Market Overview: High-Purity, High-Temperature Technical Ceramics Transforming Semiconductor & E-Mobility Markets

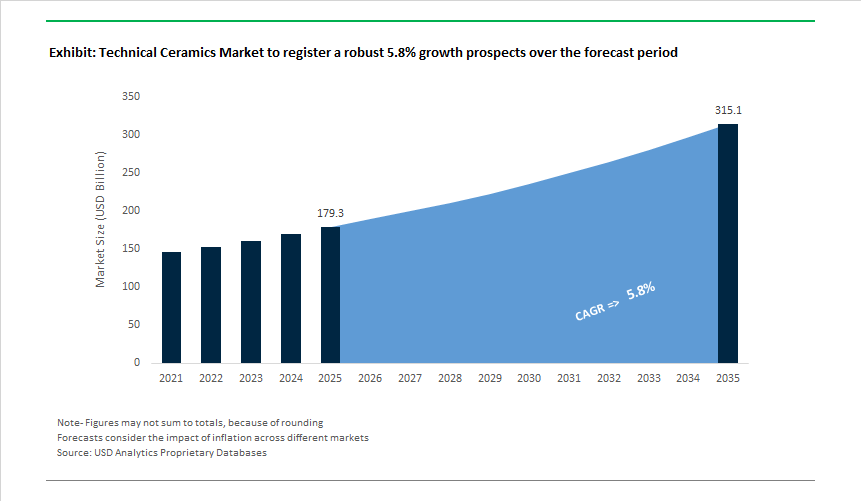

The Technical Ceramics Market is valued at USD 179.3 billion in 2025 and is projected to reach USD 315.1 billion by 2035, growing at a 5.8% CAGR as advanced industries redesign systems around purity control, thermal endurance, and lifetime reliability rather than metal-centric cost optimization. Technical ceramics are no longer treated as specialty substitutes; they are increasingly non-optional materials in environments where contamination, wear, or thermal failure directly undermine yield, safety, or regulatory compliance.

A primary structural driver is the semiconductor manufacturing ecosystem, where technical ceramics function as yield-protection materials rather than mechanical components. As device geometries shrink and plasma intensity increases, metals introduce unacceptable contamination, erosion, and particle-generation risks. Advanced ceramics are therefore being specified across etch, deposition, and chamber hardware because they can consistently meet sub-10 ppb contamination thresholds while maintaining dimensional stability under aggressive plasma exposure. For equipment OEMs and fabs, ceramic components directly influence tool uptime, wafer yield, and node-to-node scalability-making them strategic inputs embedded deep within long qualification cycles.

Electrification represents a second, equally durable growth pillar. In EV power electronics and thermal management, ceramics such as alumina and silicon nitride enable higher operating temperatures, improved thermal conductivity, and electrical insulation in compact modules. This allows power devices to function reliably beyond ~175°C, supporting higher power density, simplified cooling architectures, and extended component life. In this context, technical ceramics are not efficiency enhancers alone; they are platform enablers that reduce system complexity and warranty exposure in high-voltage architectures.

Healthcare and life-science applications reinforce the market’s defensiveness. Bioceramics are increasingly specified in joint replacements, dental implants, and spinal devices because of their exceptional wear resistance, biocompatibility, and long-term stability in the human body. By dramatically reducing wear particle generation and supporting multi-decade implant lifetimes, technical ceramics align with healthcare systems’ push toward lower revision rates and better long-term patient outcomes.

At the extreme end of operating conditions, high-temperature and structural ceramics are displacing metals in turbines, aerospace systems, hydrogen processing, and next-generation propulsion. These ceramics retain a high proportion of their mechanical strength at temperatures approaching 1,500°C, where metal alloys soften, oxidize, or creep. This capability enables new design envelopes for energy systems and advanced propulsion, positioning technical ceramics as critical materials in emerging low-carbon and high-efficiency technologies.

