Market Overview: Implant Performance Metrics Shape the Global Bioceramics Market Outlook

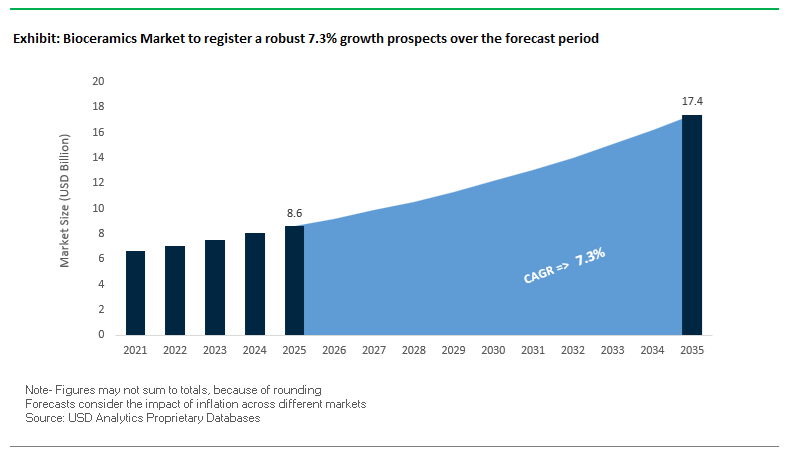

The global Bioceramics market is estimated at USD 8.6 billion in 2025 and is projected to reach USD 17.4 billion by 2035, registering a robust CAGR of 7.3% (2025–2035). For Bioceramics manufacturers and implant vendors, market growth is closely tied to quantifiable performance gains in implant longevity, mechanical strength, fracture toughness, and tissue integration. Advanced alumina, zirconia, zirconia-toughened alumina (ZTA), calcium phosphate cements, β-TCP scaffolds, and bioactive ceramics are increasingly specified in orthopedic, dental, and regenerative medicine applications where data-backed reliability is non-negotiable. OEMs and material suppliers that can consistently meet these stringent mechanical and biological benchmarks are best positioned to capture premium demand in joint arthroplasty, dental restorations, and tissue engineering.

Key Bioceramics performance insights for manufacturers and vendors

- Ultra-low wear in joint arthroplasty: Ceramic-on-ceramic (CoC) bearings based on alumina and ZTA Bioceramics used in total hip arthroplasty typically achieve wear rates <0.005 mm³ per year, significantly extending implant longevity versus conventional metal-on-polyethylene systems.

- Mechanical compatibility with cancellous bone: Self-setting calcium phosphate cements (CPCs) used as bone void fillers can achieve compressive strengths from ~1 MPa to 74 MPa, with optimal formulations engineered to match human cancellous bone in the 4–12 MPa range.

- High-strength dental applications: Yttria-stabilized zirconia (Y-TZP) Bioceramics for crowns and bridges exhibit bending strength up to ~1,200 MPa, enabling resistance to high chewing forces while supporting aesthetic, metal-free restorations.

- Fracture-tough femoral heads: Alumina Bioceramics for high-stress femoral heads must deliver fracture toughness above 4 MPa·m½, while ZTA composites often exceed this threshold to virtually eliminate fracture risk in younger and more active patient cohorts.

- 3D-printed scaffold porosity for regeneration: 3D-printed β-TCP scaffolds for bone regeneration are designed with interconnected pores ≥100 µm, actively promoting angiogenesis and rapid osteoconduction, a key differentiator for regenerative bioceramic product lines.

Market Analysis: Clinical Evidence, R&D and Capacity Expansion Accelerate Bioceramics Adoption

The global Bioceramics market is being reshaped by a combination of capacity expansion in medical ceramics, maturing clinical data on 3D-printed bioceramic implants, and intensifying pharma–biotech collaboration around drug-eluting and regenerative solutions. In October 2025, KYOCERA Fineceramics Medical GmbH inaugurated a new production facility in Waiblingen, Germany, dedicated to BIOCERAM AZUL® zirconia-based ceramic ball heads for orthopedic implants, signaling a major European capacity boost and underscoring OEM preference for premium, high-mechanical-strength Bioceramics. In April 2025, Lithoz reported five-year clinical follow-up data on 3D-printed β-TCP implants for mandibular osteotomy, achieving a 92.9% success rate and robust bone regeneration; this is a pivotal proof point for ceramic additive manufacturing as surgeons and device companies transition from pilot-scale trials to routine clinical use of patient-specific bioceramic implants.

