Market Overview: Silicon Nitride’s Shift Toward EV Powertrain Reliability & Advanced Ceramics Manufacturing

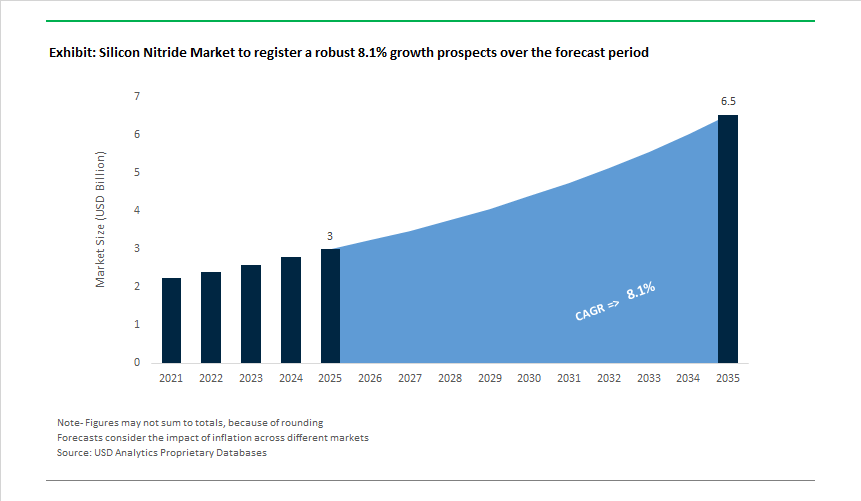

The Silicon Nitride Market is valued at USD 3.0 billion in 2025 and is projected to reach USD 6.5 billion by 2035, expanding at an 8.1% CAGR as OEMs increasingly design around lifetime reliability, thermal robustness, and system efficiency rather than short-term material cost. Silicon nitride (Si₃N₄) is no longer confined to niche advanced ceramics; it is becoming a platform material in applications where failure tolerance is approaching zero.

A key structural driver is electric mobility and power electronics reliability. As EV architectures push toward higher power density, faster switching, and aggressive temperature cycling, conventional ceramic substrates are reaching their durability limits. Silicon nitride substrates are increasingly specified in power modules because they withstand repeated thermal cycling with dramatically longer fatigue life than alumina- or aluminum-nitride-based alternatives. For automotive OEMs, this translates directly into longer inverter lifetimes, lower warranty risk, and higher confidence in high-voltage platforms, making Si₃N₄ a material choice aligned with platform durability rather than incremental efficiency gains.

In parallel, high-speed and precision-bearing applications are reshaping demand in industrial automation, energy, and mobility. Dense silicon nitride rolling elements deliver order-of-magnitude improvements in rolling contact fatigue life while operating at higher speeds and lower lubrication requirements than steel bearings. This performance enables higher spindle speeds in machine tools, improved efficiency and durability in turbochargers, and reduced maintenance in wind and industrial drive systems. The material’s low density-approximately 58% lighter than steel-reduces rotational inertia, supporting faster acceleration, lower energy loss, and reduced wear across dynamic systems.

Healthcare applications represent a structurally different but increasingly important growth vector. In orthopedic and spinal implants, silicon nitride’s combination of biocompatibility, radiolucency, and favorable surface chemistry supports bone integration while avoiding some of the imaging and wear challenges associated with metallic implants. As surgical outcomes and long-term implant performance become central to reimbursement and clinical adoption, Si₃N₄-based devices are gaining specification as performance-driven alternatives, positioning medical implants as one of the fastest-expanding end-use segments despite lower absolute volumes.

From a competitive and strategic standpoint, silicon nitride’s adoption is governed by qualification depth, manufacturing consistency, and cost-down scalability, rather than raw demand alone. Processing complexity and capital intensity create natural barriers to entry, while long qualification cycles in automotive, industrial, and medical applications lock approved materials into platforms for extended periods. As a result, suppliers capable of delivering consistent microstructure control, reliable large-scale sintering, and application-specific formulations are moving upstream in strategic importance.

