Advanced Glass Market Overview: High-Performance Glazing, Semiconductor Precision & Smart-Device Integration Driving Global Growth

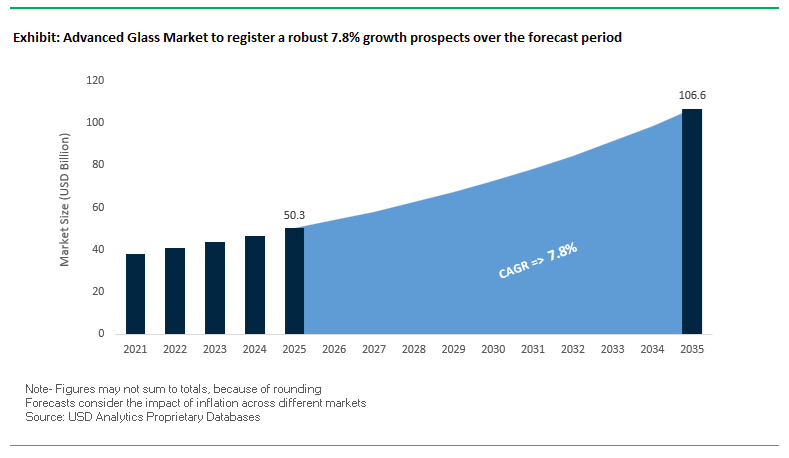

The Global Advanced Glass Industry, valued at USD 50.3 billion in 2025 and projected to reach USD 106.6 billion by 2035 at a strong 7.8% CAGR, is entering a decade defined by performance-centric innovation, semiconductor-grade purity requirements, and the rapid integration of electronics and sensing technologies into architectural, automotive, and consumer applications. As industries shift toward ultra-efficient, durable, and high-precision materials, advanced glass has become foundational to energy-efficient buildings, high-reliability semiconductors, ruggedized consumer electronics, ADAS-enabled automotive platforms, and sterile pharmaceutical packaging.

Demand is accelerating as buyers prioritize glass solutions offering thermal insulation, mechanical impact resistance, optical clarity, chemical durability, and compatibility with smart-device and sensor ecosystems. This includes the global pivot toward Low-E architectural glass capable of reducing heat loss by up to 75%, next-generation chemically strengthened cover glass achieving compressive stress levels above 850 MPa, ADAS-compliant automotive windshields engineered to maintain optical distortion below 0.05%, borosilicate pharmaceutical vials releasing less than 0.1 mg Na₂O per gram, and semiconductor display substrates achieving <5 μm TTV for ultra-high-resolution panels.

Key Insights for Advanced Glass Market Stakeholders

- EU EPBD driving Low-E adoption: High-performance Low-E coatings reduce heat loss by up to 75%, becoming essential for net-zero building compliance.

- Electronics-grade strength: Chemically strengthened cover glass now exceeds 850 MPa compressive stress, supporting premium smartphone and wearable durability.

- ADAS optical precision: Windshields require <0.05% optical distortion to ensure accurate LiDAR and camera sensor readings for autonomous driving features.

- Pharma packaging purity: Type I borosilicate tubing must yield <0.1 mg Na₂O/g extractables to maintain biologic and injectable drug integrity.

- Ultra-flat display glass: Large-format TFT/OLED glass now achieves <5 μm TTV, a necessity for high-resolution, defect-free electronic displays.

Market Analysis: Strategic Expansions, Semiconductor Alignment & Renewable Energy Glass Momentum

The Advanced Glass Industry witnessed major strategic investments and technology deployments across 2025, significantly reshaping global supply capacity, semiconductor readiness, and architectural performance standards. In November 2025, Nippon Sheet Glass (NSG) Group announced a major investment in a new high-value coating line in Poland to serve booming European demand for energy-efficient architectural glass. This expansion supports the surging need generated by EPBD-driven retrofits and new-build projects. In October 2025, Corning received reaffirmed multi-billion-dollar commitments from Apple-including a recent $2.5 billion agreement to produce all cover glass for iPhones and Apple Watches in the U.S. This solidifies Corning’s leadership in durable specialty glass and deepens the reshoring of the electronics glass supply chain. That same month, Corning reported 14% YoY Core Sales and 24% YoY Core EPS growth, largely fueled by specialty materials serving optical communications and emerging Gen AI technologies.

