Armor Materials Market Overview: Weight Reduction, Ballistic Efficiency & Material Purity Driving the Market Outlook to 2035

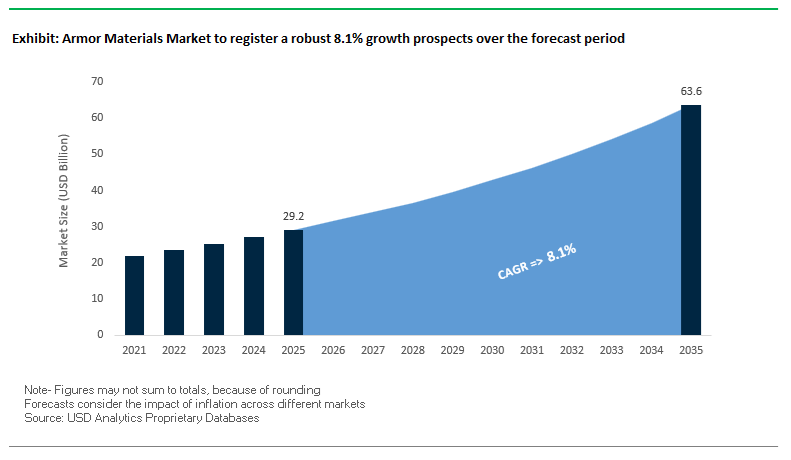

The Global Armor Materials Market, valued at USD 29.2 billion in 2025 and projected to reach USD 63.6 billion by 2035 at a strong CAGR of 8.1%, is undergoing a decisive shift toward lightweight, high-efficiency, high-purity ballistic solutions. Defense modernization programs, updated NIJ 0101.07 / RF3 and NATO STANAG ballistic standards, and the evolving demands of multi-domain warfare are rapidly accelerating the adoption of UHMWPE composites, high-density Boron Carbide (B4C), Silicon Carbide (SiC) ceramics, advanced transparent armor laminates, and next-generation armored steel alloys engineered for superior strength-to-weight performance.

As soldier systems, tactical vehicles, armored aircraft, and critical infrastructure seek enhanced mobility and survivability, procurement teams must evaluate armor materials against increasingly complex variables—weight minimization, multi-hit resistance, blast protection, fracture toughness, material purity, and supply chain resilience. Material science innovations—such as UHMWPE delivering 45% weight reduction, transparent armor achieving 20% thickness reduction, and ceramic strike faces requiring >98.5% purity—have repositioned advanced armor materials as strategic enablers of next-generation defense capability. Meanwhile, national “Buy Domestic” and sovereign manufacturing initiatives, such as India’s 12.41% DRDO budget increase, are reshaping regional supply chains and long-term procurement strategies.

Market Analysis: Ballistic Innovations, Defense Contracts & NIJ Standard Shifts Reshaping Global Procurement

The Armor Materials Market experienced a wave of transformative developments across 2024–2025, accelerating technological adoption across body armor, helmets, tactical gear, transparent armor, armored vehicles, and protective enclosures. In July 2025, Avient Corporation advanced UHMWPE technology with the launch of Dyneema® woven composites, incorporating a dual-layer architecture delivering 34% weight savings and 10× abrasion resistance - a breakthrough for next-gen helmets and modular tactical systems. That same month, Safe Pro Group secured a U.S. government-linked contract to supply ballistic protection and EOD systems for Indo-Asia Pacific operations, highlighting intensifying demand for specialized armor solutions in high-tension regions.

Strategic defense technology convergence continued into May 2025, when Motorola Solutions announced a $4.4 billion acquisition of Silvus Technologies, signaling a major push by tech giants into the defense domain - a sector that relies heavily on integrated armor systems, protected enclosures, and communication-compatible ballistic materials. Regulatory shifts further reshaped buyer requirements: from late 2024 into early 2025, manufacturers and agencies were instructed to transition toward compliance with the new NIJ 0101.07 and NIJ 0123.00 standards. This regulatory upgrade is triggering a multi-year global refresh cycle for both soft and hard armor as end-users adopt higher transparency, multi-hit testing, and fragmentation standards.