Market Analysis: Recent Developments Driving Growth in Silicon Nitride Manufacturing

The Silicon Nitride industry entered a high-innovation cycle, with transformative developments in medical ceramics, industrial energy systems, and advanced material technology. In November 2025, TRUNNANO launched a Silicon Nitride-Silicon Carbide composite engineered for extreme hardness and toughness, targeting metallurgical and energy applications requiring exceptional thermal shock resistance. Also in November 2025, Kyocera expanded its European medical ceramics footprint by opening a new Waiblingen production facility, positioning Silicon Nitride as a foundational biomaterial for orthopedic and spinal implants under the BIOCERAM AZUL® platform. On the other hand, October 2025 marked a strategic step for industrial ceramics with Lucideon and the UK Manufacturing Technology Centre signing an MoU to accelerate Silicon Nitride scale-up and optimization, signaling that Europe is rapidly industrializing advanced ceramic manufacturing.

A significant R&D shift emerged in September 2025, when HRL Laboratories and Prodways advanced 3D printing for silicon oxycarbide ceramics-an indicator of the broader movement toward Additive Manufacturing of complex Si₃N₄-class materials for aerospace and high-temperature applications. During the same month, Kyocera highlighted its Si₃N₄ solutions at the Hydrogen Technology World Expo, demonstrating components engineered to tolerate high-temperature, corrosive hydrogen environments-positioning Silicon Nitride as a future-proof material for hydrogen mobility and energy storage systems. Continuing the momentum, July 2025 research advancements focused on joining Si₃N₄ with metals such as Inconel via brazing interlayers, solving one of the most difficult integration challenges for gas turbines and EV powertrains.

Earlier developments in April 2024 showed rising adoption in renewable energy when industrial equipment manufacturers increased their specification of Si₃N₄ balls and rollers for wind turbine gearboxes, citing dramatic improvements in uptime and maintenance reduction. In March 2024, AlzChem Group AG expanded Silicon Nitride powder capacity, signaling continued confidence in the long-term growth trajectory of advanced ceramics across automotive, medical, aerospace, and photovoltaic manufacturing.

Silicon Nitride Market Trends and Opportunities

Trend 1: High-Stress Si₃N₄ Bearings in Aerospace and Turbomachinery

Aerospace and turbomachinery platforms are accelerating adoption of silicon nitride bearings to reduce rotating mass, extend service intervals, and improve resilience during lubrication loss events. With a density of ~3.2 g/cm³—roughly 40% lighter than bearing steel—Si₃N₄ delivers immediate gains in shaft dynamics and fuel efficiency.

Peer-reviewed testing published in Lubricants (October 2025) shows full-ceramic Si₃N₄ bearings maintaining structural integrity under self-lubricating conditions where steel bearings seize. At rotational speeds approaching 8,000 RPM, Si₃N₄ exhibited a friction coefficient near 0.007, enabling controlled “limp-home” operation in auxiliary power units (APUs) and critical aircraft subsystems.

Reliability modeling further strengthens the case. Weibull analyses conducted in 2025 indicate ~6.7× longer projected life versus 52100 steel bearings at a 90% confidence level, driven by resistance to micro-spalling and surface fatigue—the dominant failure modes in high-vibration environments. In practical terms, this translates into fewer unscheduled removals and lower maintenance-induced emissions.

By November 2025, aerospace technical briefings emphasized that tighter thermal tolerances enabled by Si₃N₄’s low thermal expansion improve compressor efficiency and shaft alignment, directly supporting aviation’s Net Zero 2050 objectives through incremental but system-wide fuel burn reductions.

Trend 2: Precision Net-Shape Additive Manufacturing for Medical Implants

Additive manufacturing is redefining how silicon nitride is deployed in medicine, shifting from subtractive machining to net-shape, patient-specific bioceramics that combine mechanical strength with biological performance.

