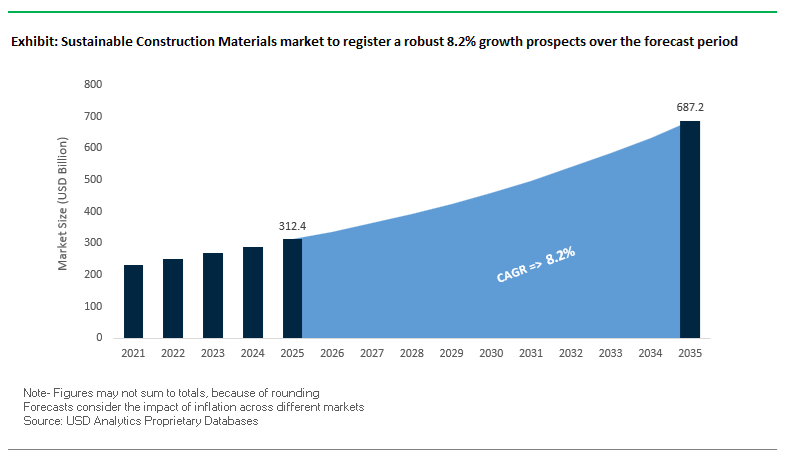

The Sustainable Construction Materials Market, valued at USD 312.4 billion in 2025, is projected to reach USD 687 billion by 2035, expanding at a strong CAGR of 8.2%. The market’s rapid evolution reflects the global shift toward low-carbon construction, regulatory pressure for embodied-carbon transparency, and accelerating adoption of green building certifications across commercial, residential, and infrastructure sectors.

The global Sustainable Construction Materials Market is experiencing transformative changes driven by regulatory accelerators, technological innovation, material substitution, and corporate decarbonization mandates. The increasing integration of advanced insulation, bio-based materials, circular construction inputs, and low-carbon cement is aligning market growth with international climate frameworks including the EU Taxonomy, LEED v5, global net-zero commitments, and national embodied-carbon legislation. The market is also being reshaped by rapidly expanding portfolios of sustainable cement, recycled aggregates, green steel, and high-performance building envelope solutions. Government funding—including Germany’s €500 million grants for bio-based building materials in May 2025—demonstrates how policy is lowering entry barriers and accelerating commercialization of mass timber, hempcrete, geopolymers, and low-carbon composites.

Recent developments between March 2025 and November 2025 highlight a market characterized by strategic M&A, technology modernization, and supply chain restructuring. In November 2025, CRH completed its USD 2.1 billion acquisition of Eco Material Technologies, strengthening its position in supplementary cementitious materials (SCMs) including fly ash and further aligning its operations with low-carbon cement production. In October 2025, Mitsubishi Chemical advanced its R&D footprint by completing a pilot wastewater treatment facility to boost cleaner manufacturing processes within chemical inputs used across sustainable insulation and coatings. The September 2025 partnership among Asahi Kasei, Mitsui Chemicals, and Mitsubishi Chemical for shared ethylene infrastructure further underscores the tightening relationship between petrochemical innovation and sustainable polymer-based building materials.

Adding further momentum, digital transformation is influencing material procurement and lifecycle management. In July 2025, a major global construction firm mandated AI-driven material forecasting and digital twin systems across all large-scale infrastructure projects by 2027—a landmark shift toward predictive, resource-efficient construction environments. Regulatory actions followed closely, with the European Commission releasing updated EU Taxonomy and LEED v5 guidelines in July 2025, raising the bar for embodied-carbon reporting and compelling manufacturers to invest in low-carbon product lines. Companies are also responding through product innovation; for example, a gypsum manufacturer launched a 95% recycled drywall line in June 2025, enhancing circular adoption across interior finishing segments. Earlier, in March 2025, a global engineering firm pioneered the use of geopolymer cement and recycled steel—reducing concrete use by 80% in a data center project—marking a significant milestone for structural-grade sustainable materials.

Market Insights: Global Sustainable Construction Materials Market Insights

Industry professionals increasingly demand materials that reduce lifecycle emissions, improve energy performance, comply with ESG frameworks, and enable circular construction models. The market continues to be shaped by structural changes—ranging from decarbonized cement and recycled aggregates to sustainable insulation, low-emission steel, and high-performance glazing—each addressing long-standing challenges of raw material intensity, waste generation, and operational energy inefficiency. As construction accounts for 40% of global raw material extraction and 37% of total emissions, demand for sustainable alternatives is no longer optional but foundational for regulatory compliance, investor trust, and long-term asset valuation.