Major contract momentum remained strong. In March 2024, Point Blank Enterprises secured a USD 215 million U.S. Army contract for modular body armor systems, reinforcing sustained military investment in weight-optimized but higher-protection soldier systems. In February 2024, DuPont launched Kevlar® EXO, a major step-change in flexibility and ballistic resistance for helmets, vests, and shields, while Avon Protection won a USD 204 million OEM contract for the U.S. Army’s Integrated Head Protection System (IHPS). Meanwhile, MSI Defense Solutions secured a $34 million Counter-UAS contract, requiring armored deployment platforms - reflecting expanding integration of armor materials into emerging defense technologies. Collectively, these recent developments confirm strong and diversified demand across personal protection, vehicle armor, transparent armor, and defense electronics enclosures.

Key Trends Redefining the Advanced Armor Materials Market

Trend 1: Transparent Ceramics and Advanced Glazing Systems Become Core to Next-Generation Vehicle and Aircraft Survivability

Modern armored vehicle and aircraft designers are rapidly replacing traditional thick laminated glass with transparent ceramic armor systems composed of materials such as Aluminum Oxynitride (ALON) and Magnesium Aluminate Spinel. These advanced ceramics deliver a step change in ballistic performance, enabling lighter, thinner, and more durable protection than conventional glass/plastic laminates. ALON’s mechanical characteristics illustrate the leap in capability—its hardness is four times greater than fused silica glass and its strength is roughly three times higher than steel of equivalent thickness, dramatically lowering areal density and improving platform mobility.

Beyond ballistic resistance, transparent ceramics provide an operational advantage through broadband transmittance across the near-UV to mid-IR spectrum. This optical range is crucial for modern ISR (Intelligence, Surveillance, Reconnaissance) systems, multispectral sensors, and targeting optics, all of which must operate across several spectral bands without distortion. Importantly, materials such as ALON and Spinel can be processed in large sizes and complex geometries, unlike single-crystal sapphire. This manufacturability enables the fabrication of panoramic windows, curved sensor domes, and large-area cockpit glazing, which significantly enhances situational awareness and threat detection capabilities for next-generation land and air platforms.

As military vehicles transition toward integrated sensor architecture and visibility-enhancing cockpit layouts, transparent ceramics are becoming indispensable to both ballistic survivability and sensor performance—positioning them as a critical growth segment of the advanced armor materials market.

Trend 2: Commercialization of Lightweight, High-Resilience Soft Armor for Law Enforcement and Civilian Security

The global proliferation of asymmetric threats has strengthened demand for advanced soft armor solutions tailored for law enforcement, private security, and critical infrastructure personnel. High-strength fibers such as Ultra-High-Molecular-Weight Polyethylene (UHMWPE) and aramid are being engineered into increasingly lightweight, concealable ballistic systems optimized for prolonged wear and broad threat coverage. UHMWPE, with its extremely high strength-to-weight ratio, enables NIJ Level IIIA soft armor vests weighing as little as 2–4 pounds, dramatically improving wearer mobility and reducing fatigue during extended missions.

Aramid and polymer-based systems are also being redesigned to enhance multi-hit capability, an essential requirement in active shooter and counter-terror scenarios where multiple ballistic impacts are possible. Modern UHMWPE fabrics additionally exhibit greater moisture and UV resistance compared to aramid fibers, preserving long-term ballistic performance for users frequently exposed to outdoor environments. These material advances are positioning soft armor not merely as protective apparel but as a high-performance, ergonomic, and durable system suitable for varied operational conditions.

As civilian security markets expand and law enforcement agencies adopt lighter and higher-performing protective solutions, this segment is expected to see accelerated innovation and widespread adoption across global jurisdictions.

High-Value Opportunities Emerging in the Advanced Armor Materials Market

Opportunity 1: Additive Manufacturing Enables Complex, Multi-Material Armor Structures with Superior Protection-to-Weight Efficiency

Additive manufacturing (AM) is creating one of the most significant opportunities in the advanced armor landscape by enabling topologically optimized, gradient-density, and multi-material protective structures that cannot be produced through conventional subtractive or casting methods. The integration of Topology Optimization (TO) with AM allows designers to remove excess mass while maintaining ballistic performance, producing organically shaped armor components that achieve substantial weight savings—an essential factor for aircraft, soldier systems, and tactical ground vehicles.

