Ballistic Protection Market Overview Driven by Soldier Modernization, NIJ 0101.07 Adoption & Lightweight Armor Innovations

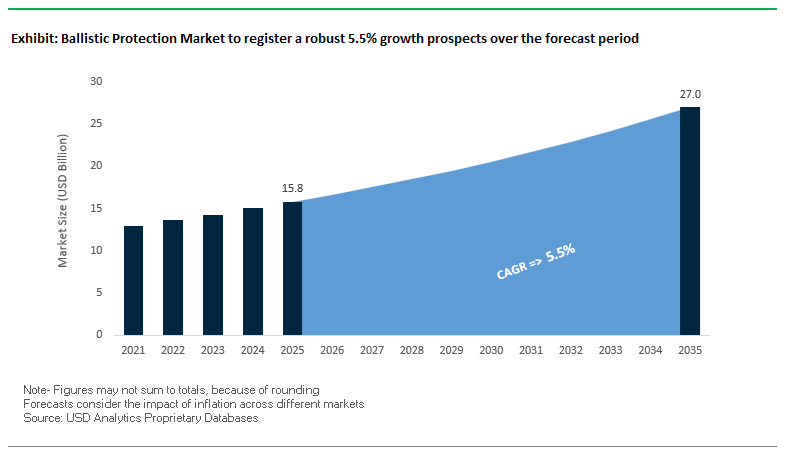

The Global Ballistic Protection Market, valued at USD 15.8 billion in 2025 and projected to reach USD 27 billion by 2035 at a 5.5% CAGR, is entering a decisive modernization phase driven by defense mobility requirements, next-generation material technologies, and large-scale regulatory alignment with NIJ 0101.07 and NIJ 0123.00 ballistic standards. As military forces shift toward lighter, modular, and multi-hit–capable armor platforms, demand is accelerating for aramid-based soft armor, ultra-high-molecular-weight polyethylene (UHMWPE) unidirectional laminates, and high-purity ceramic strike faces engineered for repeated high-velocity threat defeat. Procurement teams in defense and law enforcement now prioritize armor solutions that deliver weight reduction, operational endurance, improved ergonomics, and superior ballistic efficiency, as modern conflict environments increasingly emphasize maneuverability and sustained protection.

The transformation is reinforced by the geopolitical climate, where NATO members meeting or exceeding the 2% GDP defense-spending benchmark are initiating multi-year acquisition cycles spanning soft armor vests, hard plates, helmets, transparent armor, and vehicle survivability kits. Vehicle OEMs and armor integrators are advancing to thinner transparent armor laminates that preserve ballistic rating while reducing platform mass—critical for fuel efficiency, mobility, and payload optimization. Simultaneously, soldier lethality programs demand armor plates with enhanced multi-hit survivability, optimized backface deformation (BFD), and compatibility with emerging soldier-wearable technologies.

Key Performance and Procurement Insights

- Next-generation soft armor systems using Kevlar® EXO™ and UHMWPE UD laminates deliver 20% weight reduction without sacrificing NIJ 0101.07 threat protection.

- Advanced ceramic strike faces now support up to 8 multi-hit impacts within a 4-inch radius, aligning with the needs of urban and near-peer conflict scenarios.

- NATO defense budgets surpassing 2% GDP are accelerating procurement of body armor, helmets, and vehicle armor kits, creating predictable long-horizon demand.

- Transparent ballistic armor continues to thin—achieving 15% thickness reduction—improving vehicle agility, fuel efficiency, and payload capability.

- Global transition to NIJ 0101.07 / NIJ 0123.00 standards by late 2025 is triggering mandatory armor refresh cycles across law enforcement and military organizations.

Market Analysis: Defense Contracts, Advanced Fiber Launches & Multi-Hit Ceramic Innovations

The Ballistic Protection Market has seen a surge in strategic contracts, material breakthroughs, and modernization programs that directly impact procurement and supply chain priorities. In November 2025, BAE Systems secured a USD 390M contract modification from the U.S. Army to upgrade Bradley Fighting Vehicles to the A4 configuration-requiring integration of next-generation vehicle ballistic protection, including ceramic composites, transparent armor, and structural survivability modules. This reflects a long-term trend of armored platform recapitalization across NATO and allied regions.

