Market Overview: 4N High-Purity Alumina Emerges As A Strategic Input For EV Batteries, Leds, and Power Electronics

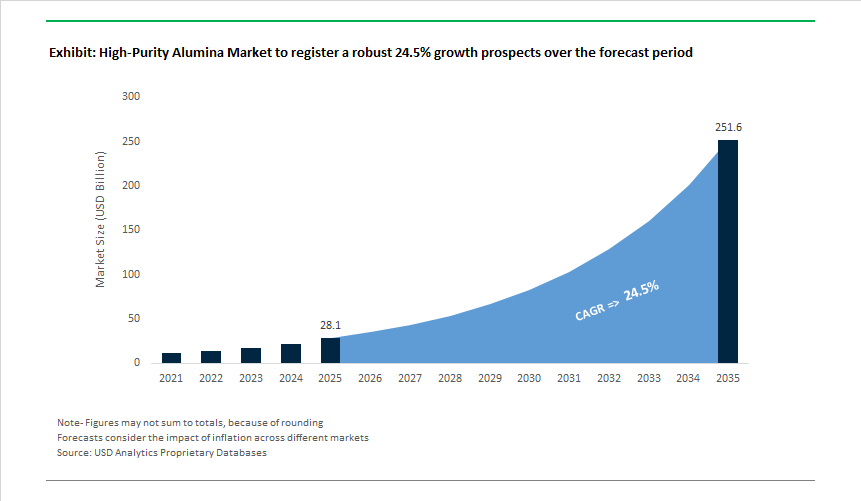

The High-Purity Alumina (HPA) market is valued at USD 28.1 billion in 2025 and is projected to surge to USD 251.4 billion by 2035, expanding at an exceptional 24.5% CAGR as ultra-high-purity ceramics become indispensable to energy storage, advanced lighting, and power electronics ecosystems. This growth is not volume-led; it is purity-led, with 4N (99.99%) HPA dominating demand due to its ability to meet the defect tolerance, thermal stability, and electrical insulation requirements of next-generation lithium-ion batteries and LED substrates.

In lithium-ion batteries, battery-grade HPA is now a non-negotiable input for ceramic-coated separators, where uniform particle size, low sodium content, and consistent alpha-phase alumina structure directly influence thermal runaway resistance and cycle life. As EV platforms move toward higher energy density cells and faster charging regimes, separator performance has become a system-level safety constraint, structurally increasing HPA loading per battery pack. OEMs and cell manufacturers increasingly lock in long-term HPA supply aligned to separator qualification cycles, elevating HPA from a specialty ceramic to a strategic upstream material in the battery value chain.

Parallel demand acceleration is occurring in LED and optoelectronics manufacturing, where 4N and higher-purity alumina is required for sapphire substrates used in high-brightness LEDs and UV applications. Here, HPA purity directly determines crystal yield, optical clarity, and thermal conductivity, making contamination control and consistency more critical than nominal capacity. As LED architectures evolve toward higher power densities and longer operating lifetimes, substrate-grade HPA specifications continue to tighten, reinforcing pricing power for qualified suppliers.

Over the forecast period, competitive positioning in the HPA market will be shaped by process control, impurity management, and scalable purification economics, rather than raw alumina availability. Producers capable of delivering stable 4N-grade output with tight control over trace metals, moisture, and phase purity - while scaling capacity to match battery and LED demand - will capture disproportionate value.

Market Analysis: Funded Capacity Scale-Ups, Joint Ventures, and Policy Signals Reshape the Global HPA Supply Base

The HPA industry’s recent development timeline demonstrates a clear shift from feasibility to funded scale-up and market diversification. In May 2024, Alpha HPA executed a final investment decision to build the world’s largest single-site HPA refinery in Gladstone, signalling project bankability for large-scale HPA supply. The following years saw strategic alliances and technology licensing that underpin feedstock and precursor stability-April 2024 KBR and Sumitomo Chemical formed a strategic alliance (propylene-oxide and related chemistries) that influences downstream HPA feedstock availability and sustainable synthesis routes.

