Packaging Laminates Market Size, Growth Forecast, and Key Insights

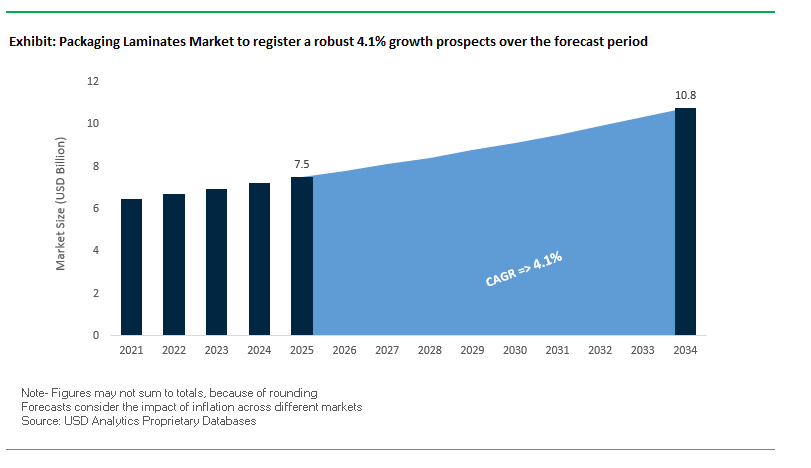

The Global Packaging Laminates Market is projected to grow from $7.5 billion in 2025 to $10.8 billion by 2034, representing a CAGR of 4.1%. Packaging laminates, composed of multiple layers of materials such as plastic, paper, and aluminum foil, are essential for protecting contents, extending shelf life, and enhancing brand appeal across industries including food, beverage, pharmaceuticals, and consumer goods. Laminates not only provide functional protection but also serve as a strategic tool for branding, consumer engagement, and regulatory compliance.

Key Insights for Industry Stakeholders

- High-Performance Barrier Laminates: Rising demand in food, beverage, and pharmaceutical packaging for multi-layer structures that protect against moisture, oxygen, and light, reducing spoilage and supporting food waste reduction initiatives.

- Sustainable and Mono-Material Solutions: Shift toward single-polymer laminates like all-PE or all-PP, simplifying recycling processes and meeting plastic circularity regulations.

- Enhanced Consumer Engagement: Advanced laminates enable digital printing, matte and velvet finishes, and haptic effects, delivering memorable unboxing experiences, especially in e-commerce-driven markets.

- Smart Packaging and Traceability: Integration of QR codes and digital interfaces on laminates for real-time product tracking, authenticity verification, and direct brand-to-consumer interaction.

- Regulatory and Environmental Compliance: Laminates support eco-friendly and legally compliant packaging, aligning with global sustainability standards.

The market’s growth is driven by the demand for sustainable, high-barrier, and digitally integrated laminates, making it a vital component of modern packaging innovation.

Recent Developments Shaping the Packaging Laminates Market

The Global Packaging Laminates Industry is evolving rapidly, driven by strategic acquisitions, technological innovation, and sustainability initiatives. In August 2025, industry reports highlighted the growing adoption of intelligent packaging solutions, including coatings with embedded sensing elements to ensure optimal product conditions during transit and storage.

In July 2025, the all-stock combination of Amcor and Berry Global Group officially closed, establishing a market leader in flexible laminates and rigid containers. Earlier in May 2025, Mondi successfully commissioned a €400 million paper machine at its Štětí mill, reinforcing its position in sustainable paper and packaging. April 2025 marked the completion of International Paper’s $9.9 billion acquisition of DS Smith, expanding its corrugated and laminated paper packaging offerings.

Significant consolidation continued with Arkema acquiring Dow’s flexible packaging laminating adhesives business in December 2024, and the Smurfit Kappa–WestRock merger in November 2024, creating a new packaging giant. In October 2024, Mondi collaborated with Nestlé to develop fully recyclable pet food pouches, advancing circular packaging initiatives. Earlier, in April 2024, Parkside launched Recoflex, a range of recyclable paper-based flexible packaging laminates with strong barrier performance and heat sealability.

