Market Overview: Ultra-High Strength, Thermal Conductivity, and Nanomaterial Performance Metrics Accelerate Market Growth

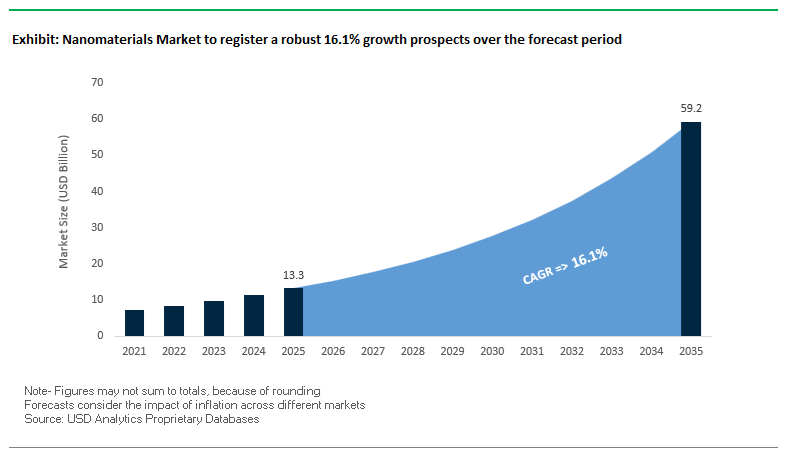

The Nanomaterials Market is projected to expand from USD 13.3 billion in 2025 to USD 59.2 billion by 2035, exhibiting an exceptional CAGR of 16.1%, one of the highest among advanced materials sectors. Growth is driven by rapidly rising adoption of carbon nanotubes (CNTs), graphene, nanoscale oxides, quantum dots, and engineered nanoparticles across electronics, semiconductors, medical therapeutics, composites, aerospace, and clean-energy systems. Manufacturers are scaling high-purity production processes to meet the stringent mechanical, electrical, and biocompatibility requirements of next-generation devices, especially as the U.S. alone continues to invest USD 2+ billion annually in nanotechnology R&D through the National Nanotechnology Initiative (NNI).

Demand is accelerating due to the unmatched material properties of carbon nanostructures. MWCNTs with tensile strengths up to 63 GPa—100× stronger than high-carbon steel—enable unprecedented reinforcement in aerospace and automotive composites. Graphene’s thermal conductivity of ~5,300 W/m·K, more than 13× higher than copper, positions it as a cornerstone of advanced thermal management systems for microelectronics. SWCNTs capable of carrying >10⁹ A/cm² current density—over 1,000× higher than copper—are increasingly targeted for semiconductor interconnects, EV batteries, and high-density energy storage devices. These properties collectively position nanomaterials as foundational elements in the transition toward lighter, faster, more energy-efficient, and higher-performing technologies.

Key Insights for OEMs, Material Scientists, and Nanotechnology Vendors

- MWCNTs deliver steel-beating strength (~63 GPa), enabling next-generation lightweight composites.

- Graphene offers world-leading thermal conductivity (~5,300 W/m·K), vital for heat-sensitive electronics.

- SWCNTs support ultra-high current densities (>10⁹ A/cm²), key for chip interconnect miniaturization.

- Government R&D support remains robust, with the U.S. NNI investing USD 2B+ annually in nanotechnology.

Market Analysis: Breakthroughs in CNT Manufacturing, Nanomedicine Advancements, and Global Production Expansions Drive Market Momentum

The Nanomaterials Market is witnessing rapid technological acceleration, with major global developments reshaping supply chains, production scalability, and application adoption. In January 2025, Tiannai Technology (China) introduced a new SWCNT grade engineered for solid-state EV batteries, reinforcing the role of CNTs as essential enablers of high-conductivity, high-energy-density battery architectures. The growing commercialization of SWCNT material systems is further supported by European expansions—most notably Nawah’s November 2024 inauguration of a large-scale carbon nanotube facility in France, boosting its annual 3D Nanocarbon production from 20,000 m² to 400,000 m² to meet European electronics demand.

