Market overview: Thermal-Critical Aluminum Nitride & Si₃N₄ Ceramic Substrates Driving High-Power Electronics Growth

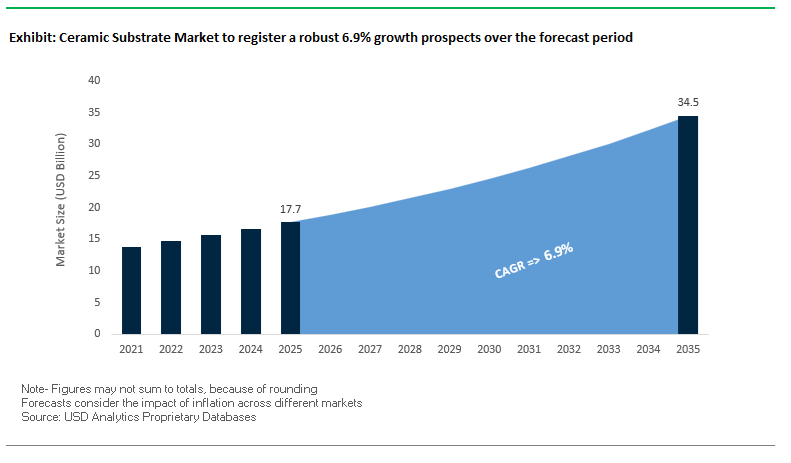

The Ceramic Substrate Market, valued at USD 17.7 billion in 2025 and projected to reach USD 34.5 billion by 2035 at a strong 6.9% CAGR, is experiencing a decisive shift toward high-performance ceramic materials as power-electronics designers, substrate buyers, and reliability engineers prioritize thermal conductivity, electrical insulation, high-frequency stability, and mechanical robustness. With next-generation EV inverters, wide-bandgap semiconductor modules (SiC/GaN), LED lighting systems, and 5G/6G RF architectures pushing device power density and thermal loads to unprecedented levels, ceramic substrates—especially Aluminum Nitride (AlN), Silicon Nitride (Si₃N₄), LTCC, and HTCC—are becoming indispensable to system performance and long-term reliability.

AlN substrates, delivering 170–230 W/m·K thermal conductivity, now dominate applications requiring ultra-efficient heat spreading, enabling compact inverter designs, higher junction temperatures, and improved lifetime margins for high-power modules. Si₃N₄ substrates, with their high fracture toughness (7 MPa·m) and exceptional thermal-shock resistance, are rapidly becoming the preferred choice for EV power modules subjected to aggressive load cycling. On the RF and telecommunications front, LTCC/HTCC multilayer ceramics provide the low dielectric loss (low tanδ) and dimensional stability required for millimeter-wave 5G/6G front-end modules, phased-array antennas, and high-frequency radar electronics. As advanced packaging moves toward larger substrates, higher integration density, and chiplet-based architectures, ceramic substrates are emerging as the foundational material platform enabling the reliability, efficiency, and miniaturization demanded through 2035.

Market Analysis: Capacity Expansions, 5G RF Substrate Launches & Cost Pressures Shaping Market Dynamics

The ceramic substrate market’s 2024–2025 timeline shows parallel forces: surging demand from e-mobility and 5G, simultaneous capacity expansions, and input cost pressure that squeezes margins. An industry report in November 2025 flagged a sharp increase in AlN substrate demand driven by 5G base station modules and next-generation EV inverters; manufacturers are expanding AlN production to meet thermal-critical orders. In September 2025, Kyocera launched a multilayer ceramic substrate explicitly for 5G RF modules, underscoring how LTCC/HTCC innovations and miniaturization are directly tied to telecom rollout requirements. These product introductions accelerate adoption because designers can now integrate passive components, filters and interconnects into compact ceramic modules that sustain high Q-factors and low insertion loss at mmWave frequencies.

