Market Overview: High-Performance Ceramics Transforming Aerospace, Electronics & Energy Systems

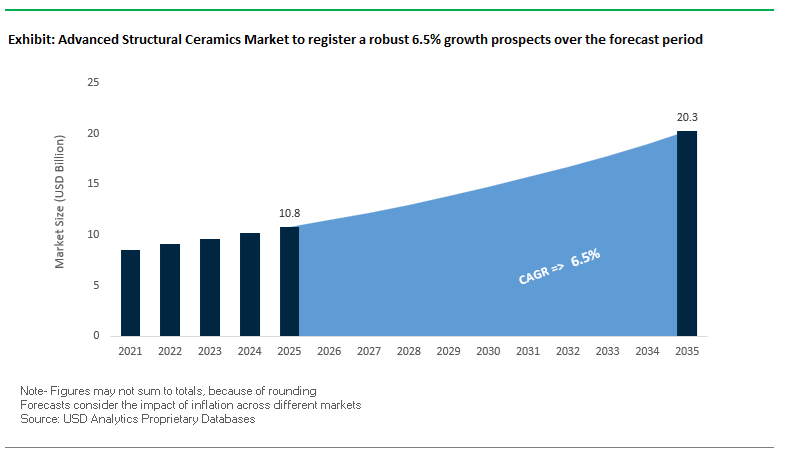

The Global Advanced Structural Ceramics Market is expected to reach USD 10.8 billion in 2025, expanding to USD 20.3 billion by 2035, with a robust CAGR of 6.5% (2025–2035). Market growth is accelerated by the rising deployment of zirconia, silicon carbide (SiC), alumina (Al₂O₃), ceramic matrix composites (CMCs), and high-purity technical ceramics across aerospace propulsion systems, electric vehicles (EVs), high-performance semiconductor fabrication, industrial wear components, biomedical implants, and next-generation thermal management systems. For manufacturers and vendors, demand is increasingly driven by performance metrics such as thermal shock resistance, extreme hardness, chemical inertness, high thermal conductivity, low density, and wear durability, establishing advanced ceramics as essential materials in high-value engineering applications.

Zirconia-based thermal barrier coatings (TBCs) now offer up to 100°C metal temperature reduction in gas turbine engines, and research indicates next-generation low-conductivity coatings may exceed 200°C reduction, unlocking higher turbine inlet temperatures and improved fuel efficiency. In EVs, SiC and AlN ceramic substrates dissipate heat 5–10× faster than polymer-based fillers, improving inverter efficiency by an estimated 9%. High-hardness alumina and SiC ceramics with 1,700–2,500 HV Vickers hardness dominate industrial pump seals and bearings enabling 20,000+ hour lifecycles. CMC substitution for nickel superalloys in jet engines reduces component weight by ≥60%, crucial for boosting thrust-to-weight ratios. Semiconductor fabrication increasingly relies on ultra-high-purity alumina and yttria ceramics to meet ≤1 particle per wafer pass, essential for 5nm and 3nm nodes.

Key Insights for Manufacturers and Vendors

- Thermal Barrier Leadership: Zirconia-based TBCs enable 100–200°C engine metal temperature reductions, supporting next-gen turbine efficiency standards.

- EV System Efficiency: SiC and AlN substrate integration boosts EV inverter efficiency by ~9%, reinforcing ceramic demand in mobility electrification.

- Extreme Hardness Advantage: Structural ceramics with 1,700–2,500 HV hardness deliver multi-year durability in high-wear industrial machinery.

- Lightweight Jet Engine Materials: SiC/SiC CMCs offer ≥60% weight reduction, enabling superior aerospace propulsion performance.

- Semiconductor Purity Requirements: Advanced ceramics maintain ~1 particle per wafer pass, critical for 3 nm fabrication precision.