The Bioceramics industry is also influenced by broader pharma and digital clinical trial consolidation, which directly impacts regulatory pathways for drug-eluting and bioactive ceramics. In November 2025, Merck & Co. agreed to acquire Cidara Therapeutics, a transaction centered on antiviral candidates but emblematic of wider pharma–biotech consolidation that will affect R&D models for drug-eluting bioceramic platforms. In December 2025, Thermo Fisher Scientific announced the acquisition of Clario Holdings, expanding its digital clinical trial and data capabilities—critical infrastructure for designing, monitoring, and validating long-term clinical trials for bioceramic implants and combination products. Also, in November 2025, Kyocera Fineceramics Europe showcased advanced ceramic materials for medical devices at Compamed 2025, emphasizing oxide and composite Bioceramics for next-generation medical technology and reinforcing the importance of Europe as an innovation and commercialization hub.

Academic and industrial research is further strengthening the technical foundation of the Bioceramics market. In May 2025, research on zirconia–alumina composites demonstrated that compositions with 70 wt% zirconia achieved an optimum compressive strength of around 370 MPa, guiding formulation strategies for high-load-bearing bioceramic components. April 2025 saw Northern Illinois University launch a new Biomaterials and Tissue Engineering Laboratory focused on novel bioactive ceramics for regenerative applications, adding to the R&D ecosystem that feeds commercial pipelines. Meanwhile, CoorsTek Bioceramics’ expansion of its distribution network in Asia, announced in 2022 and still driving growth, continues to support rising regional demand for ceramic femoral heads and liners in emerging orthopedic markets. Collectively, these developments point to a market where clinical validation, process innovation, and regional capacity expansion are interlinked drivers of long-term Bioceramics demand.

Breakthrough Toughening Mechanisms and Clinical-Grade Regenerative Platforms Driving Next-Generation Bioceramics

Market Trend 1: Rapid Clinical Adoption of Zirconia-Toughened Alumina (ZTA) for High-Reliability Hip and Knee Joint Bearings

A dominant trend reshaping the Bioceramics Market is the accelerated shift toward zirconia-toughened alumina (ZTA) composites, especially in next-generation hip and knee bearings. Traditional monolithic alumina, with a fracture toughness (KIC) of ~4 MPa·m½, is being surpassed by ZTA composites—such as Biolox® Delta—capable of achieving ≥6–8 MPa·m½, representing as much as a 100% improvement in crack resistance. This performance enhancement stems from the stress-induced tetragonal-to-monoclinic transformation of zirconia, which causes a ~4% local volume expansion that diverts and blunts propagating cracks.

ZTA’s clinical appeal is further strengthened by its complete resistance to low-temperature degradation (LTD)—a phenomenon that previously limited the adoption of 3Y-TZP zirconia. Accelerated hydrothermal aging tests equivalent to 40–80 years in vivo (50 hours at 134°C, 2 bar) reveal no detectable tetragonal-to-monoclinic transformation, validating long-term phase stability. In hip simulator studies—particularly under microseparation or shock loading—ZTA demonstrates significantly reduced volumetric wear and lower surface roughness relative to monolithic alumina, strengthening its role in high-demand joint arthroplasty. Chromium oxide (Cr₂O₃) additives restore hardness lost during zirconia inclusion, enabling ZTA to reach ≈1,900 HV, outperforming even premium alumina grades (~1,400 HV). These material advancements position ZTA as the gold-standard ceramic for ultra-low wear, high-durability orthopedic bearings.

Market Trend 2: Surge in 3D-Printed, Hierarchically Porous Bioceramic Scaffolds for Maxillofacial and Craniofacial Regeneration

The second major trend involves the rapid adoption of 3D-printed bioceramic scaffolds engineered with precise hierarchical porosity for craniofacial, maxillofacial, and bone-defect reconstruction. Additive manufacturing enables tight control of macropores between 300–600 μm, with evidence suggesting that 500–800 μm ranges maximize vascularization and osteointegration. Such pore sizes support optimal bone ingrowth, nutrient transport, and mechanical anchorage.