OCSiAl made a major supply-chain impact in October 2024 by opening its first European TUBALL™ SWCNT production plant in Serbia, with an initial 60-ton/year capacity. This milestone strengthens the global pipeline for CNT masterbatches used in plastics, rubbers, composites, and conductive coatings. Simultaneously, nanomedicine is advancing at an unprecedented pace. In May 2025, Acuitas Therapeutics and Integrated DNA Technologies announced the first personalized CRISPR gene-editing treatment using lipid nanoparticles (LNPs), highlighting the expanding clinical reliance on nanoscale delivery vehicles. Regulatory support is also strengthening: in February 2024, the FDA authorized 26 new nanomaterial-enabled personalized medicines, showcasing momentum in nanotherapeutics and diagnostics.

Academic and industry research investments continue to fuel innovation. In June 2025, researchers leveraged microgravity environments to develop next-generation nanomaterials for osteoarthritis and cancer therapies, demonstrating the strategic value of space-based R&D. Educational institutions are building talent pipelines, as seen in May 2024 when Imperial College London launched a specialized Nanomedicine and Nanodiagnostics postgraduate program. Meanwhile, researchers at the University of Connecticut reported a breakthrough in April 2025, introducing a nanoparticle drug-delivery platform capable of targeting lung cells with high specificity, reinforcing the rapid expansion of targeted nanotherapeutic systems.

Industry-Defining Trends and Commercial Opportunities Driving Next-Generation Nanomaterials Innovation

Market Trend 1: Industrial-Scale Graphene & Graphene Oxide Production Transforming Energy Storage and High-Barrier Composite Systems

The nanomaterials market is experiencing a pivotal transformation as industrial-scale production of graphene and graphene oxide (GO) moves from laboratory output to commercial-grade volumes. In energy storage, Few-Layer Graphene (FLG) has demonstrated a reversible specific capacity of 500 mAh/g at a C/5 rate, substantially exceeding the 372 mAh/g theoretical maximum of conventional graphite used in Li-ion anodes. Even at extreme fast-charging conditions, graphene-based electrodes maintain high performance, retaining >370 mAh/g at a 25C discharge rate, positioning graphene as a core material for ultra-fast charging batteries, EV packs, and solid-state systems.

Graphene oxide is simultaneously reshaping the competitive landscape for advanced coatings and barrier materials. Incorporation of 1.5 wt% GO into HDPE reduces Oxygen Permeability (OP) from 120 cc/m²·day·atm to 1.9 cc/m²·day·atm, achieving a ~98% permeability reduction. GO flakes create a tortuous diffusion path that blocks moisture, oxygen, and corrosive ions (Cl⁻), significantly enhancing corrosion protection for industrial assets, pipelines, and protective marine coatings. These performance metrics illustrate why graphene and GO are central to next-generation composite structures, corrosion-resistant coatings, and multifunctional industrial materials.

Market Trend 2: Regulatory-Driven Acceleration of High-Purity, Fully Characterized Nanomaterials for Biomedical Use

Biomedical innovation is shifting toward high-purity, tightly controlled nanomaterials, driven by evolving FDA and ICH guidelines. The FDA’s expanded definition considers materials up to 1,000 nm (1 µm) as nanomaterials if engineered for nanoscale functionality, placing a broad array of therapeutic and diagnostic platforms under tighter regulatory oversight. This necessitates rigorous characterization of Critical Quality Attributes (CQAs) such as particle size, size distribution, surface charge, morphology, and aggregation state—parameters that directly influence biodistribution, cellular uptake, and therapeutic efficacy.

Stability requirements are equally stringent. FDA guidance mandates continuous monitoring for nanomaterial aggregation, morphology shifts, or size drift during shelf-life and storage conditions. As a result, manufacturers are abandoning traditional batch synthesis and moving toward continuous-flow microfluidic production, which offers superior reproducibility, narrower size distributions, and controllable reaction kinetics. This process-control shift is redefining quality standards in nanomedicine, drug delivery systems, diagnostics, and nanoparticle-based imaging agents.