A 2025 study demonstrated Digital Light Processing (DLP) fabrication of Si₃N₄ dental implants achieving flexural strength of ~770 MPa and fracture toughness ~13 MPa·m¹ᐟ², comfortably meeting load-bearing requirements for oral restorations. These values close the historical performance gap between printed and conventionally sintered ceramics.

Hybrid material systems are also gaining traction. In 2025, 8% Si₃N₄ fiber–reinforced PEEK scaffolds produced via material extrusion showed a 52% increase in Young’s modulus (to ~6.36 GPa) versus pure PEEK, alongside superior angiogenic response—critical for spinal and complex orthopedic reconstructions.

To overcome throughput constraints, microwave sintering has emerged as a parallel enabler. New 2025 processes produced dense Si₃N₄ components with bending strength approaching 930 MPa, demonstrating that AM parts can now meet or exceed the integrity of traditionally sintered implants while enabling complex geometries tailored from patient imaging data.

Opportunity 1: Antibacterial Surface Chemistry for Orthopedic and Dental Implants

Post-surgical infection remains one of the most expensive and disruptive complications in orthopedics and dentistry, positioning silicon nitride’s intrinsic antibacterial behavior as a differentiating advantage.

Clinical comparisons in September 2025 showed that “as-fired” Si₃N₄ surfaces suppressed pathogens such as Staphylococcus aureus and Porphyromonas gingivalis by >70% versus conventional implant surfaces. The mechanism is dual: nanoscale surface topography discourages bacterial adhesion, while controlled release of ammonia and reactive oxygen species creates a hostile microenvironment for biofilms—without cytotoxicity to host cells.

Regulatory momentum is aligning with this capability. Updates to the EU Medical Device Regulation (MDR) in 2025 increasingly favor bio-functional materials that reduce infection risk without coatings or antibiotics. Comparative in vivo data show ~69% new bone formation at 90 days for Si₃N₄ implants versus ~36% for sterile titanium, materially reducing the likelihood of revision surgery.

Late-2025 research further demonstrated that thermochemical surface treatments enhance apatite formation on Si₃N₄, boosting osteointegration while preserving antibacterial action—creating a pathway toward “zero-infection” implant strategies for high-risk patients.

Opportunity 2: High-Power Substrates for EV and 5G Infrastructure

Silicon nitride is rapidly becoming the substrate of choice for Active Metal Brazing (AMB) in high-power modules, where thermal performance and mechanical reliability dictate system limits.

With thermal conductivity ranging from ~80 to 177 W/m·K, Si₃N₄ far outperforms alumina (~24 W/m·K), enabling EV power modules to manage higher heat fluxes from SiC and GaN devices. As 800V architectures proliferate, Si₃N₄ substrates supporting ~1.0 mm copper layers have demonstrated ~50% increases in power density versus legacy ceramic cores.

Mechanical resilience under thermal cycling is equally critical. Data released in 2025 by CeramTec highlighted fracture toughness ≥6.5 MPa·m¹ᐟ² and a CTE (~3.3×10⁻⁶/K) closely matched to SiC. This compatibility significantly reduces solder joint fatigue during fast charging and regenerative braking cycles.

Beyond automotive, high-power RF is emerging as a parallel demand center. In December 2025, Remtec and peer suppliers confirmed integration of Si₃N₄ into multilayer dielectric circuits for 5G base stations, where maintaining signal integrity at high frequencies must coexist with aggressive thermal dissipation. This convergence positions silicon nitride as a cornerstone material for EV electrification and dense telecom infrastructure alike.