From a strategic and competitive perspective, success in the technical ceramics market is governed by microstructural control, process consistency, and scale economics, not by raw material access alone. Capital-intensive manufacturing, tight tolerances, and long customer qualification cycles create high barriers to entry and favor suppliers with deep materials science expertise and application-specific know-how. As a result, technical ceramics are increasingly treated as infrastructure-grade materials-embedded in systems where performance failure is unacceptable and substitution risk is minimal.

Market Analysis: Global Technical Ceramics Landscape Reshaped by Capacity Expansion, Electrification and Additive Manufacturing Advances

The recent few years marked a transformative phase for the Technical Ceramics Industry, marked by strategic investments, defense contracts, additive manufacturing breakthroughs, and material innovations targeting both semiconductor and EV verticals. In December 2024, CoorsTek completed a major expansion of its Oklahoma facility, increasing production of high-performance Alumina and Silicon Carbide components used widely in automotive powertrains and medical implants. This was followed by a surge in R&D-driven innovation across 2025, including a February 2025 global product launch of a next-generation PZT piezoelectric ceramic for IoT and ultrasonic sensors-highlighting the rapid convergence of ceramics with fast-growing sensing and connectivity markets.

Momentum intensified in early 2025 as additive manufacturing for ceramics made landmark progress. January 2025 academic results confirmed that binder jetting for SiC can achieve near-theoretical density, enabling industrial-scale adoption for intricate, high-strength components. By March 2025, CoorsTek secured a multi-year U.S. Department of Defense contract to supply lightweight SiC and Alumina ballistic armor components, reinforcing the material's strategic importance for defense modernization and soldier protection systems. In April 2025, Kyocera unveiled a breakthrough SiC-based material for semiconductor equipment, offering superior plasma erosion resistance-critical for long-life operation in etch and deposition chambers.

By June 2025, CeramTec introduced Sinalit, a high-power module substrate enabling improved thermal conductivity in EV inverters and renewable systems. The industry's shift toward electrification was further amplified in October 2025, when AGC Ceramics formed a China-based joint venture to expand sales of its BRIGHTORB 3D printing ceramic materials, addressing soaring demand for complex geometries in Advanced Ceramics. This culminated in November 2025, when Morgan Advanced Materials announced a large-scale Eastern European facility to boost Silicon Carbide (SiC) production for EV powertrains-a pivotal move aimed at meeting unprecedented global demand for high-temperature, high-strength ceramic components.

Technical Ceramics Market Trends and Opportunities

Trend 1: Ultra-Pure Technical Ceramics as Structural Anchors for High-NA EUV Lithography

The transition to 2 nm and sub-2 nm logic nodes has placed unprecedented mechanical and thermal constraints on lithography tool components, particularly within High-NA EUV platforms developed by ASML. At these nodes, even picometer-scale distortions translate directly into overlay errors and yield loss.

EUV tools operate under ultra-high vacuum to prevent photon absorption, making low-outgassing, ultra-pure ceramics non-negotiable. Advanced silicon carbide and cordierite-derived ceramics with near-zero CTE (<0.02×10⁻⁶/K) are now standard in wafer chucks, reticle stages, and mirror support frames. These materials maintain dimensional stability despite exposure to 500 W+ EUV sources, where thermal gradients would deform conventional metals.

In December 2025, reports from Shenzhen highlighted domestic EUV prototype systems relying on atomically smooth ceramic handling tools to achieve contamination control at the single-particle level—an essential requirement for any future sovereign semiconductor ecosystem. Beyond thermal stability, ceramics are also favored for their high Young’s modulus (>400 GPa), which prevents structural deflection as wafer stages accelerate and decelerate at extreme speeds within sub-nanometer tolerances.

Trend 2: Porous Ceramic Membranes for High-Temperature Hydrogen and Carbon Capture Systems

The global pivot toward green hydrogen and industrial carbon capture is accelerating adoption of ceramic membranes and filters capable of operating at temperatures where polymers and metals fail. Unlike organic membranes, technical ceramics retain mechanical strength and chemical inertness beyond 600 °C, enabling continuous operation in aggressive process streams.