Complementing macropores, engineered bioceramics typically require 65–90% total porosity to enable cell infiltration, while intrinsic microporosity (<100 μm, often ≥30 vol%) resulting from sintering promotes protein adsorption and nutrient diffusion—both essential for biological fixation. The ability to fine-tune lattice geometry using gyroid, diamond, and other architected structures allows manufacturers to match scaffold stiffness to native cancellous bone (0.01–3 GPa). This prevents stress shielding while maintaining structural integrity, helping clinicians meet the most advanced reconstruction requirements across trauma, oncology, pediatric craniofacial repair, and dental implantology.

Market Opportunity 1: Bioactive Glass-Ceramic Coatings with Antibacterial Ion Release for Complex and Infected Bone Defect Management

A major commercial opportunity is emerging around bioactive glass-ceramic coatings engineered with antibacterial ions such as Ag⁺ and Cu²⁺ to treat infected bone defects and prevent implant-associated infections. These coatings consistently demonstrate 3-log to 5-log bacterial reductions—equivalent to 99.9%–99.999% kill rates—against pathogens like Staphylococcus aureus and Pseudomonas aeruginosa within 24 hours. The antibacterial efficacy follows a dual mechanism:

- Ion-doped antimicrobial action, disrupting bacterial membranes and inhibiting replication.

- Intrinsic alkalinization, where the base bioactive glass (e.g., 45S5) releases Na⁺/Ca²⁺ ions that raise local pH from ~7 to ~10, creating an environment hostile to biofilm formation.

Beyond infection control, these coatings quickly transition into an osteogenic phase. As the surface converts into hydroxycarbonate apatite (HCA)—a mineral chemically analogous to native bone—they promote osteoblast adhesion and osteoprogenitor differentiation. Critically, optimized coatings maintain a sustained antibacterial ion release profile at concentrations lethal to bacteria but non-toxic to osteoblasts, enabling their use in revision arthroplasty, trauma implants, spinal cages, and dental applications.

Market Opportunity 2: Injectable, Self-Setting Bioceramic Pastes for Minimally Invasive Procedures and Hard-Tissue Preservation

The second major opportunity centers on injectable, self-setting bioceramic pastes, especially calcium phosphate cements (CPCs), for minimally invasive procedures such as vertebroplasty, kyphoplasty, and alveolar ridge preservation. These CPCs are engineered to maintain injectability through ≤8-gauge (≤1.5 mm) needles, enabling precise delivery with reduced surgical trauma. Their hydration-based, non-exothermic setting reaction ensures that, unlike PMMA cements (which reach ~60°C), CPCs avoid thermal necrosis and preserve surrounding tissue viability.

From a mechanical perspective, fully set CPCs achieve compressive strengths of 20–50 MPa, adequate for vertebral body stabilization and craniofacial use, although still lower than PMMA. Their rheology is carefully controlled to provide a 2–4 minute working time, preventing premature setting while minimizing leakage risk. These materials provide a strong platform for local drug delivery, bioactive ion release, and regeneration in compromised bone sites. As minimally invasive orthopedic and dental procedures grow globally, injectable CPCs represent one of the strongest high-value innovation vectors in the bioceramics landscape.

Bioceramics Market Share Analysis

Market Share by Biocompatibility Type: Bio-Inert Ceramics Dominate Due to Superior Mechanical Strength and Long-Term Implant Stability

Bio-inert ceramics hold the largest share of the bioceramics market—approximately 55% in 2025—because materials such as alumina (Al₂O₃) and zirconia (ZrO₂) deliver unmatched performance for permanent, load-bearing, and aesthetically sensitive medical applications. Their exceptional mechanical strength, high fracture toughness, and outstanding wear resistance make them indispensable for orthopedic and dental implants that must withstand decades of mechanical stress without degradation. Zirconia’s superior flexural strength and natural tooth-like color have made it the material of choice for dental crowns, bridges, and implant abutments, while alumina’s ultra-low wear rates support its continued use in hip prostheses and articulating orthopedic surfaces. The chemical inertness of these materials ensures excellent biocompatibility, minimizing inflammatory response, corrosion, or leaching into surrounding tissues—critical for long-term implant survival. High dimensional stability and predictable behavior under physiological conditions further reinforce their dominance across both restorative dentistry and high-stress orthopedic applications. As demand grows for metal-free implants and next-generation ceramic components with improved aesthetics and mechanical reliability, bio-inert ceramics remain the backbone of the global bioceramics market.

