Market Overview: High-Output Piezoelectric Materials Driving Automotive, Medical, and MEMS Innovation

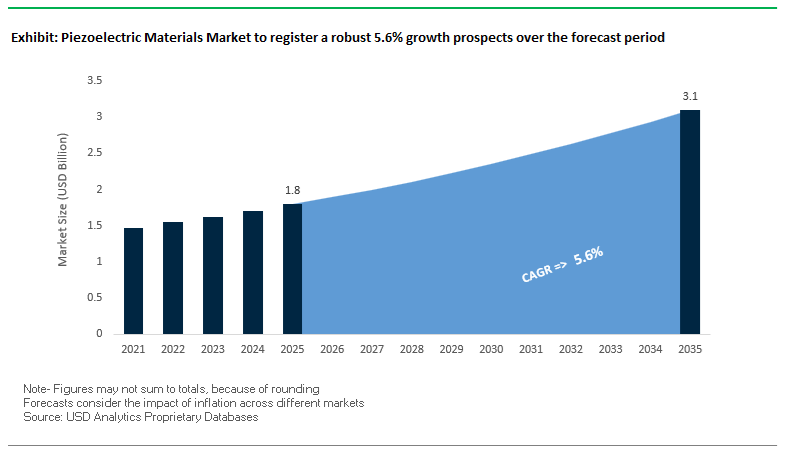

The Piezoelectric Materials Market is projected to expand from USD 1.8 billion in 2025 to USD 3.1 billion by 2035, registering a steady CAGR of 5.6% during 2025–2035. This growth is primarily driven by the rising deployment of MEMS actuators, high-precision medical ultrasound systems, automotive combustion monitoring sensors, and energy-harvesting wearables. Manufacturers and vendors are increasingly focused on material performance metrics such as piezoelectric coefficient, temperature stability, electromechanical coupling efficiency, and lead-free compliance, which define competitive differentiation in the global market.

From a technical standpoint, Lead Zirconate Titanate (PZT) remains the dominant material, delivering a d31 coefficient of 60–223 pC/N, which is 10–30× superior to commonly explored lead-free alternatives such as Aluminum Nitride (AlN). This performance advantage makes PZT indispensable for high-output MEMS actuators, ultrasonic transducers, and automotive precision sensors. Meanwhile, emerging markets such as Focused Ultrasound Surgery (FUS) rely heavily on piezoelectric transducers capable of delivering 80–90% clinical success rates through highly localized acoustic fields. Additionally, the shift toward self-powered wearables and IoT devices underscores the importance of materials capable of harvesting approximately 1 mW of energy from human motion, enabling continuous low-power sensing.

Key insights for manufacturers and technology vendors

- PZT dominance continues: PZT thin films outperform all lead-free alternatives, maintaining their position as the preferred solution for high-output piezo actuators and high-sensitivity sensors.

- Automotive temperature requirements intensify: Combustion and exhaust sensors increasingly require piezoelectric materials stable up to 1,000°C, demanding advanced ceramics or charge-mode sensing architectures.

- Strong medical sector pull: FUS therapies supported by precision piezoelectric transducers achieve 80–90% success rates, accelerating hospital adoption globally.

- Wearable energy harvesting expands: Piezoelectric films providing ~1 mW of harvested power are enabling battery-less structural health monitoring and IoT devices.

- Lead-free research gaining traction: Sustained investment in KNN-based materials aims to close the performance gap with PZT for regulatory-driven markets (EU, Japan).

Market Analysis: Product Innovation, High-Value Collaborations & R&D Momentum Shaping the Industry

The global Piezoelectric Materials Market is entering a phase characterized by technology convergence, investment in next-generation ceramics, and diversification into medical, automotive, and communications electronics. A notable development occurred in September 2024, when Spectris plc, through its HBK division, acquired Piezocryst Advanced Sensorics GmbH for €133.5 million. This acquisition immediately strengthened HBK’s portfolio of high-precision, high-temperature piezo sensors, critical for combustion engines, turbines, and industrial test systems. It also reflects broader industry movement toward integrated sensing platforms with enhanced survivability under extreme thermal conditions.

