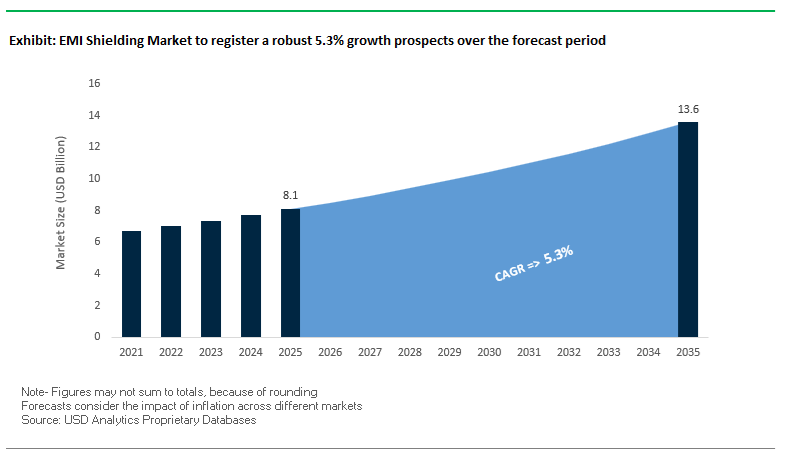

The global EMI Shielding Market is projected to grow from USD 8.1 billion in 2025 to USD 13.6 billion by 2035, registering a CAGR of 5.3% (2025–2035). The growth trajectory reflects surging design complexity in 5G/mmWave infrastructure, rapid proliferation of autonomous and connected vehicles, stringent defense and aerospace HEMP compliance, and the miniaturization of consumer, medical and industrial electronics.

Recent developments in the global EMI shielding industry underscore a clear shift toward lightweight materials, integrated thermal–EMI solutions and application-specific innovations across automotive, aerospace, defense and medical electronics. In February 2026, James Cropper Advanced Materials launched EMITEC, a new lightweight EMI shielding solution that is up to 19x lighter than conventional metal shields, directly addressing aerospace and portable device requirements where mass reduction is mission-critical. In January 2026, Parker Hannifin’s Chomerics division announced a USD 50 million capacity expansion in Eastern Europe dedicated to thermally conductive gap filler pads and conductive elastomers, aligning with the rapidly growing EV battery, inverter and fast-charging infrastructure markets where EMI shielding and thermal management must be co-optimized.

Innovation in material science and nanotechnology is also driving the next wave of flexible and ultra-thin EMI shielding. In November 2025, a major US National Laboratory reported a nanomaterial-based composite that delivers >40 dB SE at 6 GHz with only 0.1 mm thickness, validating the viability of ultra-thin, flexible EMI shielding for wearables and flexible electronics. In October 2025, DuPont introduced transparent conductive films providing >35 dB EMI shielding with >90% optical transparency, targeting head-up displays (HUDs), medical imaging screens and advanced infotainment displays, where display clarity and EMI control must coexist. In September 2025, Henkel disclosed a strategic partnership with a global 5G chipset manufacturer to co-develop package-level conformal shielding for mmWave devices, highlighting the trend toward component-level EMI solutions that support high-frequency, thermally stressed chipsets in compact packages.

Government policy and sector-specific regulations further reinforce EMI shielding demand. In June 2025, the US DoD awarded a significant contract to Laird Performance Materials (DuPont) for developing advanced magnetic shielding to protect sensitive electronics in next-generation unmanned aerial systems (UAS), emphasizing the strategic importance of low-frequency interference control in defense platforms. In May 2025, 3M brought to market EMI absorber sheets optimized for the 77 GHz band, directly serving automotive radar modules used in ADAS and collision avoidance. Regulatory tightening is also evident: in April 2025, the European Union revised its EMC Directive, introducing stricter testing and higher shielding effectiveness thresholds for wireless medical devices operating in crowded spectrum bands, a policy move that will accelerate adoption of medical-grade EMI shielding solutions across Europe. Together, these developments indicate a market pivot toward lighter, thinner, application-tailored EMI shielding with strong regulatory and investment tailwinds.

For industry professionals and buyers, the core questions are: how quickly EMI shielding specifications are tightening across frequency bands; which material systems (metal enclosures, conductive elastomers, foams, coatings, absorbers and films) are winning in high-growth applications; and how evolving EMC regulations and lightweighting requirements will reshape product portfolios and procurement decisions. The market is increasingly defined by multifunctional solutions that combine EMI shielding with thermal management, weight reduction and design flexibility, enabling OEMs to achieve compliance without sacrificing form factor, efficiency or cost targets.