The market combined public funding, JV deals and product launches to widen HPA end-use reach. March 2025 policy changes affecting Section 232 aluminum tariffs increased cost pressure on upstream aluminium chains and highlighted the commercial case for domestic HPA capacity in Western markets. Project financing milestones accelerated in May 2025 with Alcoa launching low-carbon EcoLum® billet initiatives that position integrated producers to offer lower-carbon HPA feedstocks. In April 2025, Impact Minerals announced a JV to commercialize an acid-leaching HPA route in Western Australia, reinforcing an Australia-based supply corridor for western customers. Major project funding continued into late 2025: October 2025 Alpha HPA secured a US$553 million second-stage funding tranche for Gladstone expansion and December 2025 Altech Chemicals strengthened downstream capability with an acquisition to serve medical and aerospace HPA formats.

High-Purity Alumina Market Trends and Opportunities

Market Trend 1: HPA as an Enabler for Large-Format Sapphire Glass in Semiconductor Manufacturing

The transition to sub-5nm semiconductor nodes is fundamentally reshaping materials selection inside wafer fabrication equipment, with high-purity alumina emerging as a critical enabler for sapphire-based components that meet zero-contamination requirements. As plasma etch and CVD processes intensify—both in power density and fluorine-based chemistry exposure—traditional quartz parts are exhibiting accelerated degradation, in some cases eroding up to 20% faster under high-energy plasma conditions. This reliability gap is pushing equipment OEMs toward sapphire glass grown exclusively from 4N and 5N HPA, where impurity control directly translates into longer tool uptime and higher wafer yields. In October 2025, Alpha HPA disclosed that its sapphire growth subsidiary achieved second-round qualification with a global GaN-on-sapphire semiconductor OEM, signaling that HPA-derived sapphire has crossed a critical industrial validation threshold. From a performance standpoint, industry benchmarks published in late 2025 indicate that HPA-based sapphire components maintain surface roughness below Ra < 0.1 μm even after prolonged high-temperature plasma exposure, dramatically reducing particulate shedding—one of the most persistent yield killers in advanced logic and memory fabs. This materials shift is also reinforcing supply-chain realignment, as seen in Altech Batteries’ March 2025 acquisition of a controlling stake in Advanced Ceramics Pty Ltd, aimed at vertically securing HPA output for semiconductor-grade sapphire and aerospace ceramics. Collectively, these developments position HPA not merely as a raw material, but as a structural enabler of next-generation fab reliability and contamination control.

Market Trend 2: Precision Specification of HPA Coatings for Next-Generation Li-ion Separators

Battery manufacturers are increasingly specifying high-purity alumina at the nanoscale to stabilize separators and active materials as lithium-ion chemistries push toward higher energy densities and more aggressive operating envelopes. The rapid adoption of silicon-dominant anodes and high-nickel cathodes such as NCM811 has exposed the thermal and mechanical limits of conventional polymer separators, particularly under fast-charging and high-voltage conditions. HPA is emerging as a preferred ceramic coating material because it combines exceptional dielectric strength with thermal stability well beyond the softening range of polyethylene or polypropylene membranes. In October 2025, Altech Batteries reported that its Silumina Anodes™, which apply a 2–3 nm HPA coating directly onto silicon particles, achieved 88.5% capacity retention after 500 cycles—an outcome that directly addresses silicon’s ~300% volumetric expansion during lithiation. Parallel academic work published in January 2025 demonstrated that HPA-stabilized separators exhibit thermal shrinkage of 0.8% at 160°C, compared to shrinkage exceeding 30% for uncoated PE separators, sharply reducing internal short-circuit risk. Manufacturing economics are also improving as sol–gel coating processes mature, enabling uniform HPA dispersion with minimal dead weight while maintaining dielectric breakdown voltages above 30 kV/mm. This convergence of electrochemical performance, thermal safety, and scalable coating economics is making HPA a default specification rather than an optional enhancement in next-generation battery architectures.

Market Opportunity 1: HPA for Advanced Semiconductor Packaging and Thermal Management

The acceleration of heterogeneous integration—spanning 2.5D interposers, 3D IC stacking, and HBM3 memory—has created a thermal management bottleneck that conventional organic substrates can no longer resolve. As AI accelerators and data-center processors push beyond 350 W per package, heat dissipation has become a limiting factor for performance scaling. High-purity alumina is emerging as a strategic material in this context, both as a filler in high-performance thermal interface materials and as a precursor for advanced ceramic substrates. According to disclosures from Alpha HPA in October 2025, demand for HPA-based thermal fillers in AI data-center applications is projected to increase 4.7× between 2026 and 2030, exceeding 8,000 tonnes per annum. A key differentiator in this segment is “low-alpha” HPA, produced via solvent extraction routes that eliminate trace uranium and thorium contaminants. This ultra-low radionuclide content is critical for preventing alpha-particle-induced soft errors in high-density memory and AI logic devices. Beyond fillers, HPA-derived aluminum nitride substrates are gaining traction due to their thermal conductivity of 170–230 W/m·K—nearly 300× that of FR-4—making them increasingly indispensable as liquid cooling replaces air cooling in advanced packaging. This positions HPA at the core of the semiconductor industry’s thermal evolution, with demand driven by architecture complexity rather than cyclical wafer volumes.