Several product-focused innovations followed. In November 2025, TDK Corporation introduced new TMR sensors and high-output power modules (up to 1000 W), signaling an increasing reliance on advanced piezoelectric components for power management, tactile feedback, and precision positioning—especially in gaming, robotics, and automotive electronics. Earlier, in October 2025, TDK announced a strategic agreement with Nippon Chemical Industrial to explore joint development of specialty electronic materials, including next-generation piezo ceramics. Such partnerships signal an industry shift toward materials-driven performance differentiation, especially in lead-free and high-frequency applications.

On the timing and communications front, Murata Manufacturing’s April 2025 launch of the XRGE_M_F timing series highlighted the accelerating use of piezoelectric resonators in ADAS, high-speed networking, and precision timing circuits. These devices are essential as automotive OEMs and telecom infrastructure providers migrate toward ultra-low-latency, high-frequency platforms. Parallel to industrial developments, academic institutions have continued to advance piezo technology. In August 2025, research teams reported progress in stabilizing KNN (potassium sodium niobate) for commercial lead-free alternatives to PZT. Meanwhile, January 2025 academic reviews identified PZT thin films of 100 nm to 10 μm thickness as increasingly dominant in MEMS actuators and ultrasonic transducers, reinforcing demand for nanoscale piezo material deposition.

Healthcare and biomechanical sensing applications also expanded. In Q4 2024, a Spanish clinic adopted Kistler Group’s piezoelectric force plates for diagnostic and rehabilitation workflows, confirming the rapid adoption of piezo sensing solutions in clinical biomechanics. The automotive sector continues to be a strong pull factor as well. During Q3 2024, major automakers renewed investment in piezo-controlled fuel injectors to meet tightening emissions regulations, anchored by the unmatched speed and precision of piezo actuators.

Next-Generation Transducer, RF, Polymer, and Energy Harvesting Innovations Defining Market Direction

Market Trend 1: Rapid Transition Toward High-Coupling Relaxor-PT Single Crystals for Advanced Medical Ultrasound Imaging

One of the most influential technological transitions underway in the piezoelectric materials market is the accelerated adoption of Relaxor-PT single crystals—notably PMN-PT and PIN-PMN-PT—for high-performance medical ultrasound transducers. These advanced single-crystal materials deliver a k33 electromechanical coupling coefficient above 90% (typically 92%–94%), significantly outperforming conventional PZT ceramics that operate in the 68%–75% range. This superior electromechanical efficiency translates directly into better energy conversion, reduced signal loss, and tighter control over acoustic output.

The impact extends further into strain performance. Relaxor-PT crystals achieve an exceptionally high piezoelectric strain coefficient (d33) of 1,500–2,500 pC/N, reaching performance levels 4–8× higher than the 300–600 pC/N range typical for premium PZT. This high d33 supports increased sensitivity and improved signal-to-noise ratios, enabling clearer visualization of microstructures and subtle anatomical variations.

The high k33 of these crystals allows ultrasound probes to achieve fractional acoustic bandwidths exceeding 100%, a critical improvement for achieving high axial resolution in advanced diagnostic imaging modalities such as cardiac, vascular, and high-frequency musculoskeletal scanning. Their favorable 25 MRayl acoustic impedance, compared to 30 MRayl for hard PZT, also improves coupling with soft tissue, reducing reflection losses at the interface. These combined benefits position Relaxor-PT crystals as the cornerstone material for next-generation probes, miniaturized imaging platforms, and high-definition point-of-care ultrasound systems.

Market Trend 2: Scaling of AlN and Sc-AlN Piezoelectric Thin Films for 5G/6G RF Filters and High-Frequency IoT Devices

A second major trend is the widespread integration of AlN and scandium-doped AlN (Sc-AlN) thin films into high-frequency RF filters, bulk acoustic wave (BAW) devices, and Surface Acoustic Wave (SAW) platforms powering 5G, 6G, and IoT ecosystems. Sc-doped films exhibit a dramatic improvement in piezoelectric performance; with 40% Sc doping, Sc-AlN achieves 300%–500% higher e31,f piezoelectric coefficients compared to pure AlN, enabling far higher energy efficiency in RF signal processing.

This enhancement directly raises the electromechanical coupling coefficient (kt2), enabling Sc-AlN filters to reach 10%–12% kt2, compared to ~6%–7% kt2 for undoped AlN. Higher coupling increases bandwidth capability—critical for crowded mid-band and high-band 5G frequencies.