- 5G/mmWave performance pressure: Emerging 5G and mmWave devices increasingly require shielding effectiveness (SE) of 60–80 dB in the 20–40 GHz band, accelerating adoption of high-performance EMI absorber materials and metal mesh solutions in base stations, small cells, CPE and RF front-end modules.

- Sensor-dense automotive platforms: Level 3–4 autonomous vehicles integrate 10–12 radar, LiDAR and camera sensors, each needing discrete EMI isolation, driving demand for gaskets, absorbers, films and coatings capable of preserving signal integrity for ADAS and autonomous driving.

- Miniaturization and tight tolerances: In smartphones, wearables and medical devices, sub-millimeter tolerances (0.3–0.5 mm) for EMI gasket compression and spacing necessitate advanced Form-in-Place (FIP) gaskets and conductive foams, enabling high-density PCB layouts without crosstalk.

- Defense and HEMP protection: HEMP-hardened defense and critical infrastructure assets must withstand transient field strengths up to 50 kV/m, supporting robust demand for specialized metal shielding enclosures and filters compliant with military standards.

- Ultra-thin conductive coatings: Next-generation conductive paints and coatings are delivering reliable EMI shielding at <25 μm dry film thickness, reducing device weight while maintaining SE, which is particularly valuable for portable and battery-powered electronics.

Technology-Led Trends and Emerging Opportunities Reshaping the EMI Shielding Market

Trend 1 - Conductive Polymer Composites Replace Metal Shielding in EVs and Advanced Consumer Electronics

The transition toward lightweight, high-integration electronic assemblies is fueling rapid adoption of conductive polymer composites as replacements for conventional metal EMI shielding. This shift is especially pronounced in electric vehicles (EVs) and compact consumer devices where weight reduction, thermal management, and design flexibility are priorities.

Corporate R&D investment is accelerating material innovation. In June 2025, Henkel introduced a graphene-enhanced polymer composite engineered for high-frequency EMI shielding. The launch highlighted multifunctional attributes-lightweight architecture, improved thermal dissipation, and compatibility with 5G/6G device designs-demonstrating how polymer composites are becoming essential for future telecom and electronics platforms.

Automotive OEMs are rapidly adopting these materials to extend EV range. Research shows that replacing metal components with lightweight shielding polymers in battery housings, inverters, and power distribution modules significantly reduces vehicle mass, directly improving energy efficiency. This positions conductive polymer EMI shielding as a critical enabler of EV performance optimization.

A fast-growing subset is intrinsically conductive polymers (ICPs), which allow manufacturers to produce thin, conformal coatings and complex molded geometries with predictable electrical performance. Their ability to deliver board-level shielding in compact consumer electronics makes them indispensable for smartphones, wearables, and IoT devices.

Industry investment reflects these priorities. In April 2024, BASF expanded its e-mobility plastics portfolio to include specialized EMI-shielding formulations for e-motors and power electronics-underscoring the rising demand for durable, thermally stable polymer shielding systems tailored to high-voltage automotive environments.

Trend 2 - Regulatory and EMC Compliance Pressure Strengthens Demand for Advanced EV/ADAS Shielding

Global regulatory frameworks are reshaping the EMI shielding market by enforcing rigorous safety, reliability, and electromagnetic compatibility (EMC) standards for high-voltage EV components and sensor-intensive ADAS systems.

In Europe, the UNECE Regulation No. 10 (successor to the Automotive EMC Directive) mandates stringent emission and immunity testing for road vehicles, with explicit coverage of 100V to 1000V high-voltage EV systems. These systems generate stronger electromagnetic interference, compelling automakers to adopt superior EMI shielding solutions.

ADAS platforms intensify these requirements. Radar, lidar, and camera modules must operate without signal distortion, requiring shielding materials that meet CISPR 25 emission limits-typically below 30 dBµV/m at 1 meter up to 1 GHz. This regulatory benchmark directly influences PCB design, connector architecture, and housing-level shielding strategies for automated braking, steering, and collision-avoidance functions.

Global alignment is expanding regulatory impact. India’s AISC revision of AIS-004 (Part 3) now mirrors international EMC standards and introduces new tests for EVs equipped with Rechargeable Electric Energy Storage System (REESS) charging interfaces. This addition requires automakers to control EMI originating from vehicle-to-grid coupling systems, creating new demand for high-performance shielding materials engineered specifically for charging ports, high-voltage connectors, and power electronics.

Together, these mandates elevate EMI shielding from a design preference to a regulatory requirement, driving sustained adoption across EV, ADAS, and autonomous vehicle platforms.

Opportunity 1 - High-Frequency mmWave Shielding Solutions for 5G/6G and Automotive Radar

The acceleration toward mmWave communication systems, including 5G FR2, 6G research bands, and next-generation automotive radar, is creating a high-value materials innovation opportunity. Traditional metal and polymer systems are inadequate at 77–81 GHz, 140 GHz, and emerging 0.22 THz frequencies, necessitating new EMI shielding architectures with low reflection, high absorption, and minimal insertion loss.

Government-funded R&D is catalyzing this shift. Under India’s Telecom Technology Development Fund (TTDF), C-DOT and IIT Roorkee initiated a joint program to develop polymer-based mmWave transceivers for rural 5G connectivity. The project promotes hybrid material systems-combining advanced polymers with metallization-to achieve cost-effective, high-frequency shielding performance suitable for telecom and IoT infrastructure.

Next-generation semiconductor packaging amplifies this need. Antenna-in-Package (AiP) architectures for 5G/6G devices require shielding integrated directly into the package to reduce RF path lengths and minimize mmWave transmission loss. This is generating demand for ultra-thin films, low-loss dielectrics, and advanced shielding nanomaterials tailored for sub-THz frequencies.

Automotive radar adds further complexity. With systems increasingly operating in the 77–81 GHz band and prototype platforms exploring 140 GHz, shielding must balance high effectiveness with low reflection to prevent signal distortions that compromise radar accuracy. This is expanding the market for carbon-based absorbers, graphene-enhanced films, advanced gaskets, and precision-engineered conductive polymers.

The mmWave transition represents one of the most commercially significant material innovation opportunities in the EMI shielding ecosystem.

Opportunity 2 - Sustainable, Recyclable EMI Shielding Solutions for Circular Electronics

Circular economy policies, rising global e-waste volumes, and consumer demand for sustainable electronics are generating strong commercial incentives for recyclable EMI shielding materials that do not contaminate plastics recovery streams.

The EU Waste Electrical and Electronic Equipment (WEEE) Directive explicitly mandates the design of electronics enabling reuse, recovery, and dismantling. This directly pressures manufacturers to shift away from non-recyclable metal coatings and adopt peelable, dissolvable, or mono-material shielding systems compatible with mass-market plastic enclosures.

Europe generated 13.5 million tonnes of e-waste in 2021-reinforcing the urgency of high-value material recovery. To achieve national circular economy targets, manufacturers are increasingly exploring metal-free EMI shielding based on carbon nanomaterial-reinforced polymers.

Material science innovations support this transition. Conductive nanocomposites incorporating graphene, carbon nanotubes, and hybrid carbon fillers offer superior electrical conductivity and EMI shielding effectiveness without introducing heavy metals or separation challenges. Their low density, chemical processability, and recyclability make them strong contenders for sustainable smartphone housings, IoT electronics, and home appliance components.

As global policy and consumer preference converge, sustainable EMI shielding solutions are shifting from optional to essential, creating a lucrative pathway for differentiated product portfolios built around recyclable materials.

EMI Shielding Market Share Analysis

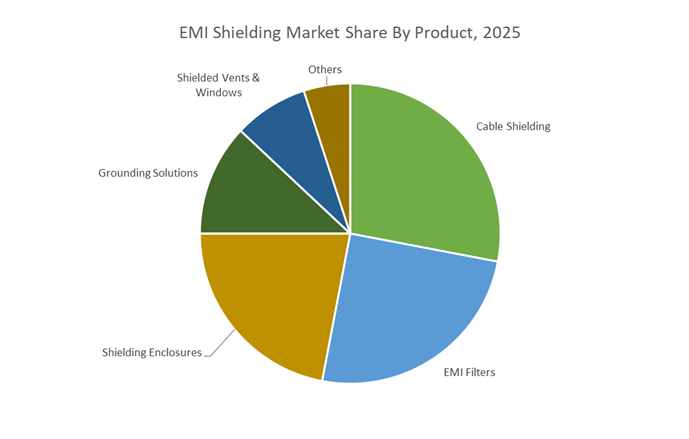

Market Share by Product/Form: Cable Shielding Leads Due to Its Critical Role in EMI Suppression Across High-Frequency Systems

Cable Shielding accounts for the largest 28% share in the EMI Shielding Market, reflecting its irreplaceable role as the primary barrier against both conducted and radiated electromagnetic interference. Because cables inherently behave like antennas—receiving external noise and emitting internal noise over extended lengths—they represent the most vulnerable and noise-intensive pathways in any electrical or electronic system. This dominant share is reinforced by the high shielding effectiveness achievable through braided, foil, or hybrid constructions, with even 70% coverage providing substantial attenuation for medium-frequency environments. In high-frequency applications above 100 MHz, where EMI challenges intensify due to increased radiated emissions, combination shields (foil + braid) have become indispensable to maintaining system integrity. Market adoption is further strengthened by the engineering reality that cable shielding often serves as the “last line of defense” for EMC compliance in power conversion equipment, motor drives, inverters, and high-speed data interfaces—areas where internal noise sources cannot be eliminated. Proper grounding techniques, which ensure a low-impedance return path for common-mode currents, enhance shielding effectiveness by reducing radiated emissions at their origin. The rising complexity of electronic architectures, electrification in automotive systems, and the expansion of high-speed digital networks continues to reinforce cable shielding’s leadership position, making it the most mission-critical form of EMI protection in the overall market.

Market Share by End-Use Industry: Consumer Electronics Dominates Due to Miniaturization and High-Frequency Device Architecture

Consumer Electronics hold the top 32% share among end-use industries, driven by massive global production volumes and the escalating density of high-frequency components inside modern devices. Smartphones, laptops, wearables, tablets, AR/VR headsets, and smart home devices all incorporate thousands of electronic components packed within increasingly compact enclosures, dramatically heightening the risk of inter-component EMI. As device housings shrink and PCB layouts become more layered and complex, internal distances between noise-sensitive and noise-generating elements may be reduced to mere millimeters, making localized EMI shielding—metal cans, conductive coatings, and compartmentalized enclosures—mandatory for interference prevention. The dominance of this segment is further reinforced by the widespread adoption of advanced wireless protocols such as 5G, Wi-Fi 6/7, millimeter-wave communication, and multi-antenna architectures, all of which require stringent control of radiated and received noise to maintain signal integrity. Because these consumer devices must comply with global regulatory frameworks such as the FCC, CE marking, and other national EMC directives, manufacturers rely heavily on shielding solutions capable of delivering 40–60 dB shielding effectiveness to meet emissions limits without compromising performance. The continuous upgrade cycle in consumer electronics, combined with the sector’s rapid innovation pace and its reliance on high-frequency, tightly integrated circuitry, solidifies its position as the largest and most influential end-use industry in the EMI shielding market.

Country Analysis: Global EMI Shielding Development Frontrunners

China: 5G Infrastructure Acceleration and High-Volume EMI Shielding Manufacturing Leadership

China stands as the most influential global force in the EMI shielding market due to its unparalleled 5G rollout pace, large-scale electronics manufacturing base, and vertically integrated supply chains for shielding materials. With over 4.6 million 5G Base Transceiver Stations (BTSs) deployed nationwide by late 2024, China has created one of the world’s largest demand centers for RF shielding solutions, wave absorbers, conductive coatings, and metalized enclosures used in base stations and small cells. This massive deployment is complemented by extensive R&D investments from institutions such as the Chinese Academy of Sciences, which are pioneering advanced carbon-based shielding materials, including graphene and carbon nanotube (CNT) composites. These innovations target lightweight EMI shielding applications essential for compact telecom and consumer electronics devices. Government policies further reinforce this momentum by prioritizing domestic manufacturing of conductive polymers, shielding gaskets, metal foils, and conductive adhesives, reducing reliance on U.S. and Japanese suppliers in strategic sectors such as defense-grade electronics and high-frequency telecom components.

China’s position is strengthened by its dominance in the consumer electronics and EV industry, both major consumers of EMI shielding tapes, electromagnetic interference laminates, and high-temperature conductive adhesives. The world’s largest electric vehicle market is prompting rapid scale-up of localized production of shielding gaskets, EMI suppression composites, and thermal management materials for Battery Management Systems (BMS), inverters, and onboard chargers, where electromagnetic interference can compromise functional safety. China’s strategic control over upstream raw materials—including nickel powders, barium titanate, and high-purity metal oxides—provides stability to a market that relies heavily on uniform, high-performance EMI shielding inputs. Parallel advances in EMC (Electromagnetic Compatibility) regulations are pushing manufacturers toward higher repeatability, consistency, and shielding effectiveness, enhancing China’s competitiveness in global EMI shielding production.

United States: Defense-Driven EMI Shielding Innovation and Leadership in mmWave 5G Systems

The United States EMI shielding market is distinguished by its stringent military specifications, strong aerospace and defense demand, and technologically advanced 5G/mmWave communication ecosystem. The U.S. Department of Defense (DoD) continues to drive high-value demand for advanced EMI shielding composites, including silver–nickel-coated paints, conductive elastomers, and radar-absorbent materials, which are essential for avionics, electronic warfare systems, and mission-critical communications. Leading companies such as Parker Hannifin’s Chomerics division are innovating Form-in-Place (FIP) conductive elastomers, enabling automated precision sealing for compact electronics while ensuring stringent environmental protection and electromagnetic suppression performance. The country’s rapid adoption of mid-band and high-band mmWave spectrum for 5G mobility and fixed wireless access is further accelerating the need for EMI absorber materials, shielded ventilation systems, and interference-suppressing device enclosures to maintain signal integrity in densely packed RF environments.

The rise of EV reshoring and semiconductor manufacturing expansion under U.S. federal incentives is creating a robust domestic ecosystem for thermal and EMI shielding components essential for next-generation power electronics. Research institutions, supported by grants from the Department of Energy (DOE) and other federal agencies, are advancing the development of transparent EMI shielding films for automotive displays, military-grade sensors, and industrial interfaces. The FCC’s rigorous EMC requirements ensure that all consumer and industrial electronics incorporate certified EMI filtering and shielding solutions, sustaining recurring demand across thousands of product categories. Combined, these elements reinforce the U.S. as a global center for high-reliability, high-frequency, and military-grade EMI shielding technologies.

Germany: Automotive EMC Precision and Industrial Automation Driving High-Performance EMI Shielding Demand

Germany’s status as a global automotive and industrial automation powerhouse drives strong demand for precision-engineered EMI shielding components compliant with stringent European EMC regulations. As German automotive OEMs accelerate deployment of electrified and software-defined vehicles, they require custom-engineered shielding gaskets, shielding cans, conductive adhesives, and RF absorbers for critical modules such as ADAS sensors, ABS controllers, electric powertrain components, and HV control units. The move toward high-voltage EV architecture is intensifying reliance on robust EMI suppression to prevent electromagnetic noise that could compromise vehicle safety and real-time communication between vehicle subsystems.

Germany’s advanced manufacturing ecosystem also generates sustained demand for shielded enclosures, cable shielding braids, and EMI suppression cores essential for Industry 4.0 systems, which operate in electromagnetically noisy factory environments. Major players such as Henkel (LOCTITE) continue to develop high-performance conductive coatings and adhesives designed for automated dispensing and long-term operational durability. Germany’s R&D-driven environment, supported by the Fraunhofer Institutes, is pioneering shielding textiles, flexible metallic foils, and advanced EMI/RFI materials optimized for medical electronics, robotics, and industrial control systems. The country’s strict adherence to the EU Electromagnetic Compatibility Directive 2014/30/EU ensures a stable and compliance-oriented market for high-precision EMI shielding technologies.

South Korea: Ultra-Thin EMI Shielding Films and Semiconductor-Level Precision for Advanced Consumer Electronics

South Korea leverages its global leadership in smartphones, displays, and memory semiconductors to shape innovation in ultra-thin EMI shielding films, high-frequency absorbers, and wafer-level EMI solutions. As Korean handset manufacturers intensify device miniaturization efforts, they require next-generation shielding solutions including micron-scale conductive films, adhesive tapes, and nano-engineered absorbers to protect RF modules, processors, camera units, and high-density PCBs. South Korea’s semiconductor sector, among the most advanced globally, drives continuous demand for chip-level EMI barriers, shielding caps, and redistribution-layer (RDL) EMI suppression materials, essential for reducing crosstalk within advanced integrated circuits.

Growing investments in 5G and early-stage 6G infrastructure are further fueling domestic R&D into novel EMI absorbers, metasurface-based suppression materials, and advanced ferrite composites engineered for ultra-high-frequency noise mitigation. At the same time, Korea’s expanding EV industry—supported by global automakers and cell manufacturers—requires shielded gaskets, conductive foams, and thermal EMI composites designed to withstand harsh automotive conditions. As South Korea deepens its footprint in global consumer electronics and semiconductor supply chains, it continues to position itself as a leader in precision EMI shielding materials optimized for next-generation high-speed, high-power electronics.

Japan: Exceptional Material Purity and High-Reliability EMI Shielding Components for Automotive and Industrial Markets

Japan remains an influential leader in the development of high-purity metals, ferrite absorbers, and precision EMI shielding components used across the telecom, automotive, and industrial automation markets. Japanese material science companies continue to dominate the production of high-performance ferrites, metal powders, and absorber sheets, essential for RF noise suppression in antennas, power converters, and high-frequency modules. Manufacturers such as Kitagawa Industries specialize in precision-engineered EMI gaskets, fingerstock contacts, and die-cut shielding components that meet the strict reliability requirements of automotive and aerospace customers.

Japan’s automotive sector—recognized globally for its uncompromising quality standards—consistently drives the adoption of long-life EMI shielding foams, thermally conductive shielding materials, and robust EMI enclosures for ADAS systems, ECU modules, and hybrid powertrains. Additionally, Japan’s advanced robotics and industrial machinery ecosystem relies on durable, high-flex cable shielding and interference-resistant enclosures to ensure consistent performance in electromagnetically dense environments. With its deep-rooted material science capabilities and precision manufacturing infrastructure, Japan continues to supply some of the world’s most trusted and high-reliability EMI shielding solutions.

Competitive Landscape of Global EMI Shielding Solutions Providers

The EMI shielding competitive landscape is shaped by a combination of materials science leadership, application-specific engineering expertise and global manufacturing presence. Leading EMI shielding companies are not only supplying conductive elastomers, films, tapes, absorbers and coatings, but are also integrating thermal management, mechanical robustness and miniaturization compatibility into their portfolios. Strategic moves in the market center on developing multi-functional materials, expanding capacity near automotive and electronics hubs, and collaborating closely with OEMs in 5G, EV, aerospace, defense and medical devices to meet evolving EMC standards and program-specific requirements.

Laird Performance Materials, part of DuPont, is a key player in thermal and EMI multifunction solutions, offering a broad portfolio of electrically conductive gaskets, EMI absorbers and thermal interface materials (TIMs). The company’s strategic focus is on multi-functional materials (MFMs) that simultaneously address thermal dissipation and electromagnetic compatibility in tightly packed electronics. Flagship products including CoolShield™ Flex and HeatsinX™ reduce the need for separate thermal and EMI components, freeing space in compact designs including automotive ECUs, telecom base stations and high-density servers. Laird’s ongoing investments in advanced FIP gasket dispensing automation further strengthen its position as a preferred partner for high-volume, high-reliability EMI shielding in automotive and industrial markets.

Parker Hannifin’s Chomerics Division is a leading provider of conductive elastomer gaskets and Form-in-Place (FIP) shielding solutions, with deep experience in rugged, high-reliability EMI applications. Its Cho-Seal® line and related conductive elastomer technologies are widely used in aerospace, defense and critical infrastructure where HEMP resistance, environmental sealing and corrosion resistance are paramount. The division’s core strengths lie in precision-engineered gaskets and seals capable of maintaining performance under extreme temperature, vibration and environmental exposure. With growing demand from EV powertrain electronics and charging infrastructure, Chomerics is leveraging its expertise to deliver EMI shielding that also withstands harsh automotive operating conditions and aligns with global EMC standards.

3M is a major innovator in EMI tapes, shielding films and absorber sheets, focusing on flexible, peel-and-stick solutions that simplify integration for design engineers. Its portfolio spans electrically conductive tapes, ultra-thin absorber materials and specialty shielding laminates, enabling effective EMI control across smartphones, tablets, networking equipment and automotive electronics. A key highlight is 3M’s 2025 launch of EMI absorber sheets optimized for the 77 GHz frequency band, directly targeting automotive radar modules used in ADAS systems. The company’s R&D is heavily concentrated on advanced conductive fillers and adhesive systems to achieve higher SE in thinner formats, supporting ongoing trends toward miniaturization and weight reduction in consumer and automotive electronics.

Henkel AG & Co. KGaA occupies a pivotal role in conductive adhesives, coatings and package-level EMI shielding materials, with a strong presence in semiconductor packaging. The company’s solutions include ultra-thin metal inks and conductive coatings applied via spray or stencil processes, enabling conformal shielding directly at the device or package level. The is particularly important for high-frequency 5G and mmWave chipsets, where per-package shielding can significantly reduce system-level interference and enable denser layouts. Henkel’s strategic alignment with high-volume semiconductor manufacturing and consumer electronics is reinforced by its focus on materials that support high-UPH (units per hour) processes, making its EMI shielding offerings attractive to top-tier chipset and module manufacturers.

DuPont de Nemours, Inc. brings strong polymer science and advanced films expertise to the EMI shielding market, offering specialized materials including Kapton® polyimide films and flexible shielding laminates. Its product portfolio is tuned to applications requiring flexibility, durability and low weight, including flexible PCBs, wearable devices and foldable electronics. DuPont’s development of transparent EMI films capable of delivering significant shielding while maintaining high optical clarity positions the company at the forefront of HUD, AR displays and medical imaging systems. Its ability to integrate EMI shielding into thin, robust polymer platforms allows OEMs to meet stringent EMC requirements without sacrificing industrial design or user experience.

TDK Corporation is a global leader in ferrite materials and EMI/EMC filters, supplying a wide range of components for noise suppression and power line filtering. Its ferrite cores, common-mode chokes and discrete EMI filters are integral to the EMC strategy of automotive ECUs, industrial drives, power supplies and data communication equipment. TDK’s core strength lies in mastering magnetic materials and passive components that ensure stable performance over wide temperature and frequency ranges. With the increasing penetration of EVs, renewable energy systems and high-speed data networks, TDK’s EMI components are critical for achieving regulatory compliance and stable operation in electrically noisy environments, reinforcing its position as a foundational supplier in the EMI shielding and EMC ecosystem.

EMI Shielding Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.1 Billion

|

|

Market Size (2035)

|

$13.6 Billion

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Material Type (Conductive Coatings & Paints, Conductive Polymers, Metal Shielding, Conductive Tapes & Laminates, EMI Gaskets & Elastomers, EMI Absorber Materials), By Product/Form (Shielding Enclosures, EMI Filters, Shielded Vents & Windows, Cable Shielding, Grounding Solutions), By End-Use Industry (Consumer Electronics, Automotive, Telecommunications & IT, Aerospace & Defense, Healthcare, Industrial), By Shielding Method (Radiation Shielding, Conduction Shielding, Absorption Shielding)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Parker Hannifin Corp. (Chomerics), 3M Company, Henkel AG & Co. KGaA, Laird Performance Materials, PPG Industries Inc., TE Connectivity, Schaffner Holding AG, Dow Inc., Tech Etch Inc., Kitagawa Industries Co. Ltd., ETS-Lindgren, Nolato AB, MG Chemicals, Averatek Corp.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

EMI Shielding Market Segmentation

By Material Type

- Conductive Coatings & Paints

- Conductive Polymers

- Metal Shielding

- Conductive Tapes & Laminates

- EMI Gaskets & Elastomers

- EMI Absorber Materials

By Product/Form

- Shielding Enclosures

- EMI Filters

- Shielded Vents & Windows

- Cable Shielding

- Grounding Solutions

By End-Use Industry

- Consumer Electronics

- Automotive

- Telecommunications & IT

- Aerospace & Defense

- Healthcare

- Industrial

By Shielding Method

- Radiation Shielding

- Conduction Shielding

- Absorption Shielding

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies: EMI Shielding Solutions Providers

- Parker Hannifin Corp. (Chomerics Division)

- 3M Company

- Henkel AG & Co. KGaA

- Laird Performance Materials

- PPG Industries Inc.

- TE Connectivity

- Schaffner Holding AG

- Dow Inc.

- Tech Etch, Inc.

- Kitagawa Industries Co. Ltd.

- ETS-Lindgren

- Nolato AB

- MG Chemicals

- Averatek Corp.

*- List not Exhaustive