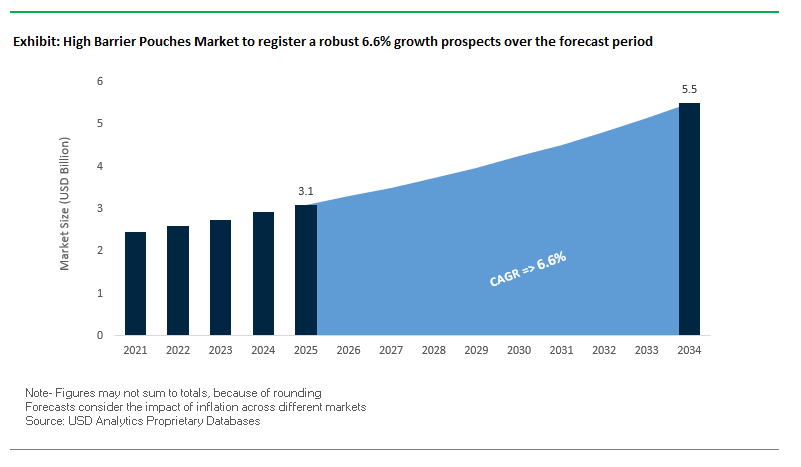

High Barrier Pouches Market Overview (2025–2034): $3.1B to $5.5B at 6.6% CAGR, mono-material shift and e-commerce durability

The Global High Barrier Pouches market supplies multi-layer, flexible packs engineered to block oxygen, moisture and UV safeguarding freshness, flavor, actives and aroma while cutting weight, cube and logistics cost versus rigid formats. Growth is anchored in convenience foods/ready meals, sterile and shelf-stable pharma, and D2C/e-commerce where puncture resistance and seal integrity are critical. The strategic pivot is toward recycle-ready mono-material pouch structures that maintain barrier without aluminum or mixed polymers, enabling participation in polyolefin or PP recycling streams. Smart-pack integrations (QR/NFC/TTI) are expanding for traceability, anti-counterfeiting and consumer engagement.

Key Insights for Industry Professionals:

- Demand engines: convenience & RTE meals, pet food, nutraceuticals, and sterile pharma dosing.

- Sustainability: rapid adoption of mono-PE / mono-PP, paper-based and aluminum-free high-barrier laminates.

- Performance: retortable barrier, abuse resistance for parcel networks, ESR (e-commerce shock resistance).

- Digitalization: smart packaging (QR/NFC/RFID/TTI) for freshness and provenance.

- Design-to-recycle: solvent-free laminating, downgauging, metallized mono-material films replacing foils.

Market Analysis: 2025 momentum in recyclable films, paper-based stand-up formats and smart-pack adoption

From January–September 2025, the high barrier pouches landscape advanced on three fronts bio-based materials, paper-based high-barrier designs, and scale investment while brand owners accelerated traceability.

In January 2025, Saica Flex introduced metallized mono-material pouches, raising aesthetics and barrier while keeping recyclability. February 2025, Mondi launched the re/cycle SpoutedPouch as a tub replacement in paints, extending recyclable pouching beyond food. March 2025, Mondi + Proquimia debuted paper-based stand-up pouches for dishwashing tabs, proving paper substrates can meet barrier, machinability and shelf impact needs. April 2025, Parkside unveiled Recoflex recyclable, paper-based materials for pouches/bags/lidding, broadening substrate choice for barrier applications.

Investment and consolidation accelerated in mid-year. June 2025 reporting highlighted surging smart packaging demand (QR, NFC, RFID) to enhance traceability and engagement. July 2025, the Amcor–Berry all-stock combination closed, creating a flexibles heavyweight with expanded film, converting and recycle-ready innovation scale. August 2025, Coveris completed a €9.5M upgrade at Halle to lift capacity and quality; DNP signaled medical focus by exhibiting sustainable healthcare packaging at Medical Fair Thailand. By September 2025, LyondellBasell–Futamura–Iwatani announced bio-based film development for cosmetics, underscoring the trajectory toward renewable, circular, high-barrier solutions.

