Advanced Ceramics Market Overview: High-Purity Innovation, Performance Reliability & Strategic Growth Metrics to 2035

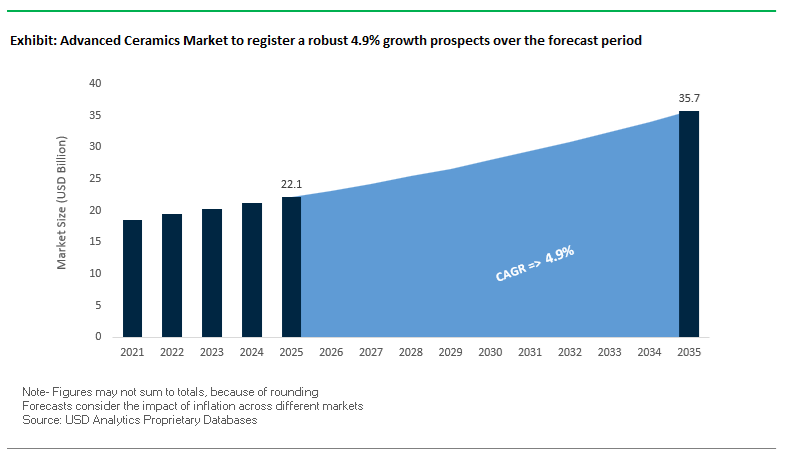

The Global Advanced Ceramics Industry, valued at USD 22.1 billion in 2025 and projected to reach USD 35.7 billion by 2035 at a 4.9% CAGR, is entering a phase of accelerated, technology-led transformation driven by the escalating performance demands of EVs, semiconductors, defense systems, telecommunications, medical devices, and high-precision industrial equipment. As OEMs push for materials capable of withstanding extreme temperatures, achieving ultra-high purity levels (up to 99.999%), enabling high-frequency signal integrity, and supporting compact high-power architectures, advanced ceramics are becoming indispensable to next-generation product design.

Industry leaders are prioritizing ceramic solutions that deliver superior thermal conductivity, fracture toughness, dielectric stability, chemical inertness, and dimensional precision, reshaping procurement standards and long-term technology roadmaps. Growth is powered by the rapid deployment of EV thermal management modules, the stringent material reliability needs of semiconductor manufacturing tools, rising defense investments in hypersonic and directed-energy platforms, and the global shift toward low-loss, high-frequency ceramics for 5G/6G networks.

Key Insights in the Advanced Ceramics Value Chain

Business development managers are focusing on sustained investment in fine ceramics engineering, AI-enabled process monitoring, automated powder handling, and proprietary ceramic composite systems engineered for ultra-demanding conditions such as hypersonic flight, high-frequency mmWave communications, and minimally invasive surgical tools.

- EV Substrate Reliability Benchmark: Silicon Nitride (Si₃N₄) substrates deliver 10x higher thermal cycling life than alumina, making them indispensable for EV inverter power modules.

- Semiconductor Purity Threshold: Ultra-high-purity alumina/yttria components exceeding 99.999% purity are now standard to safeguard yields in 5nm-and-below semiconductor processes.

- Defense-Funded Ceramic Innovation: U.S. DoD and India's iDEX scheme collectively channel >$100 million annually into hypersonic ceramics and transparent armor systems.

- 5G/6G Ceramic Performance Metrics: Low-loss ceramic substrates achieving εr = 5–8 and tanδ < 0.0005 are essential for mmWave signal integrity in next-generation telecom infrastructure.

- Medical Micro-Ceramics Demand: Piezoelectric and zirconia components <100 µm thickness are driving innovation in minimally invasive surgical tools and micro-ultrasonic sensors.

Market Analysis: Strategic Developments, Purity Investments & Advanced Ceramic Breakthroughs

The Advanced Ceramics market experienced substantial strategic and scientific developments across 2025, reshaping demand patterns and technological adoption pathways. In October 2025, Corning Incorporated, in partnership with SGD Pharma, inaugurated a new Type I borosilicate glass tubing facility in Telangana, India, strengthening supply for injectable pharmaceutical packaging at a time when global biopharmaceutical pipelines are expanding. In the same month, new industrial evaluations confirmed that Si₃N₄ substrates combined with AMB technology deliver 6–8 MPa·m toughness, more than twice the value of AlN, reinforcing their position as the premium solution for EV power electronics durability.