In October 2025, DuPont’s Kevlar® EXO™ won the prestigious Edison Award, reinforcing its role as the most advanced soft armor aramid available, offering significantly improved durability and flexibility. By September 2025, DuPont confirmed commercial availability of Kevlar® EXO™, durability-tested at 10× NIJ conditioning standards, setting a new benchmark for longevity and reliability in soft armor. Hard armor innovation accelerated in July 2025 when Avient (Dyneema®) launched HB330/HB332 UD materials, enabling up to 45% weight reduction in ballistic plates while boosting energy absorption for improved stopping power. That same month, Safe Pro Group won a regional Indo-Asia Pacific contract, demonstrating escalating demand for tactical and EOD protective systems in high-conflict zones.

Defense procurement momentum continued earlier in the cycle. In April 2024, the U.S. DoD awarded Safariland a USD 190M soft armor contract, signaling a system-wide refresh in anticipation of NIJ 0101.07 compliance. Similarly, in March 2024, Point Blank Enterprises secured a USD 215M contract for next-generation modular body armor vests, prioritizing mobility and multi-material integration. Head protection modernization advanced in February 2024, when Avon Protection plc received a USD 204M IHPS contract, confirming sustained multi-year defense investment in integrated soldier protection systems. Collectively, these developments highlight a market driven by innovation, survivability requirements, and regulatory updates that demand continuous material advancements.

Key Trends Redefining the Ballistic Protection Market

Trend 1: Rapid Transition Toward Lightweight, Multi-Threat Hard Armor Plates Driven by Operational Mobility Demands

Global defense agencies and tactical police units are accelerating the replacement of heavy steel and monolithic ceramic plates with lightweight ceramic-faced composite armor to reduce soldier load and enhance mobility. Operational mobility has become a core procurement criterion, especially as modern infantry increasingly operate in urban, dismounted, and high-tempo environments. Next-generation Level III+ ceramic composite plates, weighing as little as 4.4 pounds (≈2 kg) for a standard 10×12" configuration, deliver up to 35% weight reduction compared to steel equivalents while offering superior multi-hit protection against enhanced rifle threats, including 5.56 mm M855 “Green Tip” rounds.

Ceramic Matrix Composites (CMCs) sit at the center of this shift. Their layered design enables ceramic strike faces to shatter and erode incoming projectiles, while the UHMWPE backing layer absorbs residual kinetic energy and prevents catastrophic backface deformation. Unlike steel plates—which deform, cause severe spall, and struggle with multi-hit rifle performance—CMC-based plates maintain protection across repeated impacts and reduce injury risk.

Military load-reduction initiatives strengthen this trend. Programs targeting soldier combat loads below 100 pounds prioritize lighter hard armor plates, recognizing their disproportionate contribution to fatigue, musculoskeletal injuries, and reduced mission endurance. As protection levels increase, lightweight ceramic composites have become the only viable pathway to maintain operational effectiveness without compromising survivability.

Trend 2: Civilian and Law Enforcement Adoption of Concealable, Multi-Hit Soft Armor Accelerates

The rising frequency of active shooter events and expanding demand for executive protection have triggered a significant commercial shift toward ultra-lightweight, concealable soft armor systems. Unlike military plates, this segment prioritizes comfort, flexibility, and discreet wearability—while still meeting rigorous NIJ Level IIIA performance requirements. Modern UHMWPE-based soft armor panels achieve protection against high-energy handgun threats (up to .44 Magnum) at weights as low as 0.6 pounds per square foot, allowing police officers, security personnel, and VIP protection teams to wear full vests for 8–12 hour shifts without mobility degradation.

Aramid fibers remain essential for multi-hit scenarios, as their woven structures maintain integrity even after multiple impacts in localized zones—an increasingly important requirement for urban security forces confronting close-range multi-shot events. Both UHMWPE and aramid innovations focus heavily on Backface Deformation (BFD) control, maintaining indentation depths below the 44 mm threshold required by NIJ standards to prevent blunt trauma injuries. This evolution of soft armor design reflects a shift toward ballistic systems that offer high threat protection without sacrificing comfort or concealability.

High-Value Opportunities Emerging in the Ballistic Protection Market

Opportunity 1: Additive Manufacturing for Custom-Fitted, Topologically Optimized Plate Carriers and Armor Components

Additive Manufacturing (AM) is emerging as a transformational opportunity for the ballistic protection industry, enabling custom-fitted protective systems, structural optimization, and on-demand field-level fabrication. Research shows that body-scan-driven AM geometries achieve dimensional accuracies of under 1 mm, allowing plate carriers to distribute load more evenly and reduce chronic strain on the neck, shoulders, and lower back. This ergonomic advantage is highly valued by military and tactical units that experience long-duration load-bearing missions.

