Market Overview: High-Hardness, Mid-Ir Transparent Ceramics Transforming Aerospace, Defense & Laser Systems

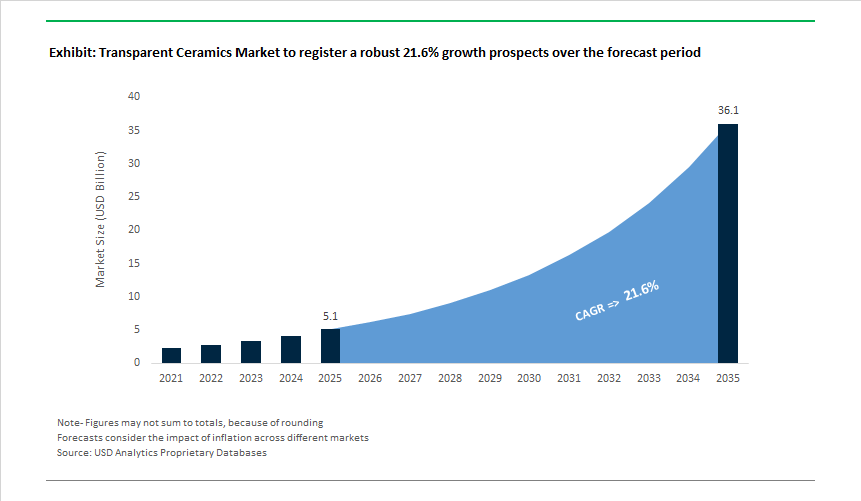

The Transparent Ceramics Industry is valued at USD 5.14 billion in 2025 and is projected to reach USD 36.37 billion by 2035, expanding at an exceptional 21.6% CAGR as aerospace, defense, and photonics platforms migrate toward operating regimes that conventional optical glass and single-crystal materials can no longer survive. This is not a substitution market driven by incremental performance; it is a capability-driven expansion where transparent ceramics unlock system architectures that would otherwise be infeasible.

At a strategic level, growth is being pulled by platform modernization and threat evolution. Next-generation aerospace vehicles, missile systems, hypersonic platforms, and directed-energy weapons operate under simultaneous mechanical, thermal, and optical stress. Transparent ceramics-such as AlON, spinel, and polycrystalline YAG-enable optical windows, domes, and gain media that maintain transparency while resisting erosion, impact, and thermal shock far beyond the limits of glass or sapphire. As a result, these materials are increasingly treated as structural-optical components, not passive windows, embedding them deeply into system qualification and defense procurement cycles.

A second structural driver is the re-architecture of infrared and laser systems. The rapid proliferation of multispectral sensing, uncooled thermal imaging, and high-power solid-state lasers has shifted material priorities toward mid-infrared transparency, high laser-damage thresholds, and thermal stability under sustained power densities. Polycrystalline transparent ceramics provide a compelling balance: they deliver high IR transmission across critical bands while enabling scalable manufacturing formats that are difficult or uneconomic to achieve with single crystals. This has accelerated adoption across EO/IR payloads, laser designators, rangefinders, and industrial and defense laser systems.

Cost, scale, and manufacturability are reinforcing adoption momentum. The market is witnessing a transition from sapphire to advanced polycrystalline ceramics as OEMs seek materials that can be produced in larger formats, tighter thickness tolerances, and more complex geometries without prohibitive yield loss. This shift materially improves program economics for transparent armor, sensor domes, and optical housings, particularly as production volumes rise and platform lifecycles extend. Manufacturers that can consistently achieve near-zero porosity, uniform grain structures, and optical homogeneity at scale are moving upstream in strategic importance.

Transparent armor represents a high-value application cluster where performance and economics converge. Modern armor systems must withstand ballistic impact, extreme aerodynamic heating, and rapid thermal gradients while preserving optical clarity for situational awareness and targeting. Transparent ceramics meet these requirements while offering higher hardness and thinner profiles than laminated glass solutions, reducing system weight and improving survivability. Once qualified, these materials are typically locked into long defense programs, supporting durable, high-margin revenue streams.