In 2024–2025, hydrogen hub programs backed by the U.S. Department of Energy and initiatives such as ARCHES reinforced the role of ceramic-supported membranes in extracting hydrogen from ammonia cracking and syngas reforming. These systems consistently achieve 99.999% hydrogen purity, outperforming polymer membranes that degrade under sulfur, steam, and thermal cycling.

Material science advances are further refining performance. Research in 2025 demonstrated that microwave sintering can produce hierarchical pore architectures, delivering ~97% hydrogen recovery while resisting hydrogen embrittlement and corrosive capture solvents. In parallel, pharmaceutical and specialty chemical producers are specifying reusable ceramic filters because they tolerate aggressive chemical cleaning, reducing lifecycle waste compared with single-use filtration—an increasingly important consideration in regulated, sustainability-driven industries.

Opportunity 1: Silicon Carbide Ceramic Matrix Composites for Accident-Tolerant Nuclear Fuel

One of the most consequential opportunities for technical ceramics is emerging in nuclear energy, where SiC-based ceramic matrix composites (CMCs) are redefining safety benchmarks for fuel cladding. Traditional zirconium alloys soften near 800 °C and generate hydrogen during loss-of-coolant accidents. In contrast, SiC-CMCs maintain structural integrity beyond 1900 °C, dramatically reducing hydrogen generation and extending operator response windows.

Systems such as SiGA® SiC-CMC cladding developed by General Atomics have demonstrated order-of-magnitude improvements in accident tolerance. This capability is now being validated at scale. In FY-2025, the U.S. Office of Nuclear Energy allocated $97.9 million specifically to Accident-Tolerant Fuel programs, with irradiation tests at Idaho National Laboratory and MIT confirming gas-tightness and fission-product retention under high neutron flux.

Beyond existing light-water reactors, SiC-CMCs are emerging as the leading materials for Gen-IV systems such as molten salt and gas-cooled fast reactors. Their radiation tolerance and high-temperature strength support longer fuel cycles, directly improving plant economics while aligning with national energy security and decarbonization goals.

Opportunity 2: High-Thermal-Conductivity Ceramic Substrates for Electric Aviation and Advanced Power Electronics

Electric aviation and high-power mobility platforms are creating a step-change in demand for ceramic substrates that combine exceptional thermal conductivity with mechanical robustness. eVTOL aircraft and hybrid-electric propulsion systems face peak power loads during takeoff that exceed automotive EV requirements, while imposing far stricter weight and reliability constraints.

Aluminum nitride (AlN) substrates—offering 7× to 8× the thermal conductivity of alumina—are increasingly specified for SiC power modules in aerospace inverters, enabling rapid heat extraction in compact, liquid-cooled architectures. For vibration-intensive environments, silicon nitride substrates provide flexural strength above 600 MPa and superior fracture toughness, reducing failure risk in flight-critical electronics.

This substrate transition is already visible in adjacent sectors. By late 2025, high-thermal-conductivity ceramics were integrated into roughly one-third of high-stress EV inverter platforms, with aerospace adoption following closely. At the same time, suppliers such as CeramTec and Murata announced capacity expansions for AlN and Si₃N₄ substrates to support 5G and RF infrastructure—applications that face similar heat-flux and reliability challenges.

Market Share Analysis: Technical Ceramics Market

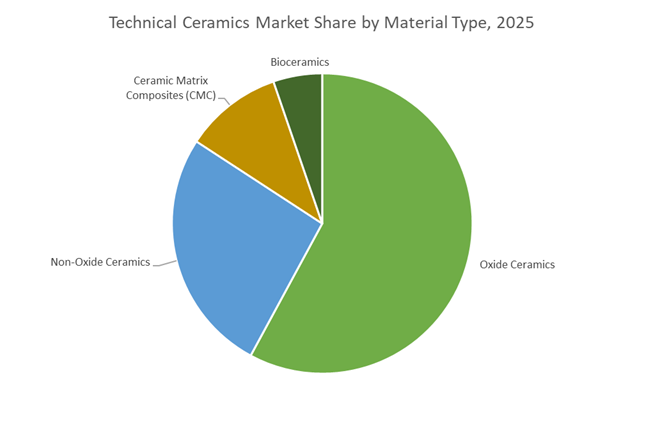

Market Share by Material Type: Oxide Ceramics Anchor Volume Through Cost-to-Performance Superiority

