Protective Packaging Market Overview: Growth Driven by E-commerce and Sustainability

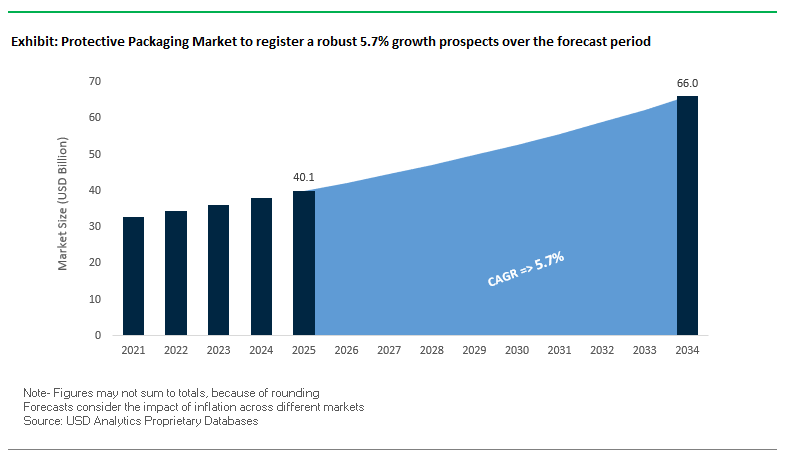

The Global Protective Packaging Market is valued at $40.1 billion in 2025 and is projected to reach $66 billion by 2034, expanding at a steady CAGR of 5.7%. The industry’s expansion is largely attributed to the rapid rise of e-commerce, where protective packaging plays a vital role in ensuring safe and damage-free product deliveries. From electronics and automotive components to pharmaceuticals and consumer goods, the need for lightweight, durable, and sustainable protective packaging solutions continues to grow.

Plastics, paper-based, and foam materials dominate the market, but sustainability pressures are reshaping material selection. A Jabil survey found that 68% of packaging decision-makers publicly committed to sustainable packaging, indicating a strong push toward recyclable and biodegradable alternatives. Meanwhile, automation in warehouses and fulfillment centers is driving demand for packaging with uniform dimensions and light weight, making it easier to integrate with high-speed systems.

For industry professionals, the protective packaging sector answers critical questions about supply chain resilience, regulatory compliance, and cost-efficiency. Companies must evaluate not just product protection, but also carbon footprint reduction and customer experience in an increasingly sustainability-driven world.

Key Insights for Professionals

- E-commerce growth is the single largest driver of protective packaging adoption, especially for fragile electronics and consumer goods.

- Lightweighting innovations such as honeycomb polypropylene and recyclable paper-based cushioning reduce both transport costs and emissions.

- Automation compatibility makes protective packaging critical for warehouse efficiency and scalable e-commerce operations.

- Sustainability commitments are reshaping material preferences, shifting reliance away from petroleum-based plastics.

Market Analysis: Recent Industry Developments in Protective Packaging

The protective packaging market is undergoing strategic acquisitions, product launches, and sustainability-focused investments, reflecting the industry’s evolution. In August 2025, Nefab Group acquired FARUSA Emballage, a Nordic company specializing in heavy-duty corrugated solutions, strengthening its footprint in engineered protective packaging. That same month, Sealed Air Corporation introduced its Instapak smart foam, tailored for e-commerce fulfillment, showcasing the industry’s move toward on-demand, automated packaging solutions.

In July 2025, Sonoco invested $30 million to expand its adhesives and sealants capacity, supporting demand for flexible and protective packaging laminates. Also in July, Mondi Group enhanced its paper-based protective portfolio with investments in recyclable air cushioning and bubble wrap alternatives, signaling a strong commitment to paper-driven sustainability. Earlier in January 2025, Ranpak unveiled three automated packaging systems in Europe, including its DecisionTower with FillPak Trident, which integrates machine vision for precise void-fill automation.

Consolidation remains a major theme. Smurfit WestRock in January 2025 launched an all-paper pallet stretch wrap, emphasizing recyclability in supply chain packaging. Meanwhile, Amcor’s $8.4 billion acquisition of Berry Global in November 2024 reshaped the competitive landscape, creating a new plastics and healthcare packaging leader. Despite a reported decline in M&A activity in late 2024, the occurrence of megadeals highlighted the industry’s ongoing appetite for consolidation and global leadership in packaging.

Protective Packaging Market: Trends and Growth Opportunities Driving Transformation

Corporate Shift Toward Plant-Based and Recyclable Cushioning Materials

One of the most influential trends in the global protective packaging market is the corporate transition away from traditional foams such as expanded polystyrene (EPS) toward plant-based and recyclable cushioning materials. This shift is not just symbolic but is backed by public ESG commitments, investor scrutiny, and regulatory requirements targeting virgin plastic reduction. Major brands like Unilever have pledged to cut virgin plastic use by 30% by 2026, and these targets directly influence protective packaging portfolios.