However, supply chain and cost factors remain a headwind: industry reporting in August 2025 highlighted raw material and energy cost volatility (e.g., aluminum feedstock, firing energy) that has materially pressured operating margins at major substrate makers such as CoorsTek and NGK Insulators. On the positive side, July 2025 EV capacity expansions among power-module OEMs in the U.S. and Europe are increasing long-term substrate demand for AlN and Si₃N₄. Earlier, in June 2024, CeramTec introduced the Sinalit® Si₃N₄ substrate aimed at automotive power modules, reflecting the market pivot toward mechanically robust, high-thermal-performance substrates. Longer-term packaging roadmaps from Intel and TSMC (late 2024) calling for larger substrate sizes (120×120 mm² and beyond) further favor ceramic substrates for their dimensional stability and low warpage - but create a manufacturing challenge for suppliers who must scale precision processes to greater area and lower defect rates.

Trends and Opportunities Reshaping High-Performance Ceramic Substrate Engineering

Trend 1: Silicon Nitride Becomes the Core Substrate for High-Power EV Power Modules Requiring Extreme Reliability

The rapid electrification of mobility, particularly the shift toward 800V and higher automotive power electronics, is making Silicon Nitride (Si₃N₄) substrates a strategic material for next-generation inverter and converter packaging. As power densities increase, conventional alumina (Al₂O₃) and aluminum nitride (AlN) substrates fail to meet the required thermal cycling life and mechanical robustness standards. Si₃N₄ overcomes these bottlenecks through an order-of-magnitude longer thermal cycling life, enabling EV inverters to survive frequent acceleration, regenerative braking, and harsh thermal gradients without solder fatigue or substrate cracking.

Beyond durability, Si₃N₄ provides flexural strength and fracture toughness more than twice that of AlN, preventing catastrophic substrate failure under high vibration loads typical of electric drive systems. Its high thermal conductivity—up to 177 W/(m·K)—supports power density increases of up to 50% relative to Al₂O₃ modules.

Trend 2: LTCC Substrates Accelerate in 5G, mmWave, and Radar as Miniaturization and High-Frequency Integrity Become Critical

The deployment of 5G New Radio (NR), satellite communication constellations, high-resolution radar, and mmWave imaging systems is driving a steep increase in demand for Low-Temperature Co-Fired Ceramics (LTCC). LTCC’s low dielectric constant and low dissipation factor enable exceptional signal integrity at frequencies above 30 GHz and extending toward 70+ GHz, making it indispensable for AiP modules, phased arrays, and compact RF front ends.

LTCC’s multilayer structure supports embedded passive components, enabling miniaturization that cannot be achieved with traditional PCB-based designs. This integration significantly reduces board footprint and improves reliability in high-frequency environments. Furthermore, LTCC’s monolithic co-sintering process supports true hermetic sealing, allowing the formation of internal cavities, hollow waveguides, and sealed sensor chambers. These attributes make LTCC the material of choice for demanding outdoor, automotive radar, unmanned systems, and aerospace communication systems requiring environmental resilience and long-term stability.

Opportunity 1: Extreme Thermal-Management Substrates for GaN, Ga₂O₃, and GaN-on-Diamond Ultra-Wide-Bandgap Devices

As the power electronics industry moves toward Ultra-Wide Bandgap semiconductors, substrate performance becomes a fundamental limiter of device power density. UWBG materials such as GaN and Ga₂O₃ generate extreme heat fluxes that exceed the capability of traditional ceramic substrates, creating a rapidly expanding opportunity for next-generation thermal spreaders.

Synthetic diamond has become the benchmark, offering thermal conductivity of 1000–2000 W/(m·K)—the highest of any material. When GaN is bonded to diamond, Thermal Boundary Conductance values up to 92 MW/m²-K have been demonstrated, allowing devices to operate at significantly lower junction temperatures and enabling higher switching frequencies and power compression ratios.

Ga₂O₃ devices, while offering exceptional breakdown voltage, suffer from intrinsically low thermal conductivity (10–27 W/(m·K)). Simulation studies show that bonding β-Ga₂O₃ to diamond substrates can reduce self-heating by up to 60% versus sapphire alternatives, creating a vital commercialization pathway. For more cost-sensitive applications, Aluminum Nitride (AlN) remains a high-performance thermal spreader at ~180 W/(m·K) with favorable cost-to-performance ratios for industrial GaN systems. These thermal-management substrates will be increasingly essential as UWBG devices move into mainstream automotive, renewable energy, and aerospace systems.