The ability of AM to consolidate multiple functions into a single structure is another strategic advantage. AM-produced armor components can integrate strike faces, backing layers, load-bearing elements, internal cooling channels, and mounting interfaces into a single unified part. This consolidation reduces assembly complexity, improves structural integrity, and enhances survivability in combat scenarios where mechanical failure modes must be minimized. Equally important is the rapid prototyping capability of AM, which enables defense programs to iterate designs quickly and produce low-volume or mission-specific parts without tooling constraints—a critical requirement for in-theater repairs and rapidly evolving threat landscapes.

As militaries prioritize lighter, more modular, and more adaptive protective systems, additive manufacturing is emerging as a cornerstone technology for next-generation armor design and supply chain resilience.

Opportunity 2: Active and Adaptive Armor Systems for Hypersonic, Directed-Energy, and Electromagnetic Threat Mitigation

The emergence of hypersonic glide vehicles (HGVs) and Directed Energy Weapons (DEWs) is expanding the threat environment far beyond the capabilities of traditional passive armor systems, creating a substantial opportunity for integrated active/passive protective architectures. High-Power Microwave (HPM) systems, for example, target the electronics of military platforms rather than their structural integrity, necessitating armor solutions that incorporate electromagnetic shielding, Faraday cage configurations, and pulse-absorption layers to protect avionics, communication systems, and missile guidance electronics.

The rapid adoption of High-Energy Lasers (HELs) as offensive weapons further accelerates demand for advanced thermal and ablative materials. R&D efforts are increasingly focused on ablative ceramic coatings and thermally conductive polymers that can absorb or dissipate the thermal shock of a laser strike, preventing structural degradation and preserving mission functionality. Meanwhile, the defense against hypersonic threats requires materials capable of withstanding extreme aero-thermal loads exceeding 2000°C, driving research into Ultra-High-Temperature Ceramics (UHTCs) and advanced Ceramic Matrix Composites (CMCs) for leading edges, nose cones, and control surfaces.

Armor Materials Market Share Analysis

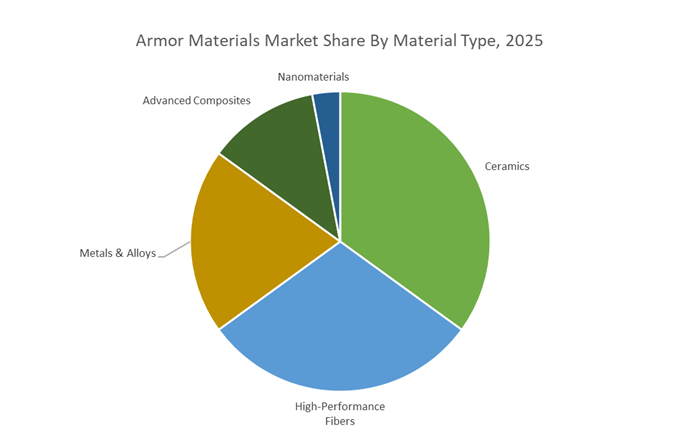

Market Share by Material Type: Ceramics Lead with 35.4% Share

Ceramics hold the largest share of the Advanced Armor Materials Market at 35.4% in 2025, underscoring their central role in modern ballistic protection systems. Their dominance stems from exceptional hardness, compressive strength, and energy-dissipation capability, making ceramic armor the primary barrier against high-velocity projectiles in both personal and vehicular protection. The strong market share reflects widespread deployment of alumina, silicon carbide, and boron carbide in military body armor plates, lightweight vehicle armor kits, and aerospace protection systems—applications where weight reduction, multi-hit capability, and high stopping power are critical performance metrics. The broader material ecosystem reinforces ceramics' leadership: high-performance fibers such as aramid and UHMWPE deliver spall containment and structural integrity; metals and alloys remain indispensable for heavy-kinetic threats and cost-sensitive platforms; advanced composites enable complex geometries and hybrid protection architectures; and nanomaterials act as enhancers in next-generation armor systems. The overall segmentation demonstrates a market increasingly prioritizing lightweight, high-efficiency armor materials, with ceramics anchoring the highest-value performance tier.

