Carbon Nanomaterials Market Overview: High-Growth Nano-Additives Powering Batteries and Advanced Composites

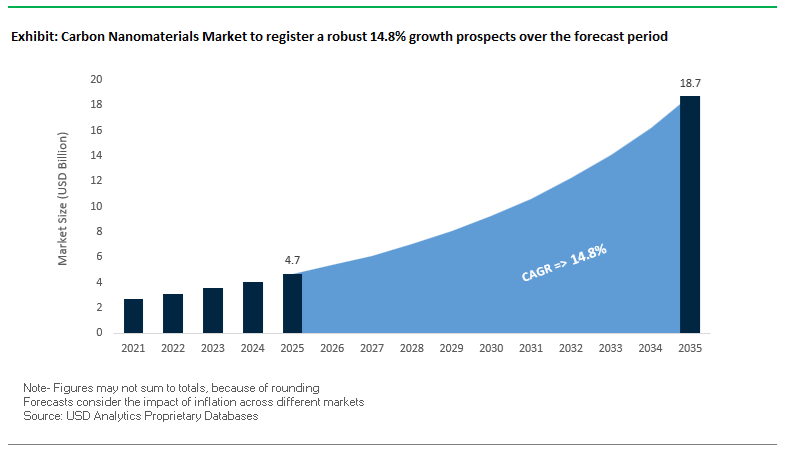

The global Carbon Nanomaterials Market is projected to grow from USD 4.7 billion in 2025 to around USD 18.7 billion by 2035, reflecting a robust CAGR of 14.8% (2025–2035). This rapid expansion is underpinned by rising adoption of carbon nanotubes (CNTs), graphene nanoplatelets (GNPs), vapor-grown carbon fibers (VGCF), and carbon quantum dots (CQDs) in lithium-ion batteries, structural composites, automotive plastics, and high-performance electronics. For manufacturers and materials vendors, the market is shifting from lab-scale innovation to multi-kiloton industrial capacity, with cost curves dropping and performance benchmarks clearly established for batteries, polymers, and coatings.

Ultra-high-performance multi-walled carbon nanotubes (MWCNTs) can deliver bulk conductivities around 10,000 S/m in polymer composites at only ~10 wt% loading, significantly outperforming traditional carbon black and enabling lighter, thinner, and more conductive parts. CNTs also bring exceptional mechanical reinforcement, with intrinsic tensile strengths near 100 GPa and elastic moduli around 1 TPa, positioning them as a premium nano-filler for aerospace, automotive, and industrial composites. In lithium-ion batteries, CNT conductive additives can cut the volume of conductive additives by ~30% while still achieving around 10% higher conductivity than carbon black, directly translating into higher active material loading and better energy density. Even at very low dosages (~0.02 wt%), graphene nanoplatelets can meaningfully improve compressive and flexural performance in polymer nanocomposites. Meanwhile, the price of single-walled CNTs (SWCNTs) has collapsed from USD 150,000–500,000/kg in 2014 to roughly USD 2,000/kg in the mid-2020s, unlocking mainstream industrial adoption.

Key market insights for manufacturers and vendors

- Strong conductivity at low loading: MWCNTs in polymer composites achieve ~10,000 S/m at ~10 wt%, enabling lighter and more efficient conductive plastics.

- Structural reinforcement opportunity: CNT tensile strength (~100 GPa) and 1 TPa modulus support premium positioning in structural composites and high-performance parts.

- Battery value proposition: CNTs can reduce conductive additive volume by ~30% while delivering ~10% higher cathode conductivity versus carbon black.

- Graphene for mechanical tuning: Trace levels (~0.02 wt%) of graphene nanoplatelets can significantly upgrade compressive and flexural properties of polymer matrices.

- Cost curve enables scale: SWCNT price reductions from >USD 150,000/kg to ~USD 2,000/kg in the mid-2020s are accelerating adoption across EV batteries, coatings, and plastics.

