Corrugated Packaging Market Overview: Scaling to $256.4 Billion by 2034 on E-commerce, Circular Fiber, and Smart Print

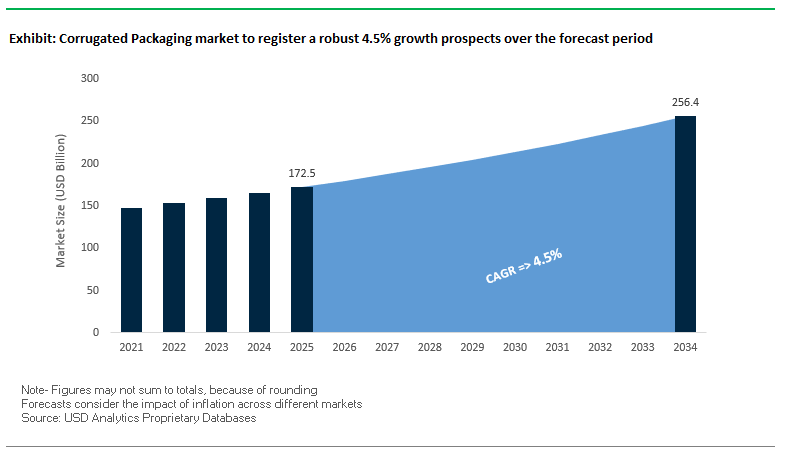

The global corrugated packaging market is projected to grow from $172.5 billion in 2025 to $256.4 billion by 2034, at a CAGR of 4.5%. Corrugated remains the backbone of fulfillment and retail-ready packaging because it uniquely blends stacking strength, cushioning, printability, and near-universal recyclability. For procurement leaders and packaging engineers, the operational questions are clear: how to balance fiber cost volatility with downgauging and design optimization; how to meet brand sustainability KPIs without compromising compression or moisture resistance; and how to exploit digital print + smart codes to lift conversion and curb returns in e-commerce.

Key Insights for decision-makers

- E-commerce Dominance: Corrugated shipper volumes continue to expand as the default for last-mile protection and reverse logistics, favored for damage reduction and high recycling capture.

- Circular Leadership: Old corrugated containers (OCC) are recovered at industry-leading rates in North America, underscoring a mature closed-loop fiber system that reduces landfill and virgin inputs.

- Smart Packaging: >30% of new high-value packs integrate QR/NFC for authentication, instructions, and post-purchase engagement turning shippers into data endpoints.

- High-Definition Printing: Rapid uptake of on-demand digital print enables SKU-level customization, retail-ready color, and shorter campaigns without inventory bloat.

Market Analysis: 2025 Developments in AI-Led Design, Fiber Capacity, and Paper-First Substitutions

Design optimization and recycled integration (Aug–Mar 2025). In August 2025, specialized analyses spotlighted AI/predictive tools that auto-tune board grades, flute profiles, and slot patterns to meet specific BCT/ECT targets while shaving fiber directly improving unit economics and sustainability. Also in August 2025, collaborative launches of PCR-rich collation shrink inputs signaled a broader packaging trend: mixed systems around corrugated (films, carriers, liners) are incorporating recycled polymers, complementing fiber circularity in multipack and protective applications. In March 2025, Saica Group committed new U.S. capacity (Anderson, IN), adding >1.2 million MSF annually timely relief for converters managing lead times and regional freight.

Consolidation reshapes paper-based competition (Jul 2025). The Smurfit Kappa–WestRock merger (July 2025) formed Smurfit WestRock, concentrating know-how across forestry, paper, and converting. The combined scale is poised to accelerate paper-based alternatives to plastics, expand print and automation capabilities, and harmonize specifications for global brands seeking consistent pack performance across regions.

Fiber formats win new use cases (Jun–Jan 2025). In June 2025, Sonoco invested in paper-bottom rigid cans a recyclable format that often ships inside corrugated outers echoing brand moves toward paper-first bill of materials. In May 2025, DS Smith introduced DryPack in North America for seafood, replacing EPS with recyclable corrugated proof of corrugated’s advance into moisture-sensitive cold-chain. In March 2025, WestRock with Liberty Coca-Cola scaled paperboard carriers to displace plastic rings; and in January 2025, Smurfit Kappa announced a major North Africa corrugated plant, extending supply close to fast-growing markets.

