon Carbide Fibers and Cost-Efficient Industrialization

China’s Silicon Carbide fibers market is expanding at an unparalleled scale, driven by aggressive national industrialization strategies and strong domestic aerospace demand. Ningbo Zhongxing New Materials Co., Ltd. has emerged as a major force, successfully scaling production to 10 tons of second-generation SiC fibers and outlining ambitious plans to reach 80–100 tons per year. This level of expansion positions China among the largest global suppliers of mid-grade SiC fibers, enabling broader adoption in domestic aircraft, unmanned systems, industrial furnaces, and heat exchanger components.

A notable focus in China is cost optimization. Chinese producers are refining the Polymer Precursor Process to make SiC fibers more accessible for cost-sensitive sectors such as industrial thermal systems and high-temperature filtration. This strategy accelerates the penetration of SiC fiber materials into mid-range industrial applications traditionally dominated by lower-performance refractory fibers. With parallel investments in aerospace materials, China is rapidly evolving from a follower to a major competitor in the second-generation SiC fiber landscape.

Germany/European Union: Building an Independent SiC Fiber Value Chain and Developing High-Temperature Industrial-Grade Fibers

Germany and the broader European Union are channeling significant public-private investments into SiC fiber innovation to reduce dependence on imports and secure strategic autonomy in Ceramic Matrix Composites (CMCs). A cornerstone of this effort is the Fraunhofer Center for High-Temperature Lightweight Construction (HTL) pilot plant in Bayreuth, Germany, which is designed to transition SiC fiber technology from laboratory scale to pre-industrial qualification. This facility plays a pivotal role in establishing a fully European SiC fiber value chain, supporting applications in aerospace engines, energy conversion, hydrogen turbines, and defense.

The EU’s Horizon 2020/Europe initiatives further strengthen the region’s capabilities. Funding directed to companies such as BJS Ceramics has enabled the successful development of third-generation SiC fibers capable of withstanding temperatures ≥1500°C (2732°F)—a vital threshold for next-generation turbines and energy systems. The region’s strategic focus on sovereignty in critical materials, combined with its strong environmental and safety regulations, ensures that Europe will emerge as a technologically sophisticated producer of specialized SiC fibers for high-value industrial sectors.

South Korea: Fusion Energy Innovation and SiC-Based Thermal Management Components

South Korea’s Silicon Carbide fiber activity is increasingly tied to advanced energy and electronics applications. National research institutions are prioritizing SiC fiber-reinforced CMCs for nuclear fusion reactor components, particularly within the KSTAR (Korea Superconducting Tokamak Advanced Research) program. SiC fibers are uniquely suited for plasma-facing structures because of their neutron irradiation resistance, high-temperature tolerance, and low activation, making them essential to long-term fusion development. These efforts place South Korea among the global leaders exploring SiC fiber roles in future fusion energy ecosystems.

Beyond fusion, South Korean electronics manufacturers are investigating SiC fiber-based composites for thermal management solutions in high-power electronics, EV inverters, and battery systems. As semiconductor devices continue to shrink while power density rises, South Korea’s R&D on heat-dissipating materials incorporating SiC fibers is expanding rapidly. This positions the country as a key innovator in SiC-enabled electronic materials for both industrial and consumer technologies.

United Kingdom: Aerospace Engine Programs Driving Co-Development of Next-Generation SiC Fiber-Reinforced CMC Components

The United Kingdom maintains a strong presence in high-performance SiC fiber adoption due to its advanced jet engine manufacturing ecosystem. With major aerospace manufacturers operating within the UK, demand is rising for co-developed SiC fiber-reinforced CMC components used in hot-section parts of next-generation engines. These programs aim to enhance fuel efficiency, reduce engine weight, and improve thermal resilience, aligning with stringent emission and performance targets.

UK industry–university partnerships are accelerating research into new SiC fiber architectures, oxidation-resistant coatings, and CMC component prototyping. These advancements support ongoing development for civil and defense aviation platforms and reinforce the UK’s strategic role as a collaborator in cutting-edge CMC materials engineering. The region’s long-standing expertise in turbine technologies ensures continued investment in SiC fibers and integration into future propulsion systems.

Competitive Landscape of the Silicon Carbide Fibers Industry: Leading SiC Fiber Producers and Integrators

The competitive landscape of the Silicon Carbide Fibers Market is dominated by a small group of specialist fiber manufacturers and integrated engine/ceramics players that control critical know-how in polymer-derived ceramics, CVD processes, and CMC integration. Companies such as UBE Corporation, Specialty Materials Inc., Nippon Carbon, GE Aerospace, and CoorsTek are positioned across different points of the SiC value chain—from continuous fiber production and monofilament reinforcements to in-house SiC/SiC CMC tape and ultra-high-purity SiC components for semiconductor and fiber-coating applications. Their strategies cluster around three pillars: achieving near-stoichiometric fiber chemistries with extremely low oxygen content, scaling industrial CMC production linked to specific engine and reactor platforms, and leveraging high-purity SiC processing to serve both traditional high-temperature markets and fast-growing clean-energy segments.