Innovation in material science is fueling this transition. Companies such as Cruz Foam are scaling “earth-digestible” alternatives made from upcycled food waste that biodegrade within eight weeks under industrial composting conditions, making them a credible replacement for EPS. Collaborations between packaging manufacturers and end-users further accelerate the movement. For instance, Mondi’s partnership with a photo booth company resulted in corrugated paperboard solutions that eliminated EPS, reduced costs, and improved logistics efficiency. Beyond compliance, these plant-based alternatives enhance corporate reputations, as sustainable packaging is increasingly tied to consumer loyalty and brand value.

Strategic Acquisitions to Dominate Automated Protective Packaging Systems

A second defining trend is the wave of strategic acquisitions in the automated protective packaging systems segment. Leading players are no longer depending solely on organic growth but are actively buying firms that specialize in automation to strengthen their market position. The acquisition of Automated Packaging Systems (APS) by Sealed Air Corporation for $510 million in 2019 exemplifies this move. Sealed Air gained not only bagging system expertise but also access to sustainable films under the EarthAware® brand, positioning itself as a provider of integrated material-plus-equipment solutions.

The driver behind these acquisitions is the booming e-commerce sector, where right-sized, automated packaging is critical to reducing labor costs, material usage, and fulfillment inefficiencies. Automation allows for rapid creation of custom packages for diverse product sizes, minimizing void fill and waste. By vertically integrating material production with automation technology, companies like Sealed Air are positioned to dominate e-commerce packaging operations, offering holistic solutions that competitors relying on standalone materials cannot match.

Development of High-Performance Fiber-Based Materials for Heavy-Duty Applications

A significant opportunity exists to expand into fiber-based protective packaging engineered for heavy-duty and fragile applications, directly competing with plastic foams. The challenge is to match the durability and cushioning of EPS while ensuring recyclability and cost-efficiency. Corporate demand is evident: PepsiCo has issued open challenges for biodegradable coatings suitable for fiber-based beverage packaging, signaling an industry-wide appetite for innovation in fiber-based barriers and cushions.

Government and foundation grants are accelerating R&D in this space. For example, Ecovative Design, a pioneer in mycelium-based packaging, secured National Science Foundation (NSF) funding to scale its agricultural waste–based alternatives. Academic research is also contributing to technical breakthroughs, with studies exploring sustainable fiber composites for use in demanding sectors like automotive dunnage, where protective strength is non-negotiable. As fiber-based materials evolve to meet both durability and recyclability requirements, they represent one of the most disruptive opportunities for the protective packaging market.

Expansion of Reusable Protective Packaging Systems for B2B Supply Chains

The growth of circular economy mandates is creating fertile ground for reusable protective packaging systems in B2B logistics. Automotive, electronics, and food distribution sectors are already deploying closed-loop systems of reusable containers and dunnage, demonstrating clear cost and waste reduction benefits. These models significantly cut single-use waste and deliver more durable, consistent protection over time.

While upfront investment is higher, lifecycle economics favor reuse. Studies from B2B packaging specialists highlight that companies adopting reusable assets achieve long-term reductions in material costs, disposal fees, and product damage during transit. The integration of IoT-enabled sensors and RFID chips into these systems further enhances value by providing real-time data on container location and condition. This not only improves inventory management but also ensures accountability in asset return and maintenance. As industries increasingly align with sustainability goals, scalable reusable protective packaging systems will become a mainstream solution for high-value B2B supply chains.

Competitive Landscape: Leading Companies in the Global Protective Packaging Industry

The protective packaging market features global leaders and specialized players that differentiate themselves through sustainable innovation, automation integration, and material science expertise.

Smurfit WestRock: Driving Circular Paper-Based Protective Packaging

Smurfit WestRock, formed by the merger of Smurfit Kappa and WestRock, leads in corrugated and paper-based protective packaging. Its solutions include pallet components, dividers, inserts, and wraps designed for lightweight strength and durability. The company leverages vertical integration from sustainable forestry to packaging design, ensuring high-quality, recyclable products aligned with circular economy principles.

Sealed Air Corporation: Expanding Smart Foam and Cushioning Systems

Sealed Air is renowned for its Bubble Wrap® brand and a wide portfolio of air pillows and foam systems. In August 2025, it launched Instapak smart foam, advancing packaging automation for e-commerce. With its digitally driven sustainability vision, Sealed Air aims to deliver zero-waste solutions while maintaining reliable product protection across global supply chains.

Pregis Corporation: Innovating with Smart and Recyclable Mailers

Pregis provides air, paper, and foam-based protective solutions, including surface protection films and flexible packaging. Its EverTec™ cushioned mailer is an all-paper, curbside recyclable solution that addresses e-commerce sustainability needs. With its Pregis IQ Innovation Center, the company tests and designs tailored protective packaging systems, making it a key innovator in circular packaging solutions.