Trends and Opportunities Driving the Corrugated Packaging Market

Strategic Integration of Digital Printing for On-Demand, Short-Run Packaging

The corrugated packaging market is undergoing a significant transformation with the rapid adoption of digital printing technologies, replacing legacy flexographic systems. This transition is being driven by growing demand for mass customization, faster time-to-market, and reduced inventory costs. For instance, Canon Europe documented a case study where a corrugated packaging producer successfully adopted digital printing to deliver short-run, highly customized packaging at speed, enabling faster response to seasonal campaigns, e-commerce promotions, and prototype development.

Beyond efficiency, digital printing is also helping reduce inventory waste. Unlike pre-printed corrugated boxes that often result in surplus stock and obsolescence, on-demand digital systems allow companies to print packaging only when required, supporting lean manufacturing models and reducing environmental impact. Additionally, advancements in high-resolution inkjet technology have elevated corrugated packaging aesthetics, enabling vibrant, full-color imagery directly on board. This enhances the unboxing experience and allows brands to use packaging as a powerful marketing asset, especially in e-commerce channels where first impressions directly influence consumer perception.

Adoption of Advanced Coatings and Treatments for Recyclable Barrier Performance

Another critical trend is the development of repulpable coatings and barrier treatments that make corrugated packaging suitable for food, beverages, and moisture-sensitive applications without compromising recyclability. Historically, wax and PE liners provided the necessary barriers but created recycling challenges. Today, suppliers are rolling out PFAS-free, water-based coatings that can withstand moisture and grease while remaining fully recyclable. According to a major supplier’s report, these coatings can be seamlessly reintroduced into the paper recycling stream, aligning with global circular economy mandates.

Scientific advancements are further accelerating this shift. A recent academic study on silica sol-gel hybrid coatings showed up to 98% reduction in water absorption for corrugated cardboard, delivering food-safe performance while eliminating harmful wax-based layers. Initiatives by organizations like the Fiber Box Association (FBA) are standardizing certifications for recyclable coated boxes, creating transparency for both brands and consumers. These developments position recyclable coated corrugated packaging as a sustainable alternative that meets both performance and regulatory requirements.

Development of AI-Driven Structural and Supply Chain Optimization Software

The growing role of artificial intelligence (AI) and machine learning (ML) presents a transformative opportunity for corrugated packaging design and logistics optimization. AI-driven platforms are now being used to generate right-sized packaging that minimizes void fill while ensuring adequate protection. This results in material cost savings, reduced shipping weight, and alignment with environmental, social, and governance (ESG) goals.

Furthermore, predictive AI applications are revolutionizing logistics. By analyzing order composition, palletization, and truck loading configurations, AI systems enable maximum space utilization, reducing freight costs and lowering Scope 3 emissions. Case studies from logistics providers have demonstrated measurable reductions in carbon emissions through AI-led packaging optimization. Additionally, generative AI platforms are shortening design cycles dramatically, producing hundreds of corrugated box designs in minutes compared to days under traditional workflows. This not only accelerates rapid prototyping but also fuels innovation in structural design, a critical factor in highly competitive e-commerce and FMCG packaging markets.

Expansion into High-Performance, Reusable Corrugated Systems

As businesses look to reduce single-use packaging, the development of reusable corrugated packaging systems is emerging as a major growth frontier. These systems are particularly attractive for B2B logistics and closed-loop supply chains, where durability, cost-efficiency, and sustainability converge. High-strength, multi-ply corrugated bins sometimes paired with durable plastic lids are designed for multiple trips and can be folded flat for return logistics, improving space efficiency.

Unlike reusable plastic containers (RPCs), which often require substantial upfront investment, reusable corrugated solutions provide a lower capital entry point for companies pursuing a circular model. Moreover, packaging firms are increasingly moving toward “asset management as a service”, offering solutions that include container tracking, cleaning, maintenance, and reverse logistics. This shift from a transactional sales model to a service-based ecosystem strengthens supplier-customer partnerships while opening new, recurring revenue streams. By bridging sustainability and economic efficiency, reusable corrugated systems are positioning themselves as a strategic alternative in closed-loop industrial and retail applications.

Competitive Landscape: Integrated Paper Leaders and Design-Led Specialists

A concentrated set of fiber-first players shape global corrugated combining forest assets, paper mills, converting plants, and recycling networks alongside innovators focused on automation, coatings, and print. Buyers should benchmark on vertical integration, recycled content, design software, moisture/grease resistance options, and e-commerce test protocols (e.g., ISTA/Transit).