Transformative Trends and High-Value Opportunities in the High Barrier Pouches Market

Strategic Shift to Monomaterial Polyolefin Structures for Recyclability

The high barrier pouches market is witnessing a decisive movement toward all-polyethylene (PE) and all-polypropylene (PP) pouch structures, replacing traditional multi-material, non-recyclable laminates. This trend is driven by brand sustainability commitments and the implementation of Extended Producer Responsibility (EPR) regulations, which require packaging to be recyclable by design. Mono-material pouches maintain the critical oxygen, moisture, and aroma barrier properties essential for food, beverage, and pharmaceutical applications, while ensuring compatibility with existing polyolefin recycling streams. Leading packaging manufacturers are developing advanced co-extrusion techniques and barrier coatings that allow high performance without compromising recyclability. This strategic pivot reshapes the flexible packaging supply chain, fostering collaboration between resin producers, film converters, and brand owners to achieve both regulatory compliance and sustainability goals.

Integration of Transparent High-Barrier EVOH Layers for Product Visibility

Consumer demand for transparent packaging combined with superior barrier protection is driving innovation in EVOH (ethylene vinyl alcohol)-integrated pouches. Thin EVOH layers, coextruded with polyolefin sealant and protective layers, replace traditional opaque aluminum foil laminates while maintaining exceptional oxygen and aroma barrier properties. This approach enables product visibility, enhancing consumer trust and engagement, particularly in premium snacks, coffee, and ready-to-eat foods. Manufacturers are optimizing layer thickness, orientation, and co-extrusion techniques to achieve the ideal balance of transparency and barrier performance. Adoption of EVOH-based pouches allows brands to differentiate on shelf appeal while adhering to sustainability mandates, offering a clear growth avenue in flexible packaging innovation.

Development of Bio-Based and Compostable High-Barrier Solutions

A significant growth opportunity exists in bio-based and certified compostable high-barrier pouches, particularly for organic, natural, and premium products. Polymers such as PLA, PHA, and cellulose derivatives can be engineered to provide oxygen, moisture, and aroma barriers comparable to conventional plastics while supporting industrial composting standards. This innovation allows brands to target eco-conscious consumers who demonstrate a willingness to pay a premium for sustainable packaging. R&D efforts are focused on enhancing mechanical performance, barrier efficiency, and shelf-life stability, creating products that meet both functional and environmental expectations. The adoption of bio-based pouches fosters collaboration between raw material suppliers, film manufacturers, and packaging converters, contributing to a circular economy and a lower environmental footprint.

Incorporation of Digital Watermarking for Intelligent Recycling

The integration of digital watermarking technologies, such as the HolyGrail 2.0 initiative, offers a transformative opportunity to address the sorting challenges in flexible packaging recycling. These watermarks enable automated detection and precise separation of pouches at recycling facilities, generating clean material streams suitable for high-quality recycling. This technology not only enhances the circular economy potential of pouches but also positions brand owners as leaders in sustainable packaging innovation. Adoption of digital watermarking requires collaboration across the value chain, including designers, converters, and recycling operators, to ensure encoding, detection, and sorting systems are fully optimized. By integrating intelligent packaging technologies, manufacturers can significantly improve recyclability rates and meet evolving regulatory and consumer expectations.

Competitive Landscape: leaders scaling recyclable, retort-capable and e-commerce-ready barrier pouches

The market features global film majors and agile converters advancing recycle-ready mono-materials, aluminum-free high-barrier, and automation-ready pouch formats across food, pet care, personal care and pharma.

Amcor drives mono-material, aluminum-free barrier pouching at global scale

Amcor pairs worldwide converting with flagship AmLite Recyclable (metal-free, high-barrier) and AmPrima® recycle-ready ranges. In July 2025 it closed the Berry combination, expanding film and rigid integration. Amcor also introduced recycle-ready high-barrier laminates for medical devices with up to 70% lower carbon footprint vs traditional aluminum laminates, aligning barrier with LCA wins. Strategy centers on making all packaging recyclable or reusable by 2025, prioritizing mono-material designs without sacrificing shelf life or machinability.