Trends and Opportunities Reshaping the Packaging Laminates Market

Accelerated Shift to Monomaterial Polyolefin-Based Laminates for Recyclability

The packaging laminates market is undergoing a transformative shift toward monomaterial polyolefin-based laminates as brand owners and regulators demand higher recyclability. Leading FMCG players are setting the pace Nestlé has committed to making 100% of its packaging recyclable or reusable by 2025, with product pouches transitioning from multi-material to monomaterial structures. This shift signals that converters must rapidly adapt to supply recyclable laminates as a non-negotiable market requirement. Collaboration across the value chain is driving innovation: SABIC and Unilever’s Knorr project, which used certified circular polypropylene from SABIC’s TRUCIRCLE portfolio, highlights how resin producers, converters, and brand owners are working together to commercialize scalable solutions. A key technical breakthrough is the development of Machine Direction Orientation (MDO) techniques combined with thin EVOH layers, allowing monomaterial PE or PP laminates to match the barrier performance of conventional PET/PE laminates. Commercial rollouts are already underway Amcor’s AmLite line of fully recyclable all-PE pouches for snacks and pet food illustrates how the industry is moving from R&D to mainstream adoption. This shift positions monomaterial laminates as the next growth standard for sustainable flexible packaging.

Adoption of High-Barrier, Recyclable Coatings to Replace Aluminum and Metallization

The drive to replace aluminum foil and metallized films in laminates is accelerating, with high-barrier recyclable coatings emerging as a viable alternative. Transparent coatings such as aluminum oxide (AlOx) and silicon oxide (SiOx) are enabling brands to maintain strong oxygen and moisture barriers while improving recyclability and product visibility essential for consumer appeal in food and beverage packaging. Investments in coating technologies are expanding, with companies like UFlex deploying vacuum deposition systems for large-scale production of transparent barrier films. Academic research supports this trajectory, showing that dual-EVOH architectures and optimized polyamide skins can pair with AlOx or SiOx coatings to create recyclable structures capable of withstanding high-temperature retort processes. This overcomes a key limitation of early recyclable laminates that failed under sterilization. As these technologies mature, they are creating a direct replacement for legacy aluminum-based structures, helping converters deliver packaging that balances sustainability, barrier performance, and consumer convenience.

Development of Bio-Based and Compostable Laminates for Flexible Packaging

One of the most significant opportunities lies in the development of bio-based and compostable laminates for applications where recycling is not feasible, such as coffee pods, condiment sachets, and single-serve packaging. Companies are commercializing certified solutions Swiss Pac’s “Plantmade” laminate is already available as a home-compostable alternative, providing a clear end-of-life pathway for single-use formats. The innovation frontier is focused on performance parity with plastics, with academic studies in Polymers highlighting PLA blends and renewable composites that achieve improved mechanical strength, moisture resistance, and barrier properties. Certification frameworks such as EN 13432 and ASTM D 6866 are essential to build brand-owner confidence in compostability claims. The adoption of products like FKuR’s Bio-Flex® compostable granules, certified under international standards, is reinforcing credibility. These laminates are particularly effective in regions with industrial composting infrastructure, diverting food-soiled flexible packaging from landfills and closing the loop by converting it into compost. This makes compostable laminates a high-potential niche within the sustainable packaging ecosystem.

Integration of Digital Watermarking into Laminate Structures for Intelligent Sortation

The integration of digital watermarking technology into laminate structures presents a breakthrough opportunity for intelligent recycling. Unlike traditional NIR sorting, digital watermarks enable precise polymer-specific and application-specific separation, creating high-purity PCR streams for flexible films. Industrial-scale trials under the HolyGrail 2.0 initiative in 2024 validated the technology’s ability to detect and sort flexible PE and PP laminates at high efficiency, even when contaminated with food residue. This breakthrough paves the way for regulatory adoption within the EU’s PPWR framework, ensuring verifiable compliance with recycled content mandates. Technology partnerships are scaling commercialization Siemens is providing digital automation and plant control systems that integrate with watermark-based sortation, laying the groundwork for smart recycling plants. The economic value is compelling: the creation of food-grade PCR streams with higher purity commands premium pricing, justifying capital investments in sorting infrastructure. For brand owners under EPR obligations, digitally watermarked laminates represent both a compliance mechanism and a competitive sustainability differentiator.

Competitive Landscape: Key Players Driving Innovation in Packaging Laminates

The Global Packaging Laminates Market is shaped by leading players leveraging materials science, vertical integration, and sustainability strategies to deliver high-performance solutions for diverse packaging applications.

Amcor PLC: Leading Sustainable and High-Barrier Packaging Laminates

Amcor is a global leader in flexible and rigid packaging laminates. In July 2025, it completed an all-stock combination with Berry Global Group, establishing a dominant presence in consumer packaging. Amcor also introduced mono-material PE flexible films with high oxygen and moisture barriers for enhanced recyclability. Its AmLite Recyclable film is a metal-free, high-barrier solution suitable for various applications, including food and medical packaging. Amcor’s strategy emphasizes sustainable innovation, circular economy alignment, and scalability to meet evolving global packaging requirements.