Semiconductor material innovation accelerated in September 2025, when SCHOTT AG introduced ultra-flat, chemically robust glass solutions for 3D IC and WLP packaging, addressing yield and reliability challenges in advanced semiconductor nodes. Renewable energy manufacturing also advanced: in July 2025, NSG converted its Rossford, Ohio facility into a high-durability solar glass production line using proprietary online coating technologies optimized for photovoltaic performance. M&A activity followed in June 2025, with SCHOTT acquiring a U.S.-based specialty glass startup to expand its automotive, electronics, and industrial materials portfolio-reflecting the rising importance of technical differentiation in advanced glass manufacturing.

The sector also saw sustainability- and performance-driven product launches. In May 2025, NSG introduced next-generation architectural glass optimized for high solar-control efficiency across urban commercial markets. In March 2025, Guardian Glass committed $20 million to R&D focused on smart, energy-efficient advanced glass solutions, with particular emphasis on thermal insulation and solar control to meet green-building codes. These developments collectively confirm the industry’s rising reliance on high-performance coatings, ultra-flat substrates, optical precision, and renewable-energy-compatible materials.

Key Trends Transforming the Advanced Glass Market

Trend 1: Ultra-Thin, High-Strength Glass Becomes the Core Structural Material for Folding and Wearable Electronics

Rapid innovation in consumer electronics—specifically foldable smartphones, rollable displays, AR/VR devices, and next-generation wearables—is driving the industrialization of ultra-thin glass (UTG) engineered to balance mechanical flexibility with optical clarity and surface hardness. Chemically strengthened UTG with a thickness range of 30–100 µm can now achieve bend radii as low as 1–3 mm, making it viable for cover windows in foldable smartphones where mechanical reliability must be maintained during thousands of daily opening-closing cycles.

Its commercial relevance has accelerated as manufacturers qualify UTG for repeated folding durability of ~200,000 cycles, while maintaining edge strengths exceeding 200 MPa in 2-point bending tests. These mechanical properties directly influence consumer device warranties, hinge design, and the longevity of flexible OLED panels. Equally important is UTG’s compatibility with Roll-to-Roll (R2R) post-processing, enabled by thicknesses below 100 µm. R2R compatibility significantly reduces production costs and enhances throughput for flexible electronics, solar cells, and electronic paper displays. As foldable and wearable electronics transition from premium niches into mainstream mass production, ultra-thin glass is becoming a foundational material for device OEMs pursuing thinness, ruggedness, and next-generation form factors.

Trend 2: Architectural Glass Advances from Passive Barrier to Active Energy-Management System

Architecture and commercial construction are rapidly adopting advanced glazing systems that transform glass from a passive enclosure material into an active, programmable component for energy management. Electrochromic (EC) “smart glass” technologies now enable buildings to dynamically modulate solar heat gain, light transmission, and thermal load in response to external conditions. EC glass can reduce Solar Heat Gain Coefficient (SHGC) by up to 91%, drastically reducing the heat load on HVAC systems during peak sunlight hours.

Simulation studies show that buildings equipped with EC glazing achieve 5–15% reductions in total energy load and up to 26% reductions in peak electricity demand, directly supporting corporate decarbonization goals and net-zero building mandates. The integration of smart sensors and automated control architectures enhances daylight harvesting while limiting glare, enabling energy savings of up to 39.5% compared to static glazing. As global building codes tighten and smart infrastructure strategies expand, advanced architectural glass is evolving into a critical enabler of sustainable building ecosystems, with strong regulatory and economic momentum supporting adoption.

High-Value Opportunities Emerging in the Advanced Glass Market

Opportunity 1: High-Durability Glass Encapsulation for Perovskite and Tandem Solar Cell Commercialization

One of the fastest-growing opportunities in the advanced glass market lies in providing highly hermetic, durable encapsulation solutions for perovskite and silicon-perovskite tandem solar cells. These next-generation photovoltaic (PV) technologies are extremely sensitive to moisture and oxygen, making ultra-durable glass essential for commercial deployment. Unlike polymer films, glass-glass encapsulation offers the barrier integrity required to pass the IEC 61215 damp heat test (1000 h at 85°C and 85% RH), with some encapsulated perovskite devices retaining over 95% of their initial efficiency—a crucial milestone for industrial qualification.