Market Opportunity 1: Nanocellulose as a High-Barrier, High-Strength, Fully Biodegradable Packaging Reinforcement

One of the most commercially scalable opportunities in the nanomaterials landscape is the deployment of nanocellulose—both cellulose nanofibers (CNF) and cellulose nanocrystals (CNC)—as a sustainable barrier and reinforcement material. Nanocellulose films deliver exceptional oxygen barrier performance, achieving OTR < 1 cc/m²·day·atm, rivaling industry-leading polymers like EVOH, which ranges from 0.04 to 0.4 cc·mm/m²·day·atm. This positions nanocellulose as a viable alternative for food packaging, pharmaceuticals, and multilayer laminates where oxygen ingress must be minimized.

Mechanical performance is another significant driver: nanocellulose films routinely exhibit tensile strengths above 100 MPa and high Young’s Modulus values, allowing for material-lightweighting and structural reinforcement without compromising durability. With diameters <100 nm, nanocellulose fibrils pack densely, creating the tortuous diffusion pathways responsible for their superior barrier properties. Crucially, nanocellulose is fully biodegradable and derived from renewable biomass, addressing regulatory and consumer pressure to eliminate petroleum-based plastics while enabling circular, low-carbon packaging solutions.

Market Opportunity 2: Quantum Dots & Perovskite Nanocrystals Enabling Ultra-Pure, Size-Tunable Emission for Micro-LED Displays

The rapid evolution of display technology is opening a lucrative opportunity for Quantum Dots (QDs) and Perovskite Nanocrystals, which offer unmatched optical precision for micro-LED, AR/VR, and ultra-high definition display panels. QDs deliver extremely narrow emission spectra, with FWHM values of 30 nm or less, producing 30–40% wider color gamuts compared to conventional phosphors. Their high photoluminescence quantum yield (70–90% QY) ensures high brightness and low power consumption—key performance metrics for next-generation displays.

The most commercially valuable property of QDs is size-tunable color emission. Small QDs (2–3 nm) emit blue to green wavelengths, while larger QDs (5–6 nm) emit orange to red, enabling precise engineering of RGB subpixels for high-resolution micro-LED arrays. Meanwhile, perovskite nanocrystals deliver similar spectral sharpness with simpler manufacturing pathways, creating additional opportunities for flexible displays and printable photonic materials. Together, QDs and perovskites are establishing themselves as critical nanomaterials for the next wave of ultra-efficient, high-color-accuracy display technologies.

Nanomaterials Market Share Analysis

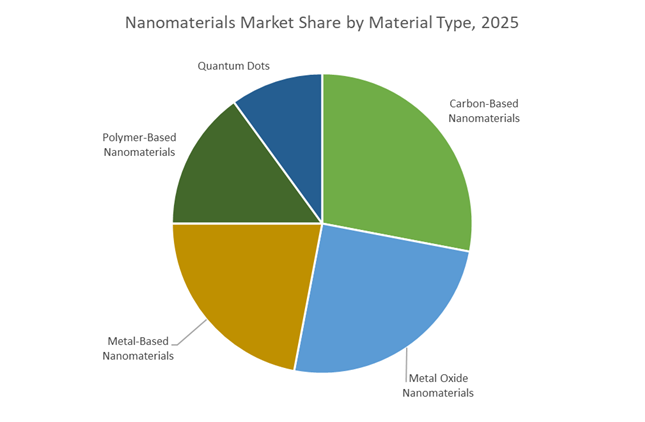

Market Share by Material Type: Carbon-Based Nanomaterials Lead Through Unmatched Conductivity and Structural Performance

Carbon-Based Nanomaterials hold the largest share of the global nanomaterials market—approximately 28%—because they deliver a unique combination of electrical, thermal, and mechanical performance that no other material class can match at the nanoscale. Carbon nanotubes (CNTs), graphene, and graphene derivatives continue to dominate high-value applications due to their exceptional intrinsic properties: CNTs exhibit tensile strengths up to 60 GPa and high aspect ratios that create effective percolation networks even at low loadings, while graphene offers one of the highest known thermal conductivities (> 3,000 W/m·K) and remarkable electron mobility. These capabilities make carbon nanomaterials essential for next-generation electronics, conductive inks, EMI shielding, battery electrodes, and composite reinforcement. Their dominance is further supported by the industrial maturity of multi-walled carbon nanotubes (MWCNTs), which enable scalable, cost-effective production for high-volume end uses such as energy storage materials and polymer composites. With the global carbon nanomaterials segment projected to exceed USD 20 billion, and CNTs alone capturing over half of that volume in some forecasts, this material class remains the technical and commercial backbone of the broader nanomaterials market.