Market Analysis: Capacity Expansions, Semiconductor Investments & Aerospace Applications Accelerating Structural Ceramics Demand

The advanced structural ceramics market is undergoing rapid transformation as global OEMs scale production capabilities in medical implants, semiconductor equipment, and aerospace propulsion systems. In October 2025, Kyocera Fineceramics Medical GmbH inaugurated a state-of-the-art manufacturing facility in Waiblingen, Germany, dedicated to BIOCERAM AZUL® ceramic ball heads, strengthening Europe’s orthopedic ceramics supply chain. In June 2025, Morgan Advanced Materials conducted its first real-time ceramic sintering research, a notable breakthrough aimed at improving consistency and throughput for SiC and alumina-based structural ceramics. Meanwhile, Kyocera expanded its materials portfolio in August 2025 with the introduction of StarCeram® N3000P, a silicon nitride variant engineered for extreme stress environments in gas-lubricated industrial seals.

Capacity expansion initiatives signal intensifying competition. In February 2025, Saint-Gobain NorPro announced a USD 40 million investment to establish a new ceramics facility in Wheatfield, New York, aimed at scaling production for industrial refractories, filtration ceramics, and wear-resistant products. Legal clarity is also shaping the competitive landscape: in October 2025, the U.S. Supreme Court’s affirmation allowing CoorsTek Bioceramics to market its pink hip components solidified competitive pathways in the biomedical ceramics market. Additionally, Kyocera Fineceramics Europe extended its semiconductor-focused footprint by expanding into a new technology and production site in Erfurt, Germany in January 2025, enhancing capabilities for semiconductor testing and manufacturing components.

Innovation-led collaborations continue to reinforce material performance improvements. In May 2024, Morgan Advanced Materials and Penn State University expanded their joint program to advance SiC technology for high-temperature and wear-intensive applications. By December 2024, Kyocera introduced a new silicon nitride material purpose-built for functional testing of next-generation microchips, supporting the rapidly growing complexity and thermal load requirements of cutting-edge semiconductor devices. Collectively, these developments highlight strong multi-sector demand for advanced structural ceramics, driven by semiconductor scaling, EV electrification, aerospace propulsion efficiency, and medical implant durability.

Transformational Trends Driving Hydrogen-Ready SiC Components and Semiconductor-Grade Precision Ceramics

Market Trend 1: Deployment of SiC and Si₃N₄ Ceramics in Hydrogen Co-Fired Industrial Gas Turbines

A defining trend in the Advanced Structural Ceramics Market is the shift toward Silicon Carbide (SiC) and Silicon Nitride (Si₃N₄) hot-gas path components capable of operating under the extreme conditions required for hydrogen co-firing. These ceramics sustain structural integrity at 1,350–1,450°C, exceeding the operational temperature limit of advanced nickel-based superalloys by 100–350°C, even when those alloys use TBCs. This elevated temperature capability enables higher turbine inlet temperatures, improving cycle efficiency and reducing CO₂ emissions.

SiC’s protective SiO₂ oxidation layer dramatically suppresses oxidation rates, with optimized SiC grades showing parabolic oxidation kinetics three orders of magnitude lower than traditional liquid-phase sintered SiC at 1,450°C (e.g., 4.91×10⁻⁵ mg²/cm⁴h). The material’s low density (≈3.2 g/cm³ versus ≈8.5 g/cm³ for superalloys) provides ≥60% weight reduction, reducing rotor mass, lowering mechanical stresses, and enabling faster ramp rates—all crucial for renewable-integrated power systems.

SiC and Si₃N₄ also exhibit exceptional thermal shock resistance, enabled by their high thermal conductivity and low CTE, making them uniquely suited to withstand rapid temperature swings during turbine start-up and shutdown. This combination of high-temperature strength, oxidation resistance, low density, and thermal shock stability is establishing SiC/Si₃N₄ ceramics as foundational materials for next-generation hydrogen-ready turbine architectures.

Market Trend 2: Precision Miniaturization of Alumina and Zirconia Components for Advanced Semiconductor Manufacturing

A second major trend is the rapid expansion of alumina (Al₂O₃), zirconia (ZrO₂), and ZTA structural ceramics in semiconductor manufacturing equipment where extreme cleanliness, precision, and plasma durability are essential. High-purity zirconia and ZTA components achieve ultra-smooth surface finishes of ≤0.02–0.05 μm (20–50 nm), minimizing particle contamination in vacuum chambers used for sub-3 nm semiconductor nodes. Such surfaces prevent micro-flaking, improve seal integrity, and reduce wafer defects.