AM also enables rapid prototyping and mission-specific customization, eliminating the tooling cost barriers associated with conventional armor manufacturing. Units can fabricate tailored hard-armor components, integrated attachments, or environmentally adaptive plates as needed—significantly reducing logistical complexity for specialized teams.

Furthermore, AM design freedom allows for functional integration, embedding ventilation channels, cable-routing pathways, and shock-damping structures directly into the carrier shell. This reduces component count, enhances thermal management, and addresses one of the most common field complaints: overheating during extended operations. As AM materials advance toward higher-strength polymers and metal-polymer hybrids, this opportunity is positioned to become a major competitive differentiator for next-generation ballistic systems.

Opportunity 2: Transparent Armor Technologies for the Expanding VIP and Commercial Vehicle Retrofit Market

Rising security concerns among commercial clients, VIPs, and high-net-worth individuals are fueling rapid growth in aftermarket vehicle armoring—particularly involving transparent armor systems that replicate factory aesthetics while delivering robust ballistic protection. The global armored vehicle retrofit sector is now a multi-billion-dollar segment, driven by demand for lightweight, discreet, and technologically advanced glazing systems.

Traditional bullet-resistant glass (BRG) poses significant drawbacks: high weight, thick profiles, and degraded vehicle handling. Advanced transparent ceramics and laminated polymer–ceramic configurations solve these issues, reducing window assembly weight by up to 50% while maintaining NIJ Level III or higher ballistic resistance. This allows vehicles to retain near-stock performance characteristics—critical for VIP mobility, inconspicuous protection, and maneuverability.

Next-generation transparent armor is incorporating sophisticated situational awareness features, including See-Through Armor (STA) systems that merge optical ceramics with integrated imaging and display technologies to deliver 360° real-time visibility. This transforms transparent armor from passive protection into an active tactical tool favored by executive security and surveillance vehicles. As retrofit markets expand across regions facing heightened urban insecurity, advanced transparent armor systems represent one of the most commercially scalable opportunities in ballistic protection.

Ballistic Protection Market Share Analysis

Market Share by Product Category: Personal Armor Leads with 40.2% Share

Personal Armor dominates the Ballistic Protection Market with a 40.2% share in 2025, reflecting its position as the highest-volume and most frequently replaced product category within global defense, law enforcement, and security ecosystems. Its leadership is driven by the continuous need for lightweight, high-performance body armor systems that meet evolving ballistic certification standards and offer improved ergonomics, multi-hit resilience, and enhanced protection against emerging ammunition types. The consumable nature of personal armor—characterized by routine replacement cycles, wear deterioration, and mandatory certification renewals—creates persistent baseline demand across military forces and police agencies worldwide. At the same time, the broader product landscape highlights rising technological complexity: vehicle armor requires multi-material integration to counter blended threats (ballistic, IED, fragmentation); aircraft, marine, and infrastructure armor are gaining traction as governments invest in fortified public spaces and critical assets; and helmets and shield systems continue evolving with advanced composites and hybrid materials. This segmentation shows a market built around protecting the soldier first while scaling advanced protection technologies across mobile platforms and built environments.