Market Share by End-User Industry: Electronics & Semiconductors Dominate Due to High-Purity, High-Performance Requirements

The Electronics & Semiconductors industry accounts for the largest share of the global nanomaterials market—nearly 25%—because nanomaterials are indispensable to the ongoing push for miniaturization, faster performance, and improved energy efficiency in semiconductor devices. As Moore’s Law slows, nanomaterials such as CNTs, graphene, metal oxides, and quantum dots are increasingly integrated into advanced electronic architectures: from high-mobility transistor channels and ultra-thin conductive interconnects to transparent electrodes in OLED panels and high-efficiency quantum dot displays. Their role in thermal management—particularly graphene-based films used to dissipate heat in compact, high-power devices—further cements their importance in consumer electronics, data centers, 5G infrastructure, and AI computing hardware. At the manufacturing level, nanomaterials enhance deposition processes, sensor functionality, and lithographic precision, supporting the semiconductor industry's shift toward sub-5 nm design rules. Because this sector consumes high-purity, high-value nanomaterials with strict performance tolerances—significantly raising the per-unit cost—the electronics segment maintains the highest revenue contribution within the market. With accelerating demand for IoT systems, flexible displays, edge computing devices, and next-gen memory technologies, the Electronics & Semiconductors segment is positioned to retain its leadership in nanomaterials utilization over the long term.

Country Analysis: Strategic National Accelerators Transforming the Global Nanomaterials Market

United States: Multi-Billion Dollar Federal Funding and Climate-Driven Nano4EARTH Innovation

The United States continues to dominate the global Nanomaterials Market through sustained federal funding and a strategic shift toward climate and semiconductor-focused nanotechnology. The FY2025 federal budget request allocated over USD 2.2 billion to the National Nanotechnology Initiative (NNI), pushing cumulative U.S. investment since 2001 beyond USD 45 billion and reaffirming the nation’s leadership across quantum materials, nanophotonics, and advanced semiconductor nanostructures. A key focus area is the Nano4EARTH Challenge, which steers federal research toward nanomaterial-enabled climate mitigation—particularly energy nanomaterials, catalytic nanostructures, carbon capture nanomaterials, and nano-enabled water purification systems. This aligns U.S. nanotechnology policy with the broader sustainability agenda while accelerating commercialization in renewable energy and industrial decarbonization.

The United States also maintains a formidable position in nanobiotechnology, with NIH contributing over USD 900 million annually to nanomedicine, nanoparticle-based drug delivery systems, biosensing materials, and cancer-targeting nanotherapeutics. In parallel, the integration of nanomaterials into advanced semiconductors is strengthened through synchronization between NNI research and the CHIPS and Science Act, fueling breakthroughs in quantum devices, nanoscale interconnect materials, and next-generation lithography. This unified approach—spanning climate, biomedical, and semiconductor nanomaterials—cements the U.S. as the world’s most diversified nanotechnology ecosystem.

China: Global Graphene Dominance and CNT Industrialization under National Manufacturing Priorities

China remains the world’s most powerful production base for graphene, graphene oxide, and carbon nanotubes (CNTs), accounting for over 70% of global graphene output and holding the leading global position in graphene patents and industrial deployments. The country’s 14th Five-Year Plan reinforces graphene’s strategic importance across EV batteries, supercapacitors, coatings, filtering membranes, and high-strength composites. Provinces such as Jiangsu—marketed as China’s “Graphene Valley”—have become core industrial hubs for commercial-scale conductive inks, flexible transparent electrodes, graphene-enhanced polymers, and lithium-ion battery additives.

