Market Overview: High-Performance Fibers Power Lightweighting Across Aerospace, Wind and EV Platforms

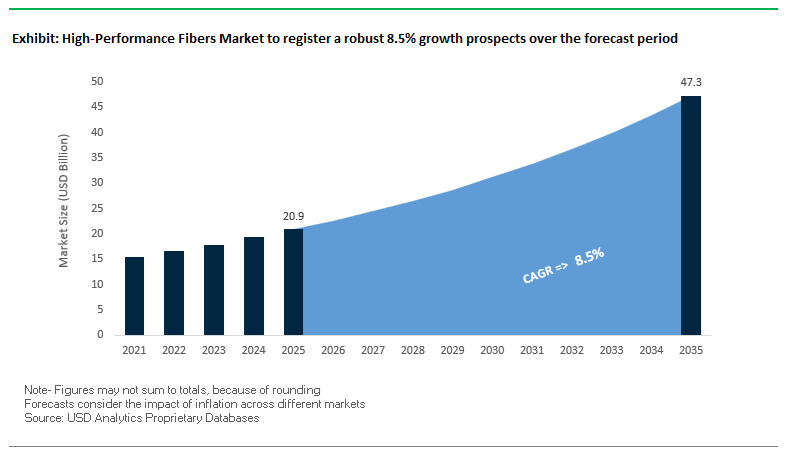

The High-Performance Fibers Market is projected to grow from USD 20.9 billion in 2025 to USD 47.3 billion by 2035, registering a strong CAGR of 8.5% (2025–2035). This expansion is underpinned by accelerating adoption of carbon fiber, aramid fiber, UHMWPE and other advanced fibers in aerospace, defense, renewable energy and electric vehicles (EVs), where strength-to-weight ratio and durability are critical performance metrics. For manufacturers and fiber converters, the market is increasingly shaped by stringent safety standards, decarbonization targets, and OEM lightweighting mandates that favor high-value, engineered fiber systems over commodity materials.

From an operational standpoint, aerospace and defense account for over 35% of global high-performance fiber demand, reflecting intensive use of carbon fiber composites and aramids in primary structures, interiors and advanced protection systems. In wind energy, each modern utility-scale turbine now incorporates around 5 tons of carbon fiber per blade set, making wind blades one of the most fiber-intensive composite applications. In the EV sector, high-performance fibers are central to lightweighting strategies targeting 30–40% component weight reduction, directly enhancing driving range and energy efficiency. However, wider penetration into mass-market automotive and industrial segments is still constrained by fiber production costs, with carbon fiber typically priced at USD 15–25/kg, keeping it concentrated in premium and mission-critical applications.

Key insights for manufacturers and vendors in the high-performance fibers market include:

- Aerospace & defense dominance: >35% share of high-performance fiber demand is tied to long-cycle aerospace and defense programs, supporting stable, backlog-driven volumes.

- Wind blades as volume anchor: ~5 tons of carbon fiber per large turbine blade set position wind energy as a structurally important growth vertical for carbon fiber producers.

- EV lightweighting as a structural growth driver: OEM targets of 30–40% weight reduction in key systems are accelerating the use of carbon fiber and aramid fiber in structures, reinforcement and safety components.

- Cost-performance trade-off remains a barrier: Carbon fiber’s USD 15–25/kg cost bracket restricts adoption in cost-sensitive, high-volume segments, keeping the focus on process optimization, recycling and alternative precursors.

Market Analysis: Portfolio Reshaping, Sustainability and EV Demand Restructure the High Performance Fibers Industry

The global high performance fibers industry is undergoing coordinated transformation across technology, sustainability and portfolio strategy. In Q1 2025, Toray Industries launched a new flame-resistant aramid fiber variant, specifically aimed at enhanced protective gear and industrial safety markets. This innovation supports the continued shift from conventional textiles toward high-performance protective fabrics in oil & gas, industrial, defense and firefighting, deepening Toray’s presence in the technical textile value chain. In October 2025, Teijin further reinforced the strategic importance of high-performance fibers to e-mobility and energy by expanding its carbon fiber production capacity in Europe, directly targeting the fast-growing EV composite manufacturing sector and advanced lightweight structures for transportation.