Market Opportunity 2: HPA-Based Adsorbents for Lithium Extraction and Water Treatment

Beyond electronics and energy storage, high-purity alumina is carving out a high-value role in environmental remediation and resource recovery, particularly where selectivity and chemical durability are paramount. Research published in RSC Advances in 2025 highlights processes that valorize lithium-extraction by-products into HPA-based aluminosilicate adsorbents capable of efficiently removing arsenic from mining effluents, aligning mineral production with circular economy principles. In parallel, activated alumina and zirconium-modified HPA adsorbents are being deployed in industrial wastewater systems to achieve up to 99% fluoride removal from spent lithium-ion battery leachates, a capability increasingly required under tightened environmental resilience frameworks introduced for 2025–2026. Perhaps most strategically, pilot-scale deployments of HPA-functionalized membranes for Direct Lithium Extraction are demonstrating lithium-to-magnesium selectivity coefficients an order of magnitude higher than conventional ion-exchange resins. This improvement has the potential to reduce the land footprint of lithium brine operations by as much as 80%, materially improving project economics and permitting outcomes. As water scarcity, mineral security, and hydrogen-linked lithium demand converge, HPA-based adsorbents are emerging as a niche but structurally important growth vector for the market.

Market Share Analysis: High-Purity Alumina Market

Market Share by Purity Grade: 5N High-Purity Alumina Becomes the Industry’s Zero-Defect Backbone

The 5N (99.999%) purity segment now captures the largest share of the High-Purity Alumina Market because it has moved from being a “premium option” to a process-critical material in battery safety, semiconductor reliability, and thermal management systems. As EV battery architectures and advanced semiconductor packages push toward higher energy density and tighter tolerances, even trace metallic contamination becomes economically catastrophic. The industry-wide acceptance of the sub-100 ppm impurity threshold has effectively disqualified 4N grades from next-generation applications, accelerating structural demand for 5N material. This shift is reinforced by the superior thermal conductivity of 5N HPA, which enables faster heat dissipation in epoxy mold compounds and power electronics—directly improving component lifespan and yield rates in fabs and battery plants. Importantly, 2025 marks a commercial inflection where particle engineering has become as important as chemical purity: near-spherical 5N morphologies now allow higher filler loading without viscosity penalties, reducing coating defects and manufacturing scrap. The result is a segment growing nearly twice as fast as the overall HPA market, driven not by price sensitivity but by risk avoidance, yield protection, and performance insurance—the exact attributes that anchor long-term market share in materials markets.

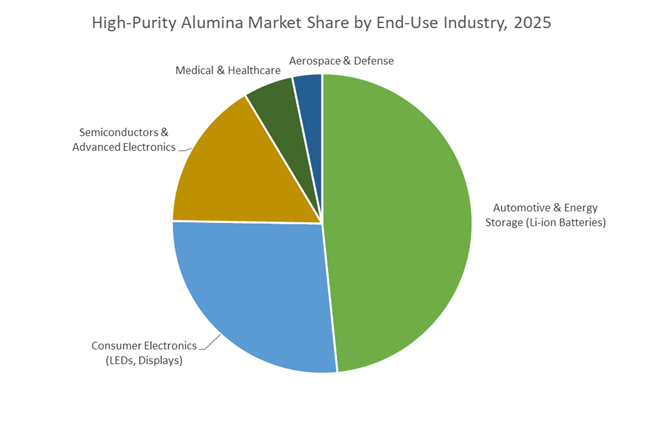

Market Share by End-Use Industry: Automotive and Energy Storage Redefine HPA’s Value Proposition