From a competitive standpoint, the industry favors players with deep process control rather than broad portfolios. Advanced sintering, hot isostatic pressing, precision polishing, and emerging additive manufacturing techniques define entry barriers, while customer qualification timelines create strong incumbency advantages. As defense agencies and laser OEMs increasingly prioritize domestic supply security and production scalability, transparent ceramics are evolving into strategic materials infrastructure rather than niche optical components.

Market Analysis: Strong Global Momentum Driven By Defense Funding, 3D Printing Capabilities and AI-Optimized Sintering

The Transparent Ceramics Industry saw a series of disruptive advancements in material science, production automation and government-backed defense research. In October 2024, CoorsTek highlighted its ability to produce polycrystalline alumina components for LiDAR systems-indicating escalating adoption of transparent ceramics across autonomous vehicle sensing. By January 2025, CeraNova achieved scale-up of large-format Spinel plates for electro-optical windows, demonstrating material scalability required for transparent armor and wide-angle optical apertures.

In March 2025, a major Japanese electronics manufacturer shifted smartphone camera lens covers to sapphire ceramic, reinforcing the movement toward mechanically superior optical materials in consumer electronics. On the other hand, May 2025 saw Saint-Gobain allocate €120 million to automate its Roussillon facility, increasing advanced ceramic output by 30% and reducing defects below 0.5%. This transition reflects global trends toward high-precision manufacturing and widening supply capacity for next-generation optical ceramics.

As the year progressed, innovation accelerated. August 2025 research validated the use of AI-optimized sintering to achieve near-theoretical densities (<0.005% porosity), a breakthrough enabling higher clarity and reduced scattering in YAG-based ceramics. In September 2025, Tethon 3D’s acquisition of TA&T expanded 3D-printing access for transparent ceramics, opening design possibilities for complex geometries. November 2025 marked Kyocera’s European production expansion for advanced optical ceramics, followed by December 2025, where the U.S. DoD awarded grants up to $1.5 million per project to advance transparent ceramic domes and sensor protection systems-solidifying aerospace and defense as the market’s fastest-growing segment.

Transparent Ceramics Market Trends and Opportunities

Trend 1: Scaling of Large-Aperture Sapphire and Spinel Windows for Defense Platforms

Defense system architectures are moving decisively toward large, integrated optical apertures rather than discrete sensor ports. This structural shift favors transparent ceramics—particularly sapphire and magnesium aluminate spinel—over conventional glass due to their unmatched hardness, thermal conductivity, and ballistic tolerance.

Between 2024 and 2025, manufacturers demonstrated large-aperture transparent ceramic windows exceeding 15–20 inches in diameter, a threshold critical for next-generation EO/IR sensor fusion. Spinel, in particular, has emerged as the preferred material for hypersonic and high-Mach platforms, offering ~10× higher thermal conductivity and ~7× higher strength than traditional glass, allowing survivability where aerodynamic heating can exceed 1,000 °C. This capability directly supports integrated targeting systems used on platforms such as advanced strike fighters and long-range unmanned systems.

From an optical standpoint, advances in colloidal processing and Hot Isostatic Pressing (HIP) have pushed spinel transmission beyond 75% in the visible spectrum and 80% in the infrared, enabling a single window to support visible, MWIR, and LWIR sensors simultaneously. This reduces payload weight, simplifies optical stacks, and improves reliability under vibration and shock. Defense funding alignment reinforces this trend, with FY-2025 U.S. aerospace and space budgets prioritizing durable, multi-spectral optics for missile guidance, ISR payloads, and space-borne imaging—applications where sapphire-based and spinel-based transparent ceramics now dominate specifications.

Trend 2: Transparent Ceramics as Plasma-Resistant Materials in EUV and DUV Lithography

At the semiconductor manufacturing frontier, transparent ceramics are becoming indispensable as chipmakers push toward 2nm and sub-2nm nodes. Extreme Ultraviolet (EUV) lithography environments impose a combination of high-energy photon exposure, aggressive plasma chemistry, and ultra-high vacuum requirements that exceed the durability limits of quartz and specialty glass.

