Ceramic Armor Market Overview: Lightweight Boron Carbide, Hybrid Composites & High-Mobility Protection Systems Driving Global Adoption

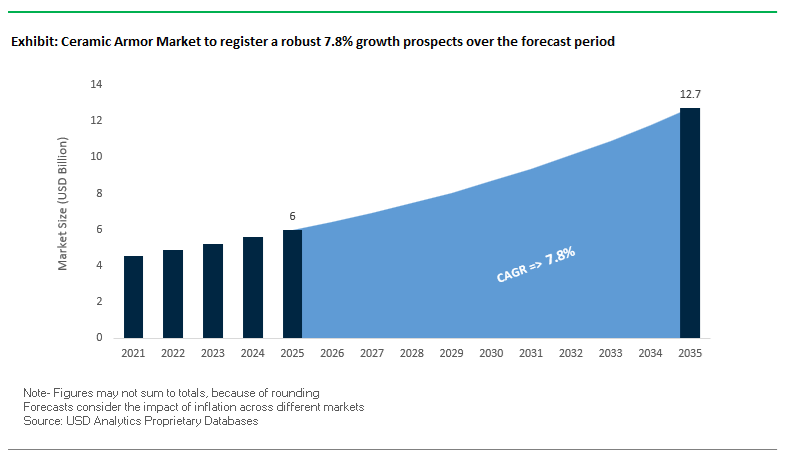

The Ceramic Armor Market, valued at USD 6.0 billion in 2025 and projected to reach USD 12.7 billion by 2035 at a strong 7.8% CAGR, is accelerating toward a new era of ultra-lightweight ballistic protection, multi-hit survivability, and advanced hybrid armor architectures. As global militaries prioritize operational mobility and soldier endurance, demand is rising sharply for high-performance Silicon Carbide (SiC) and Boron Carbide (B4C) plates, which now deliver NIJ Level IV protection at only 5.5–6.5 lbs—a benchmark that dramatically reduces fatigue and increases mission duration in high-threat environments. For defense procurement teams and material strategists, the shift toward high-purity, high-density ceramics paired with optimized backing layers (UHMWPE, aramid composites) is central to meeting evolving threats, including 7.62 mm AP rounds and complex, multi-hit kinetic engagements.

Simultaneously, vehicle protection programs for APCs, IFVs, and tactical platforms are adopting ceramic armor to achieve 30–50% weight reduction compared to traditional steel-based systems—unlocking gains in payload capacity, maneuverability, fuel efficiency, and survivability. Manufacturing innovation is amplifying this shift: Spark Plasma Sintering (SPS) and ceramic Additive Manufacturing now enable curved, complex geometries, refined grain structures, and enhanced edge stability, addressing historical brittleness and improving multi-hit reliability.

Ceramic Armor Market Analysis: Multi-Hit Material Advancements, Defense Procurement Momentum & Next-Gen Tile Manufacturing

The global Ceramic Armor Market witnessed accelerating investment and technology adoption throughout 2025, driven by heightened geopolitical risk, soldier-modernization programs, and a strong focus on survivability. In October 2025, the U.S. Department of Defense reported sustained Q4 spending on Soldier Protection Systems and armored vehicle upgrades, signaling continued demand for high-performance SiC and B4C ceramic armor plates. This followed August 2025, when the Ministry of National Defense in Taiwan announced plans to procure 48,000 Boron Carbide ceramic plates capable of stopping 7.62mm AP threats, one of the largest known procurement signals for ultra-lightweight body armor in Asia. Mass production was scheduled for 2028-2029, indicating long-term, stable demand for B4C formulations.

Simultaneously in July 2025, Avient Corporation expanded the performance envelope for hybrid ceramic armor systems with the launch of Dyneema HB330/HB332, enabling strike-face and backer integration that can achieve a 45% weight reduction in hard armor. That same month, Safe Pro Group secured a contract for ballistic protection systems in the Indo-Asia Pacific region, validating the growing operational need for modular hard armor solutions in emerging hotspots. In April 2025, materials researchers publicly presented progress in nano-structured ceramics for combat helmets, marking a strategic shift toward lighter and more impact-resistant head protection materials.