UBE Corporation: Tyranno SiC fibers enable ultra-high-temperature lightweight composites

UBE Corporation is a foundational player in the Silicon Carbide Fibers Market with its well-established Tyranno Fiber® portfolio, ranging from standard oxygen-containing grades to high-performance, near-stoichiometric Tyranno SA fibers. The company’s SA grade combines oxygen content below ~1% with a tensile modulus around 380 GPa and heat resistance up to ~1,800°C, making it a reference material for SiC/SiC CMCs in gas turbines and advanced reactors. UBE’s strategy focuses on supplying a diverse grade spectrum that allows OEMs and tier-1s to tailor cost, performance, and processing for different high-temperature applications, from industrial furnaces to aeroengines. The firm aligns its SiC fiber technology with global priorities in energy efficiency, CO₂ reduction, and exhaust fume purification, framing Tyranno fibers as key enablers of lightweight, low-emission transportation platforms. This combination of materials breadth, thermal performance, and decarbonization positioning makes UBE a critical supplier in long-term aerospace and energy programs based on SiC/SiC composites.

Specialty Materials Inc.: SCS fibers power high-temperature titanium metal matrix composites

Specialty Materials, Inc. (SMI) differentiates itself in the SiC fibers industry through monofilament CVD expertise, producing its well-known SCS fibers (SCS-6™, SCS-Ultra™) in large-diameter formats typically between 75 and 142 μm. Manufactured via a chemical vapor deposition process onto a core, these fibers feature a unique columnar microstructure optimized for load transfer and damage tolerance when embedded in metal matrix composites (MMCs), especially titanium and aluminum systems. SMI’s SCS-Ultra™ grade is engineered for superior creep-rupture resistance, meeting the demanding requirements of rotating titanium aluminide (TiAl) engine parts operating in high-temperature zones. Strategically, the company positions itself as a reinforcement specialist for high-end MMCs, serving aerospace and defense OEMs that need stiffness, fatigue resistance, and long-term dimensional stability beyond what conventional alloys can offer. This strong focus on titanium MMCs and CVD monofilaments gives Specialty Materials a defensible niche in the broader Silicon Carbide Fibers Market.

Nippon Carbon: Hi-Nicalon SiC fibers underpin next-generation aerospace CMCs

Nippon Carbon Co., Ltd. is a technology leader in continuous SiC fibers with its flagship Nicalon™ family, including Hi-Nicalon and the high-end Hi-Nicalon Type-S grades. Hi-Nicalon Type-S is a highly crystalline, near-stoichiometric SiC fiber with an extremely low oxygen content of about 0.2% and a tensile modulus around 420 GPa, offering exceptional stiffness and high-temperature stability for SiC/SiC CMCs. The company is a key supplier to advanced aircraft and rocket propulsion systems, where radiation resistance, oxidation behavior, and creep performance at elevated temperatures are critical design parameters. Nippon Carbon’s strategic focus is to refine fiber microstructure and stoichiometry to maximize in-service life in harsh thermal and oxidative environments, particularly in turbine hot sections and re-entry or hypersonic structures. Its Hi-Nicalon platform has effectively become a benchmark for high-purity SiC fibers, placing Nippon Carbon at the center of many next-generation propulsion and space programs.

GE Aerospace: Integrated SiC fiber and CMC production for advanced jet engines

GE Aerospace is both one of the largest downstream users and a rapidly growing producer of silicon carbide fibers and CMC tape, having invested over USD 200 million in dedicated factories in Huntsville, Alabama to mass-produce SiC ceramic fibers and SiC/SiC CMC tape. The company integrates these fibers directly into platforms such as the LEAP and GE9X engines, where SiC CMCs are deployed in high-pressure turbine shrouds and hot-section components to deliver substantial weight savings and up to 15% fuel burn improvements versus prior generations. In November 2025, GE Aerospace further expanded its Pune, India facility with a USD 14 million investment, strengthening its global footprint for advanced engine components tightly coupled to SiC CMC technology. This mine-to-engine-hot-section style integration—from fiber production to composite design and engine certification—gives GE unique leverage over cost, qualification timelines, and performance optimization. As OEMs and airlines pivot to more efficient narrow-body and wide-body platforms, GE’s internal SiC fiber and CMC capability makes it a pivotal force in the global Silicon Carbide Fibers Market.