Automotive and energy storage have emerged as the dominant application segment because high-purity alumina has become a non-negotiable safety and performance enabler for lithium-ion and next-generation batteries. In EV platforms, the cost of battery failure—financial, regulatory, and reputational—far outweighs the marginal cost of ultra-pure materials, making 5N HPA a default specification rather than a discretionary upgrade. Alumina-coated separators that remain dimensionally stable beyond 200°C directly address thermal runaway risk, which is now the primary constraint on fast-charging and high-density cell designs. Beyond separators, the rapid adoption of HPA-coated silicon anodes has repositioned alumina from a passive insulator to an active performance multiplier, enabling step-changes in energy density and cycle life that conventional graphite systems cannot achieve. These gains translate into tangible OEM outcomes—longer driving range, lighter battery packs, and lower cost per kilometer—which explains why battery manufacturers are locking in long-term HPA supply agreements despite price volatility elsewhere in the materials stack. As EV penetration deepens and grid-scale storage expands, this application segment continues to absorb a disproportionate share of new 5N capacity, structurally cementing its leadership in the High-Purity Alumina Market.

Competitive Landscape: Incumbent Refiners and Technology Innovators Jockey For Scale, Purity and Downstream Formats

The competitive set blends large integrated alumina producers, specialty chemical groups and technology-centric juniors that target purity, powder morphology and application-specific HPA formats (powder, granule, pellets, advanced ceramic feedstock). Leaders differentiate through process choice (hydrolysis vs acid-leach), geographic footprint (Asia-Pacific vs secure Western supply), and product breadth across LED sapphire, electronic ceramics, and battery separator coatings.

Sumitomo Chemical: Hydrolysis Specialist Producing Consistent Powder HPA For Leds and Battery Coatings

Sumitomo Chemical leverages the hydrolysis of aluminum alkoxide to produce extremely fine, consistent HPA powders with an estimated annual HPA capacity near 1,500 tpa. The company’s HPA portfolio is tightly integrated into electronics and energy materials supply chains-supplying separator coatings and synthetic sapphire feedstock for blue LEDs and next-gen power electronics (GaN-on-GaN). Sumitomo’s vertical integration across chemical precursors supports rigorous quality control and positions it to serve demanding optoelectronics and battery coating customers.

Sasol Limited: Catalyst-Grade HPA Supplier With Customizable Surface Area and Porosity For Industrial Processes

Sasol’s PURALOX/CATALOX high-purity alumina hydrates are tailored as catalyst supports and binders for refining and specialty chemical processes; the company controls physicochemical properties (surface area, porosity) to meet slurry-bed and fixed-bed reactor specifications. Sasol’s global chemicals footprint and distribution network make it a reliable supplier of high-consistency HPA feedstocks for industrial ceramics and catalyst applications where tailored morphology is mission-critical.

Alcoa Corporation: Vertically Integrated Alumina Producer Turning Scale and Low-Carbon Initiatives Into Reliable HPA Precursor Supply

Alcoa’s extensive alumina refining assets and bauxite access give it a cost and scale advantage as a supplier of HPA precursors. The company’s EcoLum® low-carbon aluminum initiative (2025) demonstrates a move to decarbonize upstream inputs-an increasingly important selling point for OEMs demanding lower-emissions HPA supply chains. Tariff-driven cost pressures in 2025 underscored Alcoa’s strategic role in offering domestic, vertically integrated HPA precursor supply to mitigate import risk.

Nippon Light Metal Co., Ltd.: Specialty Calcined HPA and Tailored Forms For Ceramics, Sapphire and Thermal Management Substrates

Nippon Light Metal produces high-purity aluminum hydroxide and calcined HPA grades (≥99.9%) used in synthetic sapphire, electronic ceramics, and heat-dissipating substrates. The company differentiates with product form flexibility-fine powders, granules, and pellets-enabling downstream processors to optimize dispersion, polishing and filler performance. Nippon’s repeatable calcination and washing processes yield materials with high electrical insulation resistance and thermal conductivity required in specialized electronics and substrate markets.

Altech Chemicals Ltd.: Low-Cost Kaolin-To-HPA Innovator Targeting 4N Volumes and Ceramic Formats For Niche High-Value Markets

Altech is commercializing a proprietary hydrochloric acid leach route to produce HPA from low-grade kaolin, aiming to bypass costly aluminum metal steps and target cost-efficient 4N HPA volumes. The company’s Dec 2025 acquisition of Advanced Ceramics Pty Ltd expands its capability to deliver HPA in finished ceramic formats for medical and aerospace niches. Altech’s Australian base and critical minerals positioning offer Western OEMs a security-of-supply alternative to Asia-centric HPA sources.