Glass’s inherently low water vapor transmission rate (WVTR) and oxygen transmission rate (OTR) are essential, as unprotected perovskites can degrade within hours when exposed to humidity above 50% RH. Moreover, because many perovskite and organic transport layers degrade at temperatures above 120–150°C, new encapsulation processes are being developed that enable ambient or low-temperature sealing using adhesive-based techniques combined with cover glass. As perovskite and tandem solar technologies scale toward gigawatt-level manufacturing, glass suppliers capable of delivering hermeticity, optical neutrality, chemical compatibility, and low-temperature processability will capture significant market share.

Opportunity 2: Glass-Ceramics and Specialty Glass for Semiconductor Packaging, Chiplets, and Advanced Carriers

Semiconductor miniaturization, heterogeneous integration, and advanced packaging architectures such as 2.5D/3D integration and chiplet-based designs are generating strong demand for glass-based interposers, carrier wafers, and glass-ceramic substrates. Glass structures featuring Through-Glass Vias (TGVs) are demonstrating substantial signal-integrity advantages—offering 1–2 dB lower insertion loss at 10 GHz and maintaining stable eye diagrams even at 70 Gb/s, outperforming silicon interposers in high-frequency, high-bandwidth data transfer.

A key materials advantage lies in specialty glass compositions that can be engineered to match the Coefficient of Thermal Expansion (CTE) of semiconductor dies, mitigating warpage, micro-bump fatigue, and thermal cycling stress during assembly. Additionally, unlike silicon substrates, glass supports large panel-size processing, creating an economically attractive pathway for scaling interposer manufacturing and reducing packaging costs for high-volume chiplet architectures.

As semiconductor devices demand better RF performance, improved thermal management, and larger-format heterogeneous integration, glass-ceramics and engineered glass substrates will become increasingly indispensable in the global semiconductor packaging ecosystem.

Advanced Glass Market Share Analysis

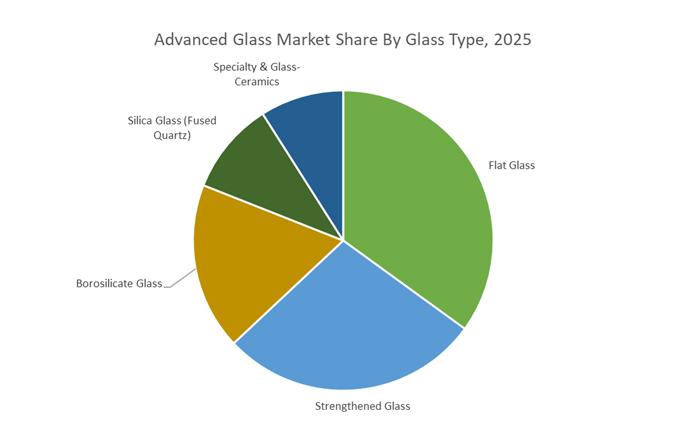

Market Share by Glass Type/Composition: Flat Glass Leads with 35.1% Share

Flat Glass dominates the Advanced Glass Market with a 35.1% share in 2025, reflecting its foundational role across construction, automotive, solar, and architectural applications. Its leadership stems from the enormous scale of global infrastructure and building development, where flat glass is indispensable for façades, windows, glazing systems, and structural elements. Although traditionally considered a volume-driven commodity, the segment’s value is increasingly enhanced through low-E coatings, multilayer laminations, solar-control films, and safety treatments, transforming flat glass into a multifunctional material aligned with energy efficiency, sustainability, and smart building requirements. The segment’s strong market share is also supported by the rapid expansion of solar photovoltaic installations, where high-transmittance flat glass is a critical component for module efficiency. Meanwhile, the surrounding glass ecosystem underscores the market’s technological bifurcation: aluminosilicate/strengthened glass drives premium value in consumer electronics, foldable devices, and protective covers; borosilicate and fused silica are mission-critical for semiconductors, laboratory equipment, and pharmaceutical packaging, where purity and thermal resistance are essential; and glass-ceramics serve high-end appliance, industrial, and optical applications. Flat glass thus anchors the market’s volume foundation while specialty compositions increasingly shape high-performance, high-margin segments.