In September 2025, Corning launched an advanced Gorilla® Glass Ceramic capable of surviving 10 repeated one-meter drops, raising durability standards for smartphones and rugged devices. Earlier, in February 2025, Kyocera announced full-scale development of an AI-powered O-RAN-compliant 5G virtualized base station, leveraging its fine ceramics expertise to enable fronthaul distances exceeding 40 km, demonstrating how ceramics and high-frequency antenna design converge in next-gen telecom systems.

The U.S. Department of Energy’s March 2025 funding commitments accelerated domestic production of advanced composite ceramics and high-purity SiC, a critical requirement for clean energy devices including inverters, high-voltage power modules, and industrial heat pumps. In parallel, a major semiconductor equipment supplier in March 2025 secured multi-year access to plasma-resistant Yttria-stabilized Zirconia (YSZ) components-evidence that the semiconductor industry is locking in long-term contracts for purity-critical ceramics as foundry expansions intensify.

Medical ceramics also advanced: in January 2025, a European producer achieved certification for new Zirconia-Toughened Alumina (ZTA) bearing surfaces offering superior wear resistance for orthopedic implants. Toward the end of Q4 2025, the UK reinforced its ambitions in ceramic technology by funding MICG to build a global center of excellence for energy-efficient, low-cost ceramic manufacturing, positioning the region as a competitive production hub for technical ceramics.

Key Trends Transforming the Advanced Ceramics Market

Trend 1: Silicon Nitride Qualification Accelerates for High-Stress Mechanical Components Across Automotive and Industrial Systems

Silicon Nitride (Si₃N₄) is evolving from a specialty technical ceramic into a mainstream engineering material for high-stress, high-value mechanical components. OEMs are increasingly approving Si₃N₄ as a direct metal replacement where durability, thermal stability, and lifetime fatigue resistance are mission-critical. One of the strongest drivers is its exceptional mechanical fatigue behavior—fully dense Si₃N₄ bearing grades have demonstrated rolling contact fatigue lives over 10× greater than high-performance bearing steels under identical high-load conditions. This performance differential is redefining expectations in high-speed rotors, hybrid bearings, precision mechanical assemblies, and advanced industrial machinery.

The material’s fracture toughness of ~6.5 MPa·m¹ᐟ² in Ceramic Injection Molded (CIM) components positions it as one of the few ceramics capable of resisting crack propagation in high-impact, cyclic-stress environments. This is opening pathways for qualification in critical engine components, precision cutting tools, and mechanical systems where failure tolerance is extremely low. Thermal performance is an equally important factor: Si₃N₄ maintains structural integrity above 1000°C and withstands rapid thermal cycling, enabling its integration into turbocharger rotors, glow plugs, and next-generation combustion technologies where heat shock resistance directly affects system efficiency and emissions.

Si₃N₄’s rapid qualification across multiple industries showcases a broader trend: advanced ceramics are no longer materials of last resort but are now being strategically engineered to replace metals in applications where reliability, longevity, and heat stability define competitive performance.

Trend 2: Ceramic Matrix Composites and Environmental Barrier Coatings Drive Propulsion and Energy System Upgrades

The push for higher efficiency in aerospace propulsion and power-generation systems has accelerated the development of Ceramic Matrix Composites (CMCs) and Environmental Barrier Coatings (EBCs) engineered to withstand temperatures beyond the capability of nickel superalloys. These high-performance ceramics are enabling hotter, lighter, and more fuel-efficient turbine architectures, reflecting one of the largest structural material transformations in modern aerospace engineering.

Commercial investment underscores the scale of this shift: GE Aviation’s $1.5 billion commitment to SiC/SiC CMC commercialization for LEAP and GE9X engine programs demonstrates industry confidence in ceramics as core enabling materials rather than experimental technologies. The market endorsement is further validated by engine order books—engines incorporating CMC components, such as the GE9X, accumulated over 700 pre-2020 presale orders worth approximately $29 billion. This confirms long-term adoption curves and establishes CMCs as foundational materials for future propulsion programs.

CMCs such as SiC/SiC operate 200–300°C higher than nickel superalloys, drastically reducing the need for complex cooling circuits. Lower cooling burden directly translates to improved thrust-to-weight ratios, fuel economy, and reduced engine mass, reinforcing CMCs’ strategic importance for both aerospace and high-temperature energy infrastructure. As turbine manufacturers expand next-generation architectures, advanced ceramics and barrier coatings will remain central to thermal efficiency gains and emissions reduction mandates.