- Construction consumes 40% of all raw materials globally, reinforcing the necessity for circular economy solutions and green material substitution.

- Low-carbon cement and blended alternatives reduce embodied carbon by 20–50%, reshaping the cement decarbonization landscape.

- Green building certifications cover 110,000+ projects worldwide, demonstrating accelerating institutional commitment to sustainability.

- Waste diversion rates of 75–85% are common in advanced sustainable construction projects due to increased use of recycled aggregates and reclaimed building elements.

- High-performance insulation and glazing enable 30–50% reductions in operational energy use, supporting the transition toward nearly zero-energy buildings (nZEB).

Trend 1 - Science-Based Carbon Targets Intensify Demand for Verified Low-Carbon Concrete

Corporate climate alignment with science-based emission pathways is reshaping procurement strategies across global construction and infrastructure markets. More than 7,000 companies worldwide are now formally committed to Science Based Targets initiative (SBTi) requirements, creating unprecedented pressure on cement, concrete, and steel supply chains to deliver quantifiable Scope 3 emissions reductions. This surge in corporate climate accountability has effectively repositioned low-carbon concrete from an alternative option to a compliance-essential material category for engineering firms, developers, and real estate portfolio owners.

Regulatory momentum amplifies this shift. The EU’s Ecodesign for Sustainable Products Regulation (ESPR) and the rollout of the Digital Product Passport (DPP) mandate standardized disclosure of embodied carbon, operationalizing transparency and penalizing high-carbon construction materials. These policies fundamentally transform purchasing patterns: high-impact materials can no longer hide behind incomplete reporting, while suppliers delivering verified low-carbon blends, alternative binders, and carbon-captured formulations gain strategic advantage.

Public procurement is also emerging as a high-impact demand catalyst. Initiatives such as Ireland’s Climate Action Plan explicitly prioritize longer-life, low-carbon cement blends in national infrastructure, showcasing how government purchasing power accelerates adoption across private markets. This institutional demand signals longevity, enabling suppliers of sustainable cementitious materials to scale with confidence.

Capital markets are reinforcing the same direction. In 2023, US$8.1 billion-around 14% of global climate tech venture funding-targeted industrial decarbonization, including carbon capture and utilization (CCU), next-generation concrete technologies, and sustainable material innovation. Such investment intensity strengthens the pathway from pilot technologies to commercial-scale production, reinforcing the long-term structural trend toward low-carbon construction materials.

Trend 2 - Digital Material Passports Accelerate Circular Economy Adoption in Construction

The transition toward a circular construction economy depends on the ability to track, certify, and reuse materials at end-of-life. The rapid emergence of Digital Product Passports (DPPs) is transforming demolition and waste streams into structured, high-value resource inventories. By late 2025, EU regulations require manufacturers and suppliers to maintain the data infrastructure necessary to generate DPPs for construction materials, forcing the industry to adopt digital traceability at scale.

This transparent data ecosystem directly benefits architects, builders, and waste management ecosystems. With standardized and verifiable product-level environmental data, stakeholders can now compare carbon footprints, validate the quality of certified timber, or evaluate performance attributes of bio-based insulation materials before specification. Material selection is shifting from cost-based decision-making to data-driven carbon and performance optimization, reinforcing the use of sustainable construction materials.

Industrial symbiosis hubs highlight the economic and environmental value of this digitalized circularity. The Humber industrial cluster in the UK demonstrated that advanced material exchange networks can deliver €2 million in annual savings while reducing 4,000 tonnes of CO₂e per year. These results show how integrated, digitally supported circular systems convert waste into economic assets-strongly validating the long-term role of material passports for demolition and reuse.

Opportunity 1 - Commercial Scaling of High-Performance Bio-Based Insulation Materials

Bio-based insulation materials are transitioning from specialized niche applications to mainstream commercial adoption, driven by regulatory alignment with building energy performance directives and mounting demand for low-embodied-carbon building solutions. Europe leads this shift, with Germany, France, and Scandinavian countries demonstrating widespread integration of bio-based insulation in new builds and renovation projects. These markets offer highly attractive scale-up environments for manufacturers seeking predictable regulatory tailwinds and mature green construction ecosystems.