With High-NA (0.55 NA) EUV scanners from ASML entering high-volume deployment in 2025—each tool exceeding $380 million in value—the tolerance for contamination or optical drift has effectively reached zero. Ultra-pure alumina- and yttria-based transparent ceramics are now specified for chamber windows, mask-handling components, and inspection interfaces because they combine zero outgassing, plasma erosion resistance, and long-term optical stability under 500W+ EUV sources.

The expansion of AI accelerators and 5G baseband silicon further amplifies this trend. With TSMC committing $32–36 billion in 2025 CAPEX, secondary demand for transparent ceramic inspection windows, metrology covers, and plasma-exposed optics is rising sharply. These components play a silent but essential role in yield protection, enabling atomic-scale defect detection without introducing particulate risk inside the fab.

Opportunity 1: High-Refractive-Index Transparent Ceramics for AR Waveguide Optics

Augmented reality hardware faces a structural bottleneck: field-of-view (FoV) expansion without lens bulk or weight penalties. Transparent ceramics—particularly lithium aluminosilicate (LAS) glass-ceramics—are emerging as the most credible solution to this challenge.

By inducing controlled nanocrystalline precipitation within the glass matrix, LAS-based transparent ceramics now achieve refractive indices approaching 1.8–1.9, significantly higher than polymer waveguides. At the same time, they deliver a ~25% increase in surface hardness, dramatically improving scratch resistance—one of the primary failure points of polymer-based AR optics. These properties allow thinner waveguides with wider FoV, directly addressing consumer comfort and optical immersion.

Thermal stability further strengthens the value proposition. Near-zero thermal expansion ensures color fidelity and optical alignment during sustained processing loads, while 2025-era ion-exchange treatments have improved surface compressive stress, enabling ruggedized AR devices for industrial, defense, and field-service applications. Manufacturing scalability is also improving: Nanoimprint Lithography (NIL) on transparent ceramic substrates is now achieving >95% transmission above 400 nm, unlocking high-volume production economics previously limited to polymer optics—without sacrificing durability.

Opportunity 2: Polycrystalline Ceramic Laser Gain Media for Fusion and Directed Energy

High-energy laser systems are undergoing a structural transformation as polycrystalline transparent ceramics displace single-crystal gain media in applications where scale, repetition rate, and thermal management are critical. Ceramic Nd:YAG and Yb:YAG now outperform boule-grown crystals in manufacturability and homogeneity, particularly for large apertures exceeding 50 mm.

Momentum accelerated following fusion ignition milestones at the National Ignition Facility, triggering global investment in Inertial Fusion Energy (IFE) architectures. In 2025, Hamamatsu Photonics demonstrated 106 J at 10 Hz laser output using a Yb:YAG ceramic multi-disk configuration, a critical stepping stone toward the 10 kJ, 10 Hz per-beam targets required for commercial fusion reactors.

From an industrial and defense standpoint, ceramic gain media offer decisive advantages: ~40% higher manufacturing yield, up to 3× higher dopant concentration, and 10× higher thermal conductivity than fused silica, dramatically reducing thermal lensing and beam distortion. By 2024–2025, composite ceramic gain architectures—featuring undoped caps diffusion-bonded to doped cores—accounted for over 65% of media used in high-energy directed-energy R&D systems. These materials are now central to scaling kilowatt-class lasers for defense, precision manufacturing, and next-generation energy systems.

Market Share Analysis: Transparent Ceramics Market

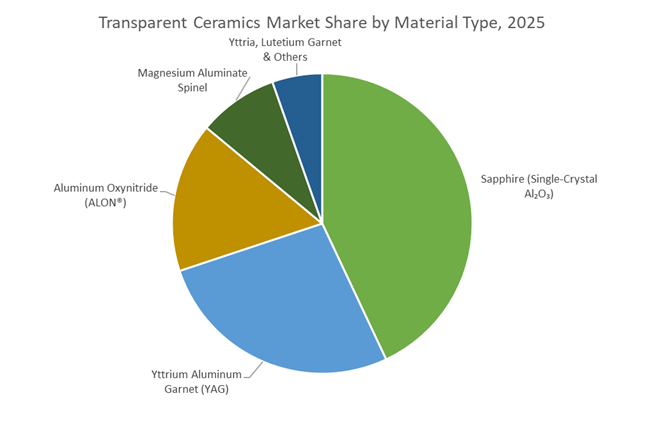

Market Share by Material Type: Sapphire Dominates Through Extreme-Environment Performance Economics