Dimensional stability is equally critical. Zirconia-based ceramics exhibit thermal expansion coefficients of ≈7–8×10⁻⁶/K, enabling consistent wafer alignment even across wide plasma temperature cycles. In plasma etch chambers, high-purity alumina demonstrates erosion rates up to 10× lower under harsh halogen-based chemistries (CF₄, Cl₂) compared to alternative ceramics or polymers, ensuring extended equipment uptime.

Additionally, alumina’s dielectric strength >10 kV/mm makes it indispensable for electrostatic chucks and high-voltage insulation components. As semiconductor geometries continue shrinking and contamination tolerances tighten, precision-engineered structural ceramics will remain a core enabler of next-generation chip fabrication.

High-Value Opportunities in Thermal-Management Ceramics and Self-Healing Protective Coatings

Market Opportunity 1: Engineering High-Thermal-Conductivity AlN Substrates for Ultra-High-Power GaN RF Devices

The rise of GaN-based RF and power electronics is creating a significant opportunity for Aluminum Nitride (AlN) substrates, driven by their exceptional thermal and mechanical compatibility. High-purity AlN materials deliver thermal conductivity of 170–200+ W/m·K, approximately 5–6× higher than alumina (≈35 W/m·K) and approaching non-toxic alternatives to Beryllium Oxide (BeO, ≈260 W/m·K).

AlN’s CTE of ≈4.5×10⁻⁶/K closely matches GaN die (also ≈4–5×10⁻⁶/K), minimizing thermal stresses, die cracking, and delamination during high-power operation. Replacing alumina with AlN can reduce semiconductor junction temperatures by 20–40°C, enabling longer device lifetimes, higher RF output power, and superior reliability in demanding telecom, defense radar, EV powertrain, and satellite communication systems.

As RF power densities continue rising, thermally advanced AlN substrates are becoming essential to maintain stable thermal management and packaging reliability across high-frequency and ultra-high-power platforms.

Market Opportunity 2: Commercialization of Self-Healing Ceramic Coatings for Extreme Temperature Corrosion and Erosion Protection

A transformative opportunity in the Advanced Structural Ceramics Market is the development of self-healing ceramic coatings designed for high-temperature corrosion and erosion environments found in turbines, industrial furnaces, and aerospace propulsion. These coatings leverage embedded SiC or MAX-phase particles within a mullite or ZrO₂ matrix to autonomously seal cracks during operation.

Self-healing systems exhibit complete closure of micro-cracks up to ~10 μm within 1–4 hours at 1,000–1,200°C, restoring structural continuity through oxidation-induced SiO₂ flow. This mechanism can recover ≥90% of the original fracture strength, significantly extending component service life.

Thermal barrier coatings (TBCs) incorporating self-healing additives demonstrate an ~18.5% reduction in mass loss under accelerated erosion conditions compared to conventional YSZ coatings. Breakthrough research has also lowered the effective healing temperature by ~250°C, enabling crack healing at temperatures achievable in a broader range of industrial applications.

These systems offer a path to longer component lifetimes, reduced maintenance cycles, and more resilient high-temperature infrastructure across energy, aerospace, and heavy industry.

Advanced Structural Ceramics Market Share Analysis

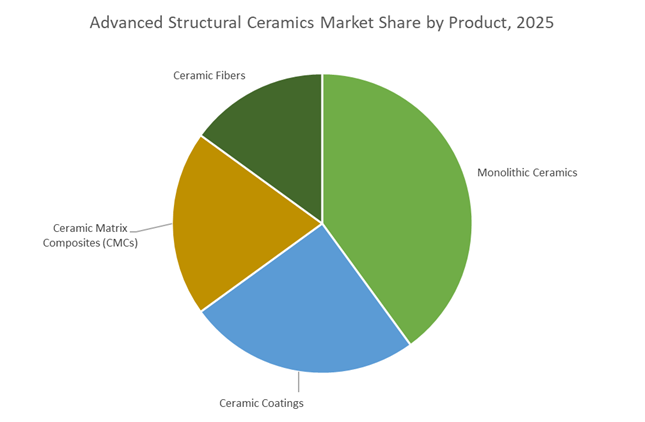

Market Share by Product Application: Monolithic Ceramics Lead Due to High-Volume Adoption Across Electrical, Mechanical, and Thermal Systems