Innovation is accelerating performance benchmarks. Global R&D programs increasingly focus on bio-based phase change materials, self-healing insulation systems, and aerogel-enhanced bio-composites-solutions engineered to overcome conventional limitations in fire safety, moisture control, and durability. These advanced sustainable insulation materials align with emerging commercial building codes requiring improved life-cycle performance, offering suppliers strong differentiation in high-value segments.

Strategic consolidation is also shaping the opportunity landscape. Kingspan Group’s acquisition of a leading bio-based insulation startup signals that major building materials manufacturers are expanding aggressively into natural and renewable insulation technologies. This acquisition trend underscores the accelerating commercialization path for next-generation bio-based insulation and validates long-term revenue potential for manufacturers innovating in low-carbon, high-efficiency building envelope solutions.

Opportunity 2 - Industrial Symbiosis Hubs Enabling Near-Zero-Carbon Cementitious Materials

Industrial symbiosis hubs are emerging as some of the most influential enablers of near-zero-carbon cementitious materials, creating localized value chains where waste becomes feedstock. The World Economic Forum’s Transitioning Industrial Clusters initiative, spanning 33 clusters across 16 countries, demonstrates a combined 832 million tonnes CO₂e reduction potential, highlighting the transformative scale achievable when materials, energy, and resources circulate within integrated ecosystems.

These synergies extend directly into cement production. Ports and industrial zones such as Antwerp-Bruges’ NextGen District are dedicating large areas-like its 88-hectare circular materials zone-to the recovery and revalorization of industrial byproducts. Slag, fly ash, and silica fume are becoming central to supplementary cementitious material (SCM) supply chains, reducing dependence on carbon-intensive clinker and enabling regional pathways to low-carbon cement.

Academic and industry-backed innovation further validates this opportunity. The Mud2Metal project has demonstrated complete utilization of Bauxite Residue, converting a traditional waste liability into a circular input for cementitious formulations and other industrial processes. These closed-loop systems show how symbiosis-driven material valorization can drastically reduce virgin material demand, strengthen resource efficiency, and support scalable production of low-carbon concrete solutions.

Sustainable Construction Materials Market Share Analysis

Market Share by Material Type: Dominance of Green Cement in Sustainable Construction Materials

Green Cement holds the leading 35% market share within the Material Type segment, and its dominance reflects a structural shift toward decarbonizing one of the world’s heaviest-emitting industries. This segment’s strong position is reinforced by the deepening global focus on reducing CO₂ emissions across cement and concrete value chains, an area where green cement technologies—such as fly ash–based, slag-based, and geopolymer formulations—deliver measurable impact. With conventional cement responsible for nearly 4–8% of global CO₂ emissions, industry professionals increasingly prioritize materials capable of eliminating or drastically reducing clinker content, the biggest emissions driver. Because 60% of cement’s emissions are tied to limestone calcination, replacing clinker with industrial byproducts enables emission cuts of up to 40%, making green cement the most effective near-term solution for embodied carbon reduction.

The substantial share commanded by Recycled/Reclaimed Materials (25%) further reflects tightening global circular economy mandates and the construction sector’s escalating waste generation. C&D waste volumes in large markets—such as the U.S., where debris output is more than double municipal waste—create a robust feedstock for recycled aggregates, reclaimed wood, and repurposed metals. Regions achieving 75–90% diversion rates demonstrate the scalability of recycling infrastructure, boosting adoption among contractors seeking lower costs, LEED points, and EPD-compliant materials. Meanwhile, Sustainable Insulation continues gaining traction due to its ability to cut building operational energy consumption by up to 50%, aligning directly with NZEB pathways and rising energy performance directives. Although these categories do not surpass green cement in share, they collectively accelerate the sector’s pivot toward integrated sustainability strategies that address both embodied and operational emissions across the full building lifecycle.