Smurfit WestRock sharpens paper-based alternatives at global scale

Born from the July 2025 merger, Smurfit WestRock offers one of the largest portfolios: heavy-duty bulk bins, retail-ready trays, e-commerce mailers, and bag-in-box. Its vertically integrated chain from certified forests to digital print and automation delivers spec consistency, speed, and fiber security. The company is commercializing paperboard carriers and seafood DryPack-type solutions that pull share from plastics/EPS, while harmonizing global specs for multinational rollouts.

International Paper Company anchors sustainability with fiber security

International Paper supplies custom corrugated from agricultural bulk to high-graphic retail-ready displays. Strategic focus: renewable fiber sourcing, closed-loop recycling, and moisture-resistant liners/coatings for produce and cold-chain. Its investment program upgrades mills and box plants for throughput and quality stability, and its e-commerce solutions emphasize damage reduction and pack right-sizing to curb DIM charges and returns.

Packaging Corporation of America (PCA) engineers bins for automation

PCA’s lineup spans BulkMaster™/Grid-Lok bulk solutions and tailored shippers with self-locking bottoms, reinforced flanges, and AS/RS-friendly designs. Differentiator: customer-centric engineering PCA co-develops pack specs to hit compression and moisture targets with minimal board. Its corrugated replaces heavier plastics in warehousing and agriculture, improving stack safety and freight efficiency without sacrificing durability.

DS Smith Plc scales recyclable seafood and retail-ready formats

DS Smith leads with 100% recyclable corrugated systems and an integrated recycling division, enabling closed-loop programs for brand owners. In May 2025, it launched DryPack in North America to replace EPS in seafood combining wet-strength liners with proven compression performance. Its purpose “Redefining Packaging for a Changing World” shows up in fit-to-product automation, print-on-demand, and supply-chain redesign that removes waste and speeds replenishment.

Mondi Group fuses heavy-duty corrugated with circular energy

Mondi’s heavy-duty corrugated and bulk liquid corrugated containers pair high-strength boards with performance liners. In June 2025, it launched re/cycle PaperPlus Bag Advanced for humidity-sensitive goods, underscoring paper-based barrier innovation; and broader investments including a Slovakia biomass power plant support its SBTi-validated 2030 strategy. Net-net: Mondi aligns renewable energy, recyclable paper systems, and high-barrier formats to expand corrugated’s addressable use cases.

Corrugated Packaging market Share Insights

Corrugated Boxes Dominate Market Share by Product Type

Corrugated boxes, including Regular Slotted Containers (RSCs), Full Overlap (FOL), and other formats, account for 72% of the corrugated packaging market in 2025, making them the undisputed backbone of modern trade and logistics. Their dominance stems from their unmatched versatility, strength, and cost-effectiveness, which make them the default packaging choice for nearly every industry, from e-commerce fulfillment centers to food distribution networks. Their compatibility with automated filling, sealing, and palletizing equipment has reinforced their role as the structural foundation of the global supply chain. Sheets and rolls form the next-largest segment, serving as flexible protective solutions for irregularly shaped goods such as furniture and auto parts, with demand closely tied to industrial output. Corrugated displays represent a smaller but high-value segment, acting as temporary retail fixtures that double as marketing tools, enabling brands to capture consumer attention at the point of purchase. Pallets and bulk containers, while smaller by unit share, are indispensable in B2B and agricultural logistics, moving high-weight loads such as bulk food ingredients or automotive parts. These segments collectively highlight how corrugated packaging serves not just as a transport medium, but also as a protective, functional, and promotional asset across industries.

E-commerce & Retail Lead Market Share by End-Use Industry

E-commerce and retail together hold 38% of the corrugated packaging market in 2025, reflecting the structural megatrend of online shopping, where each item requires its own durable and protective shipping box. The growth of direct-to-consumer (D2C) business models and rapid parcel delivery networks has further accelerated demand for corrugated solutions, with packaging now serving as both protection and a brand experience during home delivery. Food and beverages represent 32% of the market, underscoring corrugated’s critical role as the industry’s stable volume driver. From transporting beverage bottles to protecting snack multipacks, corrugated formats are essential for shelf-ready packaging and bulk distribution. The industrial sector commands a significant portion of demand, relying on heavy-duty corrugated with high-grade fluting for shipping capital goods, machinery, and spare parts. Home and personal care brands leverage corrugated boxes not only for protection but also for premium brand differentiation, with high-quality printing and unboxing design enhancing consumer perception. Electronics and other specialized industries, including pharmaceuticals and automotive, represent smaller shares but high-value niches, where corrugated packaging integrates anti-static protection, clean-room compliance, and just-in-sequence delivery functions. This segmentation highlights how corrugated packaging adapts to both volume-driven and specialized end-user requirements, making it indispensable across global supply chains.