Monolithic ceramics hold the largest share of the advanced structural ceramics market—approximately 40% in 2025—because they represent the most established, cost-efficient, and widely utilized class of advanced ceramic materials, enabling high-volume adoption across electrical insulation, wear-resistant components, and high-temperature industrial systems. Their mature manufacturing routes—such as pressureless sintering, hot pressing, and isostatic pressing—allow alumina, zirconia, and silicon carbide to be produced with consistent microstructure, high purity, and tight dimensional tolerances, supporting large-scale deployment where performance reliability is non-negotiable. These materials provide exceptional hardness, corrosion resistance, dielectric strength, and thermal stability, making them indispensable for substrates, insulators, seals, bearings, pump components, furnace linings, and catalyst supports. While emerging technologies like ceramic matrix composites (CMCs) and ceramic fibers cater to advanced aerospace and energy applications, monolithic ceramics dominate overall market share because they address the largest volume of industrial and electronic use cases and offer competitive cost-to-performance advantages. Their ubiquity in foundational sectors such as electronics manufacturing, power electronics, chemical processing, and industrial machinery ensures that monolithic ceramics remain the anchor segment of the advanced structural ceramics market.

Market Share by End-Use Industry: Electronics & Semiconductor Sector Drives Demand Through Non-Substitutable Ceramic Components

The Electronics & Semiconductor industry accounts for approximately 30% of the global advanced structural ceramics market, driven by its reliance on ceramic materials that offer unmatched dielectric properties, thermal conductivity, plasma resistance, and dimensional stability across high-frequency, high-power, and high-precision applications. Advanced ceramics such as alumina, aluminum nitride, and silicon carbide are essential for substrates, packaging components, chip carriers, and insulators used in power electronics, RF modules, microprocessors, and 5G infrastructure hardware. The explosive growth of MLCCs (Monolithic Ceramic Capacitors)—with hundreds used in a single smartphone and thousands in electric vehicles—further solidifies the sector’s commanding share. In semiconductor fabrication, ceramics serve as critical components in etching chambers, wafer handling systems, and deposition equipment, where they must withstand corrosive plasmas, extreme thermal cycling, and highly controlled vacuum processing environments. As semiconductor nodes shrink, and as AI accelerators, IoT devices, and EV power management systems drive demand for high-reliability thermal substrates and insulating materials, the Electronics & Semiconductor segment continues to expand its dominance, reinforcing its position as the primary growth engine of the advanced structural ceramics market.

Country Analysis: Global Drivers in Advanced Structural Ceramics Development

United States: Rapid Expansion in Ceramic Matrix Composites and Defense-Grade High-Performance Ceramics

The United States remains a central innovation hub in the Advanced Structural Ceramics Market, propelled by aerospace modernization, defense propulsion technologies, and large-scale electrification. A defining development is the breakthrough in 3D-printed Silicon Oxycarbide (SiOC) ceramics, announced in September 2025 by HRL Laboratories and Prodways, enabling the fabrication of dense, ultra-strong ceramic components with geometries previously impossible using traditional sintering. This advancement positions the U.S. as a global leader in next-gen ceramic additive manufacturing, particularly for high-temperature aerospace structures, thermal protection systems, and propulsion components.

U.S. defense-driven demand further strengthens the market. Firehawk Aerospace secured $4 million in AFWERX funding (September 2025) to accelerate ceramic-based propulsion technologies, highlighting the strategic significance of ceramics in rocket nozzles, hypersonic vehicles, and combustion chambers where materials must withstand extreme thermal shock. Parallel to defense initiatives, the U.S. is witnessing a major transition in Silicon Carbide (SiC) wafer production, with manufacturers scaling from 6-inch to 8-inch wafers to support EV power electronics operating at 800V+ architectures. Additionally, SINTX Technologies' acquisition of TAT (2022) underscores a push toward vertical integration across aerospace, defense, biomedical, and industrial ceramic platforms, enhancing domestic supply chain resilience.

China: Aggressive Scaling in SiC Wafers, Ultra-High-Temperature Ceramics, and Volumetric Alumina Production

China’s role in the Advanced Structural Ceramics Market is expanding rapidly as the country strengthens its semiconductor infrastructure and EV supply chains. Supported by large-scale state funding, Chinese manufacturers are building extensive new facilities for Silicon Carbide (SiC) substrates, which are essential for EV inverters and 800V architectures requiring high-voltage, high-efficiency switching performance. This aggressive capacity expansion positions China as one of the fastest-growing global suppliers of SiC materials.