AlN’s inherently high acoustic velocity of 5,800 m/s makes it ideal for 2–6 GHz operation, allowing RF components to scale with next-generation wireless technologies. The improved efficiency of Sc-AlN also enables RF filters to maintain low insertion loss (1–1.5 dB), which translates into measurable improvements in network performance, battery life in mobile devices, and thermal stability in dense electronic environments. As 5G deployments surge and 6G development accelerates, these thin-film piezoelectric materials have become foundational to high-frequency electronic architecture.

Market Opportunity 1: High-Strain, Low-Voltage Piezoelectric Polymers for Soft Robotics, Prosthetics, and Haptic Interfaces

A high-value growth opportunity is emerging in piezoelectric polymers, especially advanced formulations of PVDF and P(VDF-TrFE), which offer a compelling combination of high flexibility, large strain, and low-voltage activation. Electroactive PVDF-based polymers can deliver longitudinal strain exceeding 6%, far surpassing the <0.2% strain characteristic of brittle bulk PZT ceramics. This makes them ideal for soft robotics actuators, wearable haptic devices, and human-machine interface skins requiring large deformation and compliance.

Innovative nanocomposite formulations are demonstrating 7.2% maximum strain at just 15 V/μm, satisfying the demand for low-voltage, human-safe, and battery-efficient actuation. Although their d33 coefficient (30–35 pC/N) is significantly lower than ceramic alternatives, it is sufficiently high to enable meaningful tactile feedback in wearable haptics and flexible electronics.

With elastic modulus values between 1–3 GPa, PVDF-based materials offer excellent conformability relative to hard PZT’s 60–80 GPa. This flexibility enables complex geometry embedding, stretchable sensing surfaces, and seamless integration into textiles, prosthetics, and biomimetic robotic structures. As the soft robotics and haptics industry advances toward ultra-lightweight, compliant systems, piezoelectric polymers represent one of the highest-growth material segments.

Market Opportunity 2: Piezoelectric Energy Harvesters Enabling Self-Powered Industrial IoT Devices

The rise of Industry 4.0 is creating a transformative opportunity for piezoelectric energy harvesting systems, which enable long-life, self-powered IoT sensors in factories, grids, and remote industrial environments. PZT-based cantilever harvesters optimized for low-frequency machinery vibrations deliver 100–500 μW/cm³ when exposed to 0.5–1.0 g acceleration at 50–100 Hz, aligning precisely with the vibration signatures of motors, pumps, and rotating equipment.

A critical requirement is frequency matching. Even a 10% mismatch between the harvester’s resonance frequency and the ambient vibration peak can reduce power output by over 90%, highlighting the necessity for precision-tuned materials and mechanical design.

Industrial durability is another catalyst for adoption. Macro Fiber Composite (MFC) harvesters can withstand 10 million cycles at 1,000 V peak-to-peak with negligible degradation, demonstrating the long-term fatigue resistance required for continuous industrial use. Typical PZT stacks or MFC elements can produce 15–20 V peak open-circuit output, sufficient to charge capacitors powering low-energy wireless transmitters.

As industries prioritize predictive maintenance, wireless condition monitoring, and maintenance-free sensor nodes, piezoelectric energy harvesters offer a clear pathway to eliminating cables and batteries while enabling fully autonomous IoT networks.

Piezoelectric Materials Market Share Analysis

Market Share by Material Type: Piezoceramics Dominate Owing to Highest Electromechanical Efficiency