United States: Driving E-commerce Growth with Custom and Sustainable Corrugated Packaging

The U.S. corrugated packaging market is being transformed by the exponential growth of e-commerce, which has significantly increased demand for custom-sized, protective packaging solutions. Manufacturers are increasingly adopting box-on-demand systems, producing right-sized containers that minimize material waste, reduce shipping costs, and enhance sustainability.

Sustainability remains a central focus, with companies emphasizing lightweighting and using post-consumer recycled (PCR) content. Innovations include resins made from 100% PCR polyethylene, enhancing eco-friendly packaging initiatives. Advanced technologies, such as QR codes, RFID tags, and IoT sensors, are being integrated into corrugated boxes to provide real-time traceability, tamper detection, and enhanced supply chain visibility, particularly in pharmaceutical and food logistics. Strategic expansions and acquisitions are also driving market growth; for instance, Saica Group invested over $110 million in a new corrugated manufacturing facility in Indiana to strengthen its U.S. presence.

Germany: Leading the Circular Economy with Recyclable and Industrial Corrugated Solutions

Germany’s corrugated packaging industry is a key driver of the EU’s circular economy, strongly influenced by the German Packaging Act (VerpackG) and the European Green Deal. This regulatory framework encourages high recycling rates and the incorporation of recycled content in packaging materials. Companies are responding with fully recyclable corrugated solutions, such as DS Smith’s plastic-free e-commerce packaging, eliminating the need for additional filling materials.

The market is heavily B2B-focused, with strong demand from the automotive, machinery, and industrial sectors for durable, customized packaging suitable for transporting sensitive or high-value products. Investments in production capacity are helping manufacturers meet rising demand; for example, DS Smith invested €34.4 million in its Hungarian operations, including updating corrugators to enhance manufacturing efficiency and output.

China: High-Volume Demand Driven by Manufacturing and E-Commerce Expansion

China’s corrugated packaging market is fueled by its position as a global manufacturing and export hub and its rapidly expanding e-commerce sector, resulting in high-volume demand for efficient, cost-effective packaging. The market is also shaped by government initiatives promoting modernized supply chains and logistics systems, encouraging investments in automated production lines that increase output and ensure consistent quality.

Addressing counterfeiting and product authenticity is another critical trend, with advanced printing, smart labels, and holographic features integrated into corrugated packaging for high-value goods. However, the market is affected by raw material price fluctuations, particularly in corrugated paper, driven by global waste paper supply constraints, which influence both production costs and pricing strategies.

India: Expanding E-commerce and Sustainable Corrugated Packaging Solutions

India’s corrugated packaging market is experiencing significant growth due to the rapid expansion of e-commerce and the packaged food sector. Rising demand for home delivery of groceries, electronics, and other products has increased the need for durable, protective, and customized corrugated packaging solutions.

Government initiatives and growing environmental consciousness are driving a shift toward sustainable packaging, emphasizing the use of recycled paper in corrugated boxes. Domestic manufacturers, including Wadpack and Alok Industries, are expanding production capabilities with state-of-the-art machinery to deliver high-quality, eco-friendly corrugated boxes. The demand for export-quality packaging is also rising as India strengthens its position in global trade, requiring packaging that meets international durability and safety standards.

Brazil: Agricultural Exports and E-Commerce Propel Corrugated Packaging Demand

Brazil’s corrugated packaging market is largely driven by its agricultural and food industries, where protective packaging for fruits, vegetables, and meat products is crucial for both domestic consumption and international exports. The expansion of e-commerce further fuels demand for durable, cost-effective packaging capable of withstanding long-distance transportation.

Strategic investments are being made to capture growth opportunities, with companies investing in new manufacturing facilities and technologies to produce a wider range of corrugated products. Innovations focus on lightweight, high-strength packaging solutions that reduce transportation costs while maintaining product safety, supporting Brazil’s role as a leading exporter of agricultural commodities.