Market Share by End-Use Industry: Construction & Architecture Lead with 33.9% Share

Construction & Architecture hold the largest share at 33.9% in 2025, reaffirming the sector’s dependence on advanced glass solutions for structural transparency, safety, insulation, and energy regulation. The dominance of this segment is driven by global urbanization, green building initiatives, and regulatory mandates promoting energy-efficient façades, double- and triple-glazed units, solar-reflective coatings, and smart glass technologies. As buildings become more integrated with sustainability targets, glass innovations such as electrochromic windows, thermal-insulating layers, and self-cleaning surfaces are shifting construction from traditional materials toward high-performance architectural glass systems. Complementing this, the broader end-use landscape showcases strong multi-industry adoption: electronics and displays represent the value engine of the market, powered by the need for ultra-thin, high-strength, optically pure cover glass across smartphones, tablets, laptops, and wearables; automotive & transportation increasingly integrate advanced glass for HUD displays, panoramic roofs, embedded antennas, and solar-harvesting surfaces; pharmaceutical and healthcare sustain stable demand for borosilicate containers and diagnostic optics; and renewable energy applications, especially solar, continue to scale demand for high-transmittance, durable glass substrates.

Country Analysis: Global Advanced Glass Market Innovation Hubs

United States: Scaling High-Tech Cover Glass, Optical Composites, and Domestic Solar Glass Manufacturing

The United States continues to strengthen its position as a global leader in advanced glass materials, driven by major investments from materials science companies and federal clean energy initiatives supporting domestic manufacturing. At the forefront is Corning Incorporated, which launched Corning® Gorilla® Glass Ceramic in March 2025—a breakthrough transparent, strengthenable glass-ceramic engineered to deliver superior drop resistance, especially on rough surfaces. This positions the U.S. at the center of innovation for high-performance cover glass in mobile consumer electronics. Corning’s expanding portfolio, including Gorilla® Glass with DX/DX+, delivers enhanced optical performance, scratch resistance, and durability for next-generation mobile camera systems, reinforcing the nation’s technological dominance in advanced optical composites.

Federal clean energy policies are also catalyzing significant growth in domestic solar glass manufacturing, with Corning announcing a $1.5 billion investment in Michigan to increase U.S. output of high-efficiency solar glass—aligning with “Buy American” requirements and strengthening the country’s renewable energy supply chain resilience. The company is simultaneously reinforcing global R&D leadership with a $300 million expansion at the Sullivan Park research facility in New York, enabling continued breakthroughs in optical physics, display glass, semiconductor glass, and precision material science. Strategic partnerships are also shaping the ecosystem; Apple’s cumulative $250 million investment in Corning underscores long-term collaboration in the development and scaling of specialty glass solutions for premium consumer devices.

China: Global Stronghold in Display Substrates and Strategic Solar Glass Market Stabilization

China is the world’s largest and most influential producer of advanced display glass substrates, supported by extensive state subsidies and industrial policies that favor large domestic manufacturers like BOE. Chinese enterprises now account for 72% of global LCD production and have surpassed 50% of global OLED substrate production, cementing their dominance in television, smartphone, and IT panel supply chains. Analysts estimate that China will command an average of 85% of global display industry capital expenditure (2020–2027), enabling continuous expansion and technological upgrades in TFT-LCD and OLED substrate capacity.

China is also reshaping global solar glass markets through major reforms. In mid-2025, the Ministry of Industry and Information Technology (MIIT) announced measures to curb “disorderly competition” in solar manufacturing, leading 10 top producers—including Xinyi Solar and Flat Glass—to voluntarily cut solar glass output by 30% to stabilize prices. A significant structural shift is underway as China plans to cancel the 13% VAT export rebate on solar modules, which is expected to raise global solar equipment prices by around 9%. This policy aims to steer the industry away from destructive price wars and toward sustainable margin structures. As a result, China remains the dominant global hub for display substrates, solar glass production, and large-scale smart manufacturing infrastructure.

Germany (Europe): Precision Pharma Glass Leadership and Eco-Friendly Architectural Glazing Innovation

Germany and the broader EU maintain a strong global reputation in ultra-precise specialty glass for pharmaceuticals, architecture, and automotive applications. SCHOTT Pharma expanded its European manufacturing footprint by opening a new prefillable glass syringe facility in Lukácsháza, Hungary, in June 2024—supported by €9 million in local government investment. This expansion addresses surging demand for injectable drug delivery systems and strengthens Europe's control over critical healthcare supply chains. At the same time, SCHOTT AG fortified its tubing production capacity by investing €40 million in a second melting tank for FIOLAX® borosilicate tubing at its Mainz plant, ensuring stable supply for high-quality pharmaceutical packaging.