Oxide ceramics command approximately 55% of the global technical ceramics market, reflecting their role as the most industrially versatile and economically scalable ceramic class in 2025. Alumina (Al₂O₃) and Zirconia (ZrO₂) dominate procurement decisions because they offer a rare balance of high mechanical performance, chemical stability, and predictable cost curves, unlike non-oxide ceramics that often require niche processing or premium pricing. High-purity alumina at 99.9% purity has become the default material for semiconductor vacuum chambers and plasma-facing components, as fabs moving toward sub-3nm nodes require materials that combine zero outgassing with extreme plasma erosion resistance. Zirconia’s >1,000 MPa flexural strength positions it as one of the few ceramics capable of surviving impact-prone environments such as industrial cutting tools, fuel pumps, and automotive wear components, effectively replacing hardened steels in high-cycle applications. Equally critical is lifecycle economics: oxide ceramic valve and seal components now deliver up to 3.5× longer service life than stainless steel, materially reducing downtime and maintenance costs in chemical processing and fluid handling systems. On the precision end, oxide ceramics have achieved sub-angstrom surface finishes (Ra < 0.1 nm), enabling reliable bonding and thermal management in advanced microelectronics. This combination of manufacturability, durability, and cross-sector applicability explains why oxide ceramics remain the structural backbone of the technical ceramics market rather than a transitional material class.

Market Share by Application: Electronics & Semiconductors Drive Value Density and Specification Intensity

Electronics and semiconductors account for around 25% of total technical ceramics demand, but represent the highest value-density application segment due to extreme performance tolerances and zero-defect requirements. In 2025, oxide ceramics are no longer commodity substrates; they are mission-critical enablers for power electronics, 5G infrastructure, AI accelerators, and autonomous sensing systems. Alumina substrates delivering thermal conductivity of up to 24 W/m·K have become the preferred solution for over two-thirds of standard power modules, offering the most efficient cost-to-thermal balance for inverters, power supplies, and consumer electronics. From a signal-integrity standpoint, oxide ceramics maintain dielectric loss as low as 0.0004 at GHz frequencies, preserving over 95% signal efficiency in high-frequency telecom hardware—an essential metric for 5G base stations and early 6G development platforms. Reliability further differentiates this segment: ceramic semiconductor packages now demonstrate 99.99% hermetic sealing success, eliminating moisture-driven failure modes that limit plastic alternatives in image sensors, LiDAR, and RF modules. Beyond devices, ceramics also underpin upstream manufacturing through kiln furniture and firing systems capable of operating at 1,500°C while reducing energy consumption by roughly one-third, aligning electronics supply chains with 2025 ESG mandates. These performance and reliability imperatives explain why electronics and semiconductors, despite lower volume than industrial uses, retain a disproportionate share of market value within technical ceramics.

Competitive Landscape: Innovation-Driven Strategies Define Leadership in the Technical Ceramics Market

The competitive landscape of the Technical Ceramics Industry is defined by material-science leadership, regional manufacturing scale, semiconductor-grade purity capabilities, and technological diversification across medical, mobility, aerospace and semiconductor markets. Companies are expanding in high-growth regions, launching advanced ceramic material platforms, and deepening specialization in SiC, Si3N4, Alumina, Zirconia, and PZT systems. Additive manufacturing and plasma-resistant ceramics are emerging as core competitive differentiators.

Kyocera Corporation Strengthens Global Leadership Through Material Diversity and High-Purity Fine Ceramics

Kyocera continues to lead the global industry with more than 200 advanced ceramic materials, covering oxide, non-oxide, and single-crystal categories. Its expanding portfolio of Alumina and AlN substrates plays a pivotal role in semiconductor equipment, 5G modules, and high-frequency device packages. On the healthcare front, Kyocera supplies high-purity bioceramics that deliver exceptional biocompatibility and long-term implant durability. The company is also reinforcing its automotive presence through Silicon Nitride components designed for EV powertrains, offering unmatched thermal shock resistance and longevity. Its R&D advancements-such as improved SiC material performance for semiconductor tools-signal its commitment to extreme-condition ceramics and next-gen manufacturing.