Corrugated Packaging Market Report Scope

Corrugated Packaging market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$172.5 Billion

|

|

Market Size (2034)

|

$256.4 Billion

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Product Type (Boxes, Sheets, Pallets, Displays, Other Products), By Board Style (Single Face, Single Wall, Double Wall, Triple Wall), By Flute Type (A-Flute, B-Flute, C-Flute, E-Flute, F-Flute, Others), By End-Use Industry (Food & Beverages, E-commerce & Retail, Industrial, Home & Personal Care, Pharmaceuticals & Healthcare, Electronics, Automotive, Other Industries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

International Paper Company, WestRock Company, Smurfit Kappa Group plc, Mondi plc, Packaging Corporation of America, DS Smith plc, Oji Holdings Corporation, Rengo Co., Ltd., Saica Group, Shanying International Holdings Co., Ltd., BillerudKorsnäs AB, Georgia-Pacific LLC, Greif, Inc., Sealed Air Corporation, Hood Container Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Corrugated Packaging Market Segmentation

By Product Type

- Boxes

- Sheets

- Pallets

- Displays

- Other Products

By Board Style

- Single Face

- Single Wall

- Double Wall

- Triple Wall

By Flute Type

- A-Flute

- B-Flute

- C-Flute

- E-Flute

- F-Flute

- Others

By End-Use Industry

- Food & Beverages

- E-commerce & Retail

- Industrial

- Home & Personal Care

- Pharmaceuticals & Healthcare

- Electronics

- Automotive

- Other Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Corrugated Packaging Market

- International Paper Company

- WestRock Company

- Smurfit Kappa Group plc

- Mondi plc

- Packaging Corporation of America

- DS Smith plc

- Oji Holdings Corporation

- Rengo Co., Ltd.

- Saica Group

- Shanying International Holdings Co., Ltd.

- BillerudKorsnäs AB

- Georgia-Pacific LLC

- Greif, Inc.

- Sealed Air Corporation

- Hood Container Corporation

*List not Exhaustive

Research Coverage

This report investigates the global corrugated packaging market, highlighting breakthroughs in digital printing, AI-driven structural optimization, and sustainable material integration that are redefining the packaging landscape. USDAnalytics’ analysis reviews key technological advancements, market expansion strategies, and competitive developments, including high-value initiatives in e-commerce, food, and industrial logistics sectors. This report is an essential resource for packaging engineers, supply chain managers, sustainability leaders, and procurement professionals seeking actionable insights into design innovation, recyclability, and cost efficiency. By evaluating both historical trends (2021–2024) and future projections (2025–2034), it captures market dynamics, material innovations, digital transformation, and regulatory influences shaping corrugated packaging adoption worldwide. The analysis highlights market leadership strategies, competitive positioning, and the integration of smart technologies such as QR/NFC-enabled packaging, AI-driven logistics optimization, and recyclable coatings, offering comprehensive guidance for decision-making in an increasingly complex, sustainability-driven, and e-commerce-dominated environment.

Scope Highlights:

- Segmentation: By Product Type (Boxes, Sheets, Pallets, Displays, Other Products), By Board Style (Single Face, Single Wall, Double Wall, Triple Wall), By Flute Type (A-Flute, B-Flute, C-Flute, E-Flute, F-Flute, Others), By End-Use Industry (Food & Beverages, E-commerce & Retail, Industrial, Home & Personal Care, Pharmaceuticals & Healthcare, Electronics, Automotive, Other Industries)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Timeframe: Historic data from 2021 to 2024; forecast data from 2025 to 2034

- Companies Covered: Analysis/profiles of 15+ leading companies including International Paper Company, WestRock Company, Smurfit Kappa Group plc, Mondi plc, Packaging Corporation of America, DS Smith plc, Oji Holdings Corporation, and others

Methodology

The research methodology combines both primary and secondary approaches to provide a robust analysis of the corrugated packaging market. Primary research involved interviews with industry experts, packaging engineers, and executives from top manufacturers to capture firsthand insights on technological innovations, adoption trends, and regional demand patterns. Secondary research incorporated company reports, regulatory filings, trade publications, and proprietary databases to assess market size, growth drivers, competitive dynamics, and historical trends. Quantitative models were employed to forecast market growth from 2025 to 2034, integrating macroeconomic indicators, material cost fluctuations, and supply chain developments. Special emphasis was placed on emerging digital printing technologies, AI-assisted design optimization, and sustainable material adoption, ensuring that the methodology reflects both operational realities and strategic innovation. USDAnalytics cross-validated findings through triangulation to ensure accuracy and reliability, delivering a comprehensive and industry-ready market assessment for professionals.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.