Germany is also fostering collaboration across pharmaceutical glass ecosystems through the Alliance for RTU (Ready-to-Use), formed by SCHOTT Pharma, Gerresheimer, and Stevanato Group to accelerate global adoption of RTU vials and cartridges using advanced tubular glass. Beyond pharma, German manufacturers—including SCHOTT AG and Saint-Gobain—are leading eco-friendly architectural and automotive glazing innovation, investing in recyclable float glass, hybrid-fuel furnace technologies, and vacuum-insulated systems. These investments align directly with the EU’s strict climate and energy-efficiency directives, positioning Germany as a central force in sustainable advanced glass manufacturing and precision specialty glass engineering.

Japan: Advancing High-Precision Optical Glass and Specialized Medical & Industrial Glass Technologies

Japan retains its global edge in high-performance optical glass, lithography materials, and medical-grade functional glass, driven by decades of precision manufacturing expertise. Companies such as Yamamura Photonics are applying advanced glass processing, precision joining, and vacuum sealing technologies to produce high-hermeticity glass-metal assemblies—such as X-ray tubes and vacuum interrupter enclosures—which are essential in medical diagnostics and industrial electrical systems.

Japan is also a frontrunner in advanced optical materials R&D, with firms like Hamamatsu Photonics innovating across quantum technologies, Terahertz-wave systems for future 6G communications, and high-power laser technologies for fusion research. These developments reinforce Japan’s central role in next-generation photonics and semiconductor-related glass engineering. Complementing these innovations, AGC Inc. continues advancing automotive sensor glass with products like Wideye®, an infrared-transparent, high-optical-performance glass specifically engineered for LiDAR and autonomous driving sensors. Japan’s capabilities in miniaturization, accuracy, and materials stability position it as a global hub for optical-grade and medical-grade advanced glass technologies.

South Korea: Expanding Flexible Display Glass Technologies and Automotive Digital Glass Systems

South Korea is a global leader in flexible displays, OLED substrates, and ultra-thin strengthened glass, benefiting from the country’s dominance in consumer electronics and emerging EV technologies. Samsung Corning Advanced Glass (SCG) is at the forefront with Corning Lotus™ NXT Glass, which offers exceptional thermal and dimensional stability under ≥500°C processing—making it one of the most advanced OLED substrates available for premium smartphones, tablets, and IT displays.

The country is also aggressively innovating in foldable and rollable display glass, focusing on hybrid ultra-thin glass and composite structures capable of surviving thousands of bend cycles while preserving clarity and touch sensitivity. These innovations are essential for the next wave of flexible consumer electronics. In the automotive sector, South Korea is experiencing rising demand for high-strength in-car display cover glass and integrated glass antenna systems, including 5G Sub-6 band-compatible solutions. As vehicles evolve into digital cockpits, Korean manufacturers are scaling their production of display-grade glass and smart automotive glazing, reinforcing South Korea’s position as a dynamic hub for advanced flexible and automotive glass technologies.

Competitive Landscape: Global Leaders in Specialty Glass, Coated Architectural Products & Advanced Display Technologies

The competitive landscape of the Global Advanced Glass Industry is characterized by companies that excel in coating technology, chemical strengthening, optical precision, semiconductor packaging glass, pharmaceutical-grade tubing, and ADAS-ready automotive glazing. Market leaders differentiate through vertical integration, proprietary glass-ceramic science, large-scale float glass networks, and strategic partnerships with electronics, automotive, and renewable energy OEMs.

Corning Incorporated - Leading Innovator in Specialty Glass & U.S.-Based Cover Glass Manufacturing

Corning is globally recognized for its leadership in specialty glass and glass-ceramics, including Gorilla® Glass for mobile devices and Valor® Glass for pharmaceutical packaging. Its strategic focus on Gen AI optical infrastructure and mobile consumer electronics is reinforced by Apple’s $2.5 billion commitment to U.S.-based cover glass production. Corning met its 20% Core Operating Margin goal earlier than planned, supported by its advanced materials portfolio, and continues to drive innovation in strengthenable, transparent glass-ceramics for high-demand applications.

SCHOTT AG - High-Reliability Specialty Glass & Semiconductor-Grade Packaging Materials

SCHOTT AG is a world leader in engineered specialty glass, including ZERODUR® for precision optics and DURAN® for scientific applications. Its recent investments target thin-glass wafer solutions for 3D IC packaging, reflecting rising semiconductor complexity and packaging density requirements. SCHOTT also holds deep expertise across more than 120 optical glass types, enabling integration into advanced optics, microelectronics, pharma packaging, and energy technologies.