Opportunity 2: Ceramic Substrates for High-Temperature Sensors and Electronics in Aerospace, Oil & Gas, and Harsh Industrial Environments

Industries operating under extreme temperatures—jet engines, deep-well drilling, geothermal energy, industrial furnaces—are creating strong demand for ceramic substrates capable of supporting electronics at 300°C and above, where polymer-based and metal-based substrates fail.

Advanced ceramics such as alumina (Al₂O₃) and zirconia (ZrO₂) enable passive wireless sensors operating stably at temperatures up to 1200°C, offering real-time monitoring capabilities in harsh aerospace and propulsion environments. In the Oil & Gas sector, ceramic components are qualified for pressures exceeding 1,000 bar and continuous operation at 225°C for over 25 years, underscoring their unmatched mechanical and chemical durability.

High-Temperature Co-Fired Ceramic (HTCC) substrates—sintered at 1600–1700°C—support metallization systems capable of surviving temperatures that would degrade Ag or Cu traces above 500°C. This metallurgical stability is essential for high-reliability electronics in extreme environments where failure could result in catastrophic operational downtime or safety risks. As industries expand electrification and digital monitoring deeper into hostile environments, ceramic substrates will form the enabling backbone for sensor, control, and power systems.

Ceramic Substrate Market Share Analysis

Market Share by Material Type: Alumina (Al₂O₃) Leads with 53.9% Share

Alumina (Al₂O₃) dominates the Ceramic Substrate Market with a substantial 53.9% share in 2025, reflecting its position as the industry’s volume benchmark and the most cost-effective solution for a wide spectrum of electronic, industrial, and consumer device applications. Its leadership is anchored in a highly favorable cost-to-performance ratio, offering stable dielectric properties, mechanical robustness, chemical resistance, and manufacturability at scale—making it the default choice for LED lighting, industrial control systems, consumer electronics modules, and standard power device packaging. The material’s entrenched supply chain and compatibility with established DBC/DBC (Direct Bonded Copper) processes further reinforce its widespread use. Surrounding materials illustrate a strategic performance ladder: Aluminum Nitride (AlN) is gaining momentum as the preferred thermal substrate for high-frequency, high-power 5G and RF applications; Silicon Nitride (Si₃N₄) is expanding rapidly as the reliability-critical substrate for EV inverters due to its superior fracture toughness and thermal cycling endurance; and advanced ceramics such as LTCC, BeO, and ZrO₂ serve specialized requirements in niche defense, telecom, and medical applications. The segmentation highlights a clear migration path across the industry—from Al₂O₃ to AlN and increasingly to Si₃N₄ as performance demands escalate, particularly in electrified transportation and high-frequency communications.

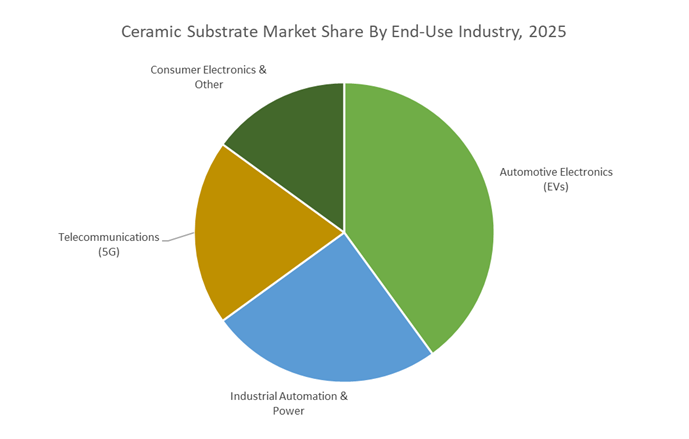

Market Share by End-Use Industry: Automotive Electronics (EVs) Lead with 41.1% Share