Market Share by Application: Body Armor Leads with 35.8% Share

Body Armor accounts for the largest application share at 35.8% in 2025, reflecting its position as the highest-volume and most continuously replenished segment of the advanced armor ecosystem. Demand is propelled by modernization of military forces, rising procurement of lightweight personal protection systems (PPS), and increased requirements for multi-threat resistance across defense, law enforcement, and security sectors. The segment’s strong share is closely tied to the transition toward lighter, more ergonomic, and higher-performance ceramic–fiber hybrid systems, designed to reduce soldier fatigue while improving survivability against rifle rounds and fragmentation threats. Beyond personal armor, the application landscape showcases a diversified adoption curve: vehicle armor leads technological integration with multi-layer systems targeting ballistic, blast, and mine resistance for next-generation tactical and armored vehicles; aerospace and marine armor prioritize extreme weight-to-protection ratios, relying on premium titanium alloys and boron carbide composites; and civil armor expands steadily through demand for transparent armor, architectural hardening, and infrastructure protection in high-risk environments.

Country Analysis: Global Advanced Armor Materials Market Innovation Hubs

United States: Modernizing Defense Armor Systems Through High-Budget Procurement and Advanced Material Innovation

The United States remains the most influential global hub for advanced armor materials, driven by monumental defense investments, domestic material security policies, and next-generation protective system development. The Department of Defense’s FY 2025 procurement and RDT&E request of $310.7 billion ensures long-term funding for armored vehicles, soldier protection systems, missile defense platforms, and thermal protection technologies. The Defense Production Act Investment (DPAI) continues strengthening supply chain resilience, including a $7 million award to The Doe Run Resources Corporation to expand domestic nickel and cobalt supply chains—critical alloying materials for advanced metallic armor. In March 2024, the DoD awarded $11.7 million to Ensign-Bickford Aerospace & Defense to scale PCBA manufacturing for hypersonic weapons, accelerating the development of ultra-high-temperature ceramic composites and thermal protection systems essential for Mach-speed defense capabilities.

The U.S. is also advancing R&D for next-generation lightweight armor systems. The National Academies’ Army Next Generation Armor Workshop (March 2025) emphasized barriers and breakthroughs in composite armor science, showcasing the Army’s commitment to ultralight, survivability-enhancing materials. Meanwhile, the personal protection market is being reshaped by Dyneema's launch of HB330 and HB332 ballistic materials, built on third-generation fiber technology that delivers up to 45% weight reduction in hard armor applications. These advancements reinforce the U.S. as a powerhouse in ballistic composite engineering, soldier survivability solutions, and high-performance armor material innovation.

United Kingdom: Strengthening Sovereign Armor Capability Through Innovation Funds and Composite Integration

The United Kingdom is accelerating its position in the advanced armor materials market through targeted government funding, increased defense budgets, and industrial consolidation. The newly launched £400 million Defence Innovation Fund (FY 2025) is designed to fast-track R&D in advanced materials, autonomous systems, and emerging technologies—creating significant pull for high-specification armor composites and protection solutions. With the UK committing to increase defense spending to 2.5% of GDP by 2027, procurement budgets will expand dramatically, enabling greater adoption of cutting-edge armor materials across upgraded military platforms.

Nearly 50% of the UK’s £62.2 billion planned defense spending for 2025/26 is allocated to equipment procurement, directly amplifying demand for composite armor, ceramic armor modules, and multi-layered protection systems for ground vehicles and soldier systems. Morgan Advanced Materials, leveraging its acquisition of Composites & Defence Systems (CDS), continues delivering integrated ceramic-composite armor solutions optimized for UK and allied defense programs. With its strategic emphasis on sovereign capability and advanced materials engineering, the UK is rapidly emerging as a leading hub for modular composite armor technologies and next-generation protective systems.

China: Accelerating Ballistic Ceramic Production and High-Strength Fiber Development for Military Modernization

China is expanding aggressively in the ballistic ceramics and high-strength fiber materials market, driven by large-scale military modernization and strong national policies promoting material self-sufficiency. Demand for lightweight vehicle armor and personal protection is increasing rapidly, with domestic production rising for SiC and Alumina ceramic tiles, essential for advanced hard armor plates. China is further closing the technological gap in UHMWPE and para-aramid fibers, recognizing their importance in soft armor, helmets, and hybrid composite armor systems.

Chinese state-owned enterprises (SOEs) are aligning under vertically integrated production models, strengthening the country’s control over ballistic ceramics, advanced metallic alloys, and composite armor materials. This alignment reduces dependency on foreign suppliers and accelerates scaling for next-generation protection systems. Combined with China’s expanding military platforms and security forces, the country continues to consolidate its position as a global producer of lightweight ceramic armor and structural composite protection technologies.