China also invests heavily in Ultra-High-Temperature Ceramics (UHTCs), with academic and government laboratories developing Zirconium Oxycarbide-based materials capable of withstanding temperatures approaching 3,500°C. These innovations are intended for hypersonic aircraft, reusable launch vehicles, and classified defense applications. Simultaneously, China maintains its dominance in mass-produced Alumina ceramics, a foundational structural ceramic used across automotive sensors, high-wear industrial components, substrates for electronics, and electrical insulation—sectors that rely on high-volume, cost-efficient ceramic solutions.

Japan: Precision Leadership in Ceramic Electronic Packaging and Silicon Nitride Automotive Components

Japan retains a global leadership position in high-reliability structural ceramics, especially in advanced electronic packaging, automotive sensors, and high-temperature engine components. Companies such as Kyocera and Murata Manufacturing are at the forefront of ceramic substrates and packaging solutions, supplying critical components for 5G networks, automotive ECUs, medical electronics, and power modules. Their expertise in microstructure control and high-density ceramic sintering allows the production of substrates with superior dielectric properties, dimensional stability, and thermal reliability.

Japan’s advanced material capabilities extend to automotive innovation, with manufacturers pioneering Silicon Nitride (Si3N4) applications in glow plugs, rocker arm pads, turbocharger rotors, and high-speed bearings. These components benefit from Si3N4’s exceptional high-temperature strength, thermal shock resistance, and low density, enabling enhanced combustion efficiency and fuel savings. Japan is also expanding into emerging hydrogen economies—Kyocera’s 2025 showcase of ceramic solutions for hydrogen combustion liners and fuel cell stacks demonstrates the country’s position at the intersection of thermal materials engineering and clean energy technology.

European Union (Germany/France/UK): Ceramic Matrix Composites for Clean Energy, Hybrid Composites, and Circular Manufacturing Models

The European Union is increasingly focused on Ceramic Matrix Composites (CMCs) for aviation and clean energy applications, driven by sustainability mandates and the need for high-efficiency energy systems. A landmark initiative is the joint effort by Composites United and Fraunhofer IGCV (February 2025) to create a circular composite economy, establishing sustainable lifecycle strategies for fiber-reinforced and ceramic composite materials. This shift is crucial as Europe moves toward next-generation energy systems that require lightweight, thermally resilient, and low-carbon materials.

Demand for Oxide-Oxide CMCs is rising in Europe due to gas turbine retrofits aimed at increasing operational flexibility and supporting renewable gas integration. These CMCs exhibit exceptional performance at temperatures up to 1,300°C (with environmental barrier coatings), making them ideal for high-temperature industrial and power-generation applications. Furthermore, the region’s automotive sector—particularly in Germany and Italy—is adopting C/SiC composites for braking systems and structural lightweighting to comply with emissions regulations and performance standards. Collectively, these drivers position the EU as a major global center for hybrid composites, advanced CMC engineering, and sustainable ceramic innovation.

South Korea: Electronics-Driven Zirconia Demand and Growing Medical Ceramics Manufacturing

South Korea’s leadership in the global electronics industry reinforces its critical role in the Advanced Structural Ceramics Market. High-purity Zirconia ceramics are widely used across consumer electronics for thermal management, precision bearing components, and wear-resistant mechanisms in smartphones, laptops, and semiconductor handling tools. These applications benefit from Zirconia’s exceptional fracture toughness, dimensional stability, and surface smoothness—attributes crucial for precision electronic systems.

South Korea is also emerging as a key producer of dental and biomedical Zirconia, leveraging its advanced manufacturing ecosystem to supply aesthetically superior, biocompatible ceramic implants and crowns to global markets. Demand is bolstered by rising adoption of ceramic-based medical devices due to their corrosion resistance, hypoallergenic properties, and long-term structural integrity. As Korea simultaneously scales EV, semiconductor, and healthcare manufacturing, the country’s reliance on advanced ceramics will continue to expand across multiple high-technology sectors.