Sapphire accounts for approximately 40% of the transparent ceramics market because it occupies a performance tier that no other transparent material can economically displace in 2025. Its dominance is not driven by optical clarity alone, but by a non-substitutable combination of hardness, thermal stability, and mechanical rigidity that directly aligns with high-value industrial and defense use cases. With a Mohs hardness of 9 and a Young’s modulus of 420 GPa, sapphire delivers six times the stiffness of standard glass, enabling its use in semiconductor carrier plates and optical windows where even micron-level deformation would compromise yield or signal accuracy. The ability to maintain structural integrity and transparency up to 2,040°C positions sapphire as the default choice for high-temperature furnaces, propulsion systems, and IR-transparent viewports, eliminating lifecycle replacement costs associated with glass or polycrystalline ceramics. Critically, 2025 manufacturing scale-ups—where sapphire boules now reach 83–200 kg via Kyropoulos and EFG methods—have shifted sapphire from a niche optics material to a large-format, commercially viable solution for surveillance windows and multi-spectral sensor domes up to 30 inches. When AR-coated, sapphire achieves 98% transmission across visible and mid-IR bands, making it indispensable for multi-sensor fusion systems used in harsh, obscured environments. These structural and optical advantages translate directly into lower failure risk, longer service life, and higher system uptime—explaining why sapphire continues to command the largest share despite higher upfront material costs.

Market Share by Application: Aerospace, Defense & Security Anchor Demand Through Mission-Critical Requirements

Aerospace, defense, and security applications represent around 35% of transparent ceramics demand, reflecting the sector’s reliance on materials that must survive ballistic impact, hypersonic heat loads, and optical distortion simultaneously. Transparent ceramics—particularly sapphire and aluminum oxynitride—have become mission-critical components rather than optional upgrades. Replacing laminated armored glass with transparent ceramics delivers up to 30% airframe weight reduction, directly improving payload capacity, fuel efficiency, and mission radius for UAVs, fighter aircraft, and ISR platforms. The application share is further reinforced by sapphire’s ability to withstand Mach 5+ thermal shock, a non-negotiable requirement for hypersonic missile seekers and advanced radomes where frictional heating destroys conventional materials. In sensing and targeting systems, sapphire optics enable 10x higher depth-measurement accuracy for reflective or semi-transparent objects, a capability now embedded into 2025–2026 defense robotics and autonomous logistics platforms. Perhaps most decisive is ballistic performance: transparent ceramic strike faces can stop .50 caliber rounds at roughly half the thickness of armored glass, allowing vehicle and cockpit designers to reduce armor footprint without sacrificing protection. These quantifiable gains in survivability, range, and system accuracy explain why aerospace and defense budgets remain the largest and most stable demand source for transparent ceramics globally.

Competitive Landscape: High-Purity, High-Performance Optical Ceramics Define Competitive Advantage

The Transparent Ceramics competitive environment is dominated by companies with deep expertise in controlled sintering, advanced powder synthesis, polycrystalline optical materials, and large-format manufacturing. Leaders succeed by combining superior mechanical properties with optical clarity, thermal-shock tolerance and the ability to deliver armor-grade components at scale.

Saint-Gobain Leads IR Transparent Ceramics With Dominant Aerospace & Laser Materials Portfolio

Saint-Gobain maintains commanding leadership, supplying CERADIR transparent ceramics to an estimated 70% of European aerospace thermal imaging systems. The company’s stronghold in YAG transparent ceramics gives it ~35% global material share, supported by heavy investment, including a €120 million automation upgrade aimed at improving output consistency and quality. Saint-Gobain’s portfolio spans visible to mid-IR applications, and products like Hexoloy SiC serve extreme environments such as nuclear viewing ports, showcasing deep integration into high-performance optical and structural ceramic markets.