High-Value Opportunities Emerging in the Advanced Ceramics Market

Opportunity 1: Ultra-Pure, Plasma-Resistant Ceramic Components for Next-Generation Semiconductor Fabrication Equipment

The semiconductor industry’s transition to sub-5 nm and 3 nm process nodes, coupled with the growth of SiC-based power electronics, is creating an unprecedented demand for ultra-pure, dimensionally stable, and plasma-resistant ceramic components inside leading-edge fabrication tools. Plasma etching chambers, CMP systems, and wafer handling equipment increasingly rely on ceramics to maintain process stability in environments where contamination risk, thermal load, and chemical exposure are extreme.

High-purity alumina (Al₂O₃), aluminum nitride (AlN), and silicon carbide (SiC) have become essential because of their superior resistance to fluorine-based plasmas, outperforming metal alternatives that degrade or shed particles under corrosive etching conditions. This directly contributes to improved wafer yield—a critical competitive metric at advanced nodes. Thermal management is an equally important driver: AlN substrates with thermal conductivities approaching 180 W/(m·K) offer unique advantages in high-performance computing and power device packaging, where thermal dissipation is a gating factor for reliability.

For CMP and wafer fixturing at extreme fabrication temperatures up to 1700°C, ceramics must meet purity specifications of 99.999%, ensuring virtually zero contamination risk while maintaining dimensional stability. These technical requirements are creating a robust growth pathway for ceramic substrate manufacturers, precision machining specialists, and ultra-pure material suppliers aligned with advanced semiconductor capital equipment markets.

Opportunity 2: Next-Generation Bioceramics for Enhanced Osseointegration, Infection Control, and Mechanical Reliability

Advanced ceramics are also establishing new frontiers in medical implants, moving far beyond traditional applications in orthopedic and dental components. The convergence of regenerative medicine, additive manufacturing, and bioactive materials science is opening opportunities for zirconia composites, porous bioceramics, biodegradable scaffolds, and antimicrobial implant materials.

Bioactive glasses such as 45S5 Bioglass® stand out for their ability to form hydroxyapatite-like layers upon contact with body fluids, enabling direct chemical bonding with bone. This osseointegration superiority over inert ceramics—such as standard zirconia—positions bioactive ceramics as a foundation for next-generation bone regeneration and implant stabilization strategies.

Breakthroughs in resorbable ceramics further expand clinical applications. Studies on 3D-printed calcium phosphate scaffolds demonstrate effective dual-antibiotic release (vancomycin + rifampin), producing significantly better bacterial reduction in implant-associated infections than conventional PMMA cement. These self-resorbable scaffolds combine structural support with localized antimicrobial performance, addressing long-standing challenges in orthopedic infection control.

Simultaneously, Y-TZP (yttria-stabilized tetragonal zirconia polycrystal) has become the gold standard for high-load dental and orthopedic implants because of its superior fracture toughness relative to alumina, reducing implant breakage risk and extending service life. As surgical innovation and personalized implant design accelerate, these advanced bioceramics will continue to expand market penetration in spine, dental, joint, and trauma applications.

Advanced Ceramics Market Share Analysis

Market Share by Material Type: Oxide Ceramics Lead with 47.9% Share

Oxide Ceramics dominate the Advanced Ceramics Market with a substantial 47.9% share in 2025, reflecting their unparalleled versatility, cost-efficiency, and deep integration across electrical, industrial, medical, and structural applications. Their leadership is rooted in a mature global supply chain and an optimal balance of electrical insulation, thermal stability, wear resistance, and biocompatibility, making them indispensable for MLCCs, substrates, insulators, dental implants, catalyst supports, and precision components. This commanding share is further reinforced by widespread use in consumer electronics and industrial automation—two sectors experiencing persistent long-term growth. Surrounding material categories reinforce the direction of market evolution: non-oxide ceramics, particularly silicon carbide, remain the fastest-expanding group as EVs, renewable energy systems, and high-power electronics shift decisively toward wide-bandgap semiconductor materials; piezoelectric ceramics (PZT) continue enabling billions of sensors, actuators, and imaging devices annually; bioceramics sustain premium margins tied to global healthcare expenditure; and glass-ceramics maintain relevance in specialty optics, dental restorations, and thermal-shock-resistant components. Collectively, these segments illustrate a market characterized by both high-volume oxide dominance and high-value innovation in non-oxide and functional ceramic technologies.