Sustainability and circularity have become central differentiators. In August 2025, Teijin Aramid announced that its Twaron® production process achieved ISCC PLUS certification, positioning its aramid fibers as a sustainably certified solution for circular material flows, particularly attractive to OEMs and Tier-1s with science-based climate targets. This builds on the May 2024 recycling partnership between Teijin Aramid and Mallinda, which focuses on recovering both Twaron® aramid fiber and resin systems from aerospace composites, enabling higher-value recycling loops and lowering the lifecycle carbon footprint of high-performance fiber-reinforced structures. In September 2024, Teijin Aramid also co-launched the Sustainable Optical Fiber and Cable Industry Alliance (SOFIA), reflecting the expansion of high performance fibers into telecom, optical cable and infrastructure domains under a common sustainability umbrella.

Portfolio rationalization is another defining theme as companies refocus on downstream, higher-margin applications. In August 2025, DuPont announced a definitive agreement to sell its Aramids business for about USD 1.2 billion, aligning the group around high-growth advanced solutions in electronics, water and specialty materials rather than commodity fiber production. This followed an earlier August 2024 divestiture of Divinylbenzene (DVB) production to Deltech Holdings, freeing DuPont to concentrate on downstream engineered materials where Kevlar®, Nomex® and high-performance polymers are integrated into systems-level solutions. In parallel, Teijin Aramid’s leadership transition in Q3 2025, with a new CEO focused on operational streamlining and cost effectiveness in the Netherlands, signals an internal efficiency drive to safeguard the long-term competitiveness of European aramid fiber production in the face of energy costs and global pricing pressures.

Over the forecast period, the high performance fibers market is structurally bullish—anchored by defense and aerospace, accelerated by EV and wind energy, and reshaped by sustainability certification, recycling technologies, and portfolio optimization. Producers that can combine cost discipline, certified low-carbon production and application-specific innovation are best positioned to capture share as the market grows to USD 47.3 billion by 2035.

Breakthrough Trends and Emerging Opportunities Transforming the High-Performance Fibers Market

Market Trend 1: Industrial-Scale Deployment of UHMWPE Fibers for Deep-Sea Offshore Renewable Cables and Dynamic Mooring Systems

The global high-performance fibers market is witnessing rapid industrial scaling of Ultra-High Molecular Weight Polyethylene (UHMWPE) for subsea renewable energy systems and deep-sea mooring lines. UHMWPE delivers an extraordinary specific tensile strength 70–71 times higher than mild steel and remains 3.3 times stronger than pearlitic steel on a weight-normalized basis, enabling major structural efficiency gains in offshore installations. With a density of just 0.97 g/cm³, UHMWPE is one of the only advanced fibers capable of floating, dramatically reducing subsea tension loads and enabling easier handling by installation vessels.

Fatigue resistance is a further differentiator—grades such as Dyneema® SK78 exhibit up to 3× longer fatigue life than standard HMPE fibers, a critical performance metric for dynamic mooring lines subjected to millions of tension cycles across 20-year operational lifetimes. The fiber’s outstanding corrosion resistance in seawater and chemical environments eliminates the degradation risks inherent to metallic systems and even outperforms aramid fibers in long-term immersion scenarios. These combined properties are positioning UHMWPE as a strategic material for next-generation floating wind, wave-energy systems, and deepwater power transmission, where weight reduction, durability, and fatigue performance are mission-critical.