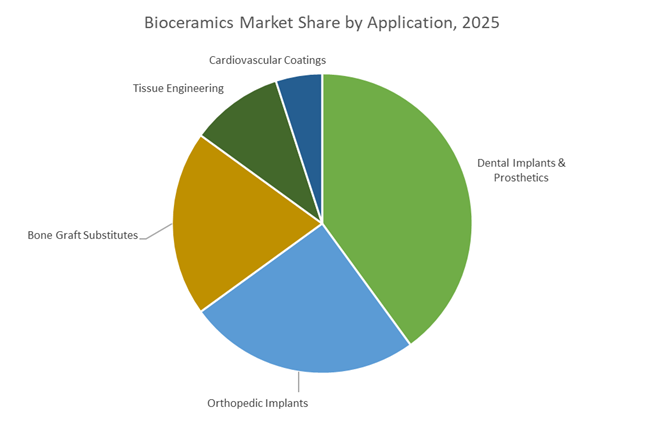

Market Share by Application: Dental Implants & Prosthetics Lead Due to High Demand for Aesthetic, Durable, and Biocompatible Restorations

The Dental Implants & Prosthetics segment accounts for nearly 40% of the global bioceramics market, supported by surging demand for metal-free, high-strength, and aesthetically superior restorative solutions. The rapid transition toward zirconia-based crowns, bridges, and abutments—driven by their lifelike appearance, excellent biocompatibility, and durability—has significantly expanded ceramic usage in both cosmetic dentistry and implantology. As tooth loss, periodontal disease, and age-related oral health issues rise globally—particularly in aging populations—demand for long-lasting dental restorations continues to climb. Bioceramics also play a vital role in root repair materials, fillers, bone graft substitutes, and coatings that enhance osseointegration in titanium implants. Increasing disposable incomes, the growth of cosmetic and restorative dentistry, and a strong shift toward premium dental materials in both developed and emerging markets further elevate the segment’s market share. Because each restoration or implant represents a high-value, high-margin consumable, dental applications remain the single largest revenue driver in the bioceramics market, anchoring long-term industry growth.

Country Analysis: Global Drivers in Bioceramics Development

United States: Regenerative Medicine Leadership and Breakthroughs in High-Strength Zirconia, Bioactive Coatings, and 3D-Printed Bioceramic Scaffolds

The United States remains at the forefront of global bioceramics innovation due to its unmatched scale of orthopedic and dental surgeries and continuous advancements in materials science, 3D printing, and regenerative medicine. The U.S. dental implant market has seen rapid integration of smart implant technology, with 2024 innovations embedding biosensors into Zirconia and Titanium-PEEK hybrid implants capable of monitoring bone-level changes and infection markers with 98.5% accuracy. This technological shift underscores the growing role of bioceramics in next-generation diagnostic and therapeutic systems. Equally transformative is the surge in bioactive glass coatings engineered by U.S. research labs, which accelerate osseointegration by forming hydroxyapatite-rich layers, significantly improving healing timelines for dental and orthopedic implants.

The U.S. also leads in multilayered, fifth-generation Zirconia, which provides superior translucency and aesthetics compared to conventional 3Y-TZP, making it the material of choice in premium restorative dentistry. Manufacturers are simultaneously optimizing these advanced Zirconia compositions for rapid sintering workflows to improve lab efficiency. In parallel, U.S. universities and startups are pioneering 3D bioprinting of porous Zirconia-based scaffolds, combining CAD/CAM precision with architected porosity structures essential for bone defect reconstruction. With over 1.2 million joint replacements and 5 million dental implants performed annually, the United States continues to drive sustained, high-volume demand for Alumina, Zirconia, and bioactive bioceramic components across both load-bearing and restorative applications.