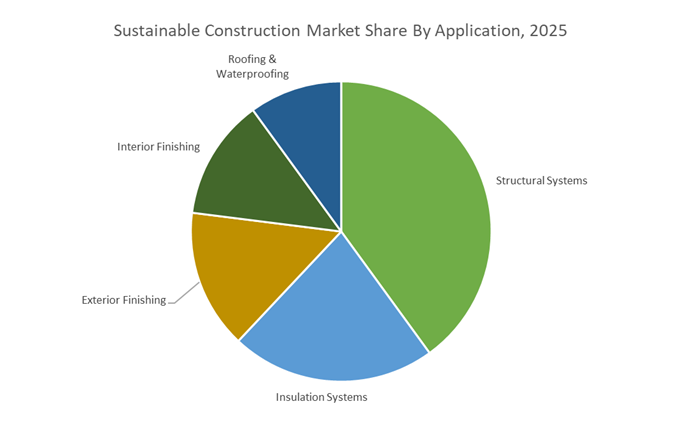

Market Share by Application: Structural Systems Lead Due to High Material Intensity and Decarbonization Impact

Structural Systems command the largest 40% share within the Application segment, underlining their central role in reducing embodied carbon and transforming core building performance. As the most material-intensive part of a building—spanning foundations, columns, slabs, framing, and load-bearing walls—structural systems consume the highest volumes of cement, steel, and aggregates. This positions the segment at the forefront of sustainability interventions, as substituting even a fraction of these materials with low-carbon alternatives produces disproportionate emissions savings. The adoption of Cross-Laminated Timber (CLT) and structural-grade engineered wood illustrates this shift, with CLT enabling 30–40% reductions in embodied CO₂ compared with steel or concrete systems. Additionally, mass timber’s natural carbon sequestration capability (~1 ton of CO₂ per cubic meter of wood) provides an added climate advantage, helping developers meet emerging embodied carbon caps in Europe, North America, and parts of APAC.

While Insulation Systems (22%) represent a smaller share, their influence on building performance remains substantial, especially as infrastructure owners prioritize operational efficiency over full lifecycle horizons. Because operational energy routinely exceeds embodied energy by several multiples over a building’s lifespan, high-performance insulation technologies have become indispensable for meeting carbon-neutrality policies and retrofit mandates. This segment’s share reflects the accelerating replacement cycle of outdated insulation materials, as well as the growing preference for bio-based or recyclable insulation solutions. Although Structural Systems remain unmatched in market share due to material volume and decarbonization potential, both categories are integral to advancing sustainable construction practices and helping markets transition toward net-zero buildings.

Country Analysis: Global Sustainable Construction Leadership

United States: Federal Buy Clean Policies Accelerating Low-Embodied Carbon Material Adoption

The United States Sustainable Construction Materials Market is undergoing one of the world’s most aggressive low-carbon transitions, driven by federal procurement dominance, stringent regulatory frameworks, and large-scale investments targeting low-embodied carbon (LEC) materials. The federal government has strategically positioned itself as the largest buyer of LEC construction inputs, reshaping demand signals across the entire domestic green building supply chain. A defining driver is the General Services Administration’s (GSA) $2 billion investment under the Inflation Reduction Act (IRA) to procure substantially lower embodied carbon construction materials for more than 150 federal projects. This move is solidifying LEC concrete, low-carbon steel, and climate-friendly building materials as the new standard for public infrastructure. The Federal Buy Clean Initiative, backed by $4.5 billion from the IRA, further deepens this regulatory push by prioritizing clean construction materials across federal procurement channels, making the U.S. one of the strongest demand creators for LEC innovation globally.

Infrastructure modernization is another major catalyst, with the U.S. Department of Transportation allocating $2 billion for states, Tribes, and local communities to adopt low-carbon materials in local infrastructure initiatives. Transparency in material sustainability profiles is advancing through the federal pilot program addressing carbon-intensive materials, which has already generated over 5,000 new Environmental Product Declarations (EPDs)—a significant boost to material-level carbon accounting. On the supply side, domestic manufacturing capacity for low-carbon materials is expanding rapidly, supported by the U.S. Department of Energy’s $6 billion Industrial Demonstrations Program (IDP) aimed at decarbonizing energy-intensive industries. In addition, the Federal-State Buy Clean Partnership, launched in 2023 with 13 states, is aligned toward harmonizing procurement standards and shaping a unified national market for clean, American-made construction materials. Together, these initiatives firmly establish the U.S. as a front-runner in sustainable construction adoption and regulatory-led decarbonization.