Australia has repositioned itself as the global anchor for low-carbon, export-oriented HPA, transitioning decisively from raw bauxite exports to downstream 4N–6N alumina refining. The May 2024 Final Investment Decision for the Gladstone “HPA First” project by Alpha HPA marked a structural inflection point. Backed by a A$600 million (~US$400 million) financing package from the Australian Government’s Critical Minerals Facility and NAIF, the refinery targets 10,000 tpa of HPA, using HCl leaching and proprietary purification to materially reduce carbon intensity versus Bayer-derived routes.

Momentum accelerated in August 2025 when Alpha HPA transferred a US$30 million royalty facility to fund Stage 2 and its Alpha Sapphire subsidiary—extending Australia’s value capture into synthetic sapphire for semiconductors and defense optics. Upstream-downstream synergy is strengthening: in April 2025, Impact Minerals formed a JV to fast-track Western Australian feedstock, leveraging proximity to Perth’s electronics and battery clusters. Collectively, Australia is building a secure, scalable HPA ecosystem with strong sovereign backing.

China: “High-Quality Development” Tightens Standards for 5N/6N Output

China’s HPA strategy is pivoting from volume to precision and compliance, aligning with semiconductor self-reliance goals. In March 2025, the Ministry of Industry and Information Technology (MIIT) released the Action Plan for the High-Quality Development of the Aluminium Industry (2025–2027), imposing stricter approvals for new capacity and prohibiting boehmite-only feedstock without comprehensive red-mud utilization—a move that elevates capital discipline and environmental performance for HPA entrants.

Despite controls, China’s scale remains unmatched: metallurgical alumina output reached 22.7 Mt in Q3 2025, prompting downstream conversion into high-purity derivatives. Exports of these derivatives rose 59.3% YoY in the first eight months of 2025, underscoring China’s ability to arbitrate surplus into higher value. Looking ahead, mandates requiring ≥30% of primary aluminum capacity to meet energy-efficiency benchmarks by 2027 favor renewables-backed hydrolysis technologies, reinforcing China’s push toward 5N/6N semiconductor-grade HPA with lower emissions.

Japan: Defining the Ultra-High-Purity (5N/6N) Frontier for 6G and AI

Japan continues to set the benchmark for ultra-high-purity alumina essential to 6G telecommunications, CMP slurries, and thermal management. In late 2024, Sumitomo Chemical commenced mass production of its NXA series ultra-fine α-alumina at Ehime Works, delivering ≤150 nm particles tailored for next-generation semiconductor polishing and high-strength components. The company targets a 30% revenue increase in FY2025 vs FY2023 in its ultra-high-purity alumina business, driven by AI data center demand.

Policy alignment reinforces leadership. Japan’s GX 2040 Vision (approved January 2025) provides R&D subsidies for chemical recycling and low-energy purification, incentivizing circular HPA supply chains without compromising purity. The result is a tightly integrated ecosystem where 5N/6N output, particle engineering, and sustainability co-evolve—cementing Japan’s role at the purity frontier.

United States: CHIPS Act Pull-Through Elevates Sapphire and Defense Demand

In the United States, the CHIPS Act is creating a powerful pull-through effect for HPA used in sapphire substrates, advanced ceramics, and defense optics. The Department of Commerce has prioritized HPA as a “critical intermediate” supporting roughly US$39 billion in fab construction, catalyzing capacity expansions by domestic leaders such as Almatis and CoorsTek.

Sustainability signals are also shaping inputs. In May 2025, Alcoa Corporation launched EcoLum® low-carbon aluminum billet, signaling broader demand for green alumina precursors compatible with low-emission HPA routes. Under the 2025 NDAA, increased funding for sapphire glass in transparent armor and missile domes provides a stable, high-value floor for 5N HPA, anchoring domestic demand beyond commercial semiconductors.

Canada: Clean-Tech HPA Powered by Hydroelectricity

Canada is emerging as a low-carbon HPA hub by leveraging abundant hydroelectric power and low-temperature HCl-to-HPA processes. In December 2025, Polar Sapphire received US$4.1 million from Sustainable Development Technology Canada (SDTC) to advance HPA tailored for solid-state batteries (SSBs). The company’s low-temperature purification materially reduces energy intensity—aligned with Canada’s Net Zero 2050 pathway.

HPA is embedded in Canada’s US$3.8 billion Critical Minerals Strategy, which offers tax credits to move from extraction to downstream high-purity processing. This policy stack positions Canada to supply clean-tech HPA into batteries and electronics with a compelling carbon advantage.