Automotive Electronics—driven predominantly by electric vehicles—hold the largest share at 41.1% in 2025, underscoring the transformative impact of EV powertrain electrification on global ceramic substrate demand. As EV inverters, onboard chargers, DC-DC converters, and battery management systems demand ever-higher thermal conductivity and exceptional reliability under extreme temperature cycling, the substrate market is shifting toward Si₃N₄ and advanced metallization technologies such as AMB (Active Metal Brazing). This dominant share reflects the EV sector’s stringent performance requirements, where substrate failure is not an option and thermal management directly influences efficiency, safety, and power density. Beyond EVs, the market is supported by robust adoption in industrial automation and power electronics, where Al₂O₃ remains the workhorse for DBC-based power modules; telecommunications and 5G infrastructure, which drive sustained demand for AlN substrates to manage high power densities in RF front-end modules; and consumer electronics, which continue to rely on Al₂O₃ for LEDs, sensors, and compact power devices. The segmentation clearly illustrates the bifurcation of the market—cost-sensitive, high-volume applications relying on alumina versus high-reliability, performance-critical applications increasingly shifting to Si₃N₄ and AlN—with automotive electronics setting the pace for next-generation substrate innovation.

Country Analysis: Global Ceramic Substrate Market Innovation Hubs

China: Scaling DBC Ceramic Substrate Production for EV Power Electronics and 5G Infrastructure Growth

China remains the global epicenter for DBC (Direct Bonded Copper) ceramic substrates, accounting for an estimated 30–35% of the worldwide market, propelled by its unmatched EV production ecosystem and power module manufacturing scale. As EV makers deploy millions of traction inverters, DC-DC converters, and onboard chargers, Chinese suppliers are rapidly integrating DBC and AMB substrates into high-volume platforms to improve thermal performance, switching efficiency, and reliability in SiC-based power systems. These materials are essential for managing heat in high-density EV power electronics, positioning China firmly as the world’s largest consumer and producer of thermally conductive ceramic substrates.

Government policies further accelerate this momentum. The STAR Market’s role in promoting high-tech material companies—such as ChaoZhou Three-Circle (CCTC)—has strengthened domestic investment in advanced ceramic substrates emphasizing innovation in material refinement, structural reinforcement, and functional property enhancement. Parallel to EV adoption, China’s rapid rollout of 5G base stations is generating massive demand for Aluminium Nitride (AlN) substrates, prized for their superior thermal conductivity and signal integrity in RF modules. As base-station density increases nationwide, Chinese ceramic substrate producers are expanding capacity for AlN for RF power amplifiers, establishing China as a dominant force across telecommunications, EV electronics, and semiconductor infrastructure.

Japan: Advancing Aluminium Nitride and Multilayer Ceramic Substrates for 5G Miniaturization and Thermal Management

Japan continues to hold a technological edge in Aluminium Nitride (AlN) ceramic substrates and high-precision multilayer ceramic architectures used in 5G, advanced RF electronics, and miniaturized modules. With Kyocera Corporation’s launch of a new multilayer ceramic substrate in September 2025, Japan is driving the global transition toward ultra-compact, high-frequency 5G RF modules that require exceptional dielectric properties, high-density circuitry, and extreme reliability. This innovation aligns with Japan’s long-term leadership in multilayer ceramic technologies used in telecommunications, automotive radar systems, and consumer electronics.

Japanese manufacturers are also leading global advancements in AlN powder refinement and substrate fabrication, enabling high thermal conductivity solutions for EV power electronics, heat sinks, and semiconductor thermal management. As demand escalates for high-performance substrates that can withstand extreme electrical and thermal loads, Japan is accelerating its shift away from toxic Beryllium Oxide (BeO) toward AlN-based alternatives for RF windows, high-power laser systems, and specialized semiconductor equipment. This positions Japan as a central hub for safe, high-performance ceramic substrate technologies essential to next-generation communications and electrified mobility.