Carbon Nanomaterials Market Analysis: Capacity Scale-Up, EV Batteries, and New Use Cases

The carbon nanomaterials market is entering an industrial-scale phase, anchored by aggressive capacity expansions dedicated to EV batteries and conductive additives. In June 2023, LG Chem announced construction of its fourth CNT plant in Daesan, South Korea, with operations scheduled for 2025. Once online, this facility will double LG Chem’s CNT production capacity to about 6,100 tons per year, directly targeting cathode and anode formulations for lithium-ion batteries. In parallel, Cabot Corporation unveiled, in January 2023, a roughly USD 200 million, five-year investment program to expand conductive carbon additive (CCA) capacity in the United States, including a first-phase addition of 15,000 metric tons per year in Pampa, Texas expected to be operational by the end of 2025. Earlier, in December 2022, Showa Denko (now Resonac) decided to increase VGCF™ (vapor-grown carbon fiber) capacity by 33%, reaching 400 tons per year at its Kawasaki plant, with expanded operations beginning in October 2023 and focused on the fast-growing xEV lithium-ion battery market.

At the higher end of the performance spectrum, OCSiAl is reshaping the single-walled CNT (graphene nanotube) segment. In November 2025, the company announced a USD 300 million investment in a flagship graphene nanotube manufacturing hub in Differdange, Luxembourg, which is slated to become the world’s largest graphene nanotube facility with start-up envisaged around 2028–2030. Also in November 2025, OCSiAl confirmed a fourfold expansion of its existing graphene nanotube plant in Serbia, providing near-term supply security while the Luxembourg hub is built. The commercial traction is already tangible: as of November 2025 reports, OCSiAl’s TUBALL™ graphene nanotubes are used in more than one million electric vehicles worldwide, demonstrating rapid mainstream adoption in EV batteries, coatings, and elastomer components.

Beyond batteries, carbon nanomaterials are penetrating automotive plastics, optoelectronics, and specialty coatings. In late 2024 and early 2025, Dotz Nano Ltd., focused on carbon quantum dots (CQDs), secured an AUD 4 million investment from Triton Funds, highlighting rising venture interest in fluorescent carbon nanomaterials for biosensing, authentication, and display technologies. Meanwhile, LG Chem has, throughout 2024 and 2025, begun supplying CNT-enhanced, metal-replacing electrostatic coating plastics to Mitsubishi Motors in Japan, with applications such as front fenders showcasing how CNTs can deliver both electrical functionality (ESD/anti-static) and weight reduction. Collectively, these developments indicate that the carbon nanomaterials market is moving from niche additives to foundational materials in EVs, advanced plastics, and functional coatings, underpinned by large-scale investments and visible commercial deployments.

Quantum-Scale Electrical Transport and Multifunctional Nanocarbon Architectures Creating Transformative Commercial Pathways

Market Trend 1: Commercial Qualification of SWCNTs as Quantum-Efficient Channel Materials for Post-Silicon Logic Transistors

A defining trend in the Carbon Nanomaterials Market is the fast-accelerating qualification of single-walled carbon nanotubes (SWCNTs) for advanced logic transistor technology as traditional silicon scaling hits physical and electrostatic limits. Experimental SWCNT FETs with sub-10 nm gate lengths have shown >4× higher diameter-normalized current density compared to cutting-edge silicon MOSFETs—achieving 2.41 mA/µm at just 0.5 V. This superior current delivery arises from CNTs’ near-ballistic quantum transport, enabling unprecedented drive currents at ultra-low power.

SWCNTs also demonstrate a steeper subthreshold slope (SS ≈ 70 mV/decade) at 10 nm channel lengths—superior to silicon’s typical ≥80 mV/dec limits—directly improving switching efficiency and reducing leakage. Advanced Gate-All-Around (GAA) CNT FET simulations further indicate that SWCNTs can meet or exceed ITRS 2028 performance targets at the 2 nm logic node, positioning CNTs as one of the few viable successors for deep-nanoscale transistor scaling.