Market Share Analysis: Silicon Nitride Market

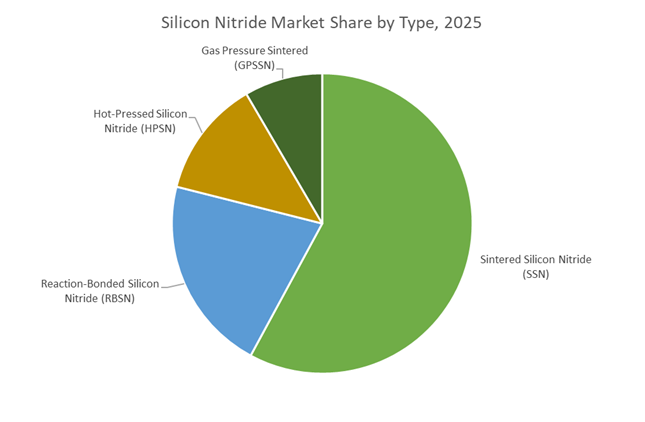

Market Share by Type: Sintered Silicon Nitride Anchors High-Volume, High-Performance Ceramic Adoption

Sintered Silicon Nitride (SSN) holds approximately 55% share of the global silicon nitride market because it uniquely combines manufacturing scalability, mechanical robustness, and design flexibility, making it the default choice for volume-driven automotive and industrial applications. Unlike hot-pressed or reaction-bonded variants, SSN supports near-net-shape forming of complex geometries at economically viable yields, a decisive advantage as OEMs seek ceramic components that can be integrated into existing production lines rather than treated as specialty parts. From a performance standpoint, SSN’s ability to deliver around 1,000 MPa flexural strength provides a compelling strength-to-weight proposition that directly displaces steel in high-stress, rotating, and impact-prone environments. This mechanical edge is reinforced by thermal stability up to 1,400°C, positioning SSN as a critical enabler for next-generation gas turbines, foundry tooling, and high-temperature industrial systems where metals face oxidation and creep limitations. Energy efficiency further strengthens SSN’s market leadership: silicon nitride rolling elements have demonstrated up to 80% friction reduction versus steel, translating into lower energy losses, extended maintenance intervals, and measurable lifecycle cost savings. Crucially, SSN also overcomes the historical brittleness associated with advanced ceramics, achieving fracture toughness levels near 6.5 MPa·m¹ᐟ², which supports adoption in heavy-duty valves, metalworking tools, and shock-loaded components. Collectively, these attributes explain why SSN has emerged as the commercially dominant silicon nitride form, balancing performance leadership with manufacturability at scale.

Market Share by Application: Automotive & Transportation Drive Volume Through Efficiency-Led Substitution

Automotive and transportation applications account for around 30% of total silicon nitride demand, reflecting how aggressively the sector is adopting advanced ceramics to meet electrification, efficiency, and durability targets. The strongest pull comes from electric powertrains, where silicon nitride hybrid bearings have become a strategic solution to one of the EV industry’s most persistent challenges: efficiency loss and premature bearing failure at high rotational speeds. Ceramic rolling elements enable motors to operate beyond 20,000 RPM without electrical arcing, a capability that directly supports 15–20% improvements in EV driving range through reduced friction and thermal losses. This insulating behavior is increasingly critical, as stray electrical currents are now linked to roughly 30% of early EV motor bearing failures, making silicon nitride as a reliability safeguard. Beyond passenger EVs, commercial transportation and heavy-duty diesel platforms are also accelerating adoption, with silicon nitride valves and injector components delivering up to three times longer service life under extreme pressure and temperature conditions—significantly lowering total cost of ownership for fleet operators. Weight reduction further reinforces automotive demand: being around 60% lighter than steel, silicon nitride components improve power-to-weight ratios, a non-negotiable metric for EVs, performance vehicles, and emerging aerospace-adjacent mobility platforms such as drones. As regulatory pressure, electrification, and efficiency benchmarking intensify, automotive and transportation applications will remain the principal volume engine translating silicon nitride’s technical advantages into sustained market share.

Competitive Landscape: Global Leaders Shaping Si₃N₄ Technology and Advanced Ceramics Supply Chains

Industry competitiveness is defined by companies that excel in powder purity, fracture toughness engineering, precision machining, biomaterial certification, and high-temperature performance. These leaders leverage materials science depth, vertically integrated production, and application-specific innovation across EVs, aerospace, medical implants, refractories, and renewable energy systems.