Competitive Landscape: Global Leaders Transforming High-Performance Ceramic Material Technologies

The competitive landscape of the Advanced Structural Ceramics Industry is anchored by established manufacturers with specialized capabilities in silicon nitride, alumina, zirconia, SiC, CMCs, and high-purity semiconductor ceramics. These companies differentiate through patented compositions, multi-step sintering technologies, vertically integrated production systems, and long-term partnerships in aerospace, medical, EV power electronics, and semiconductor manufacturing. Advancements in ceramic processing—including near-net-shape forming, hot isostatic pressing, advanced sintering, and CMC fabrication—give leading producers strong competitive advantages.

Kyocera Corporation strengthens global leadership in semiconductor and biomedical structural ceramics

Kyocera is a global leader in fine ceramics with dominant positions in silicon nitride (Si₃N₄), zirconia structural components, alumina, and aluminum nitride substrates. The company has strategically aligned its 2025 initiatives toward high-growth markets such as semiconductors, automotive electronics, and quantum technologies, supporting advanced 5G/6G millimeter-wave systems. Its expansion into a new production facility in Waiblingen (October 2025) for BIOCERAM AZUL® orthopedic ceramic ball heads reinforces its leadership in biomedical structural ceramics. Kyocera further strengthened its industrial ceramics portfolio with the StarCeram® N3000P silicon nitride launch (August 2025), delivering exceptional wear resistance and thermal durability for high-load sealing systems.

CoorsTek Inc. expands high-purity ceramic leadership across semiconductor, automotive and biomedical markets

CoorsTek provides one of the industry’s widest portfolios of alumina, zirconia, and silicon carbide structural ceramics, supporting semiconductor wafer handling, automotive powertrain systems, and industrial wear components. The company maintains a leading market share in high-purity alumina plasma etcher parts and SiC wafer boats, essential for advanced-node semiconductor fabrication. CoorsTek Bioceramics continues to be a major supplier for orthopedic and implantable ceramic components, leveraging material bioinertness for hip and knee replacements. It also manufactures polycrystalline YAG materials for lasers, autonomous vehicle systems, and next-generation medical device optics.

Morgan Advanced Materials accelerates SiC innovation for aerospace, defense and high-temperature applications

Morgan Advanced Materials produces an extensive range of alumina, zirconia, and SiC ceramics in both monolithic and composite formats for aerospace, defense, and thermal management markets. Its June 2025 real-time ceramic sintering research milestone supports more consistent and cost-efficient manufacturing of complex ceramic structures. The company collaborates closely with Penn State University to enhance SiC formulations for high-heat, high-wear environments. Morgan also supplies critical armor ceramics for defense vehicles and aircraft, alongside high-temperature seals and bearings for the oil & gas sector.

Saint-Gobain expands industrial ceramics footprint with major New York facility investment

Saint-Gobain produces high-performance silicon carbide and alumina ceramics for extreme industrial conditions, supplying filtration systems, refractory components, and wear-resistant assemblies. Its USD 40 million investment (February 2025) in a new Wheatfield, NY manufacturing facility significantly increases capacity for industrial ceramics and supports regional supply chain resilience. The company’s broader corporate strategy emphasizes industrial decarbonization, creating demand for advanced ceramics in high-efficiency heat exchangers and green technology filtration systems. Saint-Gobain remains a pivotal supplier for refractory and chemical processing sectors where thermal and corrosion resistance are mission-critical.

CeramTec GmbH reinforces its dominance in medical ceramics and EV automotive components

CeramTec is a leading pure-play ceramics manufacturer offering an extensive range of alumina, zirconia, and silicon nitride structural components. It is a global frontrunner in medical ceramics, producing BIOLOX® implant materials widely used in orthopedic and dental implants due to their superior wear performance and biocompatibility. CeramTec is also a major supplier of bearing balls for EV traction motors, enhancing drivetrain efficiency and durability. The company invests heavily in piezoceramics, enabling precision actuation and sensing in industrial machinery, high-frequency electronics, and process automation.