However, commercial adoption requires extremely tight electronic uniformity. Semiconductor-grade CNT arrays must reach ≥99.9999% semiconducting purity (“six nines”), ensuring consistent threshold voltage, mobility, and on/off behavior across large-area arrays. This purity threshold remains a technical bottleneck but is rapidly being addressed by sorting chemistries and roll-to-roll purification systems. As global foundries explore post-CMOS materials for AI processors, neuromorphic chips, and ultra-low-power IoT logic, SWCNT transistor development is becoming a top strategic investment area in the carbon nanomaterials market.

Market Trend 2: Integration of Graphene Oxide and rGO as Multifunctional High-Barrier and Thermal-Stable Additives in Industrial Coatings

A second dominant trend involves growing industrial integration of graphene oxide (GO) and reduced graphene oxide (rGO) as multifunctional additives for corrosion protection, mechanical reinforcement, and thermal stabilization in coatings and polymer composites. At extremely low concentrations—0.25–0.5 wt%—GO dramatically increases coating barrier resistance, elevating the low-frequency impedance modulus by three orders of magnitude after prolonged saline exposure relative to pristine epoxy systems.

This performance boost stems from GO’s platelet geometry, which enhances path tortuosity by 3–5×, forcing water molecules and ions to navigate much longer diffusion pathways before reaching the metal substrate. This results in anti-corrosion efficiencies of 99.64% and polarization resistance values of Rcorr ≈ 21.498 mΩ, placing GO-epoxy systems among the highest-performing corrosion-prevention coatings available. GO and rGO also increase composite thermal stability, raising the TGA 5% weight-loss temperature by 10–20°C, signaling improved thermal endurance and molecular stability. These multi-property enhancements are reinforcing GO’s commercial relevance in marine coatings, automotive primers, aerospace composites, and high-barrier industrial films.

Market Opportunity 1: Carbon Nanohorn (CNH)-Based Ultra-Microporous Adsorbents for Scalable Direct Air Capture (DAC)

Carbon nanohorns (CNHs) represent a major untapped commercial opportunity in Direct Air Capture (DAC) due to their tunable pore structure, high surface area, and favorable regeneration properties. Comparable activated carbons already demonstrate BET surface areas of 1,000–4,320 m²/g, showcasing the adsorption potential achievable with nanocarbon frameworks. Under DAC-relevant low-pressure conditions (1 bar, 25°C, 400 ppm CO₂), microporous carbon adsorbents achieve 0.75–3.15 mmol/g CO₂ uptake, with performance dominated by ultra-micropores (<0.7 nm) that maximize confinement effects for CO₂ molecules.

The key advantage lies in the low adsorption energy (20–40 kJ/mol) characteristic of physisorption-based carbon systems. This enables highly reversible CO₂ capture with minimal energy input, addressing one of the largest cost barriers in DAC technology. CNHs can be engineered to possess high densities of ultrasmall pores through controlled oxidation and activation, making them promising candidates for next-generation sorbents compatible with modular DAC reactors, urban carbon-neutral infrastructure, and industrial flue-gas hybrid systems.

Market Opportunity 2: Standardization of Carbon Nanofiber (CNF) Grades for High-Performance Thermal Interface Materials (TIMs)

A second transformative opportunity is the development of carbon nanofiber (CNF)-reinforced thermal interface materials (TIMs) for next-generation power electronics, EV inverters, SiC MOSFET modules, and data-center thermal management. Vapor-grown carbon fibers (VGCF), when incorporated into polymer matrices, deliver dramatic thermal conductivity enhancements—up to 17× higher (from 0.20 W/m·K to 3.46 W/m·K) at 50 wt% loading with proper fiber alignment.

This stems from the extraordinary intrinsic axial thermal conductivity of CNFs (600–3,000 W/m·K) and their high aspect ratios (≥25), which enable the formation of continuous, percolating thermal networks. The thermal percolation threshold for CNFs is often achieved at <10 vol%, making them significantly more effective than spherical metal or ceramic fillers. Alignment techniques such as tape casting, extrusion, and electromagnetic-field processing further amplify anisotropic thermal transport, enabling high through-plane heat extraction required for compact, high-power-density electronic modules.