Market Share by Product Type/Form: Monolithic Ceramics Lead with 52.0% Share

Monolithic Ceramics hold the largest share at 52.0% in 2025, underscoring their position as the structural and functional backbone of the advanced ceramics industry. Their dominance reflects extensive adoption in mechanical seals, cutting tools, insulators, substrates, housings, wear parts, and high-temperature components, where fully sintered ceramic bodies provide unmatched hardness, chemical resistance, and long-term durability. The segment’s strength is supported by robust demand from electronics manufacturing, semiconductor equipment, industrial machinery, and medical implants—industries that rely on stable, high-specification ceramic components. Surrounding product categories highlight where the market is technologically heading: ceramic coatings enhance metal and composite components with thermal, corrosion, and wear resistance; ceramic matrix composites (CMCs) enable ultra-high-temperature, lightweight engine components for aerospace and energy turbines; ceramic powders and feedstock are growing rapidly with the expansion of additive manufacturing and precision pressing; and ceramic filters and targets support environmental controls, semiconductor fabrication, and specialty manufacturing. The ecosystem around monolithic ceramics confirms their central role while signaling strong growth in coatings, CMCs, and advanced feedstock materials.

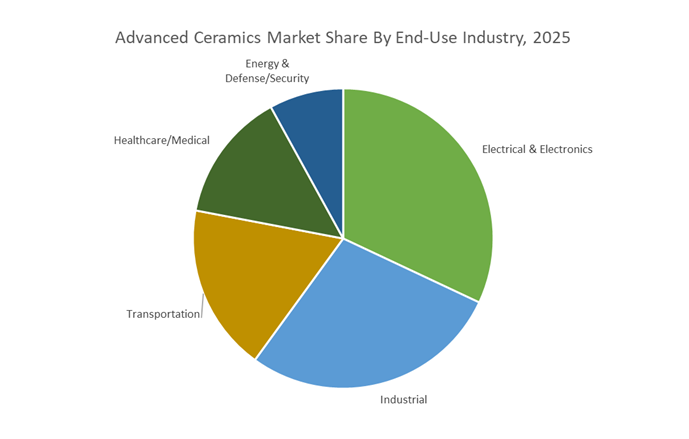

Market Share by End-Use Industry: Electrical & Electronics Leads with 32.2% Share

Electrical & Electronics is the largest end-use segment with a 32.2% share in 2025, driven by the explosive rise in semiconductor demand, the proliferation of MLCCs, and the rapid transition toward wide-bandgap power devices. Advanced ceramics are essential to the global electronics ecosystem, serving as dielectric materials in capacitors, substrates for integrated circuits, packages for high-frequency communication devices, and enablers for SiC-based power modules used in EVs and renewable energy converters. This segment’s dominance stems from the convergence of electrification, digitalization, and 5G/IoT deployment—all strong structural growth drivers. Complementary industry segments reinforce long-term market resilience: industrial applications provide reliable demand for wear-resistant and chemically inert ceramics; transportation increasingly depends on ceramics for sensors, emissions systems, and EV power electronics; healthcare relies on bioceramics for implants, dental applications, and imaging components; and energy & defense continue to invest in advanced ceramics for turbine engines, armor systems, and high-temperature insulation.

Country Analysis: Global Advanced Ceramics Market Innovation Hubs

United States: Expanding Leadership in Semiconductor-Grade Ceramics and Aerospace CMC Technologies

The United States continues to dominate the global advanced ceramics market through accelerated investments in semiconductor-grade ceramics, Ceramic Matrix Composites (CMCs), and next-generation ceramic engineering for defense and aerospace applications. The CHIPS for America Act remains a central driver of domestic high-purity ceramic manufacturing, significantly expanding production capabilities for Alumina, Aluminum Nitride (AlN), Silicon Carbide (SiC), and high-purity quartz components essential for etching, deposition, and lithography tools. This national push strengthens US independence in semiconductor materials while reinforcing its global competitiveness in microelectronics supply chains.

A major area of growth is CMC adoption across defense aviation, where the Department of Defense continues to issue large multi-year contracts for advanced CMCs designed to replace nickel-based superalloys in turbine hot sections. These materials drastically improve fuel efficiency and propulsion performance for next-generation jet engines. Simultaneously, US infrastructure modernization is boosting demand for wear-resistant industrial ceramics and advanced refractories, used extensively in chemical processing, high-temperature furnaces, and energy systems.