Coorstek Expands Global Footprint With Advanced Ceramics For Defense, Aerospace and Electrification Systems

CoorsTek leverages a broad Advanced Ceramics portfolio that supports high-performance applications ranging from EV traction motors to aerospace and defense systems. Its trademark Cerbec® Silicon Nitride and Zirconia bearing elements provide superior high-speed rotation, wear resistance and low friction, enabling next-generation automotive and aerospace platforms. The company utilizes multiple advanced manufacturing processes-including extrusion, isostatic pressing and injection molding-to meet complexity and volume requirements. Its expansion of U.S. facilities underscores its role in supplying ballistic armor, semiconductor hardware, and high-reliability electronic components.

Ceramtec Drives High-Power Electronics and Medical Implant Innovation Through Precision Bioceramics

CeramTec is globally recognized for its BIOLOX® bioceramics, a leading choice for orthopedic hip and knee implants due to exceptional wear resistance and long-term biological compatibility. Its strong semiconductor presence includes Si3N4 and Zirconia Toughened Alumina (ZTA) substrates, which offer superior thermal performance for EV drive inverters and renewable systems. The company also leads in ceramic additive manufacturing using SiSiC and Al₂O₃ materials, enabling complex geometries unattainable via traditional methods. Its high-purity components support extreme semiconductor environments, highlighting CeramTec’s strength in precision-engineered Advanced Ceramics.

Morgan Advanced Materials Accelerates Sic Production and Extreme-Environment Solutions

Morgan Advanced Materials has strategically positioned its Technical Ceramics division to address high-temperature, high-wear sectors such as aerospace, hydrogen systems, semiconductors, and clean energy. With 3.7% organic revenue growth in 2024, the company is scaling operations through a dedicated CVD-SiC facility in South Korea, catering to semiconductor manufacturing equipment. Products such as Nilcra® MgPSZ offer superior toughness and wear resistance in pumps, valves and industrial systems. Morgan additionally supplies ceramic cores for turbine blades and complex structures requiring extreme thermal and mechanical stability.

Saint-Gobain Expands High-Performance Ceramics Portfolio With Sustainability and Extreme-Duty Solutions

Saint-Gobain’s Performance Ceramics & Refractories division maintains strong positions in SiC-based furnace linings, ballistic armor, and wear-resistant systems. The company’s “Lead & Grow” strategy outlines a pathway to accelerated growth through 2030, supported by its commitment to reducing CO₂ emissions by 40-45% by 2035. Offering specialized coatings and Nitride-Bonded SiC systems for mining and power generation, Saint-Gobain remains a key supplier for industries demanding thermal shock resistance, abrasion performance, and sustainability-aligned materials.

The United States has repositioned technical ceramics as a strategic input for semiconductor sovereignty and defense modernization, particularly in advanced packaging and hypersonic propulsion. In December 2025, the U.S. Department of Commerce announced a $1.6 billion CHIPS and Science Act allocation dedicated to advanced packaging, with ceramic interposers and high-thermal-conductivity substrates identified as critical enablers for next-generation AI accelerators and high-performance computing (HPC) architectures. This funding directly addresses U.S. reliance on East Asian suppliers for alumina and silicon nitride-based substrates used in heterogeneous integration.

Parallel to semiconductor initiatives, defense-linked demand is accelerating. In September 2025, AFWERX awarded $4 million to propulsion startups such as Firehawk Aerospace to advance ceramic matrix composites (CMCs) capable of surviving temperatures above 1,200°C in hypersonic flight. Additive manufacturing has further expanded the design envelope: late-2025 collaboration between HRL Laboratories and Prodways demonstrated 3D-printed silicon oxycarbide (SiOC) ceramics with fracture toughness suitable for structural aerospace components, reinforcing the U.S. push toward vertically integrated, high-value ceramic supply chains.