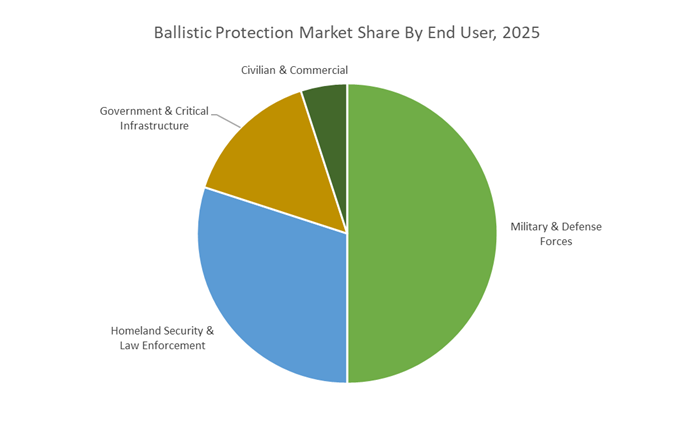

Market Share by End User: Military & Defense Forces Lead with 47.9% Share

Military & Defense Forces command the largest end-user share at 47.9% in 2025, solidifying their role as both the technology accelerator and volume anchor of the ballistic protection industry. Their dominance is driven by large-scale procurement programs, modernization initiatives, and the strategic imperative to equip soldiers with next-generation ballistic, blast, and fragmentation protection across personal armor, helmets, vehicle platforms, and fortified installations. Defense-sector demand is also shaped by geopolitical tensions, asymmetrical warfare, and battlefield digitization—all of which elevate the need for lighter, stronger, and more adaptive armor systems. Beyond the military segment, the market is reinforced by homeland security and law enforcement agencies, which contribute stable annual demand due to mandatory replacement cycles and certification expiry of soft body armor; government and critical infrastructure, which increasingly adopt transparent armor, blast-proof materials, and fortified architectural systems; and civilian and commercial segments, where demand remains small but highly event-driven. Combined, these end-user dynamics illustrate a market where defense procurement sets the innovation pace while law enforcement and infrastructure segments provide recurring, resilient demand.

Country Analysis: Global Ballistic Protection Market Innovation Hubs

United States: Transforming Soldier Survivability Through Lightweight Armor Programs and High-Impact RDT&E Funding

The United States remains the global epicenter of ballistic protection innovation, driven by unmatched defense spending, modernization programs, and the rapid adoption of next-generation soldier protection systems. In 2025, the U.S. Army awarded a landmark $416 million LSAPI contract (running through 2032) to Hardwire LLC and Leading Technology Composites for the Lares Small Arms Protective Inserts, engineered to be 30% lighter than previous standard-issue plates. This weight reduction directly reduces soldier fatigue, boosts battlefield mobility, and enhances survivability against rifle threats, marking a major leap in lightweight ceramic-composite armor engineering.

Head protection modernization is accelerating as well. In February 2024, Avon Protection plc secured a $204 million IHPS Direct OEM contract for next-generation combat helmets and soft armor vests, reinforcing the shift toward integrated head-and-torso protection systems with improved fragmentation resistance and enhanced blunt-impact mitigation. Meanwhile, U.S. law enforcement is transitioning to the new NIJ 0101.07 ballistic standard, driving nationwide replacement cycles for both handgun-rated soft armor and rifle-rated hard armor. Complementing procurement, the FY2025 President's Budget injects substantial funding into RDT&E and Procurement, supporting platforms like the Armored Multi-Purpose Vehicle (AMPV) that rely on cutting-edge ceramic, composite, and metallic armor systems. This ecosystem of procurement and innovation positions the U.S. as the leading driver of next-generation ballistic materials science.

European Union (Germany/France/Poland): EDF-Funded Ballistic Material Development and Coordinated Defense Procurement Acceleration

The European Union is rapidly scaling its ballistic protection materials industry through joint procurement mechanisms and unprecedented defense spending growth. The European Defence Fund (EDF) has committed €5.4 billion (2021–2027) to collaborative defense R&D, including advanced ballistic ceramics, high-performance fibers, soldier systems, and modular armor platforms. In May 2025, the EU launched the SAFE Loan Instrument offering up to €150 billion in competitively priced loans to member states, accelerating large-scale procurement of personal protective equipment (PPE), helmets, ballistic vests, and infantry support systems—critical amid rising geopolitical tensions.

Defense R&D is also expanding rapidly. According to EDA data, European defense R&D expenditure will rise to €17 billion in 2025, fueling research into novel armor fibers, next-generation ceramic strike faces, hybrid composite armor structures, and ultralight ballistic plates. At the national level, Poland is conducting multiple tenders for Type 2 soft bulletproof vests and helmets, reflecting increased civilian and population protection priorities. Germany, through Rheinmetall and its integrated platform strategy, continues advancing lightweight vehicle protection systems, modular armor packages for next-generation land systems, and structural ceramic armor solutions. Together, these efforts position the EU as a rapidly growing competitive hub for both soldier and vehicle ballistic protection materials.

China: Indigenous Ballistic Materials and PLA Modernization Driving Domestic UHMWPE and Ceramic Armor Development

China's ballistic protection market is expanding aggressively under the People’s Liberation Army (PLA) modernization roadmap, which aims to achieve full modernization by 2035, with intermediate goals tied to mechanization, informatization, and intelligentisation by 2027. These milestones create sustained demand for indigenous ballistic materials, including advanced UHMWPE fibers, ceramic matrix composites, and hybrid armor systems.