Ceramtec Advances High-Power Laser & Medical Transparent Ceramics Through Precision Sintering

CeramTec has emerged as a key supplier of transparent ceramics for High-Power Lasers, particularly Nd:YAG components, leveraging its expertise in high-purity sintering. The company also maintains a strong footprint in medical-grade ceramics, holding 25% more hospital contracts for high-purity materials than competitors. CeramTec’s adoption of 3D-printed Al₂O₃ and SiSiC components positions it to serve optics requiring complex geometries. The industrial segment benefits from its materials engineered to withstand extreme thermal and chemical stresses-particularly relevant for semiconductor and precision instrumentation sectors.

Coorstek Strengthens Position in Lidar, Transparent Armor & High-Strength Optical Components

CoorsTek produces tens of millions of transparent and translucent ceramic components annually, demonstrating industrial-scale manufacturing capability. Its expertise spans Polycrystalline Alumina and Spinel-key materials for transparent armor and harsh-environment sensor windows. CoorsTek’s supply to automotive LiDAR systems places it at the forefront of next-generation optical sensing. Through its Sustainable Net Shaping program, the company reduces waste via injection molding and other near-net-shape techniques, strengthening its competitiveness in cost-sensitive, high-volume applications.

Surmet Dominates ALON Transparent Armor For Defense, Missile Systems & EO Sensors

Surmet is the world’s leading producer of ALON (Aluminum Oxynitride), a flagship transparent ceramic used in lightweight transparent armor, missile domes and multispectral EO windows. ALON’s high hardness and broad-spectrum transparency deliver strong advantages over both glass and sapphire. Surmet is also expanding large-format ALON manufacturing, essential for next-gen military vehicle windows. Strategic partnerships with defense primes such as BAE Systems reinforce its role in the U.S. aerospace and defense supply chain.

Konoshima Chemical Drives Cost-Efficient Spinel Production For Mid-IR & Optical Components

Konoshima Chemical specializes in Spinel (MgAl₂O₄), one of the most cost-effective transparent ceramics for mid-IR applications-often ~45% cheaper than ALON for certain specifications. Its mastery of precision powder synthesis and uniform sintering enables scalability for optical lenses and IR sensor components. Konoshima’s materials are widely adopted in optoelectronics, specialty optics and advanced laser applications, supported by strong capabilities in polycrystalline fabrication and consistent grain boundary control.

The United States transparent ceramics market in 2025 is decisively anchored to defense modernization and aerospace sensor superiority, with Aluminum Oxynitride (ALON) positioned as a strategic material rather than a specialty ceramic. The U.S. Department of Defense’s integration of ALON into its FY2025 Joint Light Tactical Vehicle (JLTV) procurement framework marks a structural inflection point for domestic transparent ceramics capacity. Compared with conventional laminated ballistic glass, ALON panels deliver roughly 30% weight reduction at equivalent or superior ballistic protection, directly improving vehicle mobility, payload efficiency, and fuel economy. This procurement signal has accelerated upstream investment in high-purity powder synthesis, hot pressing, and large-format sintering, reinforcing transparent ceramics as a defense-critical supply chain.

Beyond ground platforms, transparent ceramics are becoming indispensable to U.S. ISR and space programs. In late 2024, Surmet Corporation supplied ALON infrared sensor domes for Northrop Grumman’s Global Hawk UAV upgrades, demonstrating a 25% improvement in target acquisition accuracy due to ALON’s thermal stability and optical uniformity under extreme operating conditions. Parallel efforts by Lawrence Livermore National Laboratory and NASA in 2025 are evaluating large-format YAG transparent ceramics for fusion laser systems and space-debris mitigation, underscoring how transparent ceramics are transitioning into dual-use strategic infrastructure materials across defense, space, and energy research.