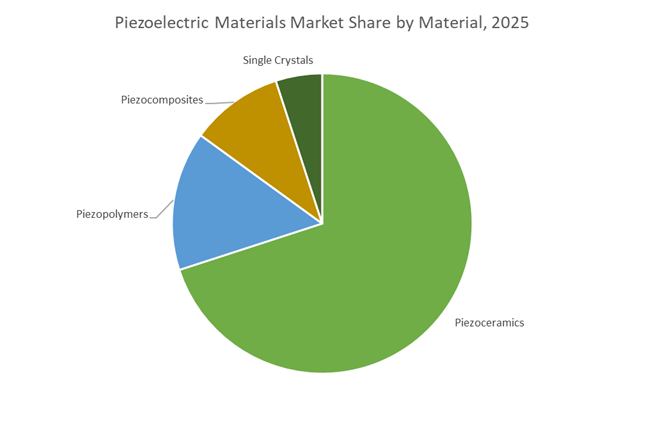

Piezoceramics, led by Lead Zirconate Titanate (PZT), hold the dominant market share of approximately 70% because they deliver the strongest piezoelectric response and the highest electromechanical coupling efficiency among all piezoelectric materials. Their superior ability to convert mechanical stress into electrical charge—and vice versa—makes them indispensable for high-precision applications in sensors, actuators, ultrasonic transducers, and advanced industrial automation systems. Beyond their intrinsic performance, piezoceramics benefit from decades of technological maturity, standardized processing, and high-volume manufacturability, which significantly lowers cost per unit and supports large-scale adoption across industries requiring reliable, temperature-stable, and frequency-stable materials. PZT specifically remains the global benchmark due to its tunability through compositional engineering, enabling manufacturers to optimize Curie temperatures, dielectric properties, and coercive fields for highly specific use cases. The extensive commercial infrastructure supporting PZT—from powder synthesis to multilayer device fabrication—further reinforces its market dominance, resulting in piezoceramics capturing the highest revenue share within the piezoelectric materials industry and remaining the preferred material system for both legacy and next-generation electromechanical devices.

Market Share by End-Use Industry: Industrial Manufacturing Leads Through Precision Automation and High-Reliability Sensing

Industrial Manufacturing represents the largest end-use segment, accounting for approximately 30% of the global piezoelectric materials market, driven by the sector’s escalating need for high-speed, high-accuracy, and high-reliability motion control and sensing technologies. As factories worldwide transition toward Industry 4.0, piezoelectric materials—especially piezoceramics—have become foundational components for automation equipment, enabling nanometer-scale positioning, rapid actuation, and precise vibration monitoring in robotics, semiconductor fabrication, CNC machinery, additive manufacturing, and smart industrial systems. Ultrasonic NDT (Non-Destructive Testing), one of the largest industrial applications of piezoelectric transducers, also fuels demand by providing essential structural integrity assessment in oil & gas, aerospace, metal fabrication, and infrastructure maintenance. Additionally, piezoelectric sensors used for dynamic pressure, strain, and flow monitoring are critical for predictive maintenance and real-time process optimization—two central pillars of advanced digital manufacturing. With global industrial automation investments accelerating and semiconductor manufacturing expanding, the industrial manufacturing sector continues to generate the highest volume and value consumption of piezoelectric materials, firmly establishing its leadership in market share.

Country Analysis: Global Leadership Dynamics Defining the Piezoelectric Materials Market

China: Regulatory-Driven Shift Toward Lead-Free Piezoelectric Ceramics and Large-Scale Industrialization

China has emerged as a central force reshaping the global Piezoelectric Materials Market due to its aggressive policy push toward lead-free piezoelectric materials, specifically Potassium Sodium Niobate (KNN) and Barium Titanate (BTO) systems. Driven by tightening environmental regulations and national goals for “green electronics,” China is accelerating the transition away from Lead Zirconate Titanate (PZT), traditionally the predominant piezoceramic. This shift is supported by major investments into new sintering techniques, grain orientation engineering, dopant optimization, and advanced material formulations that enhance the piezoelectric coefficients and mechanical durability of KNN and BTO ceramics. These improvements aim to close the performance gap with PZT, enabling their use in a broader range of applications including industrial sensors, high-cycle actuators, and consumer electronics.

China’s industrial ecosystem—spanning ceramics companies, research universities, and semiconductor fabs—has become a high-volume production hub for next-generation piezoceramics. Corporate players like Sinoceramics continue to patent low-cost, high-yield crystal growth methods for advanced piezoelectric materials, positioning China as a leader in mass manufacturing and rapid commercialization across Asia-Pacific. With its growing influence in MEMS components, IoT sensors, and robotic actuation, China’s regulatory-led transformation is reshaping global supply dynamics in the piezoelectric materials landscape.

United States: Global Stronghold in PMN-PT Single Crystals and High-Performance Piezoelectric MEMS

The United States maintains a commanding position in the Piezoelectric Materials Market through its leadership in PMN-PT (Lead Magnesium Niobate–Lead Titanate) single-crystal technology—considered one of the highest-performance piezoelectric materials available. U.S. firms such as TRS Technologies have expanded production capacity for these crystals, which deliver up to triple the strain levels of conventional PZT, making them indispensable for high-resolution medical ultrasound, naval sonar, autonomous systems, and classified defense sensing applications.