As WBG (Wide Bandgap) semiconductor adoption accelerates globally, standardized CNF grades optimized for TIMs represent a critical supply chain opportunity for ensuring reliable device cooling, extending device lifetime, and supporting the electrification and digital-infrastructure transition.

Carbon Nanomaterials Market Share Analysis

Market Share by Type: Carbon Nanotubes Lead Due to Scalability, Cost Efficiency, and Superior Multi-Functional Properties

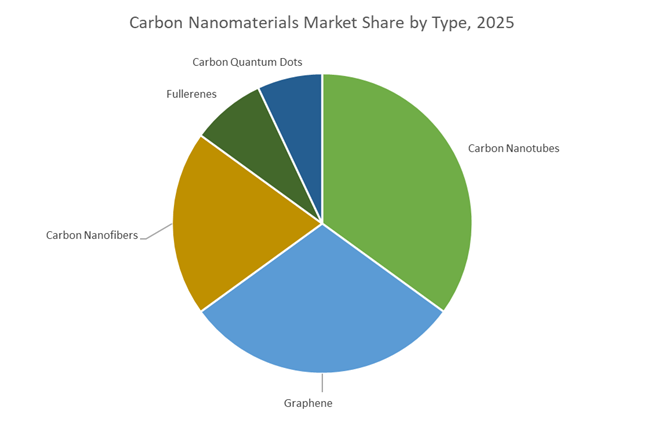

Carbon Nanotubes (CNTs) capture the largest share of the carbon nanomaterials market—approximately 35% in 2025—because they provide the most commercially scalable, cost-efficient, and performance-enhancing solution across high-volume industrial applications. Multi-Walled Carbon Nanotubes (MWCNTs), produced at large scale through chemical vapor deposition and other mature synthesis routes, dominate consumption due to their low cost relative to graphene and single-walled CNTs, while still offering exceptional electrical conductivity, mechanical reinforcement capability, and thermal stability. Their high aspect ratio enables CNTs to form percolating conductive networks at extremely low loadings, making them highly attractive as additives in polymers, elastomers, coatings, adhesives, and especially energy storage materials. CNTs also deliver tensile strengths up to 60 GPa and electrical conductivities near 10⁶ S/m (in high-quality SWCNTs), making them ideal for next-generation composite materials, antistatic compounds, and advanced electrode formulations. Their industrial maturity and versatility—spanning automotive, electronics, aerospace, and renewable energy applications—ensure CNTs remain the dominant material type within the broader carbon nanomaterials ecosystem, both in terms of volume and value.

Market Share by End-Use: Energy Storage & Conversion Dominates as CNTs Become Indispensable for Advanced Battery Technologies

The Energy Storage & Conversion sector accounts for roughly 40% of the global carbon nanomaterials market, driven by the accelerating transition to electric mobility and the rapid scaling of lithium-ion battery (LiB) manufacturing capacity. CNTs have emerged as a critical material for next-generation LiB electrodes, replacing carbon black and other conventional conductive additives due to their ability to create robust, highly conductive networks that improve charge transport, increase power density, and enable faster charging. Their mechanical flexibility and structural resilience also make CNTs essential for silicon-based anodes, where they mitigate extreme volume expansion during cycling—preserving cycle life and enhancing safety. For high-nickel cathode chemistries, CNTs reinforce particle frameworks and maintain conductivity across thousands of cycles. As global EV adoption surges, battery manufacturers are expanding CNT production partnerships and vertically integrated supply chains to secure material availability. Beyond EV batteries, CNTs are increasingly used in supercapacitors, fuel cell electrodes, and next-generation solid-state battery designs, further strengthening the energy storage segment’s commanding market share and long-term growth trajectory.