Kyocera Corporation - Expanding Fine Ceramics Leadership Into Automotive, Medical and Energy Systems

Kyocera continues to dominate the global advanced ceramics market with specialized Silicon Nitride grades such as SN287 used in RF windows, thermocouple protection tubes, and molten metal casting environments. Its October 2025 launch of a new medical ceramics facility in Waiblingen strengthens its dominance in European medical implant manufacturing. Kyocera’s design flexibility-spanning extrusion, injection molding, and sintering-allows customization for high-temperature strength components across automotive and renewable energy sectors. Through strategic visibility at global exhibitions such as the Hydrogen Technology Expo, Kyocera is positioning Si₃N₄ as a core enabling material for next-generation mobility and clean energy ecosystems.

Coorstek, Inc. - High-Reliability Si₃N₄ Components For EV, Aerospace and Industrial Bearings

CoorsTek leverages its Cerbec® Silicon Nitride bearing balls-58% lighter and 121% harder than steel-to deliver unmatched high-speed rotation performance with wear resistance ideal for precision systems. Its Si₃N₄ grades such as NBD-200 and SN-101C offer fracture toughness up to 6.5 MPa·m¹ᐟ², enabling reliability in severe-service applications including turbochargers and high-load industrial machinery. CoorsTek is a key supplier to EV traction motor bearings, where electrical insulation and thermal stability are critical. Its advanced processing, including Hot-Pressed Silicon Nitride (HPSN), ensures near-zero porosity and industry-leading mechanical properties.

Ceramtec Gmbh - Precision Silicon Nitride Solutions For Medical, Industrial and High-Temperature Systems

CeramTec is a premier supplier of engineered Silicon Nitride components used in cutting tools, industrial machinery, and diesel engine glow plugs, where thermal shock resistance and strength are essential. Its core expertise in medical ceramics positions it as a leader in biocompatible Si₃N₄ implants for joint replacement systems, leveraging superior wear resistance and antibacterial properties. CeramTec continuously invests in advanced sintering and precision finishing techniques that provide tight tolerances required in high-performance assemblies and semiconductor tooling, reinforcing its presence across high-value industrial and medical sectors.

Saint-Gobain - High-Performance Si₃N₄ For Refractories, Powertrain Components and Extreme Environments

Saint-Gobain provides Silicon Nitride solutions used in foundries, high-temperature reactors, and automotive powertrain systems, benefiting from its deep materials science capabilities. The company is a key player in research programs focused on joining Si₃N₄ to metals-an essential innovation for aerospace engines and EV power modules. Its refractory materials featuring Si₃N₄ deliver exceptional thermal shock resistance for harsh industrial environments, while its advanced finishing solutions support the precision needs of next-generation automotive components and high-temperature performance materials.

Alzchem Group AG - Foundation Of The Silicon Nitride Value Chain Through High-Purity Powder Production

AlzChem serves as a critical upstream supplier, producing high-purity Si₃N₄ powders through controlled nitridation pathways using premium silicon and nitrogen feedstocks. Its D50 powder grades are widely used by global ceramic component manufacturers across electronics, photovoltaics, automotive and medical applications. With March 2024 investments expanding its powder production capacity, AlzChem strengthens global supply chain stability and ensures long-term availability of raw materials essential for advanced ceramics manufacturing. The company’s vertical integration strategy provides OEMs with reliability and consistent material properties, supporting high-performance sintering and precision ceramic fabrication.

Japan continues to dominate the high-purity silicon nitride (Si₃N₄) powder segment, with 2025 marking a decisive shift toward ultra-fine particle engineering and low-carbon synthesis. In late 2024, UBE Corporation launched an ultra-fine silicon nitride grade featuring a 40% reduction in average particle size, enabling higher green density and lower sintering temperatures. This directly improves yield and fatigue resistance in high-speed ceramic bearings for EV motors, where thermal shock resistance and fracture toughness are critical performance differentiators.