European Union (Germany, Switzerland, UK): Precision Machining, Bioinspired Scaffolds, and High-Reliability Zirconia for Dental and Orthopedic Implants

Europe’s bioceramics ecosystem is defined by strict regulatory standards, exceptional precision manufacturing capabilities, and robust research funding that supports next-generation regenerative scaffold technologies. Landmark EU-funded initiatives such as the €3.69 million BIOBONE project have strengthened Europe’s scientific leadership in developing bio-inspired composite bioceramics engineered to mimic the hierarchical structure of natural bone. These programs place strong emphasis on controlling mechanical strength, porosity, and resorption rates, enabling the fabrication of ceramic scaffolds suitable for complex bone defect repair.

Europe is also advancing high-precision 3D printing of silicate- and calcium-phosphate-based bioceramics, with research systematically mapping the influence of pore geometry on compressive strength and biological performance. Switzerland maintains global dominance in high-end Zirconia dental implants through companies like Institut Straumann AG, which focuses on materials optimized for superior soft-tissue response and highly aesthetic outcomes. Meanwhile, German manufacturers such as CeramTec GmbH operate fully integrated production systems for high-density Alumina and Zirconia orthopedic components, including hip and knee replacements that undergo stringent fatigue-life and wear-resistance certification. Combined, these developments position Europe as a strategic hub for premium, high-precision bioceramic implants and regenerative scaffold technologies.

China: Calcium Phosphate Industrialization, Bioactive Glass Scaling, and High-Volume Dental Bioceramics for Regenerative Care

China’s bioceramics market is undergoing rapid expansion due to rising healthcare demand, aggressive industrial scaling, and sustained investment in regenerative medicine. The country has established itself as one of the world’s largest producers of bioactive ceramics, particularly Hydroxyapatite and Bioactive Glass, which are essential for bone regeneration, dental implants, and orthopedic coatings. These materials are widely used as bulk implant components or as surface-active layers that enhance osteoconduction and promote rapid bone bonding—key priorities for China’s expanding orthopedic and dental markets.

Academic and industrial R&D are heavily invested in optimizing Hydroxyapatite composites reinforced with natural polymers such as chitosan and alginate. Recent studies highlight improvements in mechanical performance, achieving compressive strengths of approximately 9.01 MPa, suitable for cancellous bone reconstruction. Furthermore, China’s booming dental healthcare sector is driving mass-scale production of Zirconia and Alumina powders and finished prosthetics, benefitting from cost-efficient powder processing and advanced ceramic machining capabilities. These developments reinforce China’s strategic role as a high-volume production leader supplying Calcium Phosphate bioceramics, dental ceramics, and regenerative biomaterial inputs to global markets.

Japan: Vertical Integration of Bioceramic Device Manufacturing and Breakthroughs in ZTA Composites for Orthopedic Longevity

Japan maintains a premium position in the bioceramics industry through its vertically integrated material-to-device manufacturing capabilities and its focus on high-performance orthopedic and dental ceramics. In October 2025, Kyocera Corporation reorganized its medical division into Kyocera Medical Corporation, consolidating its strategy to expand production of advanced bioceramic components for orthopedic implants—specifically its BIOCERAM AZUL line known for superior durability and performance in joint replacement systems. This restructuring strengthens Japan’s ability to deliver fully integrated supply chains from raw ceramic powders to finished, regulatory-certified implant systems.

Japan is also a global leader in developing Zirconia Toughened Alumina (ZTA) composites, which offer enhanced fracture toughness, wear resistance, and long-term reliability—critical factors for extending the operational lifespan of ceramic-on-ceramic hip bearings. These innovations are particularly influential in markets demanding ultra-low wear rates and exceptionally high biocompatibility. Japanese manufacturers apply rigorous quality control and extensive material testing, ensuring their bioceramic devices maintain world-leading consistency and clinical performance. As Japan pushes innovation in orthopedic ceramics, dental restorative materials, and next-generation bioceramic composites, it continues to anchor the Asia-Pacific region in advanced bioceramics development.

Competitive Landscape: Leading Bioceramics Manufacturers and Implant Material Innovators

The global Bioceramics competitive landscape is characterized by a mix of specialized advanced ceramics manufacturers and diversified materials multinationals with strong medical portfolios. Players such as CeramTec, Kyocera, CoorsTek, Morgan Advanced Materials, and Ivoclar Vivadent occupy critical positions along the value chain, from bulk bioceramic powders and bearings to highly engineered dental blocks and hermetic feedthroughs for implantable electronics. Their strategies center on clinical track record, high-purity processing, CAD/CAM integration, and micro-precision manufacturing, all aimed at meeting stringent orthopedic, dental, and regulatory performance specifications.