United States: Expanding Domestic Ceramic Substrate Capacity to Support Wide-Bandgap (WBG) Power Electronics Adoption

The United States is rapidly strengthening its ceramic substrate ecosystem to support SiC and GaN wide-bandgap power electronics, critical for advanced EV architectures, aerospace platforms, and grid power systems. CeramTec North America’s August 2025 announcement to expand U.S. ceramic manufacturing capacity highlights a national push to secure domestic supply chains for high-performance DBC, AMB, AlN, and Si₃N₄ substrates. This expansion directly targets the growing semiconductor and EV markets, as domestic OEMs increase reliance on thermally robust materials for power module reliability.

The U.S. market is also a leader in the adoption of Silicon Nitride (Si₃N₄) substrates, driven by North American EV manufacturers deploying Si₃N₄ in nearly 32% of EV inverters due to its exceptional fracture toughness, thermal cycling resistance, and high mechanical strength. As OEMs transition to 800V power architectures, the need for ceramic substrates with superior electrical insulation and Partial Discharge (PD) mitigation capabilities is rising sharply. U.S. R&D initiatives are advancing next-generation DBC designs—such as mesa substrates and field-grading structures—to reduce electric field concentration at triple points, significantly improving SiC module longevity. These innovations position the U.S. as a critical hub for high-voltage ceramic substrate technology supporting the broader WBG semiconductor revolution.

Germany/Europe: AMB Substrate Manufacturing Leadership and Automotive Tier-1 Integration for EV Platforms

Europe—anchored by Germany—remains a global innovation leader in AMB (Active Metal Brazing) and DBC ceramic substrate technology, serving as a critical supplier to leading EV OEMs and Tier-1 automotive integrators. With NGK Insulators’ March 2024 announcement to invest approximately 5 billion yen to increase AMB production capacity by 2.5× by FY2026, Europe is accelerating the scale required to support surging demand for power semiconductor modules in EV traction inverters and onboard chargers. This expansion is essential as automakers such as Volkswagen and Tesla’s European operations integrate AMB and DBC substrates to enhance thermal efficiency, module reliability, and lifetime performance in high-power EV systems.

Beyond automotive electrification, Europe’s aggressive deployment of renewable energy systems, including solar inverters and wind power converters, is sustaining long-term demand for ceramic substrates capable of handling high power densities and extreme thermal cycling. German ceramic leaders such as CeramTec GmbH are expanding portfolios in Si₃N₄ and AlN substrates, optimizing materials for industrial drives, automotive electrification, and high-voltage energy applications. With its strong Tier-1 network, advanced manufacturing capabilities, and sustainability-driven innovation strategies, Europe remains a cornerstone in the global ceramic substrate value chain.

Competitive Landscape: Multilayer LTCC Innovators, AlN Thermal Specialists & Si₃N₄ Reliability Leaders

The ceramic substrate competitive map is split between firms specializing in AlN thermal substrates, Si₃N₄ mechanical reliability, LTCC/HTCC multilayers for RF, and broader materials houses supplying multiple ceramic chemistries. Success depends on material portfolio breadth, capacity scale, application-specific product launches (e.g., 5G RF LTCC), and the ability to manage raw-material and energy cost volatility.

KYOCERA Corporation - Multilayer ceramic substrates and LTCC innovations for 5G and data-center infrastructure

Kyocera is a world leader in fine ceramics with a broad portfolio (AlN, Al₂O₃, LTCC/HTCC) and over 200 ceramic formulations. Its September 2025 launch of a multilayer ceramic substrate optimized for 5G RF modules underscores a strategic bet on telecom and data-center demand. Kyocera’s strength lies in integrating thick-film/thin-film processes and material customization to meet thermal, electrical and dimensional stability requirements for advanced packaging.

CeramTec GmbH - Si₃N₄ substrate specialist delivering e-mobility reliability with Sinalit®

CeramTec focuses on high-reliability ceramic substrates including DBC, AMB and Si₃N₄ offerings. The June 2024 introduction of Sinalit® (Si₃N₄) targets automotive power modules where fracture toughness and thermal shock resistance are critical. CeramTec supports OEMs requiring custom mechanical robustness and demonstrated thermal performance - a key advantage for EV inverter suppliers.