US research centers and ceramic leaders are also scaling AI-driven 3D printing of technical ceramics, enabling complex geometries and precision tolerances for medical devices, aerospace components, and microelectronics. In parallel, US university spin-offs are advancing bioceramic implants and glass-ceramics, supported by strong private-sector investment aimed at delivering long-lasting orthopedic and dental solutions with superior osseointegration. This multi-sector expansion firmly positions the United States as a global frontrunner in high-performance, defense-grade, and semiconductor-grade advanced ceramic technologies.

China: Accelerating Silicon Carbide Leadership and Ceramic Localization for EVs and Semiconductors

China is rapidly transforming into a global powerhouse for advanced ceramics, particularly Silicon Carbide (SiC) substrates, which are foundational for EV power electronics and 5G infrastructure. With strong state-backed financial incentives and subsidies, China has significantly increased domestic SiC wafer production capacity, reinforcing its ambitions to dominate the wide-bandgap semiconductor ecosystem. This growth is complemented by accelerated localization of high-purity ceramic components—including quartz and alumina electrostatic chucks—essential for semiconductor etching, deposition, and lithography tools.

Chinese industrial policy documents prioritize structural ceramics and functional ceramics as core technologies for national self-reliance. These materials are critical to high-temperature manufacturing, electronics, and energy systems. Additionally, China’s massive New Energy Vehicle (NEV) market is driving unprecedented demand for Silicon Nitride (Si3N4) ceramic bearings, substrates, and thermal management materials, owing to their high durability, thermal conductivity, and insulation performance.

The government’s aggressive decarbonization roadmap is further shaping ceramic material usage. National targets to standardize carbon accounting, carbon footprinting, and CCUS technologies align with China’s push to scale advanced ceramics in industrial decarbonization applications, particularly in steel and petrochemical sectors. As a result, China is solidifying its position as the world’s fastest-growing center for SiC, structural ceramics, and semiconductor ceramic components.

Japan: Advancing Electronic Ceramics, MLCC Miniaturization, and Quantum-Ready Ceramic Solutions

Japan remains a global leader in fine ceramics and functional ceramic technologies, particularly those enabling high-performance electronics, automotive systems, and quantum devices. Companies such as Murata Manufacturing continue to push innovations in Multilayer Ceramic Capacitors (MLCCs)—increasing capacitance density, thermal stability, and miniaturization to meet the demands of 5G devices, EV power electronics, and compact consumer electronics.

Japan is also making strategic advancements in ceramic packaging for quantum computing, with Kyocera showcasing next-generation solutions featuring hermetic sealing, ultra-high thermal stability, and superior insulating properties. These packaging solutions are vital for quantum processors and photonic systems, highlighting Japan’s early leadership in ceramics tailored for quantum technologies.

In the automotive sector, Japanese suppliers are expanding the use of piezoelectric ceramics in sensors, actuators, and engine controls—enhancing vehicle efficiency, emissions control, and advanced driver-assistance systems (ADAS). Moreover, Japan’s mastery in ultra-precise ceramic machining supports the production of complex geometries required for aerospace parts, implantable medical devices, and high-reliability industrial components. This combination of precision engineering and material innovation reinforces Japan’s long-standing dominance in fine electronic ceramics and emerging quantum technology applications.

Germany (Europe): Precision Structural Ceramics and Industry 4.0 Integration in Advanced Manufacturing

Germany continues to lead Europe’s advanced ceramics market through its strong engineering base, high-volume industrial manufacturing, and commitment to Industry 4.0 digitization. Companies like CeramTec play a pivotal role in delivering high-performance bioceramics for hip and knee implants, as well as silicon nitride and sialon-based structural ceramics for harsh industrial environments such as pumps, valves, and cutting tools. These materials offer unmatched wear resistance, corrosion resistance, and long-term durability—qualities essential to Germany’s industrial competitiveness.

Germany is also embedding IoT, automation, and cloud-based analytics into ceramic production processes through the national Plattform Industrie 4.0 initiative. This transformation enables defect-free manufacturing, real-time quality control, and highly efficient production workflows for advanced ceramic components across electronics, automotive, aerospace, and medical sectors.