Japan: Ultra-Fine Powder Control Anchors 6G and Space Ceramics Leadership

Japan continues to dominate functional and electronic ceramics by leveraging unmatched expertise in ultra-fine powder synthesis and sintering control. In November 2025, Kyocera unveiled expanded production of fine cordierite and silicon-infiltrated silicon carbide (SiSiC) at Space Tech Expo Europe, scaling these near-zero–thermal-expansion materials for satellite mirrors and housings. Such properties are essential for optical stability in space and high-frequency signal integrity in advanced electronics.

Telecommunications is a second growth vector. Japanese leaders Murata Manufacturing and TDK significantly increased R&D investment into piezoelectric ceramics and zirconia resonators for 6G RF filters, where signal losses at extreme frequencies render conventional materials inadequate. Supporting this industrial shift, Japan’s GX 2025 policy subsidizes microwave and flash sintering, cutting kiln energy consumption by up to 40% and strengthening Japan’s competitiveness in low-carbon, high-precision ceramic manufacturing.

Germany: Euro 7 Compliance and Aerospace Ceramics Scale-Up

Germany is consolidating its position as Europe’s structural ceramics hub, driven by aerospace efficiency targets and stringent automotive emissions regulation. In March 2025, GE Aerospace announced a €78 million investment across European sites, including Germany, to scale next-generation ceramic components that enhance fuel efficiency and durability in widebody aircraft engines. These investments underscore the growing reliance on oxide and non-oxide ceramics in high-temperature, weight-sensitive aerospace environments.

Automotive regulation is an equally powerful driver. The implementation of Euro 7 standards has forced German suppliers to accelerate production of ceramic-coated brake discs, designed to meet the new 7 mg/km non-exhaust particulate limit. In parallel, the Bremen aerospace cluster has emerged as a center for additively manufactured SiSiC structures, with Kyocera Fineceramics Europe launching dedicated lines for topology-optimized space components. Together, these trends position Germany at the intersection of sustainability, aerospace resilience, and advanced ceramic processing.

China: EV Scale and Semiconductor Self-Sufficiency Drive Ceramic Localization

China is leveraging its massive domestic EV and electronics markets to accelerate commercial-scale adoption of silicon nitride and alumina ceramics. Under the Automotive Growth Stabilization Plan released by Ministry of Industry and Information Technology in September 2025, China is targeting 15.5 million New Energy Vehicle (NEV) sales by year-end. This scale has driven sharp demand for silicon nitride bearings and ceramic substrates in SiC power modules, where thermal dissipation and mechanical reliability are critical for 800V EV architectures.

At the same time, China is prioritizing foundry-grade technical ceramics to counter Western export controls. State-backed firms are developing ultra-high-purity alumina, yttria, and silicon nitride parts for lithography and etching equipment, aiming to match global benchmarks set by CoorsTek and Kyocera. In October 2025, tighter export controls on ceramic precursors were introduced, reinforcing China’s strategy of reserving high-purity materials for domestic semiconductor and EV manufacturing ecosystems.

India: ₹25,000 Crore PLI Accelerates Electronics and Bioceramics

India is transitioning from commodity ceramics to high-value technical ceramic manufacturing through targeted incentives. In January 2025, the government launched a ₹25,000 crore ($3 billion) PLI scheme for electronic components, explicitly covering ceramic capacitors, PCBs, and camera modules, with a goal of attracting over ₹40,000 crore in cumulative investment. This initiative positions ceramics as foundational to India’s electronics self-reliance strategy rather than a peripheral input.

Medical and energy infrastructure further reinforce demand. Under Make in India, Carborundum Universal expanded production of bioinert zirconia for orthopedic and dental implants, addressing India’s ~70% import dependence in high-end medical devices. Concurrently, India’s addition of 24.5 GW of solar capacity in 2024–2025 has generated large-scale domestic demand for ceramic insulators and high-voltage substrates, anchoring long-term growth across power transmission and renewable energy systems.