Advanced Structural Ceramics Market Report Scope

Advanced Structural Ceramics Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10.8 Billion

|

|

Market Size (2035)

|

$20.3 Billion

|

|

Market Growth Rate

|

6.5%

|

|

Segments

|

By Material Type (Alumina Ceramics, Silicon Carbide Ceramics, Zirconia Ceramics, Silicon Nitride Ceramics, Titanium Carbide, Boron Carbide, Ultra-High-Temperature Ceramics), By Product Application Type (Monolithic Ceramics, Ceramic Matrix Composites, Ceramic Coatings, Ceramic Fibers), By End-Use Industry (Aerospace & Defense, Electronics & Semiconductor, Automotive, Medical & Healthcare, Energy & Power, Industrial Machinery)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kyocera, CeramTec, CoorsTek, Morgan Advanced Materials, Saint-Gobain Performance Ceramics, 3M, Corning, NGK Insulators, Applied Ceramics, Murata Manufacturing, GE Aerospace, Blasch Precision Ceramics, Ceradyne (3M), SGL Carbon, SINTX Technologies

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Advanced Structural Ceramics Market Segmentation

By Material Type

- Alumina Ceramics (Al₂O₃)

- Silicon Carbide Ceramics (SiC)

- Zirconia Ceramics (ZrO₂, YSZ)

- Silicon Nitride Ceramics (Si₃N₄)

- Titanium Carbide (TiC)

- Boron Carbide (B₄C)

- Ultra-High-Temperature Ceramics (UHTCs)

By Product Application

- Monolithic Ceramics

- Ceramic Matrix Composites (CMCs)

- Ceramic Coatings

- Ceramic Fibers

By End-Use Industry

- Aerospace & Defense

- Electronics & Semiconductor

- Automotive

- Medical & Healthcare

- Energy & Power

- Industrial Machinery

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Advanced Structural Ceramics Market

- KYOCERA

- CeramTec

- CoorsTek

- Morgan Advanced Materials

- Saint-Gobain Performance Ceramics

- 3M

- Corning

- NGK Insulators

- Applied Ceramics

- Murata Manufacturing

- GE Aerospace

- Blasch Precision Ceramics

- Ceradyne (3M)

- SGL Carbon

- SINTX Technologies.

*- List not Exhaustive

Research Coverage: Advanced Structural Ceramics Market

The latest USDAnalytics study on the Global Advanced Structural Ceramics Market provides a comprehensive, data-driven assessment of how high-performance ceramics are transforming aerospace, electronics, EV power electronics, medical implants, industrial machinery, and next-generation energy systems. Spanning zirconia, alumina, silicon carbide, silicon nitride, CMCs, and ultra-high-temperature ceramics, this report investigates the full value chain from advanced powder processing and sintering breakthroughs to application-level adoption in turbines, semiconductor tools, and e-mobility platforms. It delivers in-depth analysis reviews of key demand drivers such as hydrogen-ready gas turbines, GaN/SiC power devices, semiconductor node migration, CMC engine parts, and orthopedic bioceramics, while also assessing capacity additions, technology partnerships, and regional manufacturing footprints. The study highlights critical performance benchmarks—thermal shock resistance, dielectric strength, purity thresholds, erosion resistance, and weight reduction—to help decision-makers quantify the competitiveness of advanced structural ceramics versus metals and polymers. With detailed coverage of regulatory trends, investment pipelines, and competitive strategies of major global players, this report is an essential resource for materials suppliers, OEMs, investors, and engineering leaders seeking to align product roadmaps with long-term growth opportunities in structural ceramics.

Scope Highlights

- Segmentation

- By Material Type: Alumina Ceramics (Al₂O₃), Silicon Carbide Ceramics (SiC), Zirconia Ceramics (ZrO₂, YSZ), Silicon Nitride Ceramics (Si₃N₄), Titanium Carbide (TiC), Boron Carbide (B₄C), Ultra-High-Temperature Ceramics (UHTCs)

- By Product Application: Monolithic Ceramics, Ceramic Matrix Composites (CMCs), Ceramic Coatings, Ceramic Fibers

- By End-Use Industry: Aerospace & Defense, Electronics & Semiconductor, Automotive, Medical & Healthcare, Energy & Power, Industrial Machinery

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Timeframe Coverage: Historic data from 2021 to 2025 and detailed market forecasts from 2026 to 2034.

- Company Coverage: Includes analysis and profiles of 15+ leading manufacturers and technology providers active in the Advanced Structural Ceramics Market.