Market Trend 2: Regulatory-Driven Adoption of Para-Aramid Fibers for Thermal Runaway Mitigation in EV Battery Pack Safety Components

The transition to electrified mobility is driving demand for para-aramid fibers and aramid nanofibers (ANF) as essential reinforcement and separator materials in EV battery safety systems. With an initial decomposition temperature near 510°C, ANFs offer thermal resilience far exceeding that of conventional polyolefin separators, which melt at 130–165°C—a temperature gap that helps prevent internal shorts during thermal runaway events. Their negligible thermal shrinkage up to 300°C ensures dimensional stability under extreme heating, eliminating the risk of electrode contact.

Aramid fiber-based papers and felts also deliver a Limiting Oxygen Index (LOI) of 28–30%, evidencing strong intrinsic flame retardancy by requiring higher-than-ambient oxygen levels to support combustion. These materials maintain exceptional mechanical strength—ANF separators exhibit ≈192 MPa tensile strength, allowing them to preserve structural integrity even during rapid temperature excursions. As OEMs intensify compliance with EV safety regulations across the U.S., EU, and Asia, para-aramid systems are becoming central to thermal barriers, module separators, and battery shields engineered to contain or delay the propagation of thermal runaway.

Market Opportunity 1: Advancements in High-Modulus, Radiation-Resistant Fibers for Lightweight Commercial Spacecraft and Satellite Structures

The commercialization of LEO and GEO satellite constellations is driving the need for ultra-lightweight, radiation-tolerant fibers capable of withstanding intense thermal cycles, vacuum exposure, and high-energy particle environments. High-performance polyimide (PI) and oxidized PAN (OPAN) fibers provide high specific modulus values comparable to the strongest aerospace-grade alternatives while enabling substantial mass reduction—an essential benefit for lowering launch costs.

OPAN fibers exhibit continuous-use thermal stability up to 300°C, with tolerance for even higher short-term exposures, making them suitable for spacecraft components undergoing extreme orbital temperature fluctuations. Their LOI of 45–55% renders them among the most inherently flame-resistant fiber systems available, a crucial property for crewed vehicles and high-value electronics modules. Polyimide-based materials further demonstrate exceptional radiation resistance, retaining insulation performance and mechanical durability after prolonged exposure to electron flux, proton bombardment, and UV-rich environments. These properties support major opportunities in deployable space structures, thermal blankets, antenna booms, and radiation-shielding composites.

Market Opportunity 2: Bio-Based and Recyclable High-Performance Fibers for Circular Composite Manufacturing and Sustainable Lightweighting

The shift toward sustainable materials is accelerating innovation in bio-derived and recyclable high-performance fiber systems. Lignin, the third most abundant polymer on Earth with more than 300 billion tons available globally, represents a transformative precursor for low-cost, bio-based carbon fiber. Coupling lignin with PAN in blended precursors enhances mechanical strength and thermal stability, enabling cost-effective composite production with reduced reliance on petroleum-derived polymers.

In thermoplastic composite systems such as short carbon fiber–reinforced PEEK, recyclability is a key competitive advantage. Studies show these materials retain >92% flexural strength and >95% modulus even after multiple recycling cycles, validating the feasibility of long-life circular composite manufacturing. Stability under repeated melt-processing conditions is further enhanced with CNT additions, which limit molecular degradation—evidenced by a modest 2.9× increase in melt volume-flow rate (MVR) after nine cycles, compared with a 5.4× increase seen in conventional glass fiber–reinforced systems.

As OEMs strive to meet sustainability mandates and carbon neutrality targets, recyclable and bio-based fibers represent a high-growth opportunity for automotive lightweighting, industrial composites, consumer electronics housings, and aerospace interior components, where performance cannot be compromised.