South Korea: Semiconductor Megacluster Pulls Advanced Process Ceramics

South Korea is embedding technical ceramics into its KRW 700 trillion (~$534 billion) semiconductor megacluster strategy, particularly for advanced memory and AI packaging. Leading fabs Samsung Electronics and SK Hynix have partnered with domestic ceramic specialists to develop yttria-coated and high-purity alumina components capable of withstanding plasma-rich environments in 3D NAND fabrication.

Beyond front-end processing, the government is funding R&D into glass-ceramic interposers as alternatives to organic substrates for CoWoS and HBM stacking. These materials offer superior thermal stability and dimensional control, essential for AI-driven high-bandwidth memory architectures. As a result, technical ceramics are increasingly viewed as a core enabler of South Korea’s foundry and AI competitiveness rather than a supporting material.

2025 Strategic Matrix: Technical Ceramics National Milestones

Technical Ceramics Strategic Matrix

|

Country

|

Primary Market Driver

|

2025 Strategic Milestone

|

Key Material Focus

|

|

United States

|

Defense & semiconductors

|

$1.6B CHIPS advanced packaging funding

|

Ceramic matrix composites (CMCs)

|

|

Japan

|

6G & satellite technology

|

Kyocera fine cordierite scale-up

|

High-purity Si₃N₄ & SiSiC

|

|

Germany

|

Euro 7 & green aerospace

|

€78M GE Aerospace ceramics expansion

|

Alumina & ceramic-coated systems

|

|

China

|

EV domination (NEVs)

|

15.5M NEV growth roadmap

|

Silicon nitride bearings & substrates

|

|

India

|

Electronics PLI

|

₹25k Cr component incentive scheme

|

Ceramic capacitors & bioceramics

|

|

South Korea

|

AI chip packaging

|

Integration into $534B megacluster

|

Plasma-resistant alumina & glass-ceramics

|

Technical Ceramics Market Report Scope

Technical Ceramics Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$179.3 Billion

|

|

Market Size (2035)

|

$315.1 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Material Type (Oxide Ceramics, Non-Oxide Ceramics, Ceramic Matrix Composites, Bioceramics), By Product Type (Monolithic Ceramics, Ceramic Coatings, Ceramic Matrix Composites, Ceramic Membranes & Filters), By Application (Electronics & Semiconductors, Aerospace & Defense, Automotive, Medical & Healthcare, Energy & Power, Industrial & Machinery)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kyocera Corporation, CeramTec GmbH, CoorsTek Inc., Morgan Advanced Materials plc, Saint-Gobain S.A., NGK Insulators Ltd., 3M Company, Nippon Electric Glass Co. Ltd., Murata Manufacturing Co. Ltd., SCHOTT AG, H.C. Starck High-Performance Powders, Rauschert Steinbach GmbH, Vesuvius plc, McDanel Advanced Ceramic Technologies, DOWA Electronics Materials Co. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Technical Ceramics Market Segmentation

By Material Type

- Oxide Ceramics

- Non-Oxide Ceramics

- Ceramic Matrix Composites (CMC)

- Bioceramics

By Product Type

- Monolithic Ceramics

- Ceramic Coatings

- Ceramic Matrix Composites

- Ceramic Membranes & Filters

By Application

- Electronics & Semiconductors

- Aerospace & Defense

- Automotive

- Medical & Healthcare

- Energy & Power

- Industrial & Machinery

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Technical Ceramics Market

- Kyocera Corporation

- CeramTec GmbH

- CoorsTek, Inc.

- Morgan Advanced Materials plc

- Saint-Gobain S.A.

- NGK Insulators, Ltd.

- 3M Company

- Nippon Electric Glass Co., Ltd.

- Murata Manufacturing Co., Ltd.

- Schott AG

- H.C. Starck High-Performance Powders

- Rauschert Steinbach GmbH

- Vesuvius plc

- McDanel Advanced Ceramic Technologies

- DOWA Electronics Materials Co., Ltd.

*- List not Exhaustive