Sustainability remains a top priority. The adoption of silicon nitride and sialons is rising in processing environments that require lower maintenance costs and reduced energy consumption. Additionally, the Made for Germany initiative—backed by €631 billion in pledged investments from 61 major companies—strengthens the nation’s R&D, production capacity, and innovation ecosystem across advanced materials, including advanced ceramics. These collective efforts position Germany as Europe’s anchor for structural ceramics, industrial innovation, and digital manufacturing excellence.

South Korea: Strengthening Global Competitiveness in Ceramic Battery Materials and Advanced Display Ceramics

South Korea’s innovation agenda in advanced ceramics is driven by its global leadership in EV batteries, OLED displays, and high-tech consumer electronics. Korean battery giants are investing extensively in ceramic-coated separators, which significantly enhance thermal stability, safety, and energy density in lithium-ion batteries used for high-performance electric vehicles. These ceramic coatings are becoming an industry standard as manufacturers transition to high-nickel chemistries and ultra-fast charging platforms.

South Korea is also pioneering advanced ceramic substrates for next-generation OLED and flexible displays, which require exceptional mechanical strength, thermal management, and optical clarity. These substrates support the country’s continuous leadership in premium-tier display technologies and foldable device markets.

A transformative area of development is solid-state battery (SSB) ceramic electrolytes, where major South Korean conglomerates are scaling R&D toward commercializing oxide- and sulfide-based ceramic electrolyte systems. These innovations position South Korea at the forefront of the global shift toward solid-state energy storage, with ceramics serving as a pivotal enabling technology.

United Kingdom: Advancing Bioceramics, Technical Ceramics, and High-Temperature CMCs Through R&D Hubs

The United Kingdom is emerging as a high-impact player in advanced ceramics innovation, supported by targeted government funding, regional R&D clusters, and strong aerospace and medical technology sectors. The Midlands Industrial Ceramics Group (MICG)—funded through UK Research and Innovation’s flagship Strength in Places Fund—aims to position the Midlands as a global hub for advanced ceramics manufacturing. This initiative enhances domestic capability, attracts foreign investment, and accelerates commercialization across structural, functional, and technical ceramics.

The UK has long-standing expertise in bioceramics, particularly materials used in regenerative medicine, dental restoration, and orthopedic implants. Research institutions are developing next-generation bioactive ceramics that promote enhanced tissue regeneration and long-term implant performance.

Additionally, the UK aerospace and gas turbine industries are driving advancements in high-temperature Ceramic Matrix Composites (CMCs). These materials are essential for improving turbine efficiency, reducing emissions, and enabling lightweight designs capable of withstanding extreme operational environments. With its strong technical foundation and collaborative R&D ecosystem, the UK continues to strengthen its role as an innovation hub in advanced ceramics engineering.

Competitive Landscape: Production Capabilities, Advanced Ceramic Technologies & Strategic Direction

The competitive dynamics of the Advanced Ceramics Industry are shaped by vertical integration, proprietary powder technologies, sustained R&D in high-purity formulations, and strong alignment with next-generation sectors such as semiconductors, EVs, aerospace, and biomedical implants. Leading companies are differentiating through materials purity management, micro-device manufacturing capability, advanced substrate engineering, and end-use specialization in telecom, orthopedics, and defense.

Kyocera Corporation - Fine Ceramics Powering 5G/6G Infrastructure and Automotive Electronics

Kyocera leads global fine ceramics production with a portfolio spanning semiconductor packages, ceramic substrates for power modules, and precision cutting tools. The company is strategically prioritizing 5G/6G base-station components, mmWave-compatible antenna modules, and ceramics for automotive ADAS and EV electronics. Its repeated appearance on WSJ’s list of “World’s 100 Most Sustainably Managed Companies” underscores its long-standing leadership in sustainable, precision ceramics manufacturing.

CoorsTek, Inc. - High-Purity Technical Ceramics for Semiconductor, Aerospace and Defense

CoorsTek operates one of the industry’s largest technical ceramics platforms with over 400 proprietary formulations, covering alumina, zirconia, and high-performance SiC. Its focus on semiconductor etching/deposition components and defense-related ceramic armor positions it as a key supplier for purity-critical and mission-critical applications. Vertical integration-powder processing to finished components-gives CoorsTek unmatched material consistency and enables rapid customization for aerospace, industrial, and defense buyers.