CeramTec accelerates global leadership in BIOLOX hip joint Bioceramics

CeramTec GmbH is a world-leading manufacturer of advanced ceramics and a dominant supplier of ceramic bearings for orthopedics, with the BIOLOX® system ceramics at the core of its offering. Its BIOLOX® delta ZTA composites are widely used in hip joint implants, combining zirconia-toughened alumina to deliver exceptional fracture toughness and ultra-low wear rates in ceramic-on-ceramic bearings. The company’s clinical track record is a key competitive advantage, with tens of millions of BIOLOX® components implanted worldwide, evidencing long-term reliability and compliance with strict ISO and ASTM standards. CeramTec also secured FDA approval in 2020 for a novel surface treatment technology designed to further enhance the biocompatibility and wear resistance of ceramic femoral heads, and it is actively expanding into non-joint applications, including dental ceramics, spinal surgery components, and maxillofacial reconstruction biomaterials.

Kyocera expands BIOCERAM AZUL production for European orthopedic markets

Kyocera Corporation is a diversified technology leader with a strong position in high-performance and medical ceramics, notably through its BIOCERAM AZUL® zirconia-based Bioceramics for orthopedic hip replacements. BIOCERAM AZUL® is recognized for its high mechanical strength and distinct blue color, which offers both technical and branding differentiation in the premium hip implant segment. To better serve the European medical sector, Kyocera opened a new production facility in Waiblingen, Germany, in October 2025, dedicated to manufacturing and supplying BIOCERAM AZUL® products, significantly enhancing regional capacity and reducing supply-chain risk for OEMs. Beyond joint implants, Kyocera leverages its technical ceramics expertise to provide insulators, feedthroughs, and hermetic sealing components for implantable medical electronics such as pacemakers, where electrical safety and reliability are essential. The company’s strategic focus on micro-precision manufacturing of complex ceramic geometries with micrometer tolerances supports miniaturized, high-precision medical devices and advanced diagnostic and surgical tools.

CoorsTek scales Permallon bioceramic bearings for high-performance implants

CoorsTek, Inc. is a major global manufacturer of technical ceramics with a dedicated bioceramic implant division centered on its Permallon® alumina matrix composites. Permallon® ceramic bearing components are engineered specifically for total hip arthroplasty, providing high wear resistance and mechanical stability for long-term performance in demanding orthopedic applications. Since 2005, CoorsTek has supplied over six million critical ceramic implant components, operating under ISO 13485-certified and FDA-compliant quality systems that ensure stringent process control and traceability. The company is also a key supplier of custom ceramic components for implantable devices across neurological, cardiological, spinal, and orthopedic indications, supported by advanced forming and finishing capabilities. Strategically, CoorsTek invests heavily in R&D to further enhance the mechanical performance and fracture toughness of alumina–zirconia Bioceramics, with a particular focus on meeting the requirements of younger, more active patient populations.

Morgan Advanced Materials advances high-purity ceramic components for medical devices

Morgan Advanced Materials plc is a global engineering company specializing in high-performance materials, including advanced technical and structural ceramics used in medical applications. The company supplies high-purity alumina and zirconia ceramics for medical device components, diagnostic instruments, and fluid-handling systems where chemical inertness and biocompatibility are essential. In June 2025, Morgan announced real-time ceramic sintering research, demonstrating its commitment to optimizing manufacturing processes for high-density, high-purity ceramic products—an important differentiator for Bioceramics used in implants and medical hardware. Morgan also has deep expertise in combining ceramics with metals to create metallized ceramics and hermetic feedthrough assemblies for implantable electronics, ensuring reliable sealing and long-term performance in physiological environments. Additionally, the company is leveraging its materials science capabilities to support solid-state battery initiatives, which indirectly drives demand for advanced electrolyte ceramics and related processing technologies.