Country Analysis: Global Drivers in Carbon Nanomaterials Development

China: Scaling SWCNT and Graphene Production to Power the World’s Largest EV and Battery Ecosystem

China remains the global epicenter of Carbon Nanomaterials production, supported by unmatched manufacturing scale, rapidly expanding EV battery demand, and state-backed industrialization programs that elevate national competitiveness. A defining development in 2025 was Tiannai Technology’s successful supply of Single-Walled Carbon Nanotubes (SWCNTs) to major solid-state battery manufacturers, marking a turning point in the incorporation of CNTs into high-energy-density battery architectures. These SWCNTs enhance ionic conductivity, mechanical strength, and stability—attributes essential for enabling next-generation electrolyte designs. Meanwhile, The Sixth Element (Changzhou) Materials Technology continues expanding its graphene and graphene oxide lines, including CVD-grown graphene films for flexible electronics and conductive coatings, reinforcing China’s position as the world’s highest-volume graphene producer.

Government policy plays a pivotal role, with provincial initiatives and R&D funding mechanisms accelerating the commercialization of carbon nanofibers, CNT powders, and bulk graphene for structural composites and conductive polymers. This aligns with China’s push to vertically integrate its EV supply chain—from lithium processing to electrode formulation—where CNT additives increasingly serve as essential conductive agents in Li-ion cathodes. By 2025, Chinese battery manufacturers are intensifying CNT procurement to improve rate capability and cycle life, maintaining global cost competitiveness. Together, China’s dominance in EV batteries, large-scale graphene production, and government-led industrialization cements its leadership in the global Carbon Nanomaterials Market.

United States: High-Purity CNT Innovation, Sustainable Nanomaterial Production, and Defense-Grade Applications

The U.S. Carbon Nanomaterials ecosystem is defined by high-purity manufacturing, advanced nanomaterial engineering, and strategic deployment in defense, aerospace, and next-generation electronics. CHASM Advanced Materials significantly expanded its CNT production platform, supplying NTeC-E conductive CNT additives to meet Li-ion battery demand projected to exceed 50,000 tons annually by 2025. These high-performance additives enhance conductivity and durability in battery electrodes, supporting surging U.S. EV and energy storage growth. The nation is also emerging as a leader in sustainable nanomaterial synthesis—highlighted by Huntsman Corporation’s MIRALON™ CNT facility, which produces premium CNTs while simultaneously generating clean hydrogen through a proprietary pyrolysis route.

On the electronics front, NanoIntegris continues scaling production of its high-purity semiconducting CNT inks (e.g., IsoSol-S100), enabling thin-film transistors, flexible displays, and other next-generation semiconductor applications. The aerospace and defense sectors also reinforce U.S. competitiveness: CVD Equipment Corporation secured a $3.5 million order (Nov 2024) for a CVI production system used to manufacture Carbon Nanomaterial-enhanced composites for turbine engines and high-temperature aerospace components. This integration of advanced CNT processing, sustainability-focused nanomaterial production, and defense-grade adoption positions the U.S. as a global leader in high-value, specialty Carbon Nanomaterials.

Europe (Belgium, Serbia, United Kingdom): Nanotube Gigafactory Expansion and Graphene Electronics Commercialization

Europe’s Carbon Nanomaterials market is rapidly expanding through gigafactory-scale nanotube production, graphene electronics innovation, and strong public and private sector funding supporting high-tech applications. A landmark achievement came in October 2024 with OCSiAl’s launch of a 60-ton graphene nanotube facility in Serbia, the first production site of its kind in the region. This capacity is estimated to enable advanced nanomaterial integration into components for over 1 million Electric Vehicles, significantly strengthening Europe’s local supply of high-performance CNTs for battery, polymer, and composite applications. In parallel, the UK/EU consortium CamGraPhIC secured €25 million in 2025 to commercialize graphene-based integrated circuits for optical communications—marking a major step toward wafer-scale graphene electronics and photonics adoption.