Saint-Gobain S.A. - Sustainable Low-Carbon Architectural Glass & High-Performance Coatings

Saint-Gobain is a major global producer of flat glass and high-performance building materials, including the COOL-LITE® XTREME Low-E range and DIAMANT® low-iron glass. With a strategic focus on net-zero construction by 2050, the company is investing heavily in low-carbon production technologies such as Pilkington Mirai. Saint-Gobain’s global presence and recycled-cullet integration support its leadership in sustainable architectural glass for green buildings.

Nippon Sheet Glass (NSG) Group - ADAS-Compatible Automotive Glass & Solar Energy Glass Leader

NSG, known for the Pilkington brand, is a global leader in automotive glazing, ADAS-ready laminated windshields, and solar energy glass. Its investments follow the “4 Ds”: Decarbonization, Digitalization, and high-value industrial applications. NSG completed the first-ever carbon capture trial in the European flat glass sector and operates 27 float furnaces, including specialized solar-glass lines that support renewable-energy deployment globally.

AGC Inc. - High-Strength Display Glass & Automotive Functional Materials

AGC is a major supplier of architectural, automotive, and display glass, with significant capabilities in fluorochemicals and specialty materials for consumer electronics. Its investment strategy prioritizes next-generation high-strength glass for EVs and smart devices, meeting the durability and optical performance needs of modern electronics ecosystems. AGC retains strong market influence across APAC and Europe, supported by a diversified advanced materials portfolio.

Fuyao Glass Industry Group - Global Automotive Glass Manufacturer Supporting EV Sensor Integration

Fuyao Glass is a top-tier supplier of laminated, tempered, and advanced encapsulated glass for global automotive OEMs. The company is heavily focused on EV-specific glass requirements, including integrated Head-Up Display (HUD) capability and dynamic tinting technologies. Its extensive global production footprint enables high-volume, cost-competitive delivery of precision automotive windshields and side glass for leading automakers worldwide.

Advanced Glass Market Report Scope

Advanced Glass Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$50.3 Billion

|

|

Market Size (2035)

|

$106.6 Billion

|

|

Market Growth Rate

|

7.8%

|

|

Segments

|

By Glass Type/Composition (Aluminosilicate Glass, Borosilicate Glass, Flat Glass, Silica Glass, Specialty Glass, Glass-Ceramics), By Product Form (Substrates, Cover Glass, Tubing, Fibers, Panels, Molded Parts), By Application Function (Structural Glass, Functional Glass, Active/Smart Glass, Barrier Glass), By End-Use Industry (Electronics, Automotive, Construction & Architecture, Pharmaceutical & Healthcare, Renewable Energy, Aerospace & Defense)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Corning Incorporated, SCHOTT AG, AGC Inc., Saint-Gobain S.A., Nippon Sheet Glass Co. Ltd., Murata Manufacturing Co. Ltd., CoorsTek Inc., Taiwan Glass Industry Corporation, Gerresheimer AG, China Glass Holdings Limited, Hoya Corporation, Nippon Electric Glass Co. Ltd., Carl Zeiss AG, Stevanato Group, Xinyi Solar Holdings Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Advanced Glass Market Segmentation

By Glass Type / Composition

- Aluminosilicate Glass

- Borosilicate Glass

- Flat Glass

- Silica Glass

- Specialty Glass

- Glass-Ceramics

By Product Form

- Substrates

- Cover Glass

- Tubing

- Fibers

- Panels

- Molded Parts

By Application Function

- Structural Glass

- Functional Glass

- Active / Smart Glass

- Barrier Glass

By End-Use Industry

- Electronics

- Automotive

- Construction & Architecture

- Pharmaceutical & Healthcare

- Renewable Energy

- Aerospace & Defense

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Advanced Glass Market

- Corning Incorporated

- SCHOTT AG

- AGC Inc.

- Saint-Gobain S.A

- Nippon Sheet Glass Co., Ltd

- Murata Manufacturing Co., Ltd

- CoorsTek, Inc

- Taiwan Glass Industry Corporation

- Gerresheimer AG

- China Glass Holdings Limited

- Hoya Corporation

- Nippon Electric Glass Co., Ltd

- Carl Zeiss AG

- Stevanato Group

- Xinyi Solar Holdings Limited

*- List not Exhaustive