Chinese research institutes and defense manufacturers are scaling domestic capabilities in high-strength polyethylene fibers, advanced alumina and silicon-carbide armor tiles, and composite backing materials to reduce reliance on imported ballistic technologies. Through Civil-Military Integration, Beijing is aligning industrial ceramics, fiber manufacturing, and advanced polymer industries to support ballistic protection science, reinforcing strategic materials independence. This integrated approach ensures that ballistic armor for soldier systems, security forces, armored vehicles, and naval platforms can be designed, produced, and improved entirely within China’s domestic industrial ecosystem.

India: Aatmanirbhar Bharat Accelerating Domestic Ballistic Protection Manufacturing and Procurement Initiatives

India is rapidly strengthening its position in the global ballistic protection market through the Aatmanirbharta (self-reliance) initiative, which prioritizes indigenous production of bulletproof jackets, helmets, and advanced protective equipment. The Ministry of Defence has set an ambitious INR 1.75 Lakh Cr (~$21 billion) defense manufacturing target for 2025, explicitly including ballistic protection systems and specialized soldier-wearable gear. This initiative is driving major private-sector participation and boosting innovation in lightweight ceramic plates, aramid-based vests, and multi-hit armor systems.

Procurement momentum is rising. In December 2025, the Border Security Force (BSF) issued tenders for Bomb Blankets under MHA QR (V2) specifications, reflecting demand for advanced explosive mitigation materials. India’s establishment of Defense Industrial Corridors, particularly in Uttar Pradesh, supports ballistic protection manufacturers with test infrastructure, incentives, and cluster-based supply chain ecosystems. These developments position India as an emerging production hub for scalable, cost-effective, and increasingly high-performance ballistic armor solutions.

Taiwan: Strategic Ceramic Armor Procurement and ESAPI-Level Rifle Threat Protection

Taiwan is prioritizing advanced ceramic armor procurement to strengthen its defensive posture amid rising regional security pressures. Between 2028 and 2029, Taiwan’s military will acquire 48,000 boron carbide ballistic plates, specifically engineered for Level IV/ESAPI-class protection capable of stopping 7.62mm armor-piercing rounds. Boron carbide—one of the world’s lightest and hardest ceramic materials—provides exceptional ballistic performance with reduced soldier load, making it ideal for Taiwan’s mobility-focused defense requirements.

Taiwan’s earlier procurement activity reinforces this commitment: in February 2025, the Ministry of National Defense signed a NT$1.6 billion contract for 160,000 ceramic plates, signaling ongoing investment in lightweight soldier protection. With a clear focus on ESAPI-grade materials and supply chain reinforcement, Taiwan is rapidly enhancing its soldier survivability infrastructure through precision-engineered ceramic strike faces and advanced composite backing layers.

Competitive Landscape: Global Leaders Advancing Aramid, UHMWPE & Ceramic Armor Capabilities

The Ballistic Protection Market is dominated by companies with deep expertise in advanced fibers, ceramics, composite armor, and soldier survivability systems. Competitive differentiation is now rooted in multi-hit performance, lightweighting, flexibility, and system-level integration across soft armor, hard plates, transparent armor, and head protection. Suppliers are aligning product innovations with modernization cycles and stringent NIJ 0101.07 demands.

DuPont de Nemours, Inc. - Setting New Benchmarks in Aramid Soft Armor Technologies

DuPont remains the global leader in aramid fibers through its Kevlar® and Tensylon® portfolio, with Kevlar® EXO™ marking a major technological shift in soft armor materials. The 2024–2025 strategic push centers on enhancing soldier comfort, flexibility, and durability while meeting NIJ 0101.07 standards. Kevlar® EXO™ delivers ballistic performance comparable to UHMWPE while offering inherent flame resistance-critical for military and tactical operations. Its multi-mission adaptability ensures high adoption across law enforcement and defense agencies worldwide.

Avient Corporation (Dyneema®) - Ultra-Lightweight UHMWPE for Hard & Soft Armor Systems

Avient is the leading manufacturer of Dyneema® UHMWPE fibers, the backbone of high-performance lightweight armor. The launch of Dyneema HB330/HB332 in July 2025 provides a breakthrough in hard ballistic plates, enabling up to 45% weight reduction without compromising stopping power. Avient’s Dyneema® SB301 soft armor solutions also reduce vest weight by 20% while incorporating bio-based feedstocks that lower carbon footprint by up to 90% compared to standard HMPE. This positions Avient as the sustainability and performance leader in UHMWPE ballistic materials.