High Performance Fibers Market Share Analysis

Market Share by Fiber Type: Carbon Fiber Leads Due to Superior Strength-to-Weight Performance and Critical Use in High-End Structural Applications

Carbon Fiber holds the dominant share of the global high-performance fibers market—approximately 35% in 2025—because it delivers the unmatched mechanical, thermal, and durability characteristics required for the most performance-critical industries. Its exceptionally high strength-to-weight ratio, often five times stronger than steel yet significantly lighter, makes it indispensable for aerospace, high-end automotive, defense systems, and long-span composite structures. The material’s high modulus enables the creation of ultra-rigid structural parts—such as aircraft wings, missile bodies, and wind turbine spars—that must resist deformation under extreme loads. Carbon fiber also offers inherent resistance to high temperatures, corrosive environments, and fatigue stresses, allowing it to endure cyclic loading in aerospace and industrial machinery far better than glass or aramid fibers. Additionally, the dominance of PAN-based carbon fiber (representing 70–90% of global production) reinforces its market leadership, as PAN precursors enable the fabrication of ultra-high-strength fibers optimized for advanced composites. The strong supply chain integration between precursor manufacturers, composite producers, and aerospace and automotive OEMs further strengthens carbon fiber’s entrenched position as the leading high-performance fiber type globally.

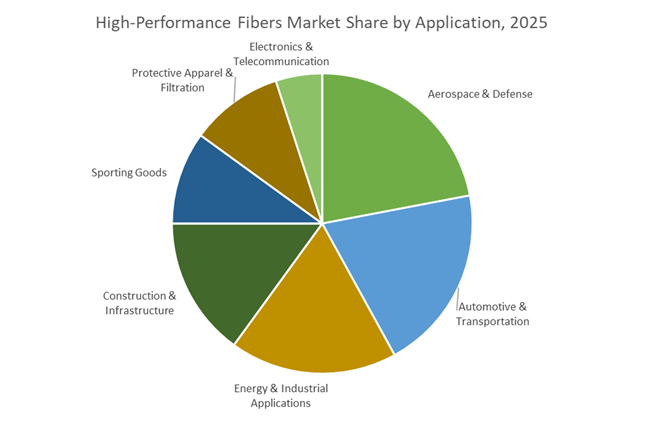

Market Share by Application: Aerospace & Defense Dominates Due to Its Reliance on High-Modulus Fibers for Efficiency, Safety, and Mission-Critical Performance

The Aerospace & Defense sector represents the largest application segment—capturing around 22% of the global market in 2025—because high-performance fibers, especially carbon fiber, are central to achieving fuel efficiency, structural optimization, and next-generation defense capabilities. Modern commercial aircraft such as the Boeing 787 and Airbus A350 use composites for more than 50% of their structural weight, relying on carbon fiber reinforced polymers (CFRP) to dramatically reduce fuel burn, extend operating range, and lower lifecycle maintenance costs. In military platforms, high-performance fibers enable lightweight ballistic protection, hypersonic vehicle components, UAV structures, and stealth technologies, all of which demand materials that offer superior stiffness, low radar reflectivity, and resistance to extreme temperatures. Although the wind energy and automotive industries consume large volumes of fiber composites, aerospace applications require higher-modulus, certified grades with stringent mechanical and safety specifications, resulting in disproportionately higher revenue contribution. As global aircraft backlogs grow and defense modernization programs accelerate, the sector continues to drive the premium end of the high-performance fibers market, solidifying its position as the most influential application segment by value.

Country Analysis: Hotspots Shaping the Global High Performance Fibers Market

China: Breakthroughs in T1000-Class Carbon Fiber and Renewable Energy Megaproject Demand

China has become the world’s most influential powerhouse in the High Performance Fibers (HPF) Market, transforming from a volume producer into a global leader in advanced carbon fiber innovation. Domestic manufacturers have successfully broken the historic Western monopoly on T1000-class high-tenacity carbon fiber, enabling local OEMs to meet stringent demands in aerospace, defense, and advanced automotive platforms. This technological milestone positions China at the forefront of global HPF material capability, driving widespread localization of critical composites.