Mondi Group: Pioneering Eco-Friendly Laminates with Integrated Manufacturing

Mondi specializes in paper and plastic-based laminates with a focus on sustainability and innovation. In May 2025, Mondi launched a €400 million paper machine at its Štětí mill, strengthening its core laminate capabilities. In October 2024, the company collaborated with Nestlé to produce fully recyclable pet food pouches. Mondi offers high-barrier films for food packaging and paper-based laminates for industrial use, emphasizing eco-friendly, recyclable, and compostable solutions. Its vertical integration ensures control over raw materials and manufacturing processes.

Sealed Air Corporation: Innovating Protective and Food Packaging Laminates

Sealed Air focuses on protective and food packaging laminates. In March 2025, the company introduced AI-enabled automation lines for custom flexible packaging, while reporting strong performance in Q2 2025 and announcing Kristen Actis-Grande as CFO. Its Cryovac® films provide superior barrier properties, extending the shelf life of perishable goods, and its Recycabel® films promote recyclability. Sealed Air aims to optimize the global food supply chain, investing in innovative, sustainable, and e-commerce-ready packaging solutions.

Uflex Limited: Advancing Sustainable and High-Performance Laminates

Uflex, an Indian multinational, is recognized for its vertically integrated operations spanning laminate manufacturing, packaging machinery, inks, and adhesives. Recent innovations include Asclepius™ BOPET film with up to 100% PCR polymer content and films with enhanced barrier properties. Uflex offers BOPET, BOPP, and CPP laminates, along with specialty metallized and holographic options, and flexible plastic recycling machinery. The company emphasizes circular economy initiatives and sustainable packaging solutions across its integrated business model.

Huhtamaki Oyj: Expanding Sustainable Food Packaging Laminates

Huhtamaki provides a wide range of flexible, paper-based, and high-performance laminates, with a focus on food safety and sustainability. In November 2024, it launched paper-based flexible packaging for confectionery in Europe, promoting recyclability. Its flexible laminates protect products, extend shelf life, and enhance brand appeal. Huhtamaki aims for fully recyclable, compostable, or reusable products by 2030, investing in new materials and technologies to lead sustainable food packaging innovation.

Packaging Laminates Market Share Insights, 2025-2034

BOPP Films Hold the Largest Market Share by Film Type in the Packaging Laminates Industry

Biaxially oriented polypropylene (BOPP) dominates the packaging laminates market with a 45% share, making it the backbone material for flexible packaging. Its superior clarity, moisture barrier, tensile strength, and cost-effectiveness make it indispensable for snack foods, confectionery, and dry goods packaging. BOPP films can be metallized, coated, or laminated with other substrates, enabling applications that range from high-barrier pouches to transparent wrappers with excellent shelf appeal. Polyethylene (PE) plays a critical role as the sealant layer across nearly all laminate structures, ensuring hermetic seals and product safety. Meanwhile, polyethylene terephthalate (PET) and polyamide (PA) serve as high-performance specialty films, favored in retort pouches, frozen foods, and heavy-duty applications where puncture resistance and oxygen barrier properties are paramount. The dominance of BOPP reflects its balance of functionality, adaptability, and affordability, making it the material of choice for the world’s largest flexible packaging applications.

Food & Beverage Industry Continues to Dominate Market Share by End-Use in the Packaging Laminates Industry

The food and beverage sector accounts for 65% of the packaging laminates market, establishing itself as the largest and most influential end-use industry. Flexible laminates are essential for extending shelf-life, ensuring freshness, and reducing food waste, particularly in snacks, frozen foods, dairy products, and ready-to-eat meals. The global shift away from rigid containers toward pouches, sachets, and flexible wraps has accelerated this dominance, with laminates enabling features such as resealability, lightweighting, and portion control. Food-grade laminates often incorporate metallized layers or transparent high-barrier coatings (AlOx, SiOx) to deliver oxygen and moisture protection while maintaining visibility. Pharmaceutical and healthcare applications represent the second-largest share, driven by sterile and high-barrier requirements, while personal care and cosmetics demand laminates for premium aesthetics combined with barrier protection. Industrial and automotive uses remain smaller but value-driven, emphasizing toughness and puncture resistance. Ultimately, the food and beverage sector drives both volume demand and material innovation, dictating the pace and direction of the global laminates industry.