Beyond personal protection, March 2025 marked growing architectural and infrastructure applications, as a European government mandated ballistic façade codes for critical buildings-expanding demand for large-format ceramic security panels. Earlier in the year, in February 2025, a European R&D consortium reported breakthroughs in Titanium Diboride (TiB₂) armor ceramics, showing promise against kinetic penetrators due to improved manufacturing efficiency and hardness profiles. In January 2025, a U.S. Supreme Court-upheld legal precedent validated CoorsTek’s right to commercialize specialized ceramic components, strengthening long-term IP protection for advanced ceramic armor technologies. Collectively, these developments underline a market characterized by rapid materials innovation, large-scale defense procurement, and a widening scope of ceramic armor applications across land systems, soldier gear, and critical infrastructure.

Trends and Opportunities Reshaping Ceramic Armor Market

Trend 1: Silicon Carbide Emerges as the Military’s Preferred Material for Next-Generation Vehicle Armor Modernization

The move from alumina (Al₂O₃) to Silicon Carbide (SiC) represents a strategic shift in armored vehicle procurement, driven by formal requirements to withstand increasingly powerful armor-piercing (AP) threats while retaining maximum vehicle mobility. SiC and B4C exhibit the highest mass effectiveness (Em) values against common battlefield rounds—meaning they deliver equivalent protection to rolled homogeneous armor (RHA) steel at dramatically lower areal densities. This weight advantage is no longer optional; it is essential for meeting mobility, air-transportability, and survivability benchmarks set by NATO and U.S. defense programs.

The U.S. Army Research Laboratory’s ManTech Armor program has played a critical role in accelerating SiC adoption. By redesigning the hot-pressing workflow to reduce manufacturing costs to levels comparable with pressureless-sintered SiC, ARL created a viable industrial base capable of supporting large-scale procurement for future vehicle fleets. Operational confidence in the material is reinforced by its existing deployment in aerospace platforms, including AC-130U gunships and C-130/C-17 transport aircraft. The qualification of sintered SiC armor for these aircraft—where weight, reliability, and temperature stability are mission-critical—provides an authoritative validation of SiC’s readiness for next-generation ground vehicle programs.

Trend 2: Rapid Expansion of Ceramic Plate Inserts in Civilian and Law Enforcement Body Armor Programs

The personal protection segment is undergoing a structural shift toward ceramic-composite inserts as law enforcement and private security agencies prepare for more frequent rifle-rated threats. While patrol officers traditionally wear NIJ Level IIIA soft armor, rising incidents involving high-velocity rifles have made lightweight ceramic/polyethylene hybrid plates essential for scalable protection strategies. These plates allow officers to rapidly up-armor to NIJ Level III or IV (RF1/RF3) without carrying heavy plates throughout an entire shift.

Ceramic plates outperform steel plates in every domain relevant to operational survivability: multi-hit resistance, projectile fragmentation capability, and low spall generation. SiC and B4C plates are engineered to break apart the projectile upon impact, while the polymer backing absorbs secondary energy—ensuring reliable performance even when impacts occur in close proximity. By contrast, steel plates often suffer from severe backface deformation or spalling, generating secondary fragments that pose additional injury risks. This performance advantage is accelerating procurement of ceramic inserts among law enforcement, border security, private military contractors, and civilian personal-defense markets.

Opportunity 1: Ceramic Matrix Composites Enable Lightweight Structural Armor for Future Combat Vehicles

Ceramic Matrix Composites (CMCs) represent a high-value opportunity as militaries pursue lighter, more mobile combat vehicles with integrated structural and ballistic functionality. Unlike monolithic ceramics—which are strong but brittle—SiC/SiC CMCs possess high specific strength and stiffness, enabling their use as both structural hull components and protective armor. This dual functionality eliminates the need for a separate metal load-bearing frame, reducing parasitic weight and improving fuel efficiency, transportability, and tactical agility.

CMCs also offer unparalleled high-temperature and oxidation stability, maintaining mechanical integrity at temperatures exceeding 2000 °C. This resilience is essential for armor exposed to blast fireballs, propulsion system heat, or future directed-energy threats. Moreover, the incorporation of SiC fibers significantly enhances fracture toughness, transitioning the armor behavior from “fail-fast” (typical of ceramics) to “fail-safe”—a critical requirement for structural components subjected to multi-hazard conditions. As global defense modernization programs shift toward lighter, modular armored platforms, CMC-based structural armor is poised to become one of the highest-growth material categories in the market.