Germany: Deep Decarbonization of Cement and Advanced Wood Engineering Technologies

Germany stands at the forefront of Europe’s sustainable construction materials transition, particularly in the decarbonization of cement—the construction sector’s most emission-intensive material. A major development comes from Heidelberg Materials, which is spearheading carbon-reduced and circular cement technologies supported by a €100 million EIB loan signed in late 2023. This financial backing accelerates Germany’s leadership in carbon-neutral construction products. By 2024, Heidelberg Materials had already reduced its specific net carbon emissions to 527 kg CO₂ per tonne of cementitious material, with an ambitious target of 400 kg by 2030, signaling a rapid shift toward low-carbon cement standards within Europe.

Germany’s innovation extends beyond cement into advanced prefabricated and engineered wood technologies, with companies like GROPYUS integrating industrial automation, digitalization, and AI-driven design to manufacture wooden wall and slab elements. These solutions deliver up to 90% lower CO₂ emissions during construction and operation compared to conventional methods, positioning engineered wood as a central pillar in Germany’s low-carbon building future. Germany is also advancing carbon-sequestering construction materials, notably the CO2ncrEAT cement-free masonry block, designed to permanently lock CO₂ into building structures. However, despite its strong technological foundation, Germany faces challenges in scaling digital construction tools such as BIM and 3D concrete printing due to structural fragmentation within its SME-dominated construction ecosystem. Regionally, Germany is gaining momentum with connected sustainable home solutions, exemplified by the ABB Smart Energy Management System (EMS) launching in 2025, supporting EV chargers, heat pumps, and sustainable building automation—further reinforcing Germany's leadership in climate-aligned construction technologies.

China: Policy-Driven Green Building Expansion and Large-Scale Recycled Material Utilization

China remains the world’s largest construction market and demonstrates unmatched scale in implementing policy-driven sustainable construction reforms. The cornerstone is the national Green Building Action Plan, which mandates increasing the proportion of green buildings and shifting the market's emphasis from energy efficiency alone to reducing overall carbon emissions. China’s commitment is further strengthened through its development of a Zero Carbon Building Standard, built in collaboration with international sustainability experts, positioning the country to set future benchmarks for net-zero construction materials and design.

China’s advancement in sustainable construction is visible in its rapid expansion of certified green buildings—leading the world in LEED-certified project area in 2023, with 1,583 projects covering over 24.5 million square meters. The nation also champions prefabrication and modular construction, highlighted by the rapid construction of the 57-story Mini Sky City in just 19 days, significantly reducing material waste and embodying lower carbon footprints. Circular construction practices are increasingly prioritized, with strong incentives for using recycled construction waste, reclaimed bricks, and innovative materials such as designer “rebirth bricks”, created from debris reinforced with wheat branches. China is also integrating renewable energy directly into building designs, exemplified by the Sun-Moon Mansion, which features a massive 5,000 m² solar rooftop saving 2.5 tons of coal and producing 6.6 million kWh of electricity annually. With its policy momentum, technological capacity, and large-scale deployment, China continues to shape global trends in sustainable and circular construction ecosystems.

United Kingdom: Bio-Composite Breakthroughs and Carbon-Negative Material Adoption

The United Kingdom is rapidly establishing itself as a strategic hub for bio-based and carbon-negative construction materials, driven by a strong commitment to achieving Net-Zero by 2050. The country is experiencing accelerating adoption of Hempcrete, a rising bio-composite made from hemp fibers, lime, and water. Hempcrete is recognized for being carbon-negative, naturally insulating, lightweight, and highly durable—qualities that significantly enrich the U.K.’s sustainable construction landscape. Additionally, British innovators are exploring Ferrock, a next-generation material made from waste steel dust and silica. Ferrock offers superior strength compared to traditional cement and permanently captures CO₂ as it cures, reflecting the U.K.’s push for radically low-carbon binders.

The circular economy is deeply embedded in the U.K.'s sustainable construction agenda. Recycled steel, which consumes 75% less energy than virgin steel, is widely adopted, while recycled plastics are being transformed into waterproof roofing tiles and advanced insulation materials. Timber-based construction is also on the rise, especially Cross-Laminated Timber (CLT), which offers renewable structural alternatives to concrete and steel while providing substantial carbon storage benefits. Furthermore, the U.K. is taking major strides in biomaterial R&D, particularly with Mycelium Composites, grown from fungal root networks to create biodegradable, fire-resistant, and lightweight construction materials. Industry leadership is reinforced through corporate commitments like Balfour Beatty’s 2024 Sustainability Strategy – Building New Futures, which outlines clear pathways to enhance climate resilience, reduce material emissions, and accelerate sustainable infrastructure.