United States Packaging Laminates Market Driven by GS1 Sunrise 2027 and EPR Regulations

The United States packaging laminates market is undergoing structural change with the GS1 Sunrise 2027 Project, which mandates a transition to 2D barcodes. This shift is driving greater adoption of RFID-enabled packaging, requiring laminate structures that can integrate with data-rich labeling. Additionally, state-level Extended Producer Responsibility (EPR) laws in Maine, Maryland, and Washington are accelerating the move toward recyclable substrates and laminates with higher post-consumer recycled (PCR) content. Together, these regulatory measures are forcing manufacturers to redesign laminates to support traceability, recyclability, and compliance.

On the innovation front, U.S. companies are prioritizing mono-material laminates that replicate the barrier properties of multi-material structures while improving recyclability. In December 2024, Dow finalized the sale of its flexible packaging laminating adhesives business to Arkema, reflecting a broader industry trend of strategic portfolio optimization and focus on sustainable technologies. Demand remains strong across e-commerce and consumer packaged goods (CPG), where lightweight, durable laminates are critical for shipping safety, while the food sector increasingly requires high-barrier laminates to maintain freshness, prevent spoilage, and extend shelf life.

Germany Packaging Laminates Market Strengthened by EU PPWR and Circular Economy Leadership

Germany’s packaging laminates market is regulated by the EU Packaging and Packaging Waste Regulation (PPWR) and the updated German Packaging Act (VerpackG) 2025, which set ambitious recyclability and reuse standards. These rules are reshaping laminate design, requiring companies to adopt easily recyclable structures and minimize environmental contamination from adhesives and inks.

Technological leadership is evident in Germany’s role as a hub for advanced laminate innovation. The German Packaging Institute (dvi) spotlighted sustainable materials at its 2025 Packaging Awards, emphasizing eco-friendly laminates and protective designs. Backed by the country’s strong recycling infrastructure, Germany is leveraging mechanical recycling technologies to generate high-quality PCR feedstock that supports a closed-loop system. Key applications dominate in food, beverages, and cosmetics, where laminates play a dual role in extending product shelf life and meeting stringent EU environmental compliance requirements.

China Packaging Laminates Market Accelerated by Dual-Carbon Targets and Smart Manufacturing

The packaging laminates market in China is expanding rapidly under the government’s dual-carbon targets, with carbon peaking set for 2030 and neutrality for 2060. Regulations introduced in June 2025 for the express delivery sector require degradable and reusable packaging, significantly increasing demand for eco-friendly laminates. These mandates are reshaping material sourcing, pushing manufacturers toward recyclable and biodegradable laminated solutions.

Chinese producers are investing heavily in automation, AI, and smart manufacturing systems to improve production quality and efficiency. The government is also developing digital regulatory platforms to ensure traceability and safety in food packaging. Corporate players are scaling operations to meet surging demand: Amcor’s state-of-the-art Huizhou facility features intelligent production systems that deliver high-quality laminates for food and e-commerce packaging. With consumer goods, electronics, and e-commerce sectors fueling growth, China is emerging as a global leader in high-volume, compliant, and sustainable packaging laminates.

India Packaging Laminates Market Supported by EPR Rules and Flexible Packaging Expansion

India’s packaging laminates market is shaped by government initiatives such as Make in India and the Production Linked Incentive (PLI) scheme, which drive domestic manufacturing investment. EPR regulations requiring 30% recycled content in rigid plastics by April 2025 are directly influencing laminate structures and encouraging development of recyclable and circular packaging solutions.

Corporate innovation is evident in Brilliant Polymers’ expansion into solvent-free adhesives, with five new product launches reinforcing sustainable lamination processes. The company is projecting revenues of INR 850–900 crore in FY2025-26 and aims to exceed INR 1,000 crore by FY2026-27 with further expansion of its Amarnath plant. Such investments highlight India’s growing role in regional supply chains for advanced flexible packaging. Demand is concentrated in the on-the-go food and beverage sector, where laminates provide strong shelf appeal, barrier protection, and durability for juices, sports drinks, RTD teas, and coffees, alongside growing demand from online retail packaging.

Japan Packaging Laminates Market Evolving Under Positive List Rules and Bio-Based Materials

Japan’s packaging laminates market is being reshaped by new food-contact material regulations, with the “positive list” system effective from June 1, 2025. This regulatory shift mandates compliance with approved synthetic materials, influencing laminate formulations for food packaging applications. As a result, companies are prioritizing safe, recyclable, and bio-based laminate designs that align with food safety and sustainability requirements.