Opportunity 2: Additive Manufacturing of Graded-Density Ceramic Armor Creates Customizable, High-Efficiency Ballistic Solutions

Additive Manufacturing (AM) presents a transformative opportunity for ceramic armor, enabling complex geometries, variable-density architectures, and platform-specific conformal designs that are impossible with traditional fabrication. Functionally Graded (FG) armor—produced via AM—allows engineers to tailor hardness, toughness, and microstructure through the armor's thickness. This multi-regime optimization is pivotal in converting the strike face into a fragmentation layer, while the posterior region absorbs and dissipates impact energy without catastrophic failure.

AM also enables true conformal armor, allowing armor tiles to match the complex shapes of turrets, unmanned ground vehicles, aircraft fuselages, and crew hatches. Eliminating geometric gaps removes ballistic weak points and reduces reliance on secondary patch armor. Graded architectures achieved through AM further reduce internal stress concentrations during high-velocity impacts. Experimental results have shown that such engineered transitions can delay crack propagation significantly, thereby improving multi-hit survivability and reducing the total required material mass.

As defense programs pursue platform-specific armor kits, unmanned systems, and modular protection suites, AM-based ceramic armor stands out as a pivotal enabler of lightweight, high-performance, rapidly configurable protection.

Ceramic Armor Market Share Analysis

Market Share by Material Type: Boron Carbide Leads with 35.8% Share

Boron Carbide (B4C) holds the largest share of the Ceramic Armor Market at 35.8% in 2025, reflecting its status as the premier high-performance ceramic for applications where every gram of weight savings directly translates into survivability and mobility advantages. Its dominance is driven by unmatched hardness, exceptional ballistic efficiency, and superior weight-to-protection ratios, making B4C the preferred material for dismounted soldier plates, special forces body armor, aviation armor modules, and other mission-critical applications where mobility is as vital as stopping power. This strong share illustrates the market’s prioritization of ultra-lightweight personal protection, especially amid rising modernization programs across NATO and allied defense forces. Surrounding material categories further shape procurement decisions: silicon carbide (SiC)—the backbone of large-scale infantry and vehicular armor procurement—balances multi-hit capability with cost-effectiveness, alumina (Al₂O₃) remains a stable choice for budget-constrained applications and spall liners, and advanced ceramics and composites blend materials to optimize impact resistance and durability. Ultimately, material selection follows a performance–cost–weight equation, positioning B4C as the top-tier ceramic for premium applications and SiC as the scalable solution for broad military use.