China’s renewable energy infrastructure expansion, especially the government-backed target of 100 GW/year of new offshore wind capacity, is dramatically increasing the demand for HS (High Strength) and HM (High Modulus) fibers for next-generation wind turbine blades. Domestic producers like Zhongfu Shenying Carbon Fiber are rapidly scaling their annual output using industrialized dry spray–wet spinning technologies, securing a top-ten global ranking. The country’s aggressive vehicle electrification schedule and lightweighting mandates continue to expand the use of carbon fiber reinforced polymer (CFRP) in NEVs. Meanwhile, Chinese companies with captive precursor lines enjoy distinct cost advantages, strengthening their competitive position in hybrid carbon-glass fiber composites for large structural applications.

Japan: Global Leader in High-Modulus Carbon Fiber, Aramid Fiber Innovation, and Specialty Fiber R&D

Japan remains the world’s most advanced hub for high-modulus carbon fiber, aramid fiber engineering, and next-generation polymer science, driven by the unmatched technological leadership of companies such as Toray Industries and Teijin Limited. These corporations continue to set global performance standards with new HM and UHM (Ultra-High Modulus) variants specifically optimized for extreme temperature aerospace structures, precision industrial tooling, and elite sporting applications. Japan’s specialty fiber portfolio extends into Polybenzoxazole (PBO), prized for exceptional flame resistance, tensile strength, and long-term thermal stability, aligning with Japan’s focus on highly specialized fibers for protective and industrial applications.

To meet rising Asia-Pacific demand, Teijin and Toray have expanded operations across China and Southeast Asia, strengthening supply resilience and shortening delivery cycles for aramid and advanced polyketone fibers. Japan’s aerospace partnerships—including long-standing qualification programs with Boeing and Airbus—ensure its high-performance fiber products remain integrated into the world’s most critical aircraft platforms. Sustainability is also becoming central: leading Japanese suppliers are investing in bio-based HPF routes and recyclable composite systems, contributing to the global shift toward circular high-performance materials.

United States: Aerospace-Qualified Carbon Fiber and Ballistic-Grade Fiber Systems for Defense Modernization

The United States remains a strategically critical market for aerospace-grade carbon fiber, ballistic protection fibers, and defense-driven high modulus materials. The U.S. military’s long-term modernization programs continue to propel demand for para-aramid fibers (Kevlar®) and Ultra-High Molecular Weight Polyethylene (UHMWPE) for body armor, aircraft armor kits, next-generation helmets, and lightweight ballistic vehicle panels. With escalating geopolitical priorities, the HPF market in the U.S. benefits from predictably rising procurement cycles and extensive federal funding.

Aerospace giants rely heavily on domestic suppliers like Hexcel Corporation, whose HexTow® carbon fiber and honeycomb cores remain essential for flagship aerospace programs such as the Boeing 787 Dreamliner and the F-35 fighter jet, where composite materials enhance fuel efficiency, fatigue tolerance, and structural integrity. Ongoing investments expand domestic prepreg production and carbon fiber precursor lines to secure the U.S. supply chain against foreign dependence. The U.S. also channels significant public–private capital into hydrogen mobility: specialized carbon fibers for Type-IV hydrogen pressure vessels are experiencing strong demand as FCEVs and large-scale hydrogen storage systems scale up.

Germany: European Center for Automotive Lightweighting and Thermoplastic Composite Integration

Germany serves as Europe’s most advanced engineering hub for automotive lightweighting, structural HPF integration, and thermoplastic composite innovation. Driven by EU emissions regulations and OEM commitments to mobility decarbonization, German automakers are accelerating adoption of carbon and glass fiber composites in chassis elements, crash structures, and battery enclosures. This trend expands the role of HPFs in increasing driving range, reducing fuel consumption, and enabling safer electric mobility.