France: Mandatory Solarization Rules and Green Industry Tax Credit Driving Material Innovation

France is reshaping its built environment through strict decarbonization mandates and aggressive financial incentives targeting clean construction materials and renewable integration. Under the French Climate & Resilience Law, effective January 1, 2024, certain new buildings and their associated parking lots are legally required to install solarization or greening systems, such as green roofs—creating immediate and substantial demand for climate-friendly construction materials. Complementing this mandate is the powerful Green Industry Tax Credit, introduced under the 2024 Finance Act, providing 20% to 60% tax credits for investments supporting the domestic production of key green technologies, including batteries, solar panels, heat pumps, and wind components.

This tax credit also applies to capital expenditures such as machinery, buildings, land, and installations that expand green industrial capacity—boosting France’s competitive advantage in sustainable material manufacturing. Corporate innovation plays a major role, with French multinational Saint-Gobain continuing to pioneer lightweight construction solutions, low-carbon building materials, and high-performance smart glass technologies. At the same time, Bouygues Construction is collaborating with partners to lower emissions at the material level, especially through accelerated adoption of low-carbon cement technologies. France’s combination of strict regulatory enforcement, strong financial incentives, and corporate innovation places it at the leading edge of sustainable construction materials adoption in Europe.

Japan: High-Performance Eco-Material R&D and Green Growth Strategy Investments

Japan is accelerating its transition toward sustainable construction materials through massive investments, advanced R&D programs, and the development of next-generation eco-materials. Under its ambitious Green Growth Strategy, Japan is allocating 2 trillion yen (approx. USD 13.5 billion) by 2030 to support innovations aimed at replacing carbon-intensive materials such as plastics, steel, and conventional concrete. A standout initiative is the development of Cellulose Nanofibers (CNF)—often referred to as “Green Steel”—which offers a strength five times that of steel while being 80% lighter, opening transformative applications in construction and aerospace.

Japan’s material innovation extends to timber construction, supported by the 2010 Promotion of Wood Use Act, which mandates CLT utilization in public buildings for enhanced seismic resilience and carbon storage. The country is also advancing breakthrough carbon recycling technologies through the Moonshot R&D Program, including Kajima Corporation’s CO₂ Concrete, which uses captured CO₂ to create climate-positive building materials. Corporate leaders such as LIXIL are strengthening sustainable construction outcomes by designing water-efficient products like the SATO Tap, which reduces water use by 50% and incorporates 80% recycled ceramics. In the steel sector, the COURSE50 Project by Kobe Steel is exploring hydrogen-based iron ore reduction to cut steelmaking emissions by 30% by 2030. Together, these initiatives position Japan as a global leader in next-generation sustainable construction materials and high-impact decarbonization technologies.

Competitive Landscape: Global Leaders in Sustainable Construction Materials

The competitive landscape of the Sustainable Construction Materials Market is defined by innovation-led strategies, major decarbonization commitments, and rapid expansion into circular and low-carbon product lines. Leading companies are reshaping material flows through advanced cement chemistries, green steel transformation, high-performance building envelope solutions, circular aggregates, and carbon-capturing concrete technologies. Their strategies combine digitalization, lifecycle assessment transparency, acquisition of recycling capabilities, and large-scale R&D investments aimed at accelerating the transition toward net-zero construction ecosystems.

Holcim continues to lead the market by expanding its ECOPlanet low-carbon cement and ECOPact green concrete portfolios, focusing heavily on reducing embodied emissions across infrastructure and commercial projects. The company invests significantly in decarbonization technologies and has committed to reducing CO₂ intensity by 10% by 2025. Holcim also pioneers 3D-printing construction materials and modular systems, enabling faster, resource-efficient building processes. Through continuous portfolio expansion—including advanced insulation and roofing systems from its Firestone division—the company positions itself as the cornerstone of global sustainable construction innovation.