Nefab Group: Strengthening Global Reach through Acquisitions

Nefab combines engineering expertise with multi-material protective packaging, offering crates, collars, and fiber-based pallet solutions. Its EdgePak Collar exemplifies its focus on lightweight, recyclable innovations. In August 2025, Nefab’s acquisition of FARUSA Emballage expanded its Nordic presence, aligning with its strategy to scale sustainable industrial packaging worldwide.

Ranpak Holdings Corp.: Automating Paper-Based Protective Solutions

Ranpak is a global leader in paper-based cushioning, wrapping, and void-fill systems. In January 2025, it launched three automated solutions, including the DecisionTower with FillPak Trident, enhancing e-commerce efficiency with machine vision. Its PadPak, FillPak, and WrapPak systems demonstrate its core focus on renewable and recyclable paper packaging that reduces environmental impact.

Sonoco Products Company: Enhancing Cold Chain and Protective Solutions

Sonoco offers rigid paper and flexible protective packaging with strong expertise in temperature-assured solutions via its ThermoSafe division. Its packaging ensures safe delivery of pharmaceuticals, vaccines, and biologics. In January 2024, Sonoco sold its Protective Solutions business to Black Diamond Capital, streamlining operations to focus on its core packaging strengths and ISC Labs® testing capabilities.

Protective Packaging Market Share Insights

Flexible Protective Packaging Leads Market Share by Product Type

Flexible protective packaging holds the largest share at 40%, reflecting its role as the backbone of modern e-commerce logistics. Air pillows, bubble wrap, and padded mailers dominate because they provide lightweight protection, reduce dimensional shipping costs, and adapt easily to a wide variety of product shapes. For online retailers and 3PLs operating in high-volume fulfillment centers, flexible formats integrate seamlessly with automated packing lines, ensuring both speed and cost efficiency. Their widespread adoption illustrates how the e-commerce boom has fundamentally reshaped the protective packaging market, shifting emphasis from heavy-duty protection to optimized space efficiency and parcel shipping performance.

E-Commerce Dominates Protective Packaging Market Share by End-Use

E-commerce accounts for 35% of demand, establishing itself as the single largest and most influential end-use industry for protective packaging. This segment is uniquely powerful because its requirements dictate packaging innovation, from the surge in curbside-recyclable paper-based mailers to lightweight flexible options that reduce shipping costs. Leading retailers like Amazon have set strict sustainability mandates, forcing upstream suppliers to redesign packaging formats. As a result, e-commerce not only generates massive volume but also serves as the testing ground for next-generation protective packaging materials and systems that eventually cascade into other industries.

United States: E-commerce Growth and Sustainable Protective Packaging Driving Market Expansion

The U.S. protective packaging market is witnessing robust growth driven by the rapid rise of e-commerce and a strong domestic manufacturing base, particularly in consumer electronics and automotive sectors. The demand for high-performance protective materials has surged to ensure safe product delivery, while innovations are focusing on eco-friendly and recyclable solutions. Companies like Pregis are emphasizing sustainable protective packaging for healthcare, electronics, and scientific instrument manufacturing, reflecting the growing commitment to environmental responsibility.

Regulatory developments, including Extended Producer Responsibility (EPR) laws in states such as Maine, Washington, and Oregon, are compelling manufacturers to adopt recyclable and sustainable packaging solutions. Additionally, the U.S. Environmental Protection Agency (EPA) promotes the use of water-soluble and non-hazardous materials, which is accelerating the shift from traditional plastic foams to paper-based protective alternatives. Technological advancements such as automated packaging systems and robotic box filling, sealing, and labeling solutions are optimizing material usage while increasing production efficiency, making U.S. protective packaging both innovative and environmentally responsible.

European Union: Regulatory Mandates and Advanced Materials Shaping Protective Packaging

The EU protective packaging market is strongly influenced by stringent regulatory frameworks such as the Packaging and Packaging Waste Regulation (PPWR 2025), which aims to reduce packaging waste and prohibits certain single-use plastic items, including miniature shampoo bottles and fresh produce packaging. Denmark’s upcoming Extended Producer Responsibility (EPR) mandate, effective October 2025, will further drive manufacturers toward recyclable and sustainable protective solutions.

European companies are leveraging these regulations to innovate in high-value industries, including automotive, electronics, and pharmaceuticals, where compact, robust, and reliable protective packaging is critical. For instance, DS Smith’s global R&D and Innovation Centre, 'R8', in the UK focuses on sustainable material research, smart packaging for supply chain tracking, and reusable fiber-based packaging, accelerating the development of next-generation protective solutions. These initiatives highlight Europe’s commitment to a circular economy while fostering technological advancement in protective packaging.