Major players like SGL Carbon SE continue expanding capacity for industrial-grade carbon fiber to support both the surging European automotive sector and the continent’s growing wind energy footprint. Germany also leads the EU in the development of thermoplastic composites, leveraging high-performance fibers integrated into PEEK, PPS, and PA matrices to enable high-speed injection molding of structurally demanding parts. With Europe’s offshore wind expansion accelerating, German-supported blade manufacturing requires long, fatigue-resistant fiber-reinforced structures. Furthermore, the nation’s universities and industrial consortia are spearheading composite recycling innovation, creating scalable pathways for reclaiming carbon and glass fibers from decommissioned blades and end-of-life automotive components—supporting the circular economy of high-performance fibers.

India: Government-Led Expansion of Technical Textiles and Domestic HPF Manufacturing Capacity

India has rapidly emerged as a high-potential growth market for high performance fibers, driven by strong government support across technical textiles, defense indigenization, and industrial infrastructure. The Production Linked Incentive (PLI) Scheme for Textiles allocates substantial funding toward MMF (Man-Made Fiber) and technical textiles capacity building, directly supporting India’s domestic production of advanced fibers used in filtration media, protective gear, automotive components, and industrial reinforcement products.

The PM MITRA Parks Scheme, with seven mega integrated textile parks, is designed to build world-class infrastructure for HPF production, reducing India’s dependence on imports and creating export-ready manufacturing ecosystems. The Ministry of Textiles is also supporting start-ups through the GREAT R&D scheme, catalyzing innovation in composite materials, biomedical textiles, and industrial HPF applications. Major global suppliers such as Owens Corning are expanding high-performance glass fiber production capabilities in India, supplying the region’s booming construction, infrastructure, and renewable energy sectors. Meanwhile, India’s defense indigenization programs are stimulating demand for locally produced aramid and UHMWPE fibers, critical for body armor, vehicle protection systems, and aerospace composites.

Turkey: Strategic Carbon Fiber Production Base Empowered by DowAksa and Regional Export Strength

Turkey plays a pivotal strategic role in the global High Performance Fibers Market, operating as a major producer and exporter of high-strength carbon fiber through the DowAksa Advanced Composites joint venture, a 50/50 partnership between Dow Chemical and Aksa. This collaboration positions Turkey as one of the most competitive global suppliers of PAN-based carbon fiber, particularly for industrial applications such as wind turbine blades, civil engineering reinforcement, and automotive composites.

Turkey’s strategic geography enables it to serve as a reliable export hub to Europe, the Middle East, and North Africa, offering shorter lead times and cost-effective logistics for downstream composite manufacturers. Its carbon fibers are integral to the large-scale production of wind turbine blades, aligning with Europe’s offshore wind expansion. Aksa’s long-standing expertise as a global acrylic fiber leader provides a strong precursor advantage, ensuring stable, high-quality feedstock for PAN-based carbon fiber manufacturing. Turkey’s continued capacity expansions and export-driven strategy strengthen its role as a competitive, globally integrated HPF supplier.

Competitive Landscape: Global Leaders Scale Carbon, Aramid and UHMWPE Fiber Platforms

The competitive landscape of the High Performance Fibers Market is dominated by a small group of global producers with deep expertise in carbon fiber, aramid fiber, UHMWPE and advanced composite systems. These companies compete not just on fiber properties, but on supply chain integration, application engineering, sustainability credentials and global service networks. Japanese leaders such as Toray Industries and Teijin Limited anchor the carbon and aramid segments, while DuPont and Honeywell remain influential in aramids and UHMWPE fibers for safety and protection. Hexcel stands out as a specialist in aerospace-grade carbon fiber and structural materials, closely tied to major airframe and engine OEMs.