CoorsTek Inc. - Broad engineered-ceramics portfolio supporting semiconductor, automotive and LED thermal needs

CoorsTek’s strength is a massive material toolbox (Al₂O₃, AlN, SiC, Si₃N₄) and experience in ultra-pure ceramic components for semiconductor processing and high-power electronics. CoorsTek supplies high-purity substrates and fixtures (e.g., SiC coated susceptors) and is positioned to meet precision demands for large-format substrates and harsh-environment applications.

MARUWA Co., Ltd. - AlN thermal substrate specialist scaling for LED and power-dense modules

MARUWA specializes in Aluminum Nitride substrates and is expanding capacity to meet rising demand from high-luminance LED lighting and industrial power modules. With AlN thermal conductivities exceeding 170 W/m·K, MARUWA addresses applications where heat removal is a limiting factor in system performance and reliability.

Murata Manufacturing Co., Ltd. - LTCC mastery for high-frequency, miniaturized RF modules and integrated passives

Murata is the global LTCC leader, delivering compact multi-function ceramic modules, filters and integrated passives for 5G/6G systems. Its LTCC technology enables low dielectric loss and high Q performance above 20 GHz, making Murata a natural partner for RF front-end suppliers seeking high integration density and superior signal integrity.

Ceramic Substrate Market Report Scope

Ceramic Substrate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$17.7 Billion

|

|

Market Size (2035)

|

$34.5 Billion

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Material Type (Alumina, Aluminium Nitride, Silicon Nitride, Beryllium Oxide, Zirconia, LTCC), By Metallization Technology (Direct Bonded Copper, Active Metal Brazing, Thick Film, Thin Film, Direct Plated Copper), By End-Use Industry (Automotive Electronics, Telecommunication, Industrial Automation, Consumer Electronics, Aerospace & Defense, Renewable Energy), By Application Type (Power Modules, LED Modules, Hybrid Circuits, Sensors, IC Packaging), By Form Factor (Plates/Sheets, Tapes, Discs, Custom 3D Geometries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kyocera Corporation, Murata Manufacturing Co. Ltd., CoorsTek Inc., CeramTec GmbH, Rogers Corporation, Ferrotec Holdings Corporation, NGK Insulators Ltd., Heraeus Electronics, ChaoZhou Three-Circle, Tong Hsing Electronic Industries Ltd., Maruwa Co. Ltd., Mitsubishi Materials Corporation, DENKA Company Limited, Remtec Inc., Shin-Etsu Chemical Co. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ceramic Substrate Market Segmentation

By Material Type

- Alumina (Al₂O₃)

- Aluminium Nitride

- Silicon Nitride

- Beryllium Oxide

- Zirconia (ZrO₂)

- Low-Temperature Co-Fired Ceramics (LTCC)

By Metallization Technology

- Direct Bonded Copper (DBC)

- Active Metal Brazing (AMB)

- Thick Film Substrates

- Thin Film Substrates

- Direct Plated Copper (DPC)

By End-Use Industry

- Automotive Electronics

- Telecommunication

- Industrial Automation

- Consumer Electronics

- Aerospace & Defense

- Renewable Energy

By Application Type

- Power Modules

- LED Modules

- Thick Film Hybrid Circuits

- Sensors

- IC Packaging

By Form Factor

- Plates / Sheets

- Tapes (for LTCC)

- Discs

- Custom 3D Geometries

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Ceramic Substrate Market

- KYOCERA Corporation

- Murata Manufacturing Co., Ltd.

- CoorsTek, Inc.

- CeramTec GmbH

- Rogers Corporation

- Ferrotec Holdings Corporation

- NGK Insulators, Ltd.

- Heraeus Electronics

- ChaoZhou Three-Circle

- Tong Hsing Electronic Industries, LTD.

- Maruwa Co., Ltd.

- Mitsubishi Materials Corporation

- DENKA Company Limited

- Remtec, Inc.

- Shin-Etsu Chemical Co., Ltd.

*- List not Exhaustive