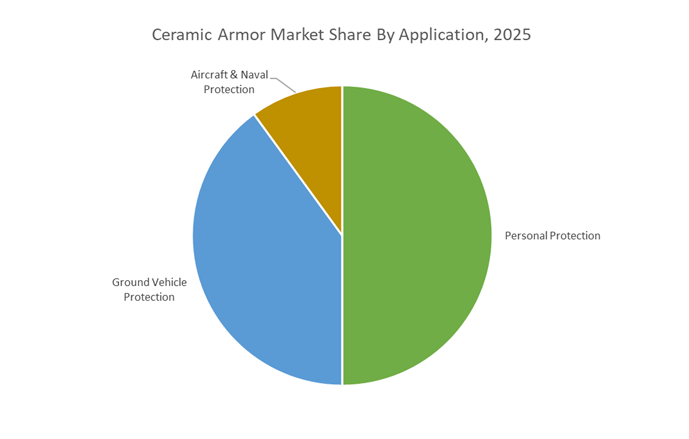

Market Share by Application: Personal Protection Leads with 48.9% Share

Personal Protection dominates the Ceramic Armor Market with a 48.9% share in 2025, reinforcing its position as the largest and most strategically important application category. This leadership reflects the global shift toward lightweight, high-mobility ballistic protection systems for military and law enforcement personnel, where ceramic strike plates are essential for defeating armor-piercing rifle rounds while keeping carried load to a minimum. The segment’s share is driven by continuous procurement cycles, stringent survivability requirements, and modernization initiatives that favor premium materials such as boron carbide and next-generation ceramic composites for maximizing protection without compromising agility. In contrast, ground vehicle protection relies heavily on silicon carbide due to its balanced cost and robust multi-hit capability, making it ideal for armored personnel carriers, tactical vehicles, and mine-resistant platforms. Aircraft and naval protection, though smaller in volume, represents the extreme end of performance requirements, justifying the use of the lightest and most advanced ceramic systems for mission-critical survivability upgrades. Collectively, the application landscape highlights a market anchored by personal armor demand, but increasingly diversified by vehicle and aerospace adoption as threat levels intensify worldwide.

Country Analysis: Global Ceramic Armor Market Innovation Hubs

United States: Material Science Leadership and Next-Generation Ceramic Armor Development

The United States remains the epicenter of advanced ceramic armor innovation, driven by the largest global defense budget and a sustained focus on soldier protection, vehicle survivability, and transparent armor modernization. With major research institutions like the Air Force Research Laboratory (AFRL) and Naval Research Laboratory, the U.S. continues to pioneer groundbreaking materials such as the ceramic ball matrix armor, a novel system using ceramic spheres encapsulated in foam and backed by polyethylene sheets. This design delivers 50% weight reduction compared to rigid ceramic plates while offering superior multi-hit performance, marking a significant shift in the evolution of flexible ceramic armor for next-generation dismounted troops.

The U.S. market is also being reshaped by strategic sourcing policies. The Department of Defense’s revised tariff framework (July 2025) targeting ceramic feedstocks and imported ballistic plates is accelerating domestic investment in silicon carbide (SiC) and boron carbide (B4C) production, including hot pressing and reaction bonding capabilities. These advancements are critical for sustaining programs such as the Armored Multi-Purpose Vehicle (AMPV), which depends on high-strength ceramic composite tiles for protection against armor-piercing rounds and fragmentation. Simultaneously, the trend toward segmented ceramic armor designs—essential for IHPS helmets and next-gen vests—reflects an industry-wide push to improve flexibility, reduce crack propagation, and maintain high multi-hit capability. The United States further strengthens its leadership through the DTIC Ceramic Armor Material Database, which aggregates three decades of performance testing on SiC, B4C, and TiB₂, enabling data-driven computational armor design.

European Union: EDF-Funded Collaborative R&D Driving Lightweight Ceramic Armor Innovation

The European Union’s ceramic armor ecosystem is defined by large-scale collaboration, regulatory alignment, and strategic autonomy goals enabled by robust investments through the European Defence Fund (EDF). In the 2025 Work Programme, the EDF allocated over €25 million specifically to the Materials and Components thematic call to support research on lighter, more resilient ceramic composites for ground combat platforms. This effort reflects Europe’s commitment to reducing soldier burden, enhancing mobility, and modernizing its armored fleets. The record volume of R&D proposals submitted in 2025 demonstrates deep industry engagement in developing next-generation ballistic ceramics, nano-structured composites, and hybrid armor architectures.

Ground combat remains a top priority, with about €192 million in EDF funding dedicated to enhancing the protection of infantry fighting vehicles, armored personnel carriers, and dismounted soldiers. A significant portion of innovation originates from SMEs supported under the European Defence Innovation Scheme (EUDIS), which allocates €336 million to fast-track breakthroughs such as advanced sintering methods, additive manufacturing of complex ceramic geometries, and lightweight ceramic plate designs. These cooperative development models strengthen Europe’s strategic autonomy by building an agile supply chain for high-performance ceramic armor, while ensuring interoperability across its multi-national defense ecosystem.

Turkey: Strategic Boron Carbide Scaling to Achieve Defense Independence

Turkey is positioning itself as a global powerhouse in boron carbide (B4C) production, leveraging the country's vast boron reserves to achieve full defense-sector independence. The opening of its first major boron carbide production plant in Bandırma (March 2023), with an initial capacity of 1,000 tons annually, represents a transformative step toward localizing the supply of one of the world’s hardest and most valuable ceramic armor materials. Turkish leadership highlights that converting boron ore into boron carbide increases its value by 300 times, and when used in armor systems, that multiplier reaches 2,000 times—underscoring the economic and strategic significance of this material.