China’s nanomaterials strategy aligns with its aggressive goals for Electric Vehicle (EV) leadership, with major investments directed towards graphene-enabled fast-charging batteries, thermally conductive composites, and lightweight structural materials. This industrial expansion is further supported by policy directives emphasizing R&D, scaling of CNT production, and the integration of nanomaterials into advanced manufacturing, sensors, and national defense applications. Collectively, China’s massive production capacity, policy-backed commercialization, and rapid scaling of supply chains anchor its position at the center of the global nanomaterials market.

South Korea: Semiconductor Nanodevice Leadership and Nanomaterials for Next-Generation Displays

South Korea is emerging as a critical global hub for semiconductor nanomaterials, nanoscale device engineering, and advanced display technologies. The Ministry of Science and ICT (MSIT) set a record-high KRW 24.8 trillion R&D budget for 2025, targeting AI semiconductors, nanoscale memory technologies, and advanced lithography—all heavily dependent on high-performance nanomaterials. Additionally, the government’s KRW 26 trillion semiconductor support package includes KRW 1.7 trillion earmarked for nanomaterials R&D, particularly in chip packaging, chip-clouding technologies, nanoscale interconnects, and high-density bonding materials.

In the display segment, South Korea is accelerating its shift toward OLED, Micro-LED, and iLED platforms, all of which utilize nanomaterial-based light emitters, Quantum Dots (QDs), nanowires, and transparent conductive films. South Korea’s leadership in premium electronics and high-efficiency automotive displays further drives demand for conductive nanomaterials, nanostructured barrier layers, and flexible substrates engineered at the nanoscale. These combined advances position South Korea as a strategically important Asian nanomaterials innovation hub.

Germany & the European Union: Graphene Flagship Momentum and 2D Materials Commercialization

Germany and the European Union represent one of the world’s most coordinated ecosystems for graphene and 2D materials commercialization, anchored by the Graphene Flagship, one of the EU’s largest-ever scientific initiatives. Under the Horizon Europe program, the Graphene Flagship continues to unite 126 industrial and academic partners, advancing applications in graphene-enhanced electronics, nanophotonics, biosensors, coatings, composites, and flexible electronics. A major component is the 2D Pilot Line, offering multi-project wafer (MPW) runs that accelerate commercialization of graphene-based CMOS devices, photonic circuits, biosensing chips, and ultra-thin energy materials.

The EU’s nanomaterials landscape is also driven by its emphasis on technological sovereignty, sustainability, and circularity. The region is expanding its industrial capacity for large-area graphene films, conductive coatings, high-frequency substrates, and functional nanocomposites aimed at EVs, energy storage, aviation, and digital technologies. Germany’s strong automotive, chemical, and machine tool industries serve as major adopters of 2D materials, reinforcing the EU’s position as a global force in applied nanotechnology.

Japan: Quantum Dot Excellence and Molecular Precision in Nanodevice Fabrication

Japan continues to be a global leader in Quantum Dot (QD) synthesis, producing high-purity, cadmium-free QDs used in next-generation displays, optical communication systems, and advanced lighting. Japanese chemical companies are pioneering eco-friendly QDs with higher quantum efficiency, superior spectral stability, and long operational lifespans, reinforcing Japan’s leadership in premium consumer electronics and photonics-enabled devices.

Japan also excels in molecular nanotechnology (MNT)—the precision engineering of nanoscale devices for computing, telecommunications, and scientific instruments. Japanese R&D institutions are investing heavily in nanodevices for ultra-high-speed optical networks, high-sensitivity sensors, and miniaturized robotics components. Its world-class nanomanufacturing capabilities make Japan indispensable in high-tech nanomaterials markets such as nanophotonics, nanostructured ceramics, and precision-engineered semiconductors.

Luxembourg: Rapid Global Scaling of SWCNT Manufacturing and Strategic Battery Partnerships

Luxembourg has rapidly emerged as a significant global player in Single-Wall Carbon Nanotube (SWCNT) manufacturing, driven by major corporate investments aimed at reshaping the global CNT supply chain. In November 2025, OCSiAl announced the development of the world’s largest graphene nanotube manufacturing hub, positioning Luxembourg as a strategic alternative to Asia for CNT sourcing. This expansion is expected to dramatically scale production of SWCNTs for conductive polymers, structural nanocomposites, elastomers, and energy storage materials.

