Ultra-High-Purity Silicon Carbide (UHP Sic) Market Overview: Yield Economics, Diameter Scaling, and Automotive Qualification Redefine Value Creation

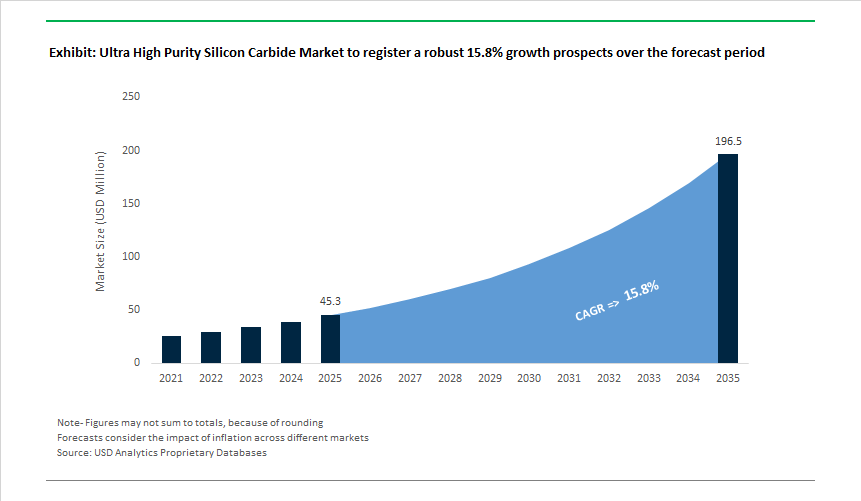

The Ultra-High-Purity (UHP) Silicon Carbide market, valued at USD 45.3 million in 2025 and projected to reach USD 196.4 million by 2035 at a 15.8% CAGR, is no longer an experimental upstream materials niche. It has become a yield-critical input market for automotive-grade power electronics, hyperscale datacenter power architectures, and RF/GaN device platforms. Demand is being pulled not simply by SiC adoption, but by OEM insistence on automotive-qualified, statistically repeatable substrates and epi-ready wafers that sustain high yields at 650-1200 V operating classes.

Across the supply chain, manufacturers are converging on a narrow set of performance thresholds that directly determine device cost and qualification timelines. Leading substrate suppliers are standardizing 5N-6N bulk SiC purity, with transition-metal contamination (Fe, Al, Ti) controlled below 1 ppm, as higher impurity levels are now directly correlated with leakage current drift and premature field failures in traction inverters and server PSUs. This is pushing tighter raw-material selection, longer crystal growth cycles, and more aggressive in-line metrology-raising capital intensity but materially improving downstream device reliability.

Automotive and industrial customers are benchmarking wafers on average BPD density and die-level yield stability over lifetime testing. Modern production lines are achieving <1,500 BPD/cm² on 150 mm 4H-SiC wafers, representing a step-change versus first-generation material and enabling meaningful reductions in current collapse and bipolar degradation. As device makers move toward 200 mm roadmaps, defect propagation control, not boule growth speed, is emerging as the binding constraint.

Further, maintaining total thickness variation (TTV) below 1.0 µm on 150 mm wafers, while preserving surface morphology suitable for uniform epitaxy, has become a prerequisite for high-volume fabs. As diameter transitions accelerate, wafer flatness, warp control, and thinning yield are emerging as silent yield killers-forcing suppliers to invest in polishing, metrology, and wafer handling technologies traditionally associated with advanced silicon fabs.

Strategically, the market is consolidating around vertically integrated models. Device OEMs and Tier-1 module suppliers are prioritizing partners that control bulk crystal growth to substrate to epitaxy, supported by multi-year capacity agreements. This is less about cost negotiation and more about supply assurance, PPAP stability, and synchronized node transitions-particularly as 800 V EV platforms and >1200 V industrial modules move into mass production.

Market Analysis: Recent Strategic, Capacity, and Technology Developments

The UHP SiC market saw concentrated investment and commercialization activity as device makers and substrate producers accelerated capacity to meet surging demand. In Jul 2024, Wolfspeed and Renesas cemented supply-chain assurances when Renesas placed a major deposit to secure a 10-year supply of SiC bare and epiwafers, signaling OEMs’ dependence on stable substrate pipelines for EV powertrains. This upstream-downstream coupling continued into Apr 2024, when leading EV manufacturers announced broad adoption of SiC in 800V platforms - a key application that materially increases SiC content per vehicle and compresses time-to-volume demand for UHP substrates.

Policy and national industrial strategy influenced capacity expansion in 2025. In Oct 2025, Japan’s METI awarded significant funding (JPY 70.5 billion) to bolster domestic SiC substrate manufacturing via Denso and Fuji Electric, targeting 310,000 substrates/year by 2027 - a move to improve supply chain sovereignty for automotive and industrial customers. Parallel to government action, private-sector process innovation advanced: Aug 2025 saw Coherent report shipments of 500 µm-thick epi wafers, enabling lower substrate cost per cm² and improving handling for high-voltage device fabrication. Market consolidation and strategic partnerships also emerged - for example, May 2025 GlobalFoundries partnered with Navitas to accelerate GaN/SiC solutions for AI datacenters, reflecting the cross-technology synergies between SiC substrates and next-generation power/RF architectures.

Regional supply dynamics shifted as Chinese substrate makers expanded capacity aggressively; by Feb 2025 industry reports suggested this expansion would stabilize prices for mid-purity 5N substrates by late 2025. On the other hand, device makers continued to optimize cell designs and wafer utilization: Nov 2025 brought X-FAB’s XSICM03 platform (reduced MOSFET cell pitch) which increases die-per-wafer economics - underscoring a parallel demand driver: wafer-level cost efficiency is as important as material purity and defect control.

Ultra High Purity Silicon Carbide Market Trends and Opportunities

Industrial Transition to 200 mm (8-Inch) Ultra-High-Purity SiC Wafers

The ultra-high-purity silicon carbide (UHP SiC) market is undergoing a structural inflection as manufacturers pivot from 150 mm to 200 mm wafer platforms, a move driven less by technology curiosity and more by manufacturing economics and EV platform scale. Increasing wafer diameter lifts usable die count per boule by roughly 1.8–1.9×, materially improving cost-per-ampere for high-voltage devices. For automotive OEMs pushing toward multi-million EV production volumes, this transition is becoming a prerequisite rather than an option.

In early 2025, Infineon Technologies AG became the first to ship power devices based on 200 mm SiC substrates, validating wafer-scale process stability across high-voltage classes used in traction inverters, rail electrification, and ultra-fast charging. Parallelly, Wolfspeed accelerated ramp-up at its Mohawk Valley fab, reaching meaningful wafer-start utilization and signaling a full transition of EV powertrain production to 200 mm by 2025. These fabs are underpinned by upstream crystal capacity expansion, where impurity control at the parts-per-billion level has become the dominant yield determinant.

Capital commitments across the value chain underscore the permanence of this shift. STMicroelectronics is executing a multi-billion-euro build-out in Catania designed for vertical integration—from UHP boule growth to back-end assembly—targeting industrial-scale 200 mm output. Strategically, the industry is accepting near-term capex intensity in exchange for long-run cost learning curves, positioning UHP SiC as a mainstream power semiconductor substrate rather than a specialty material.

High-Purity Semi-Insulating SiC for Quantum, RF, and Next-Gen Communications

Beyond power electronics, ultra-high-purity semi-insulating (HPSI) SiC is emerging as a strategic material for quantum technologies and RF systems, where defect control directly defines device viability. Color centers such as silicon vacancies and divacancies act as optically addressable quantum states, but only when background impurity concentrations are reduced to near-zero levels. Studies published in 2025 confirm that even trace contamination causes spin decoherence and frequency drift, eroding qubit performance and sensor fidelity.

From a manufacturing perspective, SiC’s compatibility with CMOS workflows gives it a structural advantage over alternative quantum substrates. Wafer-scale processability allows repeatable defect engineering, enabling quantum sensors and RF components to be produced using established semiconductor tooling rather than bespoke laboratory methods. In RF communications, the elimination of micropipes has become non-negotiable. In 2025, SICC demonstrated zero micropipe density in semi-insulating substrates, a milestone that directly improves yield and reliability for 5G and emerging 6G front-end modules where localized defects can induce catastrophic signal loss.

Notably, the industry is already signaling its next horizon. Late-2024 demonstrations of 300 mm N-type SiC substrates indicate that UHP SiC crystal growth science is advancing ahead of device demand. While commercial 300 mm adoption remains a next-decade event, early readiness strengthens SiC’s long-term position as the backbone material for ultra-high-frequency and quantum-enabled electronics.

SiC/SiC Composites for Nuclear, Hypersonics, and Extreme Environments

Ultra-high-purity SiC is also unlocking adjacent opportunities in ceramic matrix composites (CMCs), particularly for nuclear energy and hypersonic aerospace systems. Unlike monolithic ceramics, SiC/SiC composites exhibit graceful, non-catastrophic failure, a property that is essential in radiation-rich or ultra-high-temperature environments where safety margins are paramount.

In late 2025, General Atomics Electromagnetic Systems announced onshoring of SiC fiber manufacturing to support U.S. advanced reactor programs. Its hybrid densification approach reportedly shortens production cycles by ~70% while cutting energy use by ~80%, highlighting how process innovation is shaping adoption economics. Concurrent assessments by the U.S. Nuclear Regulatory Commission confirmed that near-stoichiometric, impurity-controlled SiC/SiC composites maintain mechanical integrity under neutron exposure, with purity identified as the primary factor limiting parasitic neutron absorption.

In aerospace, these same composites are being evaluated for turbine hot sections and hypersonic leading edges, where conventional nickel superalloys approach their mechanical limits. The convergence of nuclear and aerospace demand is positioning UHP SiC as both semiconductor input and a strategic extreme-environment material platform.

Ultra-High-Voltage SiC Substrates for Grid Modernization and Renewables

Grid electrification and renewable integration are creating a distinct opportunity for ultra-high-voltage SiC substrates, enabling power devices that operate directly above 15 kV. This capability supports solid-state transformers (SSTs) and compact HVDC systems, eliminating layers of copper-intensive, efficiency-eroding transformers.

In October 2025, Navitas Semiconductor disclosed 2300 V and 3300 V SiC MOSFET platforms that simplify medium-voltage grid architectures while delivering lower on-resistance at elevated temperatures. Complementary demonstrations by Oak Ridge National Laboratory and National Renewable Energy Laboratory showed that SiC-based inverters sustain higher operating temperatures with materially reduced conversion losses in utility-scale solar installations.

As utilities demand 20-plus-year reliability from power electronics, new “AEC-Plus” qualification regimes are emerging to certify SiC modules for mission-critical infrastructure. For UHP SiC producers, this elevates purity, defect density, and boule homogeneity from yield considerations to grid-level reliability enablers, anchoring long-term demand well beyond the EV cycle.

Market Share Analysis: Ultra-High Purity Silicon Carbide Market

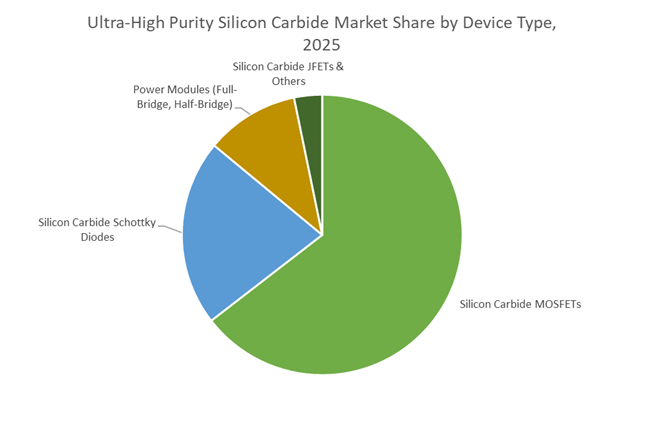

Market Share by Product Type: SiC MOSFETs Dominate High-Voltage Power Electronics Platforms

Silicon Carbide (SiC) MOSFETs account for approximately 60% of the global Ultra-High Purity Silicon Carbide Market, reflecting their position as the most value-dense and performance-critical device category in modern power electronics. This dominance is driven by SiC MOSFETs’ ability to deliver near-lossless switching efficiency, enabling power conversion systems to operate at efficiency levels that fundamentally outperform silicon-based IGBTs. Even marginal percentage gains in efficiency translate into disproportionate reductions in heat generation, which directly impacts system reliability, cooling complexity, and operating costs. Market share is further reinforced by the elimination of switching tail current, allowing SiC MOSFETs to operate at much higher frequencies and unlock substantial reductions in passive component size and overall bill of materials. Advances in device architecture have also lowered on-resistance under high-temperature conditions, ensuring stable performance under heavy electrical loads and preventing thermal runaway in mission-critical systems. Crucially, the commercial availability of 1,200V and 1,700V SiC MOSFETs has expanded addressable markets well beyond the voltage limits of conventional silicon, making these devices indispensable in next-generation automotive, industrial, and energy infrastructure platforms. Together, these efficiency, scalability, and system-level advantages explain why SiC MOSFETs remain the cornerstone product segment of the ultra-high purity silicon carbide market.

Market Share by End-User Industry: Automotive Electrification Anchors SiC Demand Growth

The automotive sector represents approximately 65% of total demand in the Ultra-High Purity Silicon Carbide Market, positioning electric and hybrid vehicles as the dominant end-use driver. This leadership is directly linked to the industry-wide transition toward 800V high-voltage vehicle architectures, where silicon-based power devices reach their physical and economic limits. SiC MOSFETs enable higher switching speeds and elevated operating temperatures, allowing automakers to shrink inverter cooling systems and reduce overall drivetrain mass—improvements that translate into measurable gains in driving range without increasing battery capacity. Market share is further reinforced by SiC’s role in enabling ultra-fast charging, where higher voltage platforms dramatically reduce charging times and improve vehicle utilization. At the system level, the adoption of SiC delivers net cost benefits by reducing cooling hardware, cabling weight, and battery oversizing requirements, offsetting the higher unit cost of SiC devices. As global OEMs accelerate electrification roadmaps and prioritize efficiency, range, and fast-charging capability, automotive applications remain the primary demand anchor for ultra-high purity silicon carbide, sustaining their dominant market share.

Competitive Landscape: UHP Sic Suppliers and Strategic Profiles

Overall market dynamics favor vertically integrated suppliers and specialized epi/substrate experts who can deliver 5N-6N purity, low-BPD substrates, precise TTV control, and scale to larger wafer diameters. The supplier field combines pure-play substrate/epi firms, legacy semiconductor materials groups, and device manufacturers moving upstream. Leadership depends on capacity investments (150→200 mm transition), defect engineering, thermal performance, and the ability to secure long-term contracts with automotive OEMs, power electronics houses, and datacenter integrators.

Wolfspeed, Inc. - Scaling To 200 Mm With Vertical Integration and Automotive-Qualified Sic Modules

Wolfspeed is a leading vertically integrated SiC player building massive capacity (John Palmour Manufacturing Center) to support a >10× increase in production. The company is a front-runner in the 200 mm transition, improving die count per wafer and reducing per-chip costs - a critical advantage for EV traction inverters and high-voltage industrial modules. Wolfspeed’s automotive-qualified 1200V modules, rated for operation at ~185°C junction temperature, demonstrate its device-level focus and supply-chain control from UHP material to packaged power modules.

Coherent Corp. - End-To-End Sic Wafer Manufacturing and Epi Innovation For RF/Gan and Power

Coherent’s vertical integration spans bulk crystal growth, slicing, polishing, and epitaxy, enabling bespoke epiwafers for high-power RF and GaN-on-SiC stacks. The company’s development and shipment of thicker epi wafers (e.g., 500 µm) help lower substrate cost per area and support robust epitaxial layers for high-voltage devices. Coherent emphasizes long-term contracts with Tier-1 automotive and industrial clients to stabilize demand and align substrate roadmaps with device requirements.

Rohm Co., Ltd. - Internalizing Substrate Supply and Innovating Double-Trench Sic Mosfets For Reduced Switching Loss

Rohm has strategically acquired SiC wafer capability to secure feedstock and scale device production (notably a 300% device capacity growth target over five years). The company’s double-trench SiC MOSFET structures reduce ON-resistance and lower switching losses by ~40% versus Si IGBTs in 1200V applications, making Rohm’s modules an attractive proposition for EV on-board chargers and industrial drives where efficiency and thermal resilience are essential.

Stmicroelectronics N.V. - Early Mover in Large-Diameter Sic Production and Multi-Year Automotive Commitments

STMicroelectronics was an early shipper of 200 mm-based SiC devices and continues to invest heavily in high-volume wafer fabs (including multi-billion euro projects) to secure its supply chain. The company holds significant multi-year supply agreements with major OEMs for 800V and higher systems, positioning ST as a key partner for automakers transitioning to SiC-based powertrains and high-voltage electrification platforms.

Resonac Corporation (Formerly Showa Denko) - High-Quality Epi Growth Specialist With Global Substrate Reach

Resonac is a major Japanese supplier of UHP SiC epitaxial wafers, focusing on low-defect layer growth and tight doping/uniformity control (thickness and doping deviations <3% across 150 mm wafers). Serving both power and RF markets, Resonac supplies epi services compatible with GaN-on-SiC architectures and supports global FABs with a stable production footprint - an important alternative for manufacturers seeking diversified supplier bases and proven epitaxial process control.

The United States Ultra High Purity Silicon Carbide market in 2025 is defined by a decisive shift toward end-to-end domestic control of SiC crystal growth, wafering, and device manufacturing. The commercial launch of 200 mm (8-inch) UHP SiC wafers marks a structural inflection point, enabling higher die yields and materially lower cost per amp for next-generation power electronics. This transition is tightly aligned with federal policy priorities under the CHIPS and Science Act, which treats compound semiconductors as critical to EV electrification, defense electronics, and AI data-center power efficiency. Following balance-sheet restructuring, Wolfspeed has repositioned its Mohawk Valley facility as the anchor asset in the U.S. SiC ecosystem, supported by proposed federal grants to stabilize long-term capacity expansion. Parallel to industrial scaling, the initiation of a Section 232 investigation into UHP SiC imports underscores Washington’s intent to deploy trade defense mechanisms to shield domestic CVD-grown, high-purity materials from price volatility and foreign overcapacity.

China: Purity Stabilization and State-Led Consolidation

China remains both the world’s largest consumer and one of the most influential producers in the UHP silicon carbide market, but its 2025 strategy reflects a pivot from aggressive volume expansion to purity management and price stabilization. By formally designating UHP SiC for third-generation semiconductors as an “encouraged industry,” Beijing has unlocked preferential access to subsidized electricity, land, and financing for compliant producers. At the same time, a state-backed consolidation fund is being deployed to merge sub-scale operators, addressing the severe oversupply conditions that triggered sharp price corrections in 2024. Leading vertically integrated players such as SICC and TanKeBlue are consolidating share in high-resistivity and aerospace-grade substrates, reinforcing China’s role as a dominant force in global SiC substrate supply while gradually tightening quality thresholds.

India: Semiconductor Mission and First-Wave SiC Fabs

India’s Ultra High Purity Silicon Carbide market has moved from policy ambition to early industrial execution under the ₹1.6 trillion India Semiconductor Mission. In 2025, government approvals for compound semiconductor fabs signal India’s intent to embed SiC within its domestic EV, rail traction, and renewable energy ecosystems. The commissioning of India’s first commercial SiC wafer facilities marks a strategic break from import dependence, particularly for high-voltage power devices. State-level electronics clusters, backed by aggressive fiscal incentives, are positioning regions near major logistics hubs as future SiC manufacturing centers. This policy-driven acceleration is reshaping India from a downstream device assembler into an emerging producer of UHP SiC substrates and epi-ready wafers tailored for high-temperature, high-frequency applications.

Japan: Economic Security and Materials Supremacy

Japan’s UHP SiC strategy is inseparable from its broader “economic security” doctrine, which prioritizes control over high-purity materials and semiconductor process know-how. Massive public funding into advanced logic manufacturing has had a spillover effect across the SiC supply chain, reinforcing demand for ultra-pure starting materials, defect-controlled crystal growth, and precision wafer processing. Japanese suppliers such as Shin-Etsu Chemical remain central to global high-purity materials supply, while domestic equipment makers continue to dominate critical cleaning and etching steps required for UHP SiC processing. New cybersecurity guidelines for semiconductor fabs further highlight the strategic sensitivity of SiC crystal growth IP, elevating UHP SiC from a commercial input to a protected national asset.

Germany & the European Union: IPCEI-Backed Power Electronics Integration

In Europe, the Ultra High Purity Silicon Carbide market is being shaped by the intersection of industrial decarbonization and power electronics sovereignty. Under the IPCEI framework and the European Chips Act, the EU is channeling capital toward vertically integrated SiC ecosystems capable of supporting automotive electrification and industrial energy efficiency. While some German expansion plans were deferred amid market volatility, long-term funding commitments remain intact, particularly for 200 mm wafer transition programs. STMicroelectronics is advancing internal substrate sourcing at its southern European campuses, reducing exposure to global price swings and reinforcing Europe’s ambition to localize critical SiC value chains for EV inverters and smart-grid infrastructure.

South Korea: Localization Under the MPE 2030 Roadmap

South Korea’s Ultra High Purity Silicon Carbide market is tightly coupled with its automotive and battery champions, driving an aggressive localization agenda under the MPE 2030 roadmap. Government-backed R&D tax credits and preferential financing are accelerating domestic capabilities in 200 mm SiC wafer growth, epitaxy, and doping control. The strategic objective is to insulate national EV supply chains from external shocks while building export-ready competence in high-purity substrates. SK Siltron has emerged as the cornerstone of this effort, ramping up 8-inch SiC production to position South Korea among the top global suppliers of automotive-grade wafers.

National Strategic Investment & Policy Comparison: Ultra High Purity Silicon Carbide Market (2025)

Ultra High Purity Silicon Carbide Market Strategic Investment Matrix

|

Country / Region

|

Primary Strategic Driver

|

Key Policy or Investment Lever

|

Core UHP SiC Focus

|

|

United States

|

Supply chain sovereignty

|

CHIPS Act grants & Section 232 probe

|

200 mm wafers, CVD purity

|

|

China

|

Price & purity stabilization

|

$7 B consolidation fund

|

High-resistivity substrates

|

|

India

|

Domestic EV ecosystem

|

₹1.6 T Semiconductor Mission

|

First-wave SiC fabs

|

|

Japan

|

Economic security

|

$25.7 B semiconductor subsidies

|

Ultra-pure crystal growth

|

|

EU (Germany)

|

Decarbonized power electronics

|

IPCEI & Chips Act (€43 B pool)

|

Integrated SiC value chains

|

Ultra High Purity Silicon Carbide Market Report Scope

Ultra High Purity Silicon Carbide Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$45.3 Million

|

|

Market Size (2035)

|

$196.4 Million

|

|

Market Growth Rate

|

15.8%

|

|

Segments

|

By Grade (5N, 6N, 7N), By Product Form (Granules, Powder, Crystals), By Wafer Size (150 mm, 200 mm, 300 mm), By Application (Power Electronics, High-Frequency Devices, Optical Electronics, Semiconductor Manufacturing Equipment), By Device Type (SiC MOSFETs, SiC Schottky Diodes, SiC JFETs, Power Modules), By End-User Industry (Automotive, Industrial, Energy & Power, Aerospace & Defense, Data Centers & IT)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Wolfspeed Inc., STMicroelectronics N.V., Coherent Corp., ROHM Co., Ltd., Infineon Technologies AG, onsemi, SK Siltron Co., Ltd., SICC Co., Ltd., TankeBlue Semiconductor Co., Ltd., Resonac Holdings Corporation, Mitsubishi Electric Corporation, Washington Mills Inc., CoorsTek Inc., Pacific Rundum Co., Ltd., Sumitomo Electric Industries Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ultra-High Purity Silicon Carbide Market Segmentation

By Grade

- 5N Purity

- 6N Purity

- 7N Purity

By Product Form

By Wafer Size

By Application

- Power Electronics

- High-Frequency Devices

- Optical Electronics

- Semiconductor Manufacturing Equipment

By Device Type

- Silicon Carbide MOSFETs

- Silicon Carbide Schottky Diodes

- Silicon Carbide JFETs

- Power Modules

By End-User Industry

- Automotive

- Industrial

- Energy and Power

- Aerospace and Defense

- Data Centers and Information Technology

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Ultra-High Purity Silicon Carbide Market

- Wolfspeed, Inc.

- STMicroelectronics N.V.

- Coherent Corp.

- ROHM Co., Ltd.

- Infineon Technologies AG

- onsemi

- SK Siltron Co., Ltd.

- SICC Co., Ltd.

- TankeBlue Semiconductor Co., Ltd.

- Resonac Holdings Corporation

- Mitsubishi Electric Corporation

- Washington Mills, Inc.

- CoorsTek, Inc.

- Pacific Rundum Co., Ltd.

- Sumitomo Electric Industries, Ltd.

*- List not Exhaustive