Complementing single-crystal dominance is the U.S. momentum in piezoelectric MEMS. In January 2024, A.M. Fitzgerald & Associates entered a strategic alliance with Sumitomo Precision Products to scale thin-film PZT MEMS manufacturing in North America. This supports the rapid adoption of precision sensors, micro-actuators, RF components, and semiconductor inspection tools. The United States invests heavily in piezoelectric R&D, with over 20% of national smart systems funding directed towards piezoceramics, piezofilms, acoustic devices, and piezoelectric tooling for next-generation aerospace and medical technologies. These combined strengths position the U.S. as the premier market for high-end, high-performance piezoelectric innovation.

Japan: Global Center for High-Power PZT Actuators, MEMS Thin-Films, and Advanced Sensor Miniaturization

Japan is historically and technologically one of the strongest contributors to the global Piezoelectric Materials Market, particularly in high-power PZT ceramics, precision actuators, and thin-film piezoelectric MEMS. Japanese manufacturers lead in developing ultra-high-density PZT materials capable of extreme RMS vibration velocities—critical for ultrasonic motors, industrial automation systems, micro-positioning stages, and high-efficiency power electronics. This specialized expertise underpins Japan’s dominance in industrial robotics, semiconductor lithography components, and precision manufacturing.

In MEMS fabrication, Japan has become the principal adopter of Aerosol Deposition (AD) for creating 10 μm thick PZT layers on silicon wafers, enabling high-performance resonators, energy harvesters, and micro-sensors. Companies such as Murata Manufacturing continue to expand their portfolio of flexible piezoelectric sensors and compact ceramic components tailored for high-volume consumer electronics, wearables, and smart home devices. Japan’s integration of materials science, electronics miniaturization, and advanced manufacturing makes it a cornerstone for piezoelectric innovation worldwide.

Germany/European Union: Horizon Europe Funding Accelerates Energy Harvesting, Sustainable Piezoceramics, and IIoT Integration

Germany and the broader European Union are shaping a sustainability-driven transformation of the Piezoelectric Materials Market, underpinned by coordinated R&D funding through Horizon Europe. Projects like ETERNAL are advancing railway monitoring systems using highly efficient piezoelectric vibration energy harvesters made from textured, multilayer piezoceramics. These initiatives directly support the EU’s mission to embed battery-free, maintenance-free sensing across industrial IoT (IIoT), smart infrastructure, and automated manufacturing systems.

European labs and industry leaders are also focusing on eco-friendly material innovation, exploring next-generation sustainable piezoelectric materials that reduce reliance on lead-based PZT without compromising performance. At the corporate level, companies like CeramTec continue to expand advanced ceramic offerings, demonstrated by the introduction of Sinalit silicon nitride substrates in June 2024 for high-performance automotive and industrial electronics. Europe’s emphasis on circularity, smart infrastructure, and clean technology is positioning the region as a major influence in energy-harvesting piezo solutions and sustainable materials integration.

South Korea: Flexible Piezoelectric Sensors, Thin-Film Integration, and Display-Embedded Piezo Technologies

South Korea is driving next-generation applications in the Piezoelectric Materials Market through rapid innovation in flexible piezoelectric materials, stretchable sensors, and piezo thin-films designed for wearables, digital healthcare, and advanced display systems. Korean research groups and electronics manufacturers are developing wearable ultrasound patches and non-invasive monitoring tools that utilize PMN-PT crystals or composite piezoceramics, enabling real-time biosignal tracking on curved or dynamic skin surfaces.

South Korea is also at the forefront of embedding piezoelectric thin-films into next-gen OLED and microLED display architectures for tactile sensing, haptic feedback, and advanced signal detection. This trend is fueling the demand for high-performance piezopolymers, nanocomposite films, and hybrid piezoelectric materials. As Korean companies scale their investment into advanced display manufacturing and sensor fusion platforms, the country is becoming a global hub for flexible, miniaturized, and multifunctional piezoelectric technologies.