CoorsTek: Ultra-high-purity silicon carbide components for extreme environments

CoorsTek, Inc. plays a critical enabling role in the Silicon Carbide Fibers Industry through its expertise in ultra-high-purity SiC materials, particularly PureSiC® CVD silicon carbide (>99.9995% purity) and CERASIC® sintered SiC. While CoorsTek does not primarily manufacture continuous SiC fibers, its CVD SiC processes and component portfolio are essential for applications such as semiconductor wafer boats, plasma etcher parts, and hot-zone hardware that operate at temperatures up to ~1,600°C and in corrosive environments. This high-purity SiC base is also relevant for fiber coatings, interphases, and precursor structures in SiC/SiC composite systems, where contamination and defect control are critical for long-life performance. CoorsTek’s strategic focus is on supplying extreme environment parts across semiconductors, energy, and industrial processing, leveraging its materials science and precision ceramics manufacturing to support the broader growth of SiC-based technologies, including SiC fibers and CMCs. Its position at the intersection of semiconductor, high-temperature ceramics, and SiC processing makes CoorsTek an important indirect but influential stakeholder in the Silicon Carbide Fibers Market ecosystem.

Silicon Carbide Fibers Market Report Scope

Silicon Carbide Fibers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$698.5 Million

|

|

Market Size (2035)

|

$6249.7 Million

|

|

Market Growth Rate

|

24.5%

|

|

Segments

|

By Fiber Generation (First Generation, Second Generation, Third Generation), By Fiber Form (Continuous Filament, Woven Cloth/Fabric, Short or Chopped Fibers), By Usage Type (Composite Applications, Non-Composite Applications), By End-Use Industry (Aerospace & Defense, Energy & Power, Industrial, Automotive)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Nippon Carbon (Nicalon), UBE (Tyranno), COI Ceramics, Specialty Materials, BJS Ceramics, Ningbo Zhongxing New Materials, Saint-Gobain, Morgan Advanced Materials, GE Aerospace, Rolls-Royce, Pratt & Whitney, Coherent Corp., Materion, UBE Industries, Hunan Zerafiber

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Silicon Carbide (SiC) Fibers Market Segmentation

By Fiber Generation

- First Generation

- Second Generation

- Third Generation

By Fiber Form

- Continuous Filament

- Woven Cloth / Fabric

- Short or Chopped Fibers

By Usage Type

- Composite Applications

- Non-Composite Applications

By End-Use Industry

- Aerospace & Defense

- Energy & Power

- Industrial

- Automotive

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Silicon Carbide (SiC) Fibers Market

- Nippon Carbon (Nicalon)

- UBE (Tyranno)

- COI Ceramics

- Specialty Materials

- BJS Ceramics

- Ningbo Zhongxing New Materials

- Saint-Gobain

- Morgan Advanced Materials

- GE Aerospace

- Rolls-Royce

- Pratt & Whitney

- Coherent Corp.

- Materion

- UBE Industries

- Hunan Zerafiber.

*- List not Exhaustive

Research Coverage

The latest Silicon Carbide Fibers Market study from USDAnalytics provides an in-depth strategic and technical assessment of how SiC fiber–reinforced ceramic matrix composites are displacing traditional superalloys in aerospace, nuclear, and advanced energy systems; this report investigates ultra-high-temperature performance windows, next-generation stoichiometric fiber platforms, coating architectures, and evolving qualification pathways across turbine, reactor, and defense programs. It synthesizes recent breakthroughs in third-generation low-oxygen SiC fibers, monazite and advanced interphase coatings, nuclear-grade SiC preforms, and SiC-based metal matrix composites, while analysis reviews OEM procurement strategies, defense-funded capacity expansion, and Asia–Europe–U.S. supply chain realignment. The study highlights the interplay between fiber generation, composite design, and end-use mission profiles, including how creep, oxidation resistance, and density advantages translate into fuel-burn reduction, CO₂ mitigation, and lifetime cost savings. Drawing on detailed benchmarking of leading producers, engine integrators, and nuclear technology developers, this report is an essential resource for materials engineers, turbine and reactor designers, defense acquisition planners, investment professionals, and strategic sourcing teams seeking to understand where silicon carbide fibers will create the highest value and how to position for the next wave of SiC/SiC CMC adoption.

Scope Highlights

- Segmentation (Fiber Generation, Form, Usage & End-Use Coverage)

• By Fiber Generation: First Generation, Second Generation, Third Generation

• By Fiber Form: Continuous Filament, Woven Cloth / Fabric, Short or Chopped Fibers

• By Usage Type: Composite Applications, Non-Composite Applications

• By End-Use Industry: Aerospace & Defense, Energy & Power, Industrial, Automotive

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, with detailed country-level outlooks, policy environments, and supply-chain positioning.

- Timeframe & Data Coverage: Historic market, pricing, and capacity data for 2021–2025 integrated with scenario-based forecasts for 2026–2034, including CAGR trends, technology penetration curves, and demand by fiber generation.

- Competitive analysis / profiles of 15+ key players across the SiC fiber and CMC value chain, including fiber manufacturers, engine and turbine OEMs, reactor technology developers, and specialist ceramics producers.