3M Company - Advanced Ceramic Strike Faces for Multi-Hit Rifle Protection

3M, through its Ceradyne division, delivers specialized Boron Carbide (B4C) and Silicon Carbide (SiC) ceramic materials used in high-end hard armor plates. Its IMP/ACT series integrates a stainless-steel crack arrestor to control fracturing and enhance multi-hit survivability-crucial for NIJ Level IV and military-grade plates. 3M’s strength lies in engineered ceramic-polymer integration for vehicle armor, protective shields, and rifle-rated plates requiring extreme hardness and lightweight performance.

BAE Systems Plc - Platform-Level Vehicle Protection & Survivability Systems

BAE Systems leads in vehicle ballistic protection, leveraging decades of defense engineering to support armored platforms globally. Its USD 390M Bradley A4 upgrade contract (November 2025) underscores its central role in U.S. armored vehicle modernization, integrating advanced armor kits, underbelly protection, and transparent armor. BAE’s extensive U.S. industrial network, including collaboration with Red River Army Depot, enables high-volume, mission-critical vehicle survivability upgrades.

Point Blank Enterprises - High-Volume Producer of Modular Body Armor Systems

Point Blank Enterprises is one of the largest manufacturers of integrated body armor for military and law enforcement forces. Its USD 215M U.S. Army contract (March 2024) for modular body armor systems reinforces its leadership in scalable, next-generation soldier protection. Point Blank integrates aramid, UHMWPE, and hybrid composites to deliver vests and plates meeting NIJ IIA–IV requirements, maintaining strong adoption across global tactical and defense agencies.

Avon Protection plc - Integrated Head & Body Protection for Soldier Survivability

Avon Protection specializes in head protection systems and respiratory gear, forming a key component of full-spectrum soldier survivability. The USD 204M IHPS contract (February 2024) highlights its importance in next-generation helmet systems that integrate ballistic protection, impact resistance, and mounting solutions for optics and communications. Avon’s multi-year delivery orders ensure continuous supply chain readiness for modern military programs.

Ballistic Protection Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$15.8 Billion

|

|

Market Size (2035)

|

$27 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Product Category (Personal Armor, Vehicle Armor, Aircraft Armor, Naval/Marine Armor, Infrastructure Protection), By Material Type (Aramid Fibers, UHMWPE, Ceramics, Hybrid Composites, Metal Alloys, Fiberglass/Composites), By Protection Level (NIJ Levels, STANAG, VPAM), By End User (Military & Defense Forces, Homeland Security & Law Enforcement, Government & Critical Infrastructure, Civilian), By Application Type (Soft Ballistic Protection, Hard Ballistic Protection, Blast/Fragment Protection, Multi-Threat Armor)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Avient Corporation, DuPont de Nemours Inc., Honeywell International Inc., Cadre Holdings Inc., BAE Systems plc, Avon Protection plc, Teijin Limited, Point Blank Enterprises Inc., Hardwire LLC, TenCate Advanced Composites, Rheinmetall AG, Armor Express, Plasan Sasa Ltd., CoorsTek Inc., DSM

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ballistic Protection Market Segmentation

By Product Category

- Personal Armor

- Vehicle Armor

- Aircraft Armor

- Naval / Marine Armor

- Infrastructure Protection

By Material Type

- Aramid Fibers

- Ultra-High-Molecular-Weight Polyethylene

- Ceramics

- Hybrid Composites

- Metal Alloys

- Fiberglass / Composites

By Protection Level

- NIJ Level IIA, II, IIIA

- NIJ Level III

- NIJ Level IV

- STANAG

- VPAM

By End User

- Military & Defense Forces

- Homeland Security & Law Enforcement

- Government & Critical Infrastructure

- Civilian

By Application Type

- Soft Ballistic Protection

- Hard Ballistic Protection

- Blast / Fragment Protection

- Multi-Threat Armor

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Ballistic Protection Market

- Avient Corporation

- DuPont de Nemours, Inc.

- Honeywell International Inc.

- Cadre Holdings Inc.

- BAE Systems plc

- Avon Protection plc

- Teijin Limited

- Point Blank Enterprises Inc.

- Hardwire LLC

- Tencate Advanced Composites

- Rheinmetall AG

- Armor Express

- Plasan Sasa Ltd.

- CoorsTek, Inc.

- DSM

*- List not Exhaustive