India: Defense-Led Demand for High-Spec Piezoceramics and Rising Localization in Aerospace Components

India’s expanding ambition in aerospace and defense manufacturing is driving rapid growth in the domestic Piezoelectric Materials Market. Government programs focused on defense localization—supported by new procurement rules, offset mandates, and indigenous development incentives—are creating a sustained requirement for high-specification piezoceramic components. These materials are essential for sonar systems, missile guidance, vibration actuators, telemetry sensors, and precision aerospace components.

As India advances its strategy to reduce import dependency in high-performance materials and build domestic capability in avionics, space systems, and autonomous platforms, piezoceramics are emerging as a crucial input. The growing collaboration between defense R&D labs, private sector manufacturers, and academic institutions is accelerating India’s capacity to prototype and eventually mass-produce specialized piezoelectric components. This government-supported ecosystem is positioning India as an emerging demand hotspot within the global piezoelectric materials landscape.

Competitive Landscape: Global Leaders Advancing High-Precision Piezo Ceramics and MEMS Integration

The competitive landscape in the Piezoelectric Materials Industry is shaped by companies with deep domain expertise in ceramic engineering, multilayer fabrication technologies, high-frequency device design, and MEMS integration. Market leadership is increasingly tied to the ability to supply automotive-grade, medical-grade, and communications-grade piezoelectric components, while maintaining strong R&D pipelines in lead-free materials and ultra-high-temperature solutions.

Murata Manufacturing strengthens its leadership in mobility and communication electronics

Murata Manufacturing is a dominant global supplier of piezoelectric sounders, buzzers, film sensors (Picoleaf™), ceramic resonators, and ultrasonic sensors, with strong integration across automotive and telecommunications markets. In FY2025, Mobility accounted for 26% and Communication for 38.7% of corporate revenues, reflecting strategic alignment with high-volume sectors requiring advanced piezo materials. Murata invests heavily in innovation, allocating ¥140 billion (≈USD 1.3 billion) to R&D in FY2024, prioritizing the evolution of advanced ceramic passive components, precision resonators, and miniaturized sensors. Its extensive experience in multilayer ceramic processing ensures scalability and consistency for MEMS and high-frequency devices, solidifying Murata’s role as a market anchor.

TDK Corporation accelerates piezo integration for DX and EX applications

TDK Corporation is a global leader in PZT materials, PiezoListen™ speakers, piezo actuators, and MEMS-based time-of-flight sensors. The company’s strategy aligns with two megatrends—Digital Transformation (DX) and Energy Transformation (EX)—as TDK supports automotive efficiency, 5G networks, robotics, and smart devices with next-generation piezo components. Its proprietary Copper Multilayer Technology provides a major cost advantage by replacing AgPd electrodes with copper during mass production, enabling high-performance piezo devices at lower manufacturing costs. TDK’s active R&D in next-generation piezoceramics and material manufacturing reinforces its position across ICT, automotive, and industrial automation markets.

PI Ceramic (Physik Instrumente) leads in ultra-precision piezo actuator technologies

PI Ceramic specializes in piezo discs, plates, bowls, and high-precision piezo actuators, supporting nanometer-scale motion control solutions. Its piezoceramic stack actuators are widely used in semiconductor lithography, microscopy, precision optics alignment, and medical ultrasound, where ultra-high resolution is essential. The company’s engineering capabilities enable sub-nanometer motion accuracy, positioning PI Ceramic as a preferred supplier for scientific research institutions and semiconductor fabs. Their technology also contributes to improved outcomes in Minimally Invasive Surgery (MIS) through advanced transducer performance.

Kistler Group advances high-temperature piezo sensors for automotive and biomechanics

Kistler Group is a global leader in piezoelectric quartz-based sensors, offering high-precision pressure, force, and acceleration measurement solutions. These sensors are essential for engine development, vehicle safety testing, biomechanics research, and industrial vibration diagnostics. Kistler’s technology is used extensively in aerospace centers and medical clinics, including its adoption by a Spanish facility in Q4 2024 for advanced diagnostics. Its ability to deliver sensors with extreme stability and responsiveness under dynamic loading makes Kistler a key supplier in mission-critical applications.