Sustainability has become an equal priority. Denka Company Limited transitioned 45% of domestic output to an eco-friendly gas-phase synthesis route, cutting carbon emissions by 32% while lifting material yield by 21%. In parallel, Japan Fine Ceramics (JFC)—a subsidiary of JGC—completed the integration of Showa Denko Materials’ ceramics business in 2025, consolidating domestic capacity for cooling seals, rail components, and SiC/oxide-integrated modules. Collectively, these moves reinforce Japan’s leadership in ultra-fine, high-reliability silicon nitride for EV, rail, and precision industrial markets.

United States: Defense Reshoring and Medical-Grade Silicon Nitride Scale-Up

The United States is reshoring sintered silicon nitride ceramics to support defense modernization and advanced medical implants, elevating Si₃N₄ to a mission-critical material. Under recent supply-chain executive orders, incentives have targeted domestic production for hypersonic radomes, turbine components, and thermal-shock-resistant aerospace parts, with industry estimates indicating ~35% of U.S. demand now tied to high-performance defense uses.

On the biomedical front, SINTX Technologies reported a 96% biocompatibility rating for its latest medical-grade silicon nitride used in spinal and dental implants. By 2025, ~31% of specialized powder output in North America is being directed to active antimicrobial coatings and load-bearing implants, underscoring rapid adoption in orthopedics. Meanwhile, H.C. Starck reallocated 33% of its R&D budget to additive-manufacturing-optimized Si₃N₄ powders for Selective Laser Sintering (SLS), enabling complex, scratch-resistant geometries for aerospace and defense.

Germany: Power Electronics, Euro 7 Compliance, and ESG Leadership

Germany is leveraging its automotive and materials heritage to push silicon nitride into 800V EV power electronics and low-emission mobility solutions. AlzChem Group AG expanded production of Silzot® high-purity silicon nitride, increasingly used as an additive in EV brake pads to reduce non-exhaust PM10 emissions—a direct response to Euro 7 requirements.

Beyond mobility, Germany’s Photonics 2025 initiative is funding silicon nitride-on-insulator (SNOI) wafers for integrated photonic circuits (PICs) used in LiDAR and telecom, where low optical loss and thermal stability are essential. ESG compliance remains central: in 2025, German manufacturers completed the transition to PFAS-free processing for silicon nitride technical ceramics to align with updated EU REACH rules, strengthening Germany’s position as Europe’s benchmark for sustainable, high-performance Si₃N₄ materials.

China: AI-Driven Quality Control and Third-Generation Semiconductor Adoption

China is rapidly upgrading from volume production to high-purity, AI-validated silicon nitride, aligning with its push into third-generation semiconductors. In mid-2024, Yantai Tomley Hi‑tech deployed AI-based inspection capable of detecting granularity deviations with 92% accuracy, cutting material waste by 25% and stabilizing substrate quality for LED and solar applications.

Policy support is accelerating adoption in electronics. The MIIT designated silicon nitride as a key dielectric for GaN-on-Si and SiC power modules, prompting firms such as SICC and Tankeblue to integrate Si₃N₄ passivation layers to boost breakdown voltage in AI data-center power chips. China also maintains leadership in photovoltaic-grade silicon nitride for anti-reflective coatings on PERC and TOPCon solar cells, anchoring demand across renewable energy.

South Korea: Megacluster Integration for AI Memory and Advanced Packaging

South Korea is embedding ultrapure silicon nitride into its KRW 700 trillion (~USD 534 billion) semiconductor megacluster strategy. In 2025, the government formally designated Si₃N₄ as a core material for 3D NAND and DRAM fabrication, with demand projected to grow ~10% annually as AI memory production scales at leading fabs.

Advanced packaging is the next frontier. The MOTIE is funding R&D into silicon nitride interposers for 2.5D/3D (CoWoS-class) architectures, where superior thermal conductivity and electrical insulation challenge conventional organic substrates. This positions South Korea to capture value in AI chip packaging, extending Si₃N₄ usage from powders into system-level thermal and dielectric solutions.