Strategic collaborations reinforce the country’s rising status: a long-term supply agreement with Molicel (May 2025) supports the integration of SWCNTs into ultra-high-power battery cells, improving energy density, cycle life, and charge-discharge rates. As global EV and consumer electronics manufacturers shift toward next-generation nanocarbon additives, Luxembourg is becoming a high-value production base within Europe’s innovation-focused materials ecosystem.

Competitive Landscape: Global Leaders Scale CNT, Graphene, Nanopowder, and Nanoparticle Manufacturing for High-Growth Applications

The competitive environment of the Nanomaterials Market is shaped by global leaders expanding production capacity, advancing nanomaterial purity and uniformity, and integrating application-specific solutions for electronics, composites, energy storage, coatings, biopharmaceuticals, and digital health technologies. Companies that control both upstream nanomaterial production and downstream formulation technologies are gaining a strategic edge as application markets scale exponentially.

Arkema Group – Arkema accelerates CNT-based composite innovation through sustainability-driven specialty materials leadership

Arkema leverages its Graphistrength® CNT platform, electroactive fluoropolymers (Piezotech®), and nanostructured resins (Kynar®) to deliver advanced materials for EVs, aerospace composites, flexible electronics, and specialty coatings. With more than 90% of its 2024 R&D patents dedicated to sustainability, Arkema is strategically positioning itself as a global champion of green materials and circular-economy innovation. Its CNT technologies strengthen lightweight composite structures, enhance electrical conductivity, and support high-performance energy systems—making Arkema a pivotal supplier to high-growth segments such as EV batteries, hydrogen systems, and next-generation electronics.

OCSiAl Group – OCSiAl leads global SWCNT production with scalable TUBALL™ nanotube technologies

OCSiAl remains the world’s largest producer of Single-Walled Carbon Nanotubes, with an aggressive expansion strategy aimed at achieving 500-ton/year production capacity. Its TUBALL™ nanotubes enhance electrical and mechanical properties at ultra-low loading levels starting at 0.01 wt.%, enabling conductive networks in polymers, rubbers, batteries, and coatings without compromising viscosity or color. The company’s European manufacturing expansion ensures a reliable supply chain for industrial-scale CNT integration, reinforcing its dominance in conductive additives for EVs, tires, energy storage devices, and industrial composites.

Nanostructured & Amorphous Materials, Inc. (NanoAmor) – NanoAmor supports global R&D through extensive nanomaterial and nanoparticle catalog offerings

NanoAmor is recognized for maintaining one of the broadest catalogs of nanomaterials—including SWCNTs, MWCNTs, graphene, nanoscale metals, metal oxides, carbides, and amorphous materials. Its portfolio caters heavily to academic research labs, early-stage industrial R&D programs, and pilot-scale nanotechnology innovators. Beyond pure nanomaterials, the company specializes in amorphous and nanocrystalline magnetic materials, positioning it as a versatile supplier supporting applications from energy storage to electromagnetic shielding, catalysis, and advanced composite structures.

BASF SE – BASF scales nanoparticulate TiO₂ and ZnO solutions for coatings, catalysis, and UV-protection markets

BASF leverages its extensive chemical manufacturing infrastructure to produce high-volume nanoparticulate TiO₂ and ZnO, widely used in coatings, sunscreens, cosmetics, and catalysts. Its functional nanocoatings enhance UV absorption, durability, antimicrobial performance, and surface hardening, reinforcing BASF’s influence in architectural coatings, industrial protection systems, and personal care formulations. Strategic integration across chemicals, dispersions, and additives allows BASF to meet global demand at scale while innovating in eco-friendly, high-performance nanomaterials.

ACS Material, LLC – ACS Material advances graphene, quantum dots, and nanofiber technologies for next-generation electronics

ACS Material plays a critical role in supplying research-grade and pilot-scale quantities of graphene nanoplates, quantum dots, nanoparticles, and nanofibers. Its leadership in cadmium-free quantum dots aligns with regulatory pressures and the rapid expansion of next-generation displays, photonics systems, and lighting technologies. With the global quantum dot ecosystem supported by more than USD 4 billion in historical R&D, ACS Material is positioned at the center of semiconductor, optoelectronic, and flexible electronics innovation. Its consistent quality, broad catalog, and strong focus on emerging applications make it a preferred supplier to research institutions and high-tech innovators worldwide.