CeramTec GmbH focuses on engineered PZT formulations for high-power industrial and medical ultrasound

CeramTec is a specialist in piezoceramic components, tubes, rings, and functional ceramics engineered for industrial and medical ultrasound systems. The company’s custom PZT formulations deliver high electromechanical coupling, thermal stability, and long-term reliability, making them essential for ultrasound imaging probes, therapeutic ultrasound, and high-power nondestructive testing (NDT). CeramTec’s strong emphasis on material science and precision manufacturing supports high-performance transducers across medical, energy, and industrial applications.

Piezoelectric Materials Market Report Scope

Piezoelectric Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.8 Billion

|

|

Market Size (2035)

|

$3.1 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Material Type (Piezoceramics, Single Crystals, Piezopolymers, Piezocomposites), By Product Form (Bulk Ceramics, Thin/Thick Films, Flexible Sheets & Films), By Application Function (Sensors, Actuators, Transducers, Energy Harvesting Devices), By End-Use Industry (Automotive, Healthcare & Medical Devices, Industrial Manufacturing, Consumer Electronics, Aerospace & Defense)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kyocera, TDK, Murata, CeramTec, CTS Corporation, Physik Instrumente (PI), Morgan Advanced Materials, Noliac (Parker Hannifin), APC International, Kistler Group, Piezosystem Jena, TRS Technologies, Mide Technology, Johnson Matthey, Sumitomo Precision Products

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Piezoelectric Materials Market Segmentation

By Material Type

- Piezoceramics

- Single Crystals

- Piezopolymers

- Piezocomposites

By Product Form

- Bulk Ceramics

- Thin / Thick Films

- Flexible Sheets & Films

By Application Function

- Sensors

- Actuators

- Transducers

- Energy Harvesting Devices

By End-Use Industry

- Automotive

- Healthcare & Medical Devices

- Industrial Manufacturing

- Consumer Electronics

- Aerospace & Defense

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Piezoelectric Materials Market

- KYOCERA

- TDK

- Murata

- CeramTec

- CTS Corporation

- Physik Instrumente (PI)

- Morgan Advanced Materials

- Noliac (Parker Hannifin)

- APC International

- Kistler Group

- Piezosystem Jena

- TRS Technologies

- Mide Technology

- Johnson Matthey

- Sumitomo Precision Products.

*- List not Exhaustive

Research Coverage

The latest Piezoelectric Materials Market study from USDAnalytics delivers a deep, data-driven viewpoint on how high-output piezoceramics, single crystals, polymers, and piezocomposites are reshaping next-generation sensing, actuation, ultrasound imaging, RF filtering, and energy harvesting ecosystems. Covering the full value chain from powders and bulk ceramics to thin/thick films and flexible sheets, this report investigates, breakthroughs, analysis reviews, highlights, this report is an essential resource for etc…… the strategic implications of PZT dominance, emerging PMN-PT and Sc-AlN platforms, lead-free roadmap developments, and the rapid adoption of piezo solutions in automotive, medical devices, industrial automation, consumer electronics, and aerospace & defense. It examines how OEM design choices, regulatory pressure on lead content, and Industry 4.0 deployments are redefining material specifications around d-coefficients, coupling factors, temperature limits, fatigue life, and integration with MEMS and IIoT architectures. In addition, the study benchmarks competitive positioning across key global vendors, mapping their product portfolios, technology partnerships, patent activity, and vertical focus areas to help stakeholders quantify addressable opportunities, assess supply resilience, and prioritize R&D and capex decisions in a fast-evolving piezoelectric materials landscape.

Scope Highlights

- Segmentation: Comprehensive coverage by material family (Piezoceramics, Single Crystals, Piezopolymers, Piezocomposites), product form (Bulk Ceramics, Thin / Thick Films, Flexible Sheets & Films), core function (Sensors, Actuators, Transducers, Energy Harvesting Devices), and end-use industry (Automotive, Healthcare & Medical Devices, Industrial Manufacturing, Consumer Electronics, Aerospace & Defense).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, with region-specific demand patterns, regulatory environments, and investment priorities.

- Timeframe: Includes rigorously back-tested historic data from 2021 to 2025 and forward-looking market forecasts for 2026 to 2034, with value/volume outlooks and CAGR benchmarks.

- Companies: Detailed analysis and profiles of 15+ leading and emerging players, including strategy assessment, product positioning, technology focus, and key recent developments across the piezoelectric materials ecosystem.