Turkey: Building a Vertically Integrated Armor Ecosystem and Expanding Global Ceramic Armor Exports

Turkey has emerged as a rapidly growing force in the international armor materials market, driven by a strategically integrated defense industrial base and strong government backing. Nurol Teknoloji’s Phase-2 contract for the 2025 Ballistic Protective Vest Project reinforces Turkey’s long-term commitment to domestic armor production. The company specializes in manufacturing Boron Carbide (B4C) and Silicon Carbide (SiC)—two of the hardest and lightest ceramic materials used in elite armor plates. This vertical integration allows Turkey to control quality, cost, and performance across the full armor value chain.

Turkey’s export strategy is equally aggressive. Nurol Teknoloji has expanded its presence through investments in Germany and the United States, enabling deeper integration into NATO-aligned supply chains and global armor procurement markets. With high domestic demand and international expansion, Turkey is positioning itself as a leading supplier of ceramic armor plates, vehicle armor kits, and personal protective systems.

Germany (Europe): Integrated Vehicle Protection Systems and Specialty Ceramic Armor for Defense and Civilian Security

Germany plays a central role in Europe’s advanced armor materials ecosystem, leveraging its engineering strength, defense manufacturing expertise, and growing demand for both military and civilian protection systems. Rheinmetall AG is pioneering integrated vehicle protection architectures that merge passive armor (composites and alloys) with active defense systems for next-generation armored vehicles. This integrated approach significantly enhances vehicle survivability against kinetic and explosive threats.

Germany is also a major contributor to ceramic armor innovation. CeramTec GmbH manufactures lightweight technical ceramics—including Alumina, SiC, and B4C—engineered for high hardness, multi-hit capability, and reduced mass. These materials are used in body armor, vehicle armor kits, and specialty shielding solutions. On the civilian side, rising demand for covert, lightweight armor in VIP vehicles, law enforcement fleets, and cash-in-transit vehicles is driving innovation in thin, advanced composite panels and hybrid ceramic-polymer systems. Germany’s multidisciplinary approach ensures strong growth across both military and high-security civilian armor applications.

Sweden: High-Strength Armor Steel and Corrosion-Resistant Metallic Solutions for Heavy and Naval Platforms

Sweden continues to expand its presence in the advanced metallic armor materials market, leveraging world-leading expertise in high-strength steel and titanium alloys. SSAB AB remains a global leader in the production of ultra-high-strength, wear-resistant armor steels, widely used in ground combat vehicles, heavy-duty armored platforms, and naval vessel protection. These steels are engineered for superior toughness, ballistic resistance, and structural integrity under extreme conditions.

Swedish defense contractors are also advancing the development of lightweight titanium alloys for components where weight reduction is crucial—such as naval systems, armored land vehicles, and specialty aerospace defense platforms. Titanium’s exceptional strength-to-weight ratio and corrosion resistance make it a preferred choice for high-performance, long-life armor applications. Sweden’s capabilities in metallurgical innovation continue to solidify its importance in the global advanced armor materials market.

Competitive Landscape: Global Leaders Advancing UHMWPE, Aramid Fibers, Ceramics & Armored Steel

The Armor Materials competitive landscape is dominated by companies leveraging advanced fiber science, ceramic engineering, armored steel metallurgy, and integrated soldier protection systems. Market leadership is shaped by R&D strength, compliance with emerging NIJ/ STANAG standards, vertically integrated production capabilities, and the ability to supply high-volume defense modernization programs.

DuPont de Nemours, Inc. - Advancing Aramid Fiber Innovation for Next-Generation Body Armor

DuPont maintains global leadership in aramid fibers (Kevlar®), which form the backbone of soft armor and composite armor systems worldwide. The 2024 launch of Kevlar® EXO strengthens its position by offering improved flexibility, lighter weight, and compatibility with NIJ 0101.07 certification pathways. DuPont’s materials protect a vast majority of global defense and police personnel, creating high entry barriers due to exceptional ballistic consistency, reliability, and vertically integrated fiber engineering.