Italy: Super-Precision Mechatronics and Ceramic Rolling Elements

Italy has emerged as Europe’s “ceramic valley” for high-performance mechatronics, with silicon nitride central to super-precision motion systems. The SKF Airasca Center of Excellence, operational in late 2024/early 2025, now serves as SKF’s global hub for super-precision bearings. These designs employ Si₃N₄ rolling elements to achieve rotational speeds and heat tolerance unattainable with steel, targeting premium EV drivetrains and aerospace.

Italian manufacturers are also pioneering non-magnetic, electrically insulating Si₃N₄ components for robotics and Physical-AI systems, where sensor fidelity and electromagnetic neutrality are essential. This specialization anchors Italy’s role in luxury, high-precision ceramic applications, complementing broader EU efforts to localize advanced materials.

2025 Strategic Matrix: Silicon Nitride Market by Country

Silicon Nitride Strategic Matrix

|

Country

|

Primary Market Driver

|

2025 Strategic Milestone

|

Key Material / Grade Focus

|

|

Japan

|

High-speed EV bearings

|

UBE ultra-fine grade (−40% particle size)

|

High-purity Si₃N₄ powders

|

|

United States

|

Defense & MedTech reshoring

|

SINTX medical-grade scale-up; AM R&D shift

|

Sintered & AM-optimized ceramics

|

|

Germany

|

Euro 7 / ESG compliance

|

AlzChem Silzot® expansion; PFAS-free processing

|

Brake additives, SNOI substrates

|

|

China

|

AI quality control & WBG chips

|

92%-accuracy AI inspection; GaN/SiC passivation

|

PV-grade & dielectric Si₃N₄

|

|

South Korea

|

AI memory & packaging

|

Megacluster designation of ultrapure Si₃N₄

|

Semiconductor-grade powders, interposers

|

|

Italy

|

Super-precision mechatronics

|

SKF Airasca excellence center

|

Hybrid ceramic rolling elements

|

Silicon Nitride Market Report Scope

Silicon Nitride Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3 Billion

|

|

Market Size (2035)

|

$6.5 Billion

|

|

Market Growth Rate

|

8.1%

|

|

Segments

|

By Type (Sintered Silicon Nitride, Reaction-Bonded Silicon Nitride, Hot-Pressed Silicon Nitride, Gas Pressure Sintered Silicon Nitride), By Grade (Standard Grade, High-Purity Grade, Ceramic-Grade Powder), By Application (Automotive & Transportation, Electronics & Semiconductors, Medical & Healthcare, Aerospace & Defense, Industrial & Metalworking, Renewable Energy)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

UBE Corporation, Denka Company Limited, Kyocera Corporation, CeramTec GmbH, AlzChem Group AG, SINTX Technologies Inc., CoorsTek Inc., Toshiba Materials Co. Ltd., Rogers Corporation, Morgan Advanced Materials, 3M Technical Ceramics, NGK Insulators Ltd., H.C. Starck Tungsten Powders, Yantai Tomley Hi-Tech Advanced Materials, Vesta Si

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Silicon Nitride Market Segmentation

By Type

- Sintered Silicon Nitride (SSN)

- Reaction-Bonded Silicon Nitride (RBSN)

- Hot-Pressed Silicon Nitride (HPSN)

- Gas Pressure Sintered Silicon Nitride (GPSSN)

By Grade

- Standard Grade

- High-Purity Grade

- Ceramic-Grade Powder

By Application

- Automotive & Transportation

- Electronics & Semiconductors

- Medical & Healthcare

- Aerospace & Defense

- Industrial & Metalworking

- Renewable Energy

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Silicon Nitride Market

- UBE Corporation

- Denka Company Limited

- Kyocera Corporation

- CeramTec GmbH

- AlzChem Group AG

- SINTX Technologies, Inc.

- CoorsTek, Inc.

- Toshiba Materials Co., Ltd.

- Rogers Corporation

- Morgan Advanced Materials

- 3M Technical Ceramics

- NGK Insulators, Ltd.

- H.C. Starck Tungsten Powders

- Yantai Tomley Hi-Tech Advanced Materials

- Vesta Si

*- List not Exhaustive