Japan: Fusion Energy, Clean Synthesis, and Laser-Grade Ceramics

Japan’s transparent ceramics strategy is tightly coupled with fusion energy development and sustainable materials processing, leveraging decades of leadership in fine ceramics and chemical engineering. In September 2025, Konoshima Chemical announced a major breakthrough in Yttrium Aluminum Garnet (YAG) transparent ceramics optimized for high-output laser assemblies used in experimental fusion reactors. These ceramics must sustain extreme photon flux, thermal gradients, and long-duty cycles—performance regimes where conventional optical glass and single-crystal sapphire are structurally limited.

A critical differentiator for Japan lies in resource strategy and synthesis sustainability. Konoshima’s seawater-derived magnesium compounds, disclosed in August 2025, reduce reliance on constrained brine or mined inputs, strengthening long-term material security for spinel- and YAG-based transparent ceramics. These advances are reinforced by the Japanese government’s GX 2040 Vision, which is actively funding low-emission sintering and energy-efficient densification techniques. As a result, Japan is emerging as the global benchmark for laser-grade, fusion-ready transparent ceramics manufactured under carbon-constrained industrial models.

Germany: Circular Glass-Ceramics and Precision Optical Integration

Germany’s transparent ceramics market is distinguished by its emphasis on circular economy compliance and high-precision optical systems, aligning sustainability mandates with industrial competitiveness. In August 2025, SCHOTT AG completed a landmark industrial pilot demonstrating that externally collected glass-ceramic shards can be remelted and reincorporated without measurable performance degradation. This achievement represents a pivotal step toward closed-loop manufacturing for technical glass-ceramics—an area previously constrained by purity and defect concerns.

On the application side, SCHOTT’s February 2025 launch of advanced transparent ceramics for industrial sensors and defense-grade laser optics reflects Germany’s strength in system-level integration. These materials offer enhanced scratch resistance, thermal shock tolerance, and optical stability in harsh environments, supporting deployment in smart factories, autonomous inspection systems, and directed-energy platforms. Investments at SCHOTT’s Mainz facility in digital kiln management and energy-intensity reduction further reinforce Germany’s role as Europe’s hub for sustainable, high-precision transparent ceramic production.

China: Resource Authorization and Industrial-Scale Armor Production

China is repositioning itself from a volume-driven ceramics producer to a strategic regulator of transparent ceramic inputs, particularly rare earth elements essential to advanced compositions. In December 2025, the Ministry of Commerce of the People's Republic of China implemented a managed licensing framework covering yttrium and other rare earths critical for YAG and spinel transparent ceramics. This policy prioritizes domestic value-added processing, effectively channeling rare earth availability toward Chinese sintering, HIP, and SPS facilities rather than raw export markets.

Industrial upgrading is visible across the value chain. At Ceramics China 2025, more than 800 exhibitors showcased advances in Hot Isostatic Pressing (HIP) and Spark Plasma Sintering (SPS) designed to minimize light-scattering defects in large-format transparent armor panels. These capabilities are increasingly aligned with China’s automotive roadmap, where transparent ceramic-based LIDAR sensor windows are being adopted to support the 15.5 million New Energy Vehicle (NEV) production target. Collectively, these developments position China as a scale-driven yet tightly controlled producer of transparent ceramics for armor, sensing, and mobility applications.

South Korea: Sapphire-Based Thermal and Medical Applications

South Korea’s transparent ceramics strategy is embedded within its KRW 700 trillion semiconductor megacluster, where thermal resilience and optical durability are mission-critical. In January 2025, Kyocera Corporation expanded its South Korean operations with a new portfolio of polycrystalline sapphire components engineered for plasma-rich semiconductor processing environments and high-resolution medical imaging. Sapphire’s combination of optical transparency, hardness, and chemical resistance makes it indispensable for wafer processing windows, inspection optics, and implantable diagnostic devices.

In parallel, the South Korean government is funding R&D into glass-ceramic interposers for High Bandwidth Memory (HBM) stacks, where thermal loads from AI accelerators exceed the capabilities of organic substrates. Transparent and semi-transparent ceramics are increasingly evaluated for their ability to combine heat spreading, electrical insulation, and optical access, positioning South Korea at the intersection of transparent ceramics, advanced packaging, and medical technology.