Innovation is being led by firms like Stora Enso, which has partnered with Japanese companies to develop paper-based barrier laminates capable of protecting fragile and temperature-sensitive products. These advances align with Japan’s commitment to cut greenhouse gas emissions by 46% by 2030 and achieve net zero by 2050. Applications are especially strong in ready-to-drink tea, coffee, and snack packaging, where Japanese consumers prioritize lightweight, durable, and aesthetically pleasing laminates that maintain product integrity while supporting sustainability goals.

Brazil Packaging Laminates Market Driven by ANVISA Food Safety Rules and PNRS Recycling Mandates

Brazil’s packaging laminates market is strongly influenced by the National Solid Waste Policy (PNRS) and regulations from the National Health Surveillance Agency (Anvisa). New rules introduced in 2025 place shared responsibility on manufacturers and consumers for end-of-life packaging management, driving adoption of laminates compatible with recycling systems. Anvisa also ensures that packaging laminates used in food and beverage sectors comply with sanitary and safety standards, especially for canned goods and processed foods.

Corporate activity reflects the country’s pivot toward sustainable solutions. Klabin, in partnership with Optima and Soulpack, launched a fully recyclable paper-based diaper packaging in 2025, demonstrating the use of bio-based materials like corn starch and sugarcane bagasse in laminate development. The food and beverage industry remains Brazil’s largest consumer of laminates, where high-barrier packaging is essential to maintaining product safety and extending shelf life. With recycling mandates tightening, demand for eco-friendly laminates is expected to rise sharply.

Packaging Laminates Market Report Scope

Packaging Laminates Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.5 Billion

|

|

Market Size (2034)

|

$10.8 Billion

|

|

Market Growth Rate

|

4.1%

|

|

Segments

|

By Material Type (Paper & Paperboard, Plastic, Aluminum Foil, Others), By Film Type (BOPP, PET, PE, PA), By Application (Flexible Packaging, Rigid Packaging), By End-Use Industry (Food & Beverage, Healthcare & Pharmaceutical, Personal Care & Cosmetics, Industrial, Automotive)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Constantia Flexibles Group, Berry Global Inc., Huhtamaki Oyj, Tekni-Plex, Inc., UFlex Ltd., ProAmpac LLC, Jindal Poly Films Limited, Sealed Air Corporation, Coveris Holdings S.A., Transcontinental Inc., Winpak Ltd., Klabin S.A., Toray Industries, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Packaging Laminates Market Segmentation

By Material Type

- Paper & Paperboard

- Plastic

- Aluminum Foil

- Others

By Film Type

By Application

- Flexible Packaging

- Rigid Packaging

By End-Use Industry

- Food & Beverage

- Healthcare & Pharmaceutical

- Personal Care & Cosmetics

- Industrial

- Automotive

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Packaging Laminates Market

- Amcor plc

- Mondi Group

- Constantia Flexibles Group

- Berry Global Inc.

- Huhtamaki Oyj

- Tekni-Plex, Inc.

- UFlex Ltd.

- ProAmpac LLC

- Jindal Poly Films Limited

- Sealed Air Corporation

- Coveris Holdings S.A.

- Transcontinental Inc.

- Winpak Ltd.

- Klabin S.A.

- Toray Industries, Inc.

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive, multi-step research methodology to deliver actionable insights into the Global Packaging Laminates Market. Our approach integrates primary and secondary research to ensure accuracy, reliability, and relevance for industry professionals. Primary research includes in-depth interviews with key stakeholders such as packaging manufacturers, brand owners, converters, suppliers, and regulatory authorities to capture emerging trends, innovations, and compliance practices. Secondary research involves analyzing company reports, trade publications, patents, regulatory filings, and industry journals to validate market dynamics and competitive developments. Quantitative techniques, including market sizing, growth projection, and CAGR calculations from 2025 to 2034, are applied to assess market value and forecast trends. Our methodology also evaluates material innovations such as BOPP, PE, PET, PA films, mono-material laminates, bio-based and compostable laminates, and high-barrier coatings, along with technological advancements in smart packaging, digital watermarking, and traceability. Regional insights across the United States, Europe, China, India, Japan, and Brazil are incorporated to understand regulatory impacts, sustainability initiatives, and market-specific adoption patterns. By synthesizing competitive intelligence, material science developments, regulatory frameworks, and end-use requirements, USDAnalytics provides a comprehensive market outlook that supports strategic planning, investment decisions, and innovation roadmaps for packaging industry professionals.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.