Huhtamaki scales blueloop™ and ESR performance in pet food and pharma

Huhtamaki offers retort pouches for ambient foods and pharma barrier formats against moisture/light, under its blueloop™ sustainable portfolio. The firm launched high-performance films designed for circularity and provides ESR (e-commerce shock resistance) options for large-format pet food pouches. Its 2030 strategy commits to all products being recyclable/compostable/reusable, supported by global footprint and co-development with CPGs.

ProAmpac advances curbside-recyclable and retortable mono-PP pouches

ProAmpac’s ProActive Recyclable RP-1000HB delivers high oxygen/grease resistance with curbside recyclability; RT-4000 (patented mono-PP) withstands aggressive retort conditions. The company pushes structural innovation (e.g., ProActive Recyclable FibreSculpt, >90% fiber, launched Feb 2024) while maintaining stiffness and sealability for HFFS/stand-up applications. Strategy: sustainability without performance trade-offs, tuned to brand owner line speeds and print quality.

Sealed Air (CRYOVAC®) extends shelf life with ultra-thin, display-ready barriers

Sealed Air’s CRYOVAC® portfolio covers high-barrier pouches and Barrier Display Film (BDF) crystal-clear packs balancing O2/aroma protection with fog control for meats, poultry and prepared foods. The company’s downgauged, ultra-thin films reduce resin use while retaining abuse resistance and hermeticity. Beyond materials, Sealed Air integrates equipment and automation, optimizing throughput, seal reliability and labor efficiency for retailers and processors.

Mondi accelerates paper-based and mono-material recyclable pouch systems

Mondi’s innovation cadence spans mono-material spouted and shaped pouches designed for recycling, and re/cycle RetortPouch replacing aluminum with a high-barrier film architecture. In February 2025, it launched paper-based stand-up pouches with Proquimia; July 2025 saw PaperPlus Bag Advanced a moisture-protective paper bag using up to 60% less plastic vs conventional films. Under MAP2030, Mondi designs packaging “sustainable by design”, marrying barrier, machinability and end-of-life.

High Barrier Pouches Market Share Insights

Polyethylene Leads Market Share by Material in High Barrier Pouches Industry

Polyethylene (PE) holds the largest share of the high barrier pouches market at 30% in 2025, reflecting its indispensable role as the sealing layer in almost every laminate structure. PE provides excellent heat-sealability, flexibility, and moisture barrier properties, making it the foundational inner layer across both food and non-food applications. PET, with 25% share, dominates as the structural outer layer, offering strength, clarity, and moderate gas barrier properties, while polypropylene (PP) complements as a cost-effective material with strong performance in clarity and durability. EVOH, though used in smaller proportions, plays the pivotal role of providing ultra-high oxygen barrier performance, particularly in premium pouches for coffee, meats, and dried snacks. Polyamide (PA) adds puncture and abrasion resistance, vital for large-format pet food pouches and heavy-duty applications. Aluminum foil remains the ultimate barrier for oxygen, moisture, and light, though its use is limited by cost, lack of microwaveability, and sustainability concerns. Together, this mix demonstrates how PE ensures sealing performance, PET and PP provide structure, EVOH enables ultra-barrier functionality, and PA and aluminum deliver durability and absolute protection in specialized niches.

Food and Beverages Dominate Market Share by Application in High Barrier Pouches Industry

The food and beverages sector accounts for 75% of high barrier pouch demand in 2025, underscoring its critical role in global packaging innovation. Coffee, snacks, dairy, sauces, meats, and ready-to-eat meals increasingly depend on barrier pouches to ensure freshness, safety, and consumer convenience, with multi-layer laminates designed for precise oxygen, moisture, and light protection. Pet food represents the second-largest segment at 15%, where large, durable pouches with puncture resistance and robust seals are essential to contain fats and oils while maintaining flavor stability. Pharmaceuticals and healthcare, though smaller in share, are a premium, compliance-driven niche, requiring sterile barrier protection for medical devices, moisture-sensitive drugs, and diagnostic kits, often with regulatory features such as desiccants or tamper-evident seals. Cosmetics and personal care represent a specialized but growing segment, leveraging barrier pouches for samples, single-use skincare, and formulations requiring protection from oxidation and UV exposure. This segmentation shows how food and beverages dominate volume, pet food drives durability-focused adoption, and pharmaceuticals and cosmetics expand premium, specification-driven demand.