Saint-Gobain strengthens the sustainable construction supply chain through its leadership in insulation, high-performance glass, gypsum products, and lightweight materials. Its materials are instrumental in achieving energy efficiency and improved indoor environmental quality across residential and commercial buildings. With ongoing R&D aimed at reducing CO₂ emissions, Saint-Gobain integrates sustainability into high-profile projects, including applications in the Paris 2024 Olympic Village. By reducing transportation emissions through lightweight materials, the company enhances both environmental and structural performance for large-scale construction.

CRH leverages its global footprint in heavy building materials to accelerate the adoption of recycled aggregates and low-carbon cement technologies. A notable milestone was the November 2025 acquisition of Eco Material Technologies for USD 2.1 billion, strengthening its leadership in supplementary cementitious materials. CRH is also expanding its low-carbon asphalt production through its Tarmac division, emphasizing recycled content and reducing lifecycle emissions across road infrastructure. The dual focus on circular inputs and low-carbon output technologies solidifies CRH as a central player in the decarbonization of global construction.

ArcelorMittal, one of the world’s largest steel manufacturers, plays a critical role in reducing embodied carbon in structural materials. The company is actively developing hydrogen-based steelmaking pathways and deploying CCUS technologies across its facilities. Its innovations are visible through flagship projects, including producing reduced-carbon steel for the Paris 2024 Olympic Torch. ArcelorMittal’s sustainable steel solutions support high-performance structural applications and demonstrate the feasibility of large-scale decarbonization in heavy construction materials.

BASF integrates specialty chemicals, advanced binders, insulation materials, and high-performance coatings to strengthen energy-efficient construction systems. Its solutions reduce water consumption in cement, enhance concrete durability, and improve building envelope thermal performance. BASF also invests heavily in digital tools that provide lifecycle assessments (LCAs), helping construction firms and developers quantify environmental impacts and make informed procurement decisions. With strong capabilities in engineered wood additives and cool roof coatings, BASF’s portfolio is central to sustainable material innovation.

Cemex advances low-carbon and net-zero concrete solutions through its Vertua product line, achieving more than 40% CO₂ reduction in key markets. The company’s “Future in Action” strategy positions it at the forefront of cement decarbonization through alternative clinker factors, SCM integration, and carbon capture deployment. Cemex’s R&D programs are actively industrializing sustainable construction materials that reduce reliance on traditional cement chemistries. Its initiatives reinforce the company’s reputation as a global pioneer in net-zero cement and concrete innovation.

Sustainable Construction Materials market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$312.4 Billion

|

|

Market Size (2035)

|

$687 Billion

|

|

Market Growth Rate

|

8.2%

|

|

Segments

|

By Material Type (Green Cement, Recycled Metal, Bio-Based Composites, Recycled/Reclaimed Materials, Sustainable Insulation, Aggregates), By Application (Insulation Systems, Structural Systems, Roofing & Waterproofing, Interior Finishing, Exterior Finishing), By End-User (Building Construction, Industrial Construction, Infrastructure), By Construction Type (Structural Materials, Non-Structural Materials)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Holcim, Saint-Gobain, Sika AG, Heidelberg Materials, Kingspan Group PLC, CRH plc, Cemex, Owens Corning, Skanska, VINCI, Bouygues, ACCIONA, Kajima Corporation, DuPont de Nemours Inc., BASF SE

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Sustainable Construction Materials Market Segmentation

By Material Type

- Green Cement

- Recycled Metal

- Bio-Based Composites

- Recycled/Reclaimed Materials

- Sustainable Insulation

- Aggregates

By Application

- Insulation Systems

- Structural Systems

- Roofing & Waterproofing

- Interior Finishing

- Exterior Finishing

By End-User

- Building Construction (Residential, Commercial, Institutional)

- Industrial Construction (Manufacturing Plants, Data Centers)

- Infrastructure

By Construction Type

- Structural Materials

- Non-Structural Materials

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Sustainable Construction Materials Market

- Holcim (LafargeHolcim)

- Saint-Gobain

- Sika AG

- Heidelberg Materials

- Kingspan Group PLC

- CRH plc

- Cemex

- Owens Corning

- Skanska

- VINCI

- Bouygues

- ACCIONA

- Kajima Corporation

- DuPont de Nemours, Inc.

- BASF SE

*- List not Exhaustive