Avient Corporation - Expanding UHMWPE Composites Through Dyneema® Innovations

Avient is a top-tier manufacturer of UHMWPE fiber (Dyneema®), used extensively in ultra-lightweight hard armor, helmets, and tactical gear. The Dyneema® woven composite introduced in July 2025 showcases major performance gains, including 34% weight reduction and significantly higher abrasion resistance. Avient is also expanding UHMWPE applications across aerospace and consumer markets, while retaining firm leadership in personal ballistic protection systems.

3M Company - Supplying Advanced Ceramics & Transparent Armor Through Ceradyne

3M (via Ceradyne) is a major supplier of Boron Carbide (B4C) and Silicon Carbide (SiC) ceramic components used in ESAPI-grade plates and transparent armor systems. Its sharpened post-spin-off industrial strategy prioritizes safety, defense, and electronics - all high-growth markets requiring advanced armor materials. Ceradyne’s established U.S. presence ensures reliable ceramic supply for military plate programs, multi-hit solutions, and transparent armor assemblies.

SSAB AB - Leading Global Producer of High-Hardness Armored Steel (Armox® Series)

SSAB’s Armox® line is a benchmark for ballistic-grade armored steel, offering 500 HBW hardness combined with exceptional toughness suited for vehicle hulls, protected cabins, and blast-resistant structures. SSAB’s metallurgical expertise supports production of thinner, lighter, yet stronger steel armor - enabling weight reductions essential for mobility-centric military and civilian armored platforms. The company continues to drive innovation in quenched and tempered steels tailored for STANAG-rated vehicle protection.

Point Blank Enterprises, LLC - Dominant Supplier of Modular Body Armor Systems

Point Blank Enterprises is a major U.S. defense supplier specializing in modular soft and hard armor systems. Its USD 215 million U.S. Army contract (March 2024) demonstrates strong operational volume and trust across federal procurement channels. With a portfolio spanning NIJ Level IIA to Level IV, the company serves thousands of defense and law-enforcement agencies globally, supporting modularity, mobility, and enhanced survivability.

Avon Protection plc - Integrated Head & Body Protection Systems for Military Modernization

Avon Protection delivers advanced soldier survivability systems, including IHPS ballistic helmets, body armor elements, respiratory protection, and integrated combat systems. Its USD 204 million Direct OEM contract (February 2024) solidified long-term supply for the U.S. Army’s next-generation head protection program. Avon’s capability to merge ballistic protection with communication, respiratory, and ergonomic features positions it as a preferred partner across NATO and allied forces.

Armor Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$29.2 Billion

|

|

Market Size (2035)

|

$63.6 Billion

|

|

Market Growth Rate

|

8.1%

|

|

Segments

|

By Material Type (Advanced Composites, Ceramics, High-Performance Fibers, Metals & Alloys, Nanomaterials), By Application (Vehicle Armor, Body Armor, Aerospace Armor, Marine Armor, Civil Armor), By Protection Level (Personal Protection, Vehicle Protection), By Solution Type (Passive Armor, Reactive Armor, Active Protection Systems Components)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DuPont de Nemours Inc., Teijin Limited, Honeywell International Inc., 3M Company, CeramTec GmbH, CoorsTek Inc., BAE Systems plc, Rheinmetall AG, Morgan Advanced Materials plc, ATI Inc., Avient Corporation, Plasan Sasa Ltd., Saint-Gobain S.A., SSAB AB, Nurol Teknoloji

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Armor Materials Market Segmentation

By Material Type

- Advanced Composites

- Ceramics

- High-Performance Fibers

- Metals & Alloys

- Nanomaterials

By Application

- Vehicle Armor

- Body Armor

- Aerospace Armor

- Marine Armor

- Civil Armor

By Protection Level

- Personal Protection

- Vehicle Protection

By Solution Type

- Passive Armor

- Reactive Armor

- Active Protection Systems (APS) Components

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Armor Materials Market

- DuPont de Nemours, Inc.

- Teijin Limited

- Honeywell International Inc.

- 3M Company

- CeramTec GmbH

- CoorsTek, Inc.

- BAE Systems plc

- Rheinmetall AG

- Morgan Advanced Materials plc

- ATI Inc.

- Avient Corporation

- Plasan Sasa Ltd.

- Saint-Gobain S.A.

- SSAB AB

- Nurol Teknoloji

*- List not Exhaustive