By expanding domestic B4C manufacturing, Turkey is strengthening its ability to produce body armor plates, ceramic strike faces, and vehicular armor tiles without reliance on imports. This investment directly supports the country’s long-term defense roadmap, enabling Turkey to develop high-purity ceramics that meet international ballistic standards. As ballistic threats evolve, the localized production of B4C is expected to fuel rapid innovation in lightweight ceramic armor systems, integrated protection kits for armored vehicles, and border security technologies—reinforcing Turkey’s goal of full indigenization across critical defense platforms.

China: Silicon Carbide Acceleration and Dual-Use Material Expansion Driving Ceramic Armor Capabilities

China is rapidly emerging as a major global force in silicon carbide (SiC) ceramic armor, propelled by its dual-use material strategy serving both defense and high-tech industries such as EVs and semiconductors. Demand for SiC substrates in electric vehicles and renewable power electronics is significantly reducing production costs, enabling wider application of high-purity SiC plates in military ballistic systems. In January 2025, domestic manufacturers such as SNAM Abrasives introduced High Purity SiC (HP SiC) with 99.99% purity—meeting the stringent mechanical and thermal requirements for cutting-edge armor tiles used in next-generation soldier and vehicle protection.

China’s modernization agenda, particularly its focus on strengthening the Aerospace & Defense segment, has accelerated the deployment of SiC armor solutions. SiC’s superior hardness, fracture toughness, and high-temperature stability make it a core material for ceramic matrix composites (CMCs) used in armored vehicles, aircraft components, and high-performance protective systems. This alignment between civilian material innovation and military modernization enables China to rapidly expand domestic capacity for lightweight ballistic ceramics, reduce import dependence, and reinforce its goal of advancing indigenous protection technologies across land and aerospace domains.

Competitive Landscape: High-Purity Ceramics, Hybrid Armor Backers & Global Defense-Grade Tile Manufacturing

The competitive environment in the Ceramic Armor Market is shaped by vertically integrated ceramic tile manufacturers, advanced composite suppliers, defense OEMs, and specialized material innovators. Market differentiation is driven by ceramic purity (SiC/B4C grades), grain structure engineering, manufacturing scale, plate consistency, and proven performance in NIJ Level IV, ESAPI, and STANAG testing regimes. Companies that pair ceramic strike faces with aramid/UHMWPE backers hold a strategic advantage as modern armor increasingly relies on hybridized solutions to balance weight, cost, and survivability.

3M Company (Ceradyne) - Leading Supplier of Boron Carbide and Silicon Carbide for ESAPI and Vehicle Armor

Ceradyne, a 3M subsidiary, remains one of the dominant global producers of B4C and SiC ceramic armor materials, supplying critical tiles used in NIJ Level IV and ESAPI systems. Its sustainability-focused manufacturing upgrades-including closed-loop water systems and waste-recycling infrastructure at its Tennessee facility-enhance ESG compliance for defense customers. Ceradyne’s ceramic formulations deliver proven stopping capability against .30-06 AP threats, forming a cornerstone of U.S. military body armor programs.

CoorsTek Inc. - High-Performance Ceramic Tiles for Body and Vehicle Armor with Precise Microstructural Control

CoorsTek operates secure, high-volume ceramic production lines offering customized SiC, Al₂O₃, and B4C tiles in SAPI formats and ultra-thin vehicle armor configurations (1mm+). Its proprietary CeraShield™ ceramics are engineered for low density, high hardness, and tight microstructure control, enabling consistent ballistic results across multiple threat levels. CoorsTek leverages a strong IP portfolio validated by the 2025 U.S. Supreme Court–upheld ruling, strengthening its market positioning.

Saint-Gobain (Performance Ceramics & Refractories) - Advanced SiC/B4C Armor Materials Tailored for Mission-Specific Requirements

Saint-Gobain provides a diverse portfolio of ceramic armor materials, including Hexoloy® and Forceram®, engineered for differing mission profiles ranging from soldier kits to UAV and aircraft applications. The company’s Norbide® Hot-Pressed Boron Carbide offers optimized density and hardness for ultra-lightweight air armor. Saint-Gobain supports customers through full solution design-from modeling to final deployment-ensuring multi-hit resilience and reliable fragmentation resistance.