Ivoclar Vivadent drives CAD/CAM innovation in dental Bioceramics

Ivoclar Vivadent AG is a leading player in dental materials, with a strong focus on Bioceramics and CAD/CAM solutions for esthetic and restorative dentistry. Its portfolio includes IPS e.max® ZirCAD (zirconia) and IPS Empress® (leucite glass-ceramic) materials, which are widely used for crowns, veneers, and fixed partial dentures. These dental Bioceramics are engineered to combine high mechanical strength—zirconia can reach around 1,000 MPa flexural strength—with natural translucency, meeting demanding aesthetic and functional requirements in modern prosthodontics. Ivoclar is heavily invested in the digital dentistry workflow, supplying both sintered and presintered bioceramic blocks optimized for CAD/CAM milling systems to ensure precision fit and reproducible quality. The company also continuously innovates cementation and bonding systems specifically tailored to all-ceramic restorations, helping clinicians achieve long-term marginal integrity and reduce the risk of secondary decay, which in turn reinforces the clinical adoption of bioceramic dental solutions.

Bioceramics Market Report Scope

Bioceramics Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.6 Billion

|

|

Market Size (2035)

|

$17.4 Billion

|

|

Market Growth Rate

|

7.3%

|

|

Segments

|

By Biocompatibility Type (Bio-Inert Ceramics, Bio-Active Ceramics, Bio-Resorbable Ceramics), By Material Type (Alumina, Zirconia, Calcium Phosphate, Bioactive Glass, Silicon Nitride), By Application (Dental Implants & Prosthetics, Orthopedic Implants, Bone Graft Substitutes, Tissue Engineering, Cardiovascular Coatings)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

CeramTec, Kyocera, Zimmer Biomet, Stryker, Dentsply Sirona, Straumann, Tosoh, CoorsTek, Morgan Advanced Materials, dsm-firmenich, CAM Bioceramics, Shandong Sinocera, 3M, Nobel Biocare, Himed

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bioceramics Market Segmentation

By Biocompatibility Type

- Bio-inert Ceramics

- Bio-active Ceramics

- Bio-resorbable Ceramics

By Material Type

- Alumina

- Zirconia

- Calcium Phosphate

- Bioactive Glass

- Silicon Nitride

By Application

- Dental Implants & Prosthetics

- Orthopedic Implants

- Bone Graft Substitutes

- Tissue Engineering

- Cardiovascular Coatings

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Bioceramics Market

- CeramTec

- KYOCERA

- Zimmer Biomet

- Stryker

- Dentsply Sirona

- Straumann

- TOSOH

- CoorsTek

- Morgan Advanced Materials

- dsm-firmenich

- CAM Bioceramics

- Shandong Sinocera

- 3M

- Nobel Biocare

- Himed

*- List not Exhaustive

Research Coverage

The latest Bioceramics Market study from USDAnalytics provides a deep-dive technical and commercial assessment of how implant performance metrics are reshaping material selection across orthopedics, dental implants, and regenerative medicine. Drawing on clinical datasets, manufacturing benchmarks, and competitive moves, this report investigates the relationships between wear rates, fracture toughness, porosity architecture, and tissue integration to quantify where alumina, zirconia, ZTA, calcium phosphate cements, β-TCP scaffolds, and bioactive ceramics are gaining share. The study highlights breakthroughs in zirconia-toughened alumina bearings, 3D-printed scaffolds with hierarchical porosity, injectable self-setting cements, and bioactive glass-ceramic coatings with antibacterial ion release, while analysis reviews address how evolving regulatory expectations and digital clinical trial platforms are influencing approval timelines for next-generation bioceramic implants and combination products. With detailed coverage of supply chain expansions, regional demand shifts, and technology roadmaps, this report is an essential resource for executives, R&D leaders, product managers, and investors who need decision-grade insights on the global Bioceramics market landscape and its trajectory through 2035.

Scope Highlights

- Segmentation (Global Bioceramics Market Segmentation)

- By Biocompatibility Type: Bio-inert Ceramics, Bio-active Ceramics, Bio-resorbable Ceramics

- By Material Type: Alumina, Zirconia, Calcium Phosphate, Bioactive Glass, Silicon Nitride

- By Application: Dental Implants & Prosthetics, Orthopedic Implants, Bone Graft Substitutes, Tissue Engineering, Cardiovascular Coatings

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Timeframe Coverage: Historic data from 2021 to 2025 and detailed market forecasts from 2026 to 2034.

- Companies Covered: Analysis and profiles of 15+ leading Bioceramics manufacturers, implant OEMs, and advanced material innovators.