Toray Industries drives global growth in carbon fiber and recycled high-performance textiles

Toray Industries, Inc. is one of the most influential players in the high performance fibers market, with a portfolio that spans TORAYCA® carbon fiber, nylon, polyester and specialized technical textiles. The company operates an integrated supply chain from raw yarn to finished and sewn products, leveraging its strengths in polymer chemistry, carbon fiber precursors and nanotechnology to deliver consistent quality into aerospace, automotive, sports and industrial composites. Toray is also actively developing and commercializing recycled fibers—including its “&+™” brand derived from used plastic bottles—and recycled carbon fiber applications, aligning with OEM decarbonization targets. Its leadership in PAN-based carbon fibers for aerospace primary structures positions the company as a cornerstone supplier for programs such as next-generation commercial aircraft and high-performance industrial systems.

Teijin builds aramid and carbon fiber leadership with a strong sustainability agenda

Teijin Limited commands a powerful position in aramid and carbon fibers, with flagship brands such as Twaron® and Technora® (para-aramid), Teijinconex® (meta-aramid) and Tenax® (carbon fiber). Teijin’s core strengths lie in high-strength protection and safety solutions, where Teijinconex® is widely used in firefighting and industrial protective apparel due to its heat and flame resistance. The company is also at the forefront of sustainable materials, with the Twaron® aramid process achieving ISCC PLUS certification, and collaborative projects—such as with Bridgestone on solar car tires—showcasing circular and bio-based content in demanding applications. Beyond protection, Teijin’s fibers are increasingly deployed in infrastructure and energy, including lightweight, high-strength reinforcement for deep-sea submarine power cables and expanded carbon fiber capacity in Europe dedicated to EV composite demand and advanced mobility structures.

DuPont refocuses on downstream high-value applications as it divests aramids

DuPont de Nemours, Inc. remains a key technology leader in high performance materials, with legacy fiber brands such as Kevlar® (para-aramid) and Nomex® (meta-aramid) alongside Vamac® elastomer and a broad portfolio of high-performance engineering polymers. Strategically, DuPont is in the process of simplifying its portfolio, with the planned sale of its Aramids business in 2025 and the earlier divestment of Divinylbenzene production in 2024, enabling a sharper focus on high-growth markets including electronics, water and advanced industrial solutions. In automotive, Kevlar® fiber and Vamac® elastomer are central to lightweighting, noise reduction and durability, helping engineers meet stringent heat and pressure requirements of downsized, high-efficiency engines and e-powertrains. Across applications—from ballistic protection to industrial gaskets—Kevlar®’s strength of up to 10x that of steel on an equal weight basis remains a critical differentiator for safety and reliability.

Honeywell leverages UHMWPE Spectra fibers for ballistic and medical applications

Honeywell International Inc. is a leading force in UHMWPE-based high performance fibers, with its Spectra® fiber and Spectra Shield® ballistic composites forming the backbone of many advanced armor systems. Spectra® fiber is pound-for-pound about ten times stronger than steel and offers up to 40% higher specific strength than aramid fibers, making it a benchmark material for military and law enforcement ballistic protection, helmets, vests and vehicle armor. Honeywell’s strategy centers on developing integrated armor systems, where Spectra Shield® composite structures deliver maximum protection while maintaining low weight, a critical factor in soldier mobility and vehicle performance. In parallel, the company is expanding into medical device applications, leveraging medical-grade UHMWPE fibers for minimally invasive surgical tools and implants, tapping into long-term growth in high-precision, high-strength medical technologies.

Hexcel consolidates its position as an aerospace-focused carbon fiber and composites specialist

Hexcel Corporation is a specialist in advanced composites and structural materials, with its HexTow® continuous carbon fiber, honeycomb cores and high-performance resin systems used extensively across global aerospace and defense programs. The company is a primary supplier of carbon fiber and prepreg materials for iconic platforms such as the Airbus A350 and Boeing 787, making it deeply embedded in long-term aircraft production cycles and OEM technology roadmaps. Hexcel pursues an integrated structural materials strategy, developing and marketing solutions that span from raw fiber through prepregs and molding compounds to finished structural components, ensuring tight control over performance and qualification. Ongoing investments and strategic facility expansions across North America, Europe and Asia-Pacific are designed to secure supply, reduce lead times and support rising demand from commercial aerospace recovery, defense modernization and emerging space launch vehicle programs, reinforcing its competitive edge in the high performance fibers market.