China: E-commerce Boom and Green Technology Boost Protective Packaging Market

China’s protective packaging market is growing rapidly, fueled by exponential e-commerce expansion through platforms like Alibaba and JD.com. Government initiatives under the 14th Five-Year Plan aim to control plastic pollution and promote the remanufacturing industry, encouraging sustainable packaging practices and environmentally responsible production.

Strict quality control requirements for exports have increased demand for high-performance protective materials, including bubble wrap, foam packaging, and molded pulp solutions. The government also incentivizes the adoption of green technology through tax benefits, driving manufacturers to integrate sustainable practices into their protective packaging operations. These efforts collectively reinforce China’s position as a rapidly advancing market for eco-friendly, high-performance protective packaging solutions.

India: Regulatory Reforms and Industrial Growth Accelerating Protective Packaging Adoption

India’s protective packaging market is being reshaped by regulatory reforms such as the Plastic Waste Management (Amendment) Rules, 2024, which emphasize Extended Producer Responsibility (EPR) for producers, importers, and brand owners. The ban on certain single-use plastic items since 2022 is creating a high demand for water-soluble, biodegradable, and zero-waste alternatives, driving innovation in protective packaging materials.

The country is also positioning itself as a hub for Outsourced Semiconductor Assembly and Test (OSAT) services, with multiple projects approved under the India Semiconductor Mission (ISM) that require advanced protective packaging for sensitive components. The government’s implementation of the National Single Window System and development of plug-and-play semiconductor parks are attracting investment and accelerating project approvals. These combined efforts are fostering the growth of sustainable, high-quality, and technologically advanced protective packaging solutions in India.

Protective Packaging Market Report Scope

Protective Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$40.1 Billion

|

|

Market Size (2034)

|

$66 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Product Type (Flexible Protective Packaging, Foam Protective Packaging, Rigid Protective Packaging, Paper-based Protective Packaging, Other Products), By Material (Foam Plastics, Paper & Paperboard, Plastics, Other Materials), By Function (Cushioning, Void-fill, Blocking & Bracing, Insulation, Surface Protection, Wrapping), By End-Use Industry (E-commerce, Electronics, Food & Beverages, Automotive & Transportation, Pharmaceuticals & Healthcare, Industrial Goods)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sealed Air Corporation, Pregis LLC, Smurfit Kappa Group Plc, DS Smith Plc, International Paper Company, WestRock Company, Sonoco Products Company, Amcor plc, Huhtamaki Oyj, Storopack Hans Reichenecker GmbH, Ranpak Holdings Corp., Pregis LLC, Pro-Pac Packaging Limited, Uflex Ltd., Berry Global Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Protective Packaging Market Segmentation

By Product Type

- Flexible Protective Packaging

- Foam Protective Packaging

- Rigid Protective Packaging

- Paper-based Protective Packaging

- Other Products

By Material

- Foam Plastics

- Paper & Paperboard

- Plastics

- Other Materials

By Function

- Cushioning

- Void-fill

- Blocking & Bracing

- Insulation

- Surface Protection

- Wrapping

By End-Use Industry

- E-commerce

- Electronics

- Food & Beverages

- Automotive & Transportation

- Pharmaceuticals & Healthcare

- Industrial Goods

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Protective Packaging Market

- Sealed Air Corporation

- Pregis LLC

- Smurfit Kappa Group Plc

- DS Smith Plc

- International Paper Company

- WestRock Company

- Sonoco Products Company

- Amcor plc

- Huhtamaki Oyj

- Storopack Hans Reichenecker GmbH

- Ranpak Holdings Corp.

- Pregis LLC

- Pro-Pac Packaging Limited

- Uflex Ltd.

- Berry Global Inc.

* List Not Exhaustive

Methodology

USDAnalytics has conducted a detailed and systematic analysis of the global Protective Packaging Market, integrating both primary and secondary research to provide actionable insights for industry professionals. Our methodology combines interviews with key stakeholders in packaging manufacturing, e-commerce fulfillment, and logistics operations alongside an in-depth review of corporate reports, mergers and acquisitions, regulatory frameworks, and sustainability initiatives. Market sizing and forecast projections are derived from historical trends, innovations in flexible, foam, rigid, and paper-based protective packaging, and the increasing adoption of plant-based, recyclable, and automated packaging systems. Segmentation covers product type, material, function, and end-use industry, with regional analysis of major markets including the U.S., EU, China, and India. Competitive intelligence evaluates leading companies such as Sealed Air, Pregis, Smurfit WestRock, DS Smith, and Sonoco, highlighting strategic investments, material innovations, and automated packaging advancements. By synthesizing regulatory drivers, technological developments, and sustainability trends, USDAnalytics delivers a precise, professional overview of market dynamics, growth opportunities, and strategic imperatives for decision-makers.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.