India: Scaling Special-Grade Alumina and High-Purity Oxides

India is transitioning from primary aluminum to value-added high-purity derivatives, supported by accelerated approvals and state-owned capacity. In October 2025, National Aluminium Company issued an EOI to establish a rotary kiln for Special Grade Alumina (SGA) at Damanjodi—signaling intent to move into higher-margin alumina streams with submissions extending into January 2026.

Policy momentum extends to adjacent oxides. In December 2025, the Ministry of Mines highlighted initiatives to leverage India’s bauxite base into high-purity oxides, including 99.99% nuclear-grade gadolinium oxide, as part of a broader critical minerals push. The “Saksham Niveshak” fast-track campaign (launched August 2025) is expediting approvals across Odisha and Gujarat, positioning India as a rising industrial- and special-grade HPA supplier.

2025 Strategic Matrix: High-Purity Alumina (HPA) by Country

High-Purity Alumina (HPA) Matrix

|

Country

|

Primary Development Focus

|

Strategic Policy / News

|

Purity / Material Emphasis

|

|

Australia

|

Export-to-refined pivot

|

A$600M federal financing (Alpha HPA)

|

4N HPA & sapphire

|

|

China

|

Supply-chain resilience

|

MIIT Action Plan 2025–2027

|

Semiconductor 5N/6N

|

|

Japan

|

ICT & energy saving

|

NXA series mass production

|

≤150 nm ultra-fine α-alumina

|

|

United States

|

Semiconductor substrates

|

CHIPS Act pull-through; NDAA

|

Sapphire substrates for AI/defense

|

|

Canada

|

Solid-state batteries

|

US$4.1M SDTC (Polar Sapphire)

|

Low-carbon SSB feedstock

|

|

India

|

Special-grade expansion

|

NALCO SGA EOI (Oct 2025)

|

Industrial & special grades

|

High-Purity Alumina Market Report Scope

High-Purity Alumina Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$28.1 Billion

|

|

Market Size (2035)

|

$251.4 Billion

|

|

Market Growth Rate

|

24.5%

|

|

Segments

|

By Purity Level (4N, 5N, 6N), By Production Technology (Aluminum Alkoxide Hydrolysis, HCl Leaching, Modified Bayer Process, Sol-Gel & CVD), By Product Form (Powder, Pellets & Beads, Tablets, Slurries & Pastes), By Application (Li-ion Battery Separators, LED & Optoelectronics, Semiconductors, Sapphire Glass, Industrial Ceramics), By End-Use Industry (Automotive & Energy Storage, Consumer Electronics, Aerospace & Defense, Medical & Healthcare)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sumitomo Chemical Co. Ltd., Alpha HPA Limited, Sasol Limited, Baikowski S.A., Nippon Light Metal Holdings Co. Ltd., Alcoa Corporation, CHALCO, Altech Batteries Ltd., Polar Performance Materials, FYI Resources Limited, Hebei Pengda Advanced Materials, Zibo Honghe Chemical, CoorsTek Inc., Rio Tinto Alcan, Nabaltec AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

High-Purity Alumina Market Segmentation

By Purity Level

By Production Technology

- Aluminum Alkoxide Hydrolysis

- Hydrochloric Acid (HCl) Leaching

- Modified Bayer Process

- Sol-Gel & Chemical Vapor Deposition (CVD)

By Product Form

- Powder

- Pellets & Beads

- Tablets

- Slurries & Pastes

By Application

- Li-ion Battery Separators

- LED & Optoelectronics

- Semiconductors

- Sapphire Glass

- Industrial Ceramics

By End-Use Industry

- Automotive & Energy Storage

- Consumer Electronics

- Aerospace & Defense

- Medical & Healthcare

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in High-Purity Alumina Market

- Sumitomo Chemical Co., Ltd.

- Alpha HPA Limited

- Sasol Limited

- Baikowski S.A.

- Nippon Light Metal Holdings Co., Ltd.

- Alcoa Corporation

- Aluminum Corporation of China Limited (CHALCO)

- Altech Batteries Ltd.

- Polar Performance Materials

- FYI Resources Limited

- Hebei Pengda Advanced Materials Technology Co., Ltd.

- Zibo Honghe Chemical Co., Ltd.

- CoorsTek Inc.

- Rio Tinto Alcan

- Nabaltec AG

*- List not Exhaustive