High-Performance Fibers Market Report Scope

High-Performance Fibers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$20.9 Billion

|

|

Market Size (2035)

|

$47.3 Billion

|

|

Market Growth Rate

|

8.5%

|

|

Segments

|

By Fiber Type (Carbon Fiber, Aramid Fiber, Glass Fiber, Specialty Polymers, Other Fibers), By End-Use Application (Aerospace & Defense, Automotive & Transportation, Sporting Goods, Energy & Industrial Applications, Construction & Infrastructure, Electronics & Telecommunication, Protective Apparel & Filtration), By Intermediate Product (Continuous Filament Yarns, Chopped/Staple Fibers, Roving/Tow, Prepregs, Woven Fabrics/Nonwovens)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Toray Industries, DuPont, Teijin, Mitsubishi Chemical Group, Hexcel, SGL Carbon, Solvay, Owens Corning, Kolon Industries, Zoltek, Toyobo, Kermel, DowAksa, Hyosung, Zhongfu Shenying

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

High-Performance Fibers Market Segmentation

By Fiber Type

- Carbon Fiber

- Aramid Fiber

- Glass Fiber

- Specialty Polymers

- Other Fibers

By End-Use Industry

- Aerospace & Defense

- Automotive & Transportation

- Sporting Goods

- Energy & Industrial Applications

- Construction & Infrastructure

- Electronics & Telecommunication

- Protective Apparel & Filtration

By Intermediate Product

- Continuous Filaments Yarns

- Chopped / Staple Fibers

- Roving / Tow

- Prepregs

- Woven Fabrics / Nonwovens

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in High-Performance Fibers Market

- Toray Industries

- DuPont

- Teijin

- Mitsubishi Chemical Group

- Hexcel

- SGL Carbon

- Solvay

- Owens Corning

- Kolon Industries

- Zoltek

- Toyobo

- Kermel

- DowAksa

- Hyosung

- Zhongfu Shenying.

*- List not Exhaustive

Research Coverage: High Performance Fibers Market

The latest USDAnalytics study on the High Performance Fibers Market provides an in-depth strategic assessment that goes far beyond topline sizing as this report investigates how carbon fiber, aramid fiber, UHMWPE and other advanced fiber systems are reshaping aerospace, wind energy, EVs, protective apparel and industrial applications; it captures key technology breakthroughs in fiber precursors, recycling, fire resistance and fatigue performance, while our analysis reviews OEM lightweighting mandates, decarbonization roadmaps, defense modernization programs and renewables build-out that collectively redefine demand visibility through 2035; the study highlights how portfolio reshaping, ISCC-certified aramid production, new UHMWPE offshore uses and EV battery safety fibers are changing competitive positioning and margin structures across regions, and this report is an essential resource for executives, product strategists, investors and procurement leaders who need granular insight into pricing dynamics, capacity additions, application-specific adoption curves, sustainability initiatives and long-term contract opportunities across the global high performance fibers ecosystem.

Scope Highlights

- Segmentation:

By Fiber Type – Carbon Fiber, Aramid Fiber, Glass Fiber, Specialty Polymers, Other Fibers

By End-Use Industry – Aerospace & Defense; Automotive & Transportation; Sporting Goods; Energy & Industrial Applications; Construction & Infrastructure; Electronics & Telecommunication; Protective Apparel & Filtration

By Intermediate Product – Continuous Filament Yarns; Chopped / Staple Fibers; Roving / Tow; Prepregs; Woven Fabrics / Nonwovens

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Time Frame: Historic data from 2021 to 2025 and forecast data from 2026 to 2034.

- Companies Covered: Analysis / profiles of 15+ leading high performance fiber producers and composite material players.