Saint-Gobain S.A. - High-Performance Ceramic Materials for Renewable Energy and Sustainable Construction

Saint-Gobain maintains a strong ceramics portfolio including boron nitride, SiC grains, and fused alumina for industrial processes. The company is investing in sustainable construction materials and renewable energy ceramics, such as high-temperature ceramics for solar panel manufacturing and heat recovery systems. Operating in 75+ countries, Saint-Gobain integrates advanced ceramics across abrasives, refractories, and engineered components, reinforcing its global dominance in high-performance materials.

Corning Incorporated - Glass & Ceramic Science Innovations for Electronics and Pharmaceutical Systems

Corning’s dual leadership in advanced glass and ceramic science enables it to pioneer products such as Gorilla® Glass Ceramic, MACOR® machinable ceramics, and high-tech substrates for life sciences. Its expansion into pharmaceutical glass tubing and next-gen durable cover materials demonstrates its deep expertise in strengthening, optical clarity, and thermal resistance. Corning remains uniquely positioned to merge optics, ceramics, and precision manufacturing for next-generation consumer electronics and drug-delivery systems.

Morgan Advanced Materials plc - Ceramics, Carbon, and Insulation for High-Reliability Industrial Applications

Morgan Advanced Materials specializes in technical ceramics, high-temperature insulation, and piezoelectric materials used in aerospace gas turbines, high-voltage systems, and medical devices. The company’s strategic focus on electrification-including ceramic-to-metal seals and high-voltage insulation-aligns with surging demand from EVs and grid infrastructure. Its portfolio serves environments where failure is unacceptable, making it a key material supplier for defense, healthcare, and energy-critical components.

CeramTec GmbH - Bioceramics and High-Performance Ceramics for Orthopedics and Automotive Systems

CeramTec is a global leader in bioceramics with renowned BIOLOX® medical materials, supporting orthopedic implant longevity and biocompatibility. The company continues advancing high-performance ceramics for automotive components (e.g., turbocharger and engine parts) and precision piezo-ceramics. Its long clinical track record and deep expertise in medical-grade ceramics position CeramTec as a major supplier to global orthopedic markets and high-reliability engineering applications.

Advanced Ceramics Market Report Scope

Advanced Ceramics Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$22.1 Billion

|

|

Market Size (2035)

|

$35.7 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Material Type (Oxide Ceramics, Non-Oxide Ceramics, Glass-Ceramics, Piezoelectric Ceramics, Bioceramics), By Product/Form (Monolithic Ceramics, Ceramic Matrix Composites, Ceramic Coatings, Ceramic Filters, Ceramic Powders, Target Materials), By End-Use Industry (Electrical & Electronics, Transportation, Healthcare/Medical, Defense & Security, Energy, Industrial), By Application Function (Structural Ceramics, Functional Ceramics, Bioceramics)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kyocera Corporation, Morgan Advanced Materials plc, CeramTec GmbH, CoorsTek Inc., Murata Manufacturing Co. Ltd., Saint-Gobain S.A., 3M Company, Corning Incorporated, NGK Insulators Ltd., SCHOTT AG, Rauschert GmbH, Nippon Carbon Co. Ltd., H.C. Starck GmbH, TOTO Ltd., Vesuvius plc

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Advanced Ceramics Market Segmentation

By Material Type

- Oxide Ceramics

- Non-Oxide Ceramics

- Glass-Ceramics

- Piezoelectric Ceramics

- Bioceramics

By Product Type / Form

- Monolithic Ceramics

- Ceramic Matrix Composites

- Ceramic Coatings

- Ceramic Filters

- Ceramic Powders

- Target Materials

By End-Use Industry

- Electrical & Electronics

- Transportation

- Healthcare / Medical

- Defense & Security

- Energy

- Industrial

By Application Function

- Structural Ceramics

- Functional Ceramics

- Bioceramics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Advanced Ceramics Market

- KYOCERA Corporation

- Morgan Advanced Materials plc

- CeramTec GmbH

- CoorsTek, Inc.

- Murata Manufacturing Co., Ltd

- Saint-Gobain S.A

- 3M Company

- Corning Incorporated

- NGK Insulators, Ltd.

- SCHOTT AG

- Rauschert GmbH

- Nippon Carbon Co., Ltd

- H.C. Starck GmbH

- TOTO Ltd

- Vesuvius plc

*- List not Exhaustive