United States High Barrier Pouches Market Driven by Sustainability and Technological Innovation

The U.S. high barrier pouches market is significantly shaped by a fragmented regulatory environment, including California's SB-54 Extended Producer Responsibility (EPR) law, mandating a 25% reduction in plastic use by 2032. This legislation encourages the shift toward recyclable and mono-material pouch designs, promoting sustainability across the packaging sector. Technological advancements are accelerating innovation, exemplified by ProAmpac's RP-1000HB, a curbside-recyclable high-barrier paper packaging, and the integration of smart features such as QR codes for traceability and consumer engagement.

Corporate investments are pivotal, with Amcor’s planned acquisition of Berry Global Group enhancing R&D capabilities and expanding sustainable production. High barrier pouches see strong demand across food and beverage, pharmaceuticals, and personal care sectors, fueled by e-commerce growth and consumer preference for on-the-go, resealable packaging. The industry emphasizes eco-friendly materials, including bio-based films and recyclable paperboard, aligning with regulatory pressures and evolving consumer demand for sustainable packaging solutions.

Germany High Barrier Pouches Market Leverages Circular Economy and Regulatory Compliance

Germany’s high barrier pouches market operates under strict regulatory frameworks, including the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025. The regulation mandates fully recyclable or reusable packaging by 2030, while phasing out certain chemicals and setting recycled content requirements. Technological innovation is central, with SÜDPACK and SN Maschinenbau unveiling advanced, sustainable stand-up pouches, showcasing the country’s focus on high-quality, eco-friendly packaging solutions.

Germany’s well-established Packaging Act (VerpackG) drives leadership in the circular economy by incentivizing recycling-friendly designs through modulated fees. The market is particularly strong in food, beverage, and medical sectors, with a robust manufacturing base and high export activity for specialty foods and pharmaceuticals, reinforcing demand for reliable, high-performance high barrier pouches.

China High Barrier Pouches Market Expands with Domestic Manufacturing and Green Initiatives

China’s high barrier pouches market is being transformed by government initiatives targeting sustainability, including the “dual carbon” goal and the March 2024 Action Plan promoting industrial upgrades and sustainable materials. Regulatory reforms such as GB/T 31268, effective November 2024, limit excessive packaging, particularly for e-commerce goods, directly influencing pouch design and material usage.

Technological advancements are accelerating production efficiency, driven by AI and “5G plus industrial internet” integration. Corporate investments, like Dow’s collaboration with Mengniu to launch a mono-material PE yogurt pouch in August 2023, emphasize recyclability and circular economy practices. A strong focus on domestic manufacturing is enabling local companies to substitute imported technology and meet rising demand for high-quality, sustainable packaging across food and beverage segments.

India High Barrier Pouches Market Gaining Momentum from Circular Economy Policies

India’s high barrier pouches market is benefiting from circular economy initiatives, including the draft Environment Protection (Extended Producer Responsibility for Packaging) Rules, 2024. Technological adoption is increasing, with automated printing systems and specialized pouch manufacturing enabling growth in frozen foods, snacks, and personal care packaging. UFlex is pioneering aluminum-free laminates and bio-based films, highlighting the market’s strong sustainability push.

Corporate investments are growing to meet rising domestic demand, supported by the Make in India initiative, which encourages local manufacturing and technological advancement. Key applications include food processing, personal care, and e-commerce packaging, with consumers increasingly preferring sustainable, high-performance pouches that enhance convenience and product freshness.

Japan High Barrier Pouches Market Focuses on High-Performance and Functional Packaging

Japan’s high barrier pouches market is anchored in advanced precision manufacturing and next-generation production ecosystems. The Plastic Resource Circulation Act, effective April 2022, promotes sustainable material usage and limits single-use plastics, driving adoption of eco-friendly packaging solutions. High-performance and value-added pouches are gaining prominence, with innovations such as IoT-enabled films, easy-open tear notches, and resealable closures addressing aging populations and single-person households.

Companies like Toppan Inc. are pioneering recycled BOPP films for mass production, while ZACROS has established a strong presence in the domestic market with Doypacks for cosmetic refill products. Japan’s focus on specialized, high-quality pouches reflects a combination of regulatory compliance, