Market Snapshot - Hybrid Reinforcement Architectures are Reframing the Cost-Performance Frontier in Structural Composites

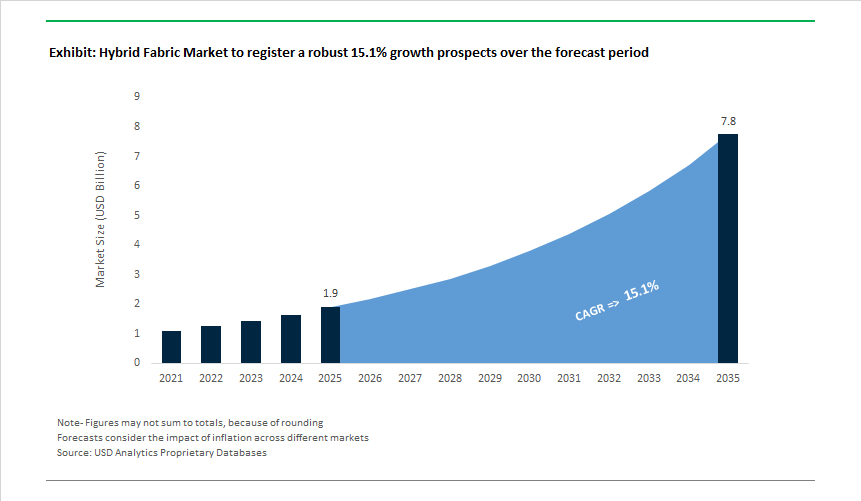

The Hybrid Fabric Market stands at USD 1,859.2 million in 2025 and is projected to reach USD 7,587.2 million by 2035, advancing at a 15.1% CAGR as composite designers increasingly optimize performance per dollar, rather than absolute material properties. Hybrid fabrics-engineered combinations of carbon, glass, and aramid fibers within a single textile architecture-are gaining traction because they allow OEMs to dial in stiffness, impact resistance, weight, and cost at the laminate level, something monolithic reinforcements cannot achieve.

Across automotive, aerospace, defence, wind energy, and high-performance sporting goods, hybrid fabrics are being adopted to replace metals and reduce structural mass by 40-60%, translating directly into fuel-economy gains, extended EV driving range, higher payload margins, and improved dynamic performance. Carbon/glass hybrids, in particular, have emerged as the commercial backbone of the market. By delivering roughly 65% of the stiffness of full-carbon laminates at a materially lower fiber cost, these hybrids enable OEMs to deploy lightweight composite structures at scale in applications where all-carbon solutions remain economically constrained. This cost-performance balance is increasingly specified in automotive structural panels, battery enclosures, and wind turbine components.

In defence and protection systems, glass/aramid hybrid fabrics address a different performance equation. Here, the combination of aramid’s high energy absorption and glass fiber’s stiffness supports improved ballistic resistance, controlled failure modes, and weight reduction in helmets, vehicle armor panels, and personnel protection systems. These hybrids are favored where impact tolerance and multi-hit performance are prioritized over maximum stiffness, reinforcing the role of hybridization as a design tool rather than a compromise.

From the manufacturing perspective, woven hybrid fabrics remain the dominant format, reflecting their superior drapability, fiber alignment control, and compatibility with established composite processes such as resin transfer molding, prepreg layup, and compression molding. Woven architectures also simplify preforming for complex geometries, reducing scrap rates and cycle times-an increasingly important consideration as hybrid fabrics move from niche to volume production. Over the forecast period, competitive advantage will accrue to suppliers that can offer repeatable hybrid architectures, tight fiber volume control, and application-specific weave designs, enabling OEMs to standardize performance while retaining flexibility across platforms.

Recent Market-Moving Events: Capacity Builds, Strategic Partnerships and Policy Incentives

Activity over the past two years confirms both demand acceleration and strategic positioning by legacy fiber and composite groups. In December 2024, Teijin Aramid unveiled a highly sustainable, high-tenacity aramid fiber that strengthens the material base for aramid hybrid fabrics used in ballistic and cut-resistant applications. During February 2025, the Indian government approved INR 10,683 crore (~US$1.3 billion) under the PLI scheme to stimulate domestic manufacture of man-made fibre (MMF) fabrics and technical textiles, explicitly supporting hybrid and high-performance composites-this policy is a material demand signal for regional fabric makers and converters.

Through June 2025 Hexcel deepened strategic supply ties with Kongsberg Defence & Aerospace and collaborated on the FLYING WHALES LCA60T airship project, expanding hybrid fabric uptake into defence and novel air mobility platforms. September 2025 was busy for Hexcel: it co-launched an advanced composite pressure vessel with HyPerComp (targeting Type-IV carbon overwrap hydrogen storage), and expanded its Americas aerospace distribution network to improve responsiveness for eVTOL and UAV suppliers. In November 2025 Hexcel also signalled internal optimisation by appointing an Interim CFO to sharpen financial strategy as the company scales hybrid prepreg and fabric output. Finally, December 2025 Toray Industries increased production capacity for carbon-based hybrid fabrics to meet surging defense and motorsports demand-confirming that both supply and finance moves are converging to meet multi-sector hybrid fabric demand.

Hybrid Fabric Market Trends and Opportunities

Customized Multi-Material Weaves for EV Battery Enclosures

Electric vehicle battery systems have become one of the most safety-critical structures in modern mobility, forcing material innovation beyond monolithic composites. Hybrid fabrics—particularly carbon–glass and carbon–aramid (Kevlar) architectures—are being engineered to deliver controlled failure behavior under crash and intrusion scenarios.

Independent studies published in May 2025 show that Hybrid Fiber-Reinforced Polymer (HFRP) laminates achieve up to 152.9% higher impact energy absorption than pure carbon composites. This performance stems from hybridized failure modes: brittle carbon fibers fracture to dissipate energy quickly, while glass or aramid fibers undergo progressive deformation, preventing sudden structural collapse. As a result, hybrid fabrics are increasingly specified for battery trays, underbody shields, and crash-relevant enclosure zones, where regulatory scrutiny around thermal runaway and mechanical penetration is intensifying.

Weight efficiency remains a parallel driver. According to U.S. Department of Energy, every 10% reduction in vehicle mass improves energy efficiency by 6–8%, a relationship OEMs now treat as a hard engineering lever rather than a theoretical benchmark. This has accelerated sourcing agreements between European automakers and Hexcel during 2024–2025 for hybrid-fabric battery housings and structural body panels.

Cost engineering is reinforcing adoption. Glass–carbon hybrid fabrics strategically place carbon fiber only in primary load paths, while glass fiber occupies secondary regions. This zoning approach preserves compressive stiffness and buckling resistance while reducing fabric density and raw-material exposure—an increasingly important factor amid carbon fiber price volatility and supply-chain regionalization.

Functional Yarns Embedded for In-Mold Electronics and Smart Structures

Hybrid fabrics are rapidly evolving into multifunctional platforms through the integration of conductive and sensing yarns directly into the textile architecture. This shift enables In-Mold Electronics (IME), where antennas, heaters, and sensors are molded into composite parts without secondary wiring or assembly.

Research published in August 2025 demonstrates that hybrid electronic yarns (e-yarns) embedded within structural fabrics can achieve temperature sensitivities approaching 2.96% per °C, enabling real-time thermal monitoring across complex composite geometries. These systems rely on metal-plated or silver-coated yarns combined with PTFE-based interconnections that survive resin infusion and molding without signal degradation.

Market data indicates that metal-plated conductive yarns—primarily silver and copper—are on track to represent around 40% of conductive textile mechanisms by 2026, reflecting their signal stability and compatibility with IME processes. This is particularly relevant in automotive interiors, battery housings, and aerospace panels, where embedded electronics reduce wiring mass and assembly complexity.

Structural Health Monitoring (SHM) is another fast-emerging application. European deployments, including sensing approaches pioneered by Eddytec, show that hybrid fabrics with integrated sensing layers can detect micro-cracks and delamination in carbon composite structures well before visible damage occurs. This capability is increasingly valued in aerospace and premium automotive platforms, where predictive maintenance directly impacts lifecycle cost and safety certification.

Hybrid Overwrap Fabrics for 700 bar Hydrogen Pressure Vessels

The global transition toward hydrogen mobility is creating a structurally demanding application for hybrid fabrics: Type IV Composite Overwrapped Pressure Vessels (COPVs) designed for 700 bar (70 MPa) storage. While carbon fiber remains the primary load-bearing element, hybridization with aramid or glass fibers is becoming standard practice to enhance impact resistance and durability.

As documented in February 2025, the industry-wide shift from 35 MPa to 70 MPa systems has exposed pure carbon overwraps to higher risks from impact damage and abrasion during handling and service. Hybrid fabrics mitigate these risks by introducing fibers with higher strain-to-failure and superior damage tolerance, improving survivability under drop, puncture, and cyclic loading conditions.

Liner interaction is another critical design variable. Polyamide (PA) liners, commonly used in Type IV vessels, can allow slow hydrogen permeation that degrades epoxy matrices over time. Hybrid overwrap fabrics with specialized barrier coatings are now being developed to act as secondary containment layers, extending certified service life toward 15–20 years, which aligns with hydrogen infrastructure depreciation models.

Policy-driven investment is reinforcing this opportunity. National export and industrial missions—such as India’s ₹25,060-crore Export Promotion Mission (2025–2031)—explicitly target advanced engineering goods, including high-pressure hydrogen storage systems, where hybrid fabrics are central to meeting international certification and safety standards.

Hybrid Spar-Cap Fabrics for Ultra-Long Offshore Wind Blades

Offshore wind turbines exceeding 10–15 MW are pushing blade lengths beyond 120 meters, creating structural challenges that neither pure glass nor pure carbon fabrics can solve economically. The spar cap, which carries the majority of bending loads, is emerging as a prime application for hybrid fabrics that balance stiffness, fatigue resistance, and cost.

In June 2025, Sinoma Science & Technology announced a $25.2 million investment in a new blade manufacturing facility in Uzbekistan, focused on advanced hybrid composites for next-generation turbines. These blades require materials that limit tip deflection while maintaining fatigue endurance over 25+ years in offshore environments.

Manufacturing efficiency is a decisive factor. Hybrid fabrics such as Magic Flow UD from SAERTEX enable resin infusion speeds up to 3.5× faster in thick laminates. Their architecture supports fiber volume fractions approaching 60% while providing integrated electrical conductivity for lightning protection—an essential requirement for offshore blades.

From an economic perspective, hybrid spar-cap architectures are reducing Levelized Cost of Energy (LCOE) by enabling lighter blades with longer service intervals. Processing speed improvements of ~15% translate directly into lower blade CAPEX and faster project commissioning, making hybrid fabrics a strategic enabler for large-scale offshore wind deployment.

Market Share Analysis: Hybrid Fabric Market

Market Share by Fiber Type: Carbon–Glass Hybrid Fabrics as the Cost-Optimized Structural Standard

Carbon–glass hybrid fabrics account for approximately 40% of the Hybrid Fabric Market because they resolve the industry’s central trade-off between mechanical performance and economic scalability. Pure carbon fiber delivers unmatched stiffness but remains cost-prohibitive for high-volume applications, while glass fiber alone lacks the modulus required for next-generation lightweight structures. Carbon–glass hybrids sit at a structurally optimal midpoint, delivering up to 80% of carbon’s stiffness at a 40–50% lower raw material cost, which has made them the default choice for manufacturers under cost and weight pressure. Beyond cost, their market leadership is reinforced by mechanical robustness: the integration of high-elongation glass fibers meaningfully improves strain-to-failure, reducing brittle fracture risk and improving damage tolerance under dynamic loads. This property is especially valued in transportation structures where impact behavior increasingly dictates material selection. From a manufacturing standpoint, carbon–glass hybrids also outperform pure carbon fabrics due to higher permeability, enabling resin flow rates that are 30–40% faster in vacuum infusion and RTM processes—an advantage that directly translates into shorter cycle times and higher plant utilization. Combined with precise areal weight control (down to ~150 g/m²), these hybrids allow engineers to localize carbon reinforcement only where stiffness is mission-critical, reinforcing their position as the most production-efficient and qualification-friendly fiber architecture in the hybrid fabric ecosystem.

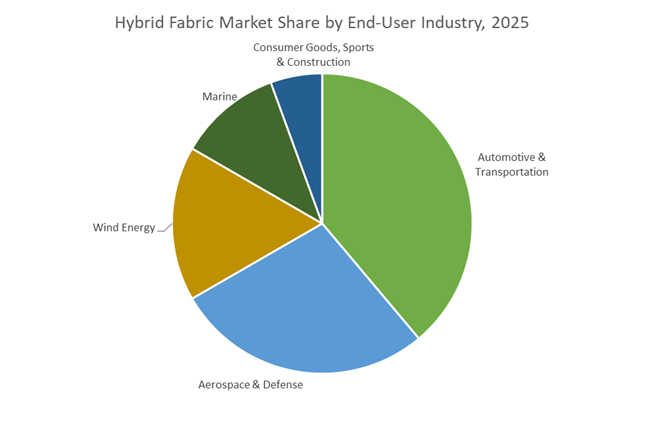

Market Share by Application: Automotive & Transportation as the Primary Demand Anchor

Automotive and transportation represent around 35% of total hybrid fabric consumption, positioning the sector as the market’s dominant volume driver rather than a niche adopter. The rise of electric vehicles has fundamentally altered material economics: battery packs add significant mass, forcing OEMs to pursue aggressive lightweighting strategies without absorbing the full cost of carbon fiber. Carbon–glass hybrid fabrics have emerged as the preferred solution, enabling 40–60% mass reduction versus high-strength steel in body-in-white and semi-structural components while remaining compatible with automotive cost targets. Their superior **energy absorption performance—up to 2× that of pure carbon in crash scenarios—**has accelerated adoption in safety-critical parts such as seat structures, door modules, and rear floor assemblies. In parallel, 2025 EV platforms operating on 800V electrical architectures have created demand for materials that combine EMI shielding, thermal stability, and impact resistance—capabilities that hybrids uniquely deliver through the complementary behavior of carbon and glass fibers. From a regulatory perspective, OEMs increasingly quantify lightweighting in emissions terms: each kilogram saved through hybrid fabric integration can eliminate roughly 20 kg of CO₂ over a vehicle’s lifetime, making these materials a direct compliance lever for Europe’s 2025 CO₂ reduction mandates. As a result, automotive applications continue to anchor hybrid fabric market share through a combination of cost discipline, safety performance, and regulatory alignment, reinforcing their structural dominance in the market.

Competitive Landscape: Established Carbon, Aramid and Integrated-Material Players Expanding Hybrid Portfolios

Major suppliers differentiate through vertical integration (fiber to fabric to prepreg), breadth of hybrid layups (carbon/glass, glass/aramid), certified supply to aerospace/defence, and partnerships to enter emerging mobility and hydrogen markets. Below is a concise market overview followed by H3 company entries.

Leading players are leveraging fibre ownership, advanced woven/NCT capability, and distribution networks to supply hybrid fabrics for high-rate aerospace, defence ballistic systems, eVTOL/UAV, hydrogen storage vessels, wind blades, and sporting goods.

Hexcel Corporation - Vertically Integrated Hybrid Fabric and Prepreg Leader For Aerospace, Defence and New-Mobility Applications

Hexcel controls fiber-to-prepreg value streams and markets the HexForce® line of woven and NCF hybrid fabrics (including ultra-light 1K reinforcement). Strategic partnerships in June 2025 (Kongsberg) and distribution expansion in September 2025 position Hexcel to supply high-rate aerospace and eVTOL programs; its co-developed pressure-vessel solution with HyPerComp (Sep 2025) shows hybrid fabrics moving into Type-IV hydrogen storage. Hexcel’s R&D on higher-modulus fibers (HexTow® IM9 improvements) and acoustic cores (for nacelle integration) strengthens its end-to-end composite system proposition.

Toray Industries - Global Carbon-Fiber Leader Expanding Hybrid Fabric Capacity To Serve Motorsports, Defence and Industrial Sectors

Toray’s Torayca® carbon leadership ensures both quality and volume security for hybrid fabric production. The December 2025 capacity expansion targets high-performance motorsports and defence applications where carbon/glass and carbon/aramid hybrids reduce mass while controlling cost. Toray’s material breadth (TETORON®, AMILAN®) enables functional hybrid textiles for heavy-duty industrial uses, and its collaborations with Hyundai and other OEMs signal cross-sector mobility strategies.

Teijin Limited - Aramid and Nanofiber Specialist Focusing On Ballistic Hybrid Fabrics and Wearable Functional Textiles

Teijin’s aramid expertise (Twaron®, Technora®) underpins glass/aramid hybrids for ballistic armour and vehicle protection. The company’s Dec 2024 sustainable high-tenacity aramid advances ballistic fabric performance and sustainability credentials. Teijin also leverages NANOFRONT® nanofiber tech to create hybrid wearable textiles with integrated sensing-opening markets in protective healthcare garments and advanced personnel systems.

Solvay S.A. - Resin and Thermoplastic Systems Partner Enabling Prepreg Hybrid Fabrics and Recyclable Thermoplastic Hybrids

Solvay supplies epoxy, PEKK and thermoplastic matrix systems used to produce hybrid prepregs and towpregs-enabling faster part production and end-of-life pathways through thermoplastic recyclability. Its strategic focus on thermoplastic composites supports high-volume automotive and space-structure use-cases where hybrid fabrics must be integrated into rapid manufacturing cycles and circular material flows.

SGL Carbon - Textile Systems and NCT Specialist Delivering Tailored Hybrid Layups For High-Stress and Space Heritage Applications

SGL Carbon’s SIGRATEX® portfolio (woven, UD, multiaxial) and non-crimp textile capability (NCT) allow precise fiber alignment for load-path-optimised hybrid layups used in structural, defence and space programs. With a history supplying ablative carbon for rocket nozzles, SGL combines traceable carbon fiber supply and automation-readiness (RTM/VARTM support) to serve high-stress hybrid components and automated production environments.

The United States hybrid fabric market remains the global reference point for carbon/aramid and glass/carbon hybrid reinforcements, with 2025 defined by defense modernization and tariff-driven nearshoring. The establishment of the U.S. Investment Accelerator within the Department of Commerce in March 2025 is coordinating $100+ billion in high-tech investments, accelerating domestic capability across advanced polymer substrates, hybrid textiles, and composite reinforcements used in AI accelerators and aerospace structures. This policy alignment compresses qualification timelines for hybrid fabrics specified in defense and space platforms.

Trade dynamics amplified localization. New U.S. tariffs on imported aramid and carbon fiber precursors in 2025 catalyzed rapid expansion of domestic weaving and finishing. Hexcel Corporation and Plascore Inc. reported record backlogs tied to U.S.-sourced aerospace and defense programs. Late-2025 disclosures from defense contractors also pointed to elevated procurement of HexWeb®-reinforced hybrid panels, supporting the ~$3.68 billion aircraft seals and structural components sub-sector and reinforcing the U.S. as the premium market for flight-qualified hybrid fabrics.

China: Technical Textile Upgrade, Circularity & Export Governance

China’s hybrid fabric market is transitioning from commodity textiles to high-value technical reinforcements, embedded in the country’s High-Quality Development framework. Data released by the National Bureau of Statistics (NBS) in October 2025 showed a divergence: while general textile output rose 2.2%, chemical fibers and technical fabrics expanded 5.6% over the first three quarters—signaling capital migration into advanced hybrid blends.

Circularity is becoming a competitive lever. In early 2025, BASF commissioned its first commercial loopamid® facility in Shanghai, enabling textile-to-textile recycling of Polyamide 6—even in dyed, elastomer-containing hybrid fabrics—back to high-purity monomers. Export governance tightened in November 2025 as MOFCOM introduced monitoring for high-performance fiber precursors, prioritizing domestic access for EV battery housings and COMAC aerospace programs. China’s strategy blends circular manufacturing with supply control to secure downstream hybrid fabric availability.

Germany: EPR Mandates Drive Bio-Hybrid and Thermoplastic Reinforcements

Germany is setting the global benchmark for sustainable hybrid fabrics, leveraging the EU’s Circular Economy Action Plan and newly adopted Extended Producer Responsibility (EPR) rules. Following the European Parliament vote on September 9, 2025, German producers began implementing EPR schemes that internalize collection and recycling costs for hybrid textiles—forcing rapid redesign toward recyclable thermoplastic and bio-hybrid structures.

Innovation was on display at K 2025, where German engineering firms unveiled carbon/basalt hybrid yarns delivering ~40% cost reduction versus pure carbon while maintaining fire-safety compliance for European rail interiors. Automotive OEMs further validated the approach in late 2025 with pilots of bio-attributed hybrid interior panels, combining natural fibers with recycled high-performance nylon to cut cradle-to-gate emissions—positioning Germany as the nexus of regulatory compliance and hybrid material innovation.

India: Bharat Tex Momentum, PLI Scale-Up & Mega Textile Parks

India is rapidly ascending the hybrid fabric value chain through policy-backed scale and infrastructure build-out. Bharat Tex 2025 (February, New Delhi) showcased the country’s “Farm to Fibre” integration, as the government reported ₹3 lakh crore in textile exports with a target of ₹9 lakh crore by 2030. This growth trajectory is steering capital toward glass/carbon and natural/synthetic hybrid fabrics for industrial and protective applications.

Under the ₹10,683 crore PLI scheme, the Ministry of Textiles approved funding via the GREAT initiative for startups developing glass/carbon hybrid fabrics for medical and industrial PPE. Capacity acceleration is structural: seven PM MITRA Mega Textile Parks—with expected $10 billion investment—are providing plug-and-play ecosystems for hybrid weavers and composite manufacturers. India’s model couples export ambition with domestic scale, strengthening its position as a global technical textiles hub.

Japan: 6G-Ready Hybrid Fabrics and Ultra-Gap Integration

Japan’s hybrid fabric strategy centers on ultra-gap technologies that embed electronics into textile architectures. In 2025, Japanese electronics and textile firms piloted carbon/glass hybrid EMI-shielding fabrics for 6G signal reflectors, balancing mechanical stiffness with precisely tuned dielectric properties at terahertz frequencies—a requirement for smart-city infrastructure.

Policy support under the GX 2040 Vision (Cabinet-approved January 2025) is accelerating bio-based hybrid yarns for Advanced Air Mobility (eVTOL), where extreme lightweighting directly translates to battery endurance. Cross-border collaboration adds depth: in December 2025, Japan and India advanced joint development of basalt-based hybrid textiles for high-speed rail and industrial filtration, reinforcing Japan’s leadership in electronics-integrated hybrid fabrics.

South Korea: Semiconductor Packaging Clusters and High-Temperature Hybrids

South Korea is integrating hybrid fabrics into its AI-driven semiconductor ecosystem, treating textiles as functional components in packaging and thermal management. In December 2025, the government announced ₩260.1 billion for compound semiconductors and ₩360.6 billion for advanced packaging by 2031—explicitly including polyimide-hybrid fabrics as dielectric and structural layers in high-density chip stacking.

The Gwangju Southern Semiconductor Innovation Belt is anchoring this push, focusing on packaging hubs that deploy high-temperature hybrid fabrics for AI data centers. Concurrently, Korean composite firms expanded capacity for carbon-basalt and glass-basalt hybrid yarns in late 2025, targeting the global aerospace market’s demand for fire-resistant, lightweight interior structures—cementing South Korea’s role at the intersection of materials science and semiconductor packaging.

2025 Strategic Matrix: Hybrid Fabric Market by Country

Hybrid Fabric Market Matrix

|

Country

|

Primary Market Driver

|

2025 Strategic Milestone

|

Hybrid Fabric Focus

|

|

United States

|

Defense & nearshoring

|

U.S. Investment Accelerator

|

Carbon/aramid aerospace reinforcements

|

|

China

|

Circular manufacturing

|

loopamid® Shanghai startup

|

Recycled PA6 hybrid blends

|

|

Germany

|

Regulatory compliance

|

EU EPR rules implementation

|

Carbon/basalt & bio-hybrids

|

|

India

|

Industrial scaling

|

Bharat Tex 2025; PLI expansion

|

Glass/carbon technical textiles

|

|

Japan

|

6G & AAM (eVTOL)

|

GX 2040 Vision

|

High-frequency dielectric hybrids

|

|

South Korea

|

AI chip packaging

|

Gwangju semiconductor hub

|

Polyimide-reinforced hybrids

|

Hybrid Fabric Market Report Scope

Hybrid Fabric Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1859.2 Million

|

|

Market Size (2035)

|

$7587.2 Million

|

|

Market Growth Rate

|

15.1%

|

|

Segments

|

By Fiber Combination (Carbon-Glass, Carbon-Aramid, Aramid-Glass, Carbon-UHMWPE, Natural Fiber Hybrids, Thermoplastic Hybrids), By Form (Composite Form, Non-Composite Form), By Weaving Technology (Woven Fabrics, Non-Crimp Fabrics, Multiaxial Fabrics, Braided Structures, 3D Orthogonal Weaves), By Application (Structural Components, Interior & Trim, Protective Gear, Sporting Goods, Industrial & Marine), By End-User Industry (Aerospace & Defense, Automotive & Transportation, Wind Energy, Marine, Consumer Goods & Sports, Building & Construction)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Hexcel Corporation, Toray Industries Inc., SGL Carbon SE, Teijin Limited, Solvay / Syensqo, Gurit Holding AG, DSM / Avient Corporation, Owens Corning, BGF Industries Inc., Textum OPCO LLC, Exel Composites Plc, Taiyuan Heavy Industry Co. Ltd., Arrow Technical Textiles Pvt. Ltd., Isomatex S.A., Hacotech GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Hybrid Fabric Market Segmentation

By Fiber Combination

- Carbon-Glass Hybrid

- Carbon-Aramid (Kevlar) Hybrid

- Aramid-Glass Hybrid

- Carbon-UHMWPE Hybrid

- Natural Fiber Hybrids

- Thermoplastic Hybrids

By Form

- Composite Form

- Non-Composite Form

By Weaving Technology

- Woven Fabrics

- Non-Crimp Fabrics

- Multiaxial Fabrics

- Braided Structures

- 3D Orthogonal Weaves

By Application

- Structural Components

- Interior & Trim

- Protective Gear

- Sporting Goods

- Industrial & Marine

By End-User Industry

- Aerospace & Defense

- Automotive & Transportation

- Wind Energy

- Marine

- Consumer Goods & Sports

- Building & Construction

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Hybrid Fabric Market

- Hexcel Corporation

- Toray Industries, Inc.

- SGL Carbon SE

- Teijin Limited

- Solvay S.A. / Syensqo

- Gurit Holding AG

- Royal DSM N.V. / Avient Corporation

- Owens Corning

- BGF Industries, Inc.

- Textum OPCO, LLC

- Exel Composites Plc

- Taiyuan Heavy Industry Co., Ltd.

- Arrow Technical Textiles Pvt. Ltd.

- Isomatex S.A.

- Hacotech GmbH

*- List not Exhaustive