India: Electronics PLI and Medical Import Substitution

India’s transparent ceramics market is in an early but strategically significant growth phase, driven by electronics localization and medical import substitution. Under the ₹25,000 crore Production Linked Incentive (PLI) scheme, the Ministry of Electronics and Information Technology is incentivizing domestic production of ceramic capacitors, RF substrates, and transparent dielectric components for 5G/6G communication systems. These initiatives aim to reduce reliance on East Asian suppliers while establishing India as a regional alternative for advanced electronic materials.

Healthcare represents a parallel demand engine. Indian manufacturers are scaling production of bioinert transparent zirconia for dental and orthopedic restorations, targeting a reduction in the country’s ~70% dependence on imported high-end medical ceramics. As regulatory frameworks mature and sintering expertise improves, India’s transparent ceramics sector is evolving from laboratory-scale output toward commercial-grade medical and electronic applications, supported by sustained policy backing.

2025 Strategic Matrix: Transparent Ceramics National Comparison

Transparent Ceramics Strategic Matrix

|

Country

|

Primary Strategic Driver

|

2025 Strategic Milestone

|

Primary Material Focus

|

|

United States

|

Defense & aerospace systems

|

ALON adoption in JLTV and UAV upgrades

|

Aluminum Oxynitride (ALON)

|

|

Japan

|

Fusion energy & clean synthesis

|

Konoshima YAG breakthrough for fusion lasers

|

Yttrium Aluminum Garnet (YAG)

|

|

Germany

|

Circular economy & optics

|

Successful remelting of glass-ceramics

|

High-precision glass-ceramics

|

|

China

|

Resource sovereignty & scale

|

MOFCOM licensing for yttrium/REE inputs

|

Sintered armor & LIDAR ceramics

|

|

South Korea

|

Semiconductor & MedTech

|

Kyocera sapphire expansion

|

Polycrystalline sapphire

|

|

India

|

Electronics PLI & healthcare

|

₹25k Cr incentive-driven localization

|

Bioceramics & RF dielectrics

|

Transparent Ceramics Market Report Scope

Transparent Ceramics Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.14 Billion

|

|

Market Size (2035)

|

$36.37 Billion

|

|

Market Growth Rate

|

21.6%

|

|

Segments

|

By Material Type (Sapphire, Yttrium Aluminum Garnet, Aluminum Oxynitride, Magnesium Aluminate Spinel, Zirconium Oxide, Yttria, Lutetium Aluminum Garnet), By Product Form (Sheets & Plates, Domes & Hemispheres, Rods & Tubes, Custom Shaped Components), By Application (Optics & Optoelectronics, Aerospace / Defense & Security, Healthcare & Medical, Consumer Electronics, Energy & Industrial)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

CoorsTek Inc., Surmet Corporation, SCHOTT AG, Kyocera Corporation, Konoshima Chemical Co. Ltd., CeramTec GmbH, II-VI Optical Systems, Murata Manufacturing Co. Ltd., CeraNova Corporation, Saint-Gobain S.A., AGC Inc., Meller Optics Inc., Raytheon Technologies, General Electric, Xiamen Wintrustek Advanced Materials

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Transparent Ceramics Market Segmentation

By Material Type

- Sapphire

- Yttrium Aluminum Garnet

- Aluminum Oxynitride

- Magnesium Aluminate Spinel

- Zirconium Oxide

- Yttria

- Lutetium Aluminum Garnet

By Product Form

- Sheets & Plates

- Domes & Hemispheres

- Rods & Tubes

- Custom Shaped Components

By Application

- Optics & Optoelectronics

- Aerospace, Defense & Security

- Healthcare & Medical

- Consumer Electronics

- Energy & Industrial

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Transparent Ceramics Market

- CoorsTek, Inc.

- Surmet Corporation

- SCHOTT AG

- Kyocera Corporation

- Konoshima Chemical Co., Ltd.

- CeramTec GmbH

- II-VI Optical Systems

- Murata Manufacturing Co., Ltd.

- CeraNova Corporation

- Saint-Gobain S.A.

- AGC Inc.

- Meller Optics, Inc.

- Raytheon Technologies

- General Electric

- Xiamen Wintrustek Advanced Materials

*- List not Exhaustive