Nanomaterials Market Report Scope

Nanomaterials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$13.3 Billion

|

|

Market Size (2035)

|

$59.2 Billion

|

|

Market Growth Rate

|

16.1%

|

|

Segments

|

By Material Type (Carbon-Based, Metal-Based, Metal Oxide, Polymer-Based Nanomaterials, Quantum Dots), By Dimensionality (0D, 1D, 2D, 3D Nanomaterials), By End-User (Electronics & Semiconductors, Energy Storage & Generation, Medical & Life Sciences, Aerospace & Defense, Automotive, Paints & Coatings)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, Cabot Corporation, Dow, Arkema, OCSiAl, Nanophase Technologies, LG Chem, Showa Denko (Resonac), American Elements, DuPont, Quantum Materials, CHASM Advanced Materials, Nanocyl, Advanced Nano Products, Evonik Industries

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Nanomaterials Market Segmentation

By Material Type

- Carbon-Based Nanomaterials

- Metal-Based Nanomaterials

- Metal Oxide Nanomaterials

- Polymer-Based Nanomaterials

- Quantum Dots

By Dimensionality

- 0D Nanomaterials

- 1D Nanomaterials

- 2D Nanomaterials

- 3D Nanomaterials

By End-User

- Electronics & Semiconductors

- Energy Storage & Generation

- Medical & Life Sciences

- Aerospace & Defense

- Automotive

- Paints & Coatings

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Nanomaterials Market

- BASF

- Cabot Corporation

- Dow

- Arkema

- OCSiAl

- Nanophase Technologies

- LG Chem

- Showa Denko (Resonac)

- American Elements

- DuPont

- Quantum Materials

- CHASM Advanced Materials

- Nanocyl

- Advanced Nano Products (ANP)

- Evonik Industries

*- List not Exhaustive

Research Coverage

The latest Nanomaterials Market study by USDAnalytics offers a comprehensive, decision-grade assessment of how carbon nanotubes, graphene, metal and metal-oxide nanoparticles, nanocellulose, quantum dots and other engineered nanostructures are reshaping high-performance applications across electronics, energy storage, medical & life sciences, transportation and aerospace. This report investigates the interplay between ultra-high tensile strength, exceptional thermal conductivity, quantum-scale electronic behavior and evolving regulatory expectations, and connects these breakthroughs to commercial adoption curves, capex cycles and technology roadmaps through 2034. It delivers analysis reviews on manufacturing scale-up (from lab to multi-ton SWCNT and graphene plants), evolving quality and characterization standards, and the impact of multi-billion-dollar public R&D programs such as the U.S. National Nanotechnology Initiative on global competitive positioning. The study highlights how nanomaterials are enabling fast-charging batteries, high-density semiconductor interconnects, advanced barrier coatings, biodegradable packaging and precision nanomedicine platforms, while also examining risk factors such as toxicology data gaps, EHS compliance and supply concentration in key regions. By integrating quantitative market modeling with detailed value-chain mapping, patent and funding analysis, technology benchmarking and end-user adoption case studies, this report is an essential resource for OEM strategists, material scientists, procurement leaders, investors and nanotechnology vendors seeking to align product portfolios, partnerships and capital allocation with the next decade of nanomaterials market expansion.

Scope Highlights

- Segmentation By Material Type: Carbon-Based Nanomaterials, Metal-Based Nanomaterials, Metal Oxide Nanomaterials, Polymer-Based Nanomaterials, Quantum Dots

- Segmentation By Dimensionality: 0D Nanomaterials, 1D Nanomaterials, 2D Nanomaterials, 3D Nanomaterials

- Segmentation By End-User: Electronics & Semiconductors, Energy Storage & Generation, Medical & Life Sciences, Aerospace & Defense, Automotive, Paints & Coatings

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data from 2021 to 2025 and forecast data from 2026 to 2034.

- Companies: Analysis / profiles of 15+ companies.