Morgan Advanced Materials - Technical Ceramics for Defense with Improved Cost Efficiency and High-Temperature Performance

Morgan Advanced Materials focuses on ballistic ceramics and composite systems optimized for weight savings and performance against fragmentation. In 2025, the company achieved £24M in efficiency gains, strengthening cost competitiveness while maintaining capacity for defense-grade ceramics. Its materials are used across soldier protection, armored vehicles, and aerospace applications requiring precise temperature and mechanical resilience.

CeramTec GmbH - High-Purity Ceramic Tiles for Body Armor with Microstructural Uniformity and Advanced R&D

CeramTec leverages decades of expertise in medical and industrial ceramics to manufacture extremely uniform SiC/B4C tiles with tight tolerance control. Ongoing R&D investments target higher homogeneity and lower density ceramics to improve the cost-to-performance ratio for large procurement programs. The company’s precision manufacturing practices translate into consistent ballistic performance and scalable supply.

TenCate Advanced Composites (Toray) - Critical Composite Backing Layers for Hybrid Ceramic Armor Systems

While not a ceramic manufacturer, TenCate (Toray) plays a pivotal role by supplying aramid, carbon fiber, and UHMWPE composite backers that absorb residual projectile energy after ceramic strike-face failure. These materials are essential for multi-hit survivability and anti-spall performance in hybrid armor plates. TenCate’s system-level approach aligns with next-gen modular hard armor programs worldwide.

Ceramic Armor Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6 Billion

|

|

Market Size (2035)

|

$12.7 Billion

|

|

Market Growth Rate

|

7.8%

|

|

Segments

|

By Material Type (Boron Carbide, Silicon Carbide, Alumina, Titanium Diboride, Ceramic Matrix Composites, Hybrid Ceramic Systems), By Product Type (Hard Armor Plates, Vehicle Armor Tiles, Ballistic Helmets, Aircraft Armor, Modular Armor Systems), By Application (Personal Protection, Ground Vehicles, Naval Vessels, Aircraft), By Manufacturing Process (Hot Pressing, Sintering, Reaction Bonding, Additive Manufacturing), By Standard/Protection Level (NIJ Level III, NIJ Level IV, STANAG 4569, NATO Standards)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

CoorsTek Inc., Saint-Gobain S.A., Morgan Advanced Materials plc, Kyocera Corporation, BAE Systems plc, Avon Protection plc, TenCate Advanced Armor, DuPont de Nemours Inc., Advanced Ceramics Manufacturing, Ceradyne Inc., Rheinmetall AG, Armor Express, Plasan Sasa Ltd., SLAN Abrasives Pvt. Ltd., Hardwire LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ceramic Armor Market Segmentation

By Material Type

- Boron Carbide (B₄C)

- Silicon Carbide (SiC)

- Alumina (Al₂O₃)

- Titanium Diboride (TiB₂)

- Ceramic Matrix Composites (CMCs)

- Hybrid Ceramic Systems

By Product Type

- Hard Armor Plates

- Vehicle Armor Tiles

- Ballistic Helmets

- Aircraft Armor

- Modular Armor Systems

By Application

- Personal Protection

- Ground Vehicles

- Naval Vessels

- Aircraft

By Manufacturing Process

- Hot Pressing

- Sintering

- Reaction Bonding

- Additive Manufacturing

By Standard / Protection Level

- NIJ Level III

- NIJ Level IV

- STANAG 4569

- NATO Standards

- Spall Resistance

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Ceramic Armor Market

- CoorsTek, Inc.

- Saint-Gobain S.A.

- Morgan Advanced Materials plc

- Kyocera Corporation

- BAE Systems plc

- Avon Protection plc

- TenCate Advanced Armor

- DuPont de Nemours, Inc.

- Advanced Ceramics Manufacturing

- Ceradyne, Inc.

- Rheinmetall AG

- Armor Express

- Plasan Sasa Ltd.

- SLAN Abrasives Pvt. Ltd.

- Hardwire LLC

*- List not Exhaustive