Europe also excels in nanomaterial-enhanced composites for transport and defense. Nanocyl SA (Belgium) continues to scale Multi-Walled CNT masterbatches for automotive plastics, delivering improved mechanical properties and ESD performance critical for modern mobility platforms. Additionally, Black Swan Graphene’s partnership with Graphene Composites (2025) applies graphene nanoplatelets to develop the GC Shield ballistic protection technology, highlighting strong defense-sector pull for graphene-reinforced materials. Together, Europe’s nanotube gigafactories, graphene semiconductor programs, and high-performance composite deployments support its emergence as a pivotal region for advanced Carbon Nanomaterials manufacturing and commercialization.

Japan: Ultra-Pure CNTs and Graphene for Battery Safety, Fuel Cells, and High-Reliability Electronics

Japan continues to solidify its reputation for ultra-high-purity Carbon Nanomaterials tailored for demanding applications in consumer electronics, fuel cells, and automotive power systems. Leading producers such as Toray Industries and Showa Denko leverage decades of expertise in carbon fiber, chemical engineering, and precision materials to deliver exceptionally consistent CNT and graphene products. These materials are integral to Japan's advanced battery sector, where improving safety, conductivity, and thermal stability remains paramount—particularly for EV batteries operating in compact, high-energy-density configurations.

Japan is also advancing nanomaterial-enabled clean energy technologies. Carbon Nanomaterials are increasingly used as support structures for platinum catalysts in PEM fuel cells, enabling superior durability, improved catalyst utilization, and higher fuel cell performance—an essential requirement for Japan’s hydrogen mobility roadmap. This focus on stable, high-purity materials strengthens Japan’s leadership in next-generation battery safety, hydrogen fuel cells, and high-reliability electronic components. Through precise material engineering and deep supply chain integration, Japan maintains a strong competitive position in the global Carbon Nanomaterials Market.

Competitive Landscape in the Carbon Nanomaterials Market: Battery-Grade CNTs and Graphene Nanotubes Lead

The global carbon nanomaterials industry is dominated by a mix of large chemical producers and focused nanotechnology specialists that are scaling capacity to meet EV, energy storage, and advanced materials demand. Key players such as LG Chem, OCSiAl, Cabot Corporation, Showa Denko (Resonac), and Nanocyl are building vertically integrated CNT and graphene nanotube platforms, offering powders, masterbatches, and conductive carbon systems optimized for lithium-ion batteries, conductive polymers, and ESD-safe components. Strategic investments in new plants, proprietary reactor technologies, and high-dosage concentrates are central to securing long-term supply, lowering unit costs, and solving the dispersion and integration challenges that have historically slowed adoption.

LG Chem strengthens CNT leadership in EV battery applications

LG Chem is a leading force in the carbon nanomaterials market, with a strong, vertically integrated focus on multi-walled CNTs for EV battery applications. The company is a major producer of MWCNTs used as conductive additives in lithium-ion battery cathodes, enabling higher energy density and better rate performance. With the construction of its fourth CNT plant in Daesan, announced in June 2023 and scheduled to be operational in 2025, LG Chem is targeting a total CNT capacity of about 6,100 tons per year, placing it among the highest-volume producers globally. Its proprietary fluidized bed reactor technology allows each production line to reach up to 600 tons per year, one of the largest single-line capacities in the industry. Strategically, LG Chem is extending its CNT portfolio beyond conventional LIBs into next-generation lithium–sulfur and solid-state batteries, while also supplying CNT-filled plastics for automotive exterior parts such as metal-replacing electrostatic coating plastics for Mitsubishi Motors’ front fenders.

OCSiAl dominates the SWCNT (graphene nanotube) niche

OCSiAl, headquartered in Luxembourg, is a highly specialized single-walled CNT (SWCNT) producer that brands its products as graphene nanotubes. Its flagship offering, TUBALL™ graphene nanotubes, and TUBALL™ MATRIX high-dosage concentrates are engineered to deliver high purity, excellent dispersibility, and straightforward integration into elastomers, plastics, and energy storage systems. OCSiAl claims to hold over 90% of global SWCNT production capacity, giving it a unique degree of influence over this ultra-high-performance segment of the carbon nanomaterials market. In November 2025, the company announced a USD 300 million investment in a new graphene nanotube hub in Differdange, Luxembourg, while simultaneously committing to a fourfold expansion of its Serbia plant, ensuring both short-term and long-term supply growth. Performance-wise, adding TUBALL™ MATRIX to elastomers has been shown to improve tear strength by up to 90% and tensile strength by up to 36%, alongside significant gains in conductivity—capabilities that underpin its adoption in over one million EVs globally.

Cabot Corporation expands conductive carbon additive capacity

Cabot Corporation leverages its historic expertise in conductive carbon black to build a broader portfolio of conductive carbon additives (CCAs) and carbon nanostructures for the battery and conductive plastics markets. Its product line spans Vulcan® conductive carbon blacks, engineered carbon nanostructures (CNS), and CNTs, giving cell makers multiple options for tuning resistivity and rheology. In January 2023, Cabot announced a ~USD 200 million investment over five years to expand CCA capacity in the United States, including an initial 15,000 metric tons per year in Pampa, Texas, targeted for operation by the end of 2025. This capacity is tightly aligned with the anticipated 20–30% global growth in EV battery-related CCA demand, particularly for high-nickel and high-capacity chemistries. Building on its legacy, Cabot continues to engineer conductive carbons with specific nitrogen surface areas and particle sizes to meet precise conductivity, dispersion, and mechanical property requirements across polymers and electrode slurries.

Showa Denko (Resonac) scales VGCF for xEV lithium-ion batteries

Showa Denko, now operating as Resonac, is a key Japanese producer of vapor-grown carbon fiber (VGCF™), an important carbon nanomaterial used primarily in lithium-ion battery electrodes. VGCF’s fibriform structure delivers excellent electrical and thermal conductivity, making it ideal for enhancing both performance and safety in xEV battery packs. In December 2022, Resonac decided to increase VGCF™ production capacity by 33% to 400 tons per year at its Kawasaki plant, with the expanded output becoming operational in October 2023. This expansion directly targets the rapidly growing xEV lithium-ion battery market, where VGCF is used in both cathodes and anodes to maintain lithium-ion movability, slow performance degradation, and extend cycle life. Its high thermal conductivity also supports improved battery thermal management, accelerating heat dissipation from electrodes—an increasingly critical attribute for fast charging and high-power EV platforms.

Nanocyl specializes in industrial-scale MWCNTs and masterbatches

Nanocyl SA, based in Belgium, focuses exclusively on the industrial development and production of multi-walled carbon nanotubes, positioning itself as a European leader in the carbon nanomaterials market. Its core product family, NC7000™ MWCNTs, is characterized by a high aspect ratio (length/diameter >100), which is essential for achieving low percolation thresholds in conductive polymer systems. Beyond raw CNTs, Nanocyl provides a broad range of pre-dispersed masterbatches and formulations, such as PLASTICYL™ CNT masterbatches and conductive paints and coatings, designed to simplify dispersion and integration for automotive and electronics customers. Strategically, the company focuses on meeting rigorous automotive and industrial standards, supplying CNT solutions that deliver electrostatic discharge (ESD) protection for fuel system components and electronic housings. Its materials are widely deployed in anti-static and ESD composites, helping designers reach surface resistivities below 10⁹ ohms/sq in sensitive environments such as cleanrooms, fuel handling, and electronics assembly.

Carbon Nanomaterials Market Report Scope

Carbon Nanomaterials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.7 Billion

|

|

Market Size (2035)

|

$18.7 Billion

|

|

Market Growth Rate

|

14.8%

|

|

Segments

|

By Type (Carbon Nanotubes, Graphene, Carbon Nanofibers, Fullerenes, Carbon Quantum Dots), By Synthesis Method (Chemical Vapor Deposition, Arc Discharge, Laser Ablation, HiPco Process, Mechanical/Liquid-Phase Exfoliation), By Form (Powder, Dispersions & Suspensions, Sheets & Films), By End-Use Application (Energy Storage & Conversion, Electronics & Semiconductors, Structural Composites, Biomedical & Healthcare, Environmental Technologies)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

LG Chem, Cabot Corporation, OCSiAl, Arkema, Jiangsu Cnano, Showa Denko, Toray Industries, Huntsman, Nanocyl, NanoXplore, Black Swan Graphene, The Sixth Element, Hanwha Corporation, Global Graphene Group, CHASM Advanced Materials

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Carbon Nanomaterials Market Segmentation

By Type

- Carbon Nanotubes

- Graphene

- Carbon Nanofibers

- Fullerenes

- Carbon Quantum Dots

By Synthesis Method

- Chemical Vapor Deposition (CVD)

- Arc Discharge

- Laser Ablation

- HiPco Process

- Mechanical / Liquid-Phase Exfoliation

By Form

- Powder

- Dispersions & Suspensions

- Sheets & Films

By End-Use Industry

- Energy Storage & Conversion

- Electronics & Semiconductors

- Structural Composites

- Biomedical & Healthcare

- Environmental Technologies

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Carbon Nanomaterials Market

- LG Chem

- Cabot Corporation

- OCSiAl

- Arkema

- Jiangsu Cnano

- Showa Denko

- Toray Industries

- Huntsman

- Nanocyl

- NanoXplore

- Black Swan Graphene

- The Sixth Element

- Hanwha Corporation

- Global Graphene Group

- CHASM Advanced Materials.

*- List not Exhaustive

Research Coverage: Carbon Nanomaterials Market

The latest Carbon Nanomaterials Market study from USDAnalytics delivers an end-to-end strategic assessment of how carbon nanotubes, graphene, carbon nanofibers, fullerenes, and carbon quantum dots are reshaping next-generation batteries, structural composites, and electronic materials. Drawing on quantitative datasets and deep-dive case work, this report investigates how falling SWCNT price curves, EV battery gigafactory investments, and graphene-enabled functional coatings are redefining performance and cost baselines across energy storage and advanced materials value chains. The study tracks technology breakthroughs such as six-nines semiconducting SWCNT purity for post-silicon logic, high-barrier graphene oxide coatings, and CNF-reinforced thermal interface materials, while our comparative analysis reviews competitive positioning in CNT, graphene, and VGCF capacity build-outs. It highlights how carbon nanomaterial producers are moving from lab-scale R&D to multi-kiloton production, how OEMs are integrating CNT and graphene into lithium-ion and solid-state batteries, and how nano-additive formulation choices impact conductivity, mechanical reinforcement, and thermal management in real-world use cases. By combining technology roadmaps, end-use demand modeling, pricing trajectories, and regulatory considerations into one integrated narrative, this report is an essential resource for battery manufacturers, chemical companies, composite processors, electronics OEMs, and investors seeking to benchmark strategies, de-risk capex decisions, and capture high-growth opportunities in the global Carbon Nanomaterials Market.

Scope Highlights

- Segmentation

- By Type: Carbon Nanotubes, Graphene, Carbon Nanofibers, Fullerenes, Carbon Quantum Dots

- By Synthesis Method: Chemical Vapor Deposition (CVD), Arc Discharge, Laser Ablation, HiPco Process, Mechanical / Liquid-Phase Exfoliation

- By Form: Powder, Dispersions & Suspensions, Sheets & Films

- By End-Use Industry: Energy Storage & Conversion, Electronics & Semiconductors, Structural Composites, Biomedical & Healthcare, Environmental Technologies

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Horizon: Historic data from 2021 to 2025 and detailed forecast outlook from 2026 to 2034.

- Companies Covered: Analysis / profiles of 15+ companies active in carbon nanomaterials, including CNT, graphene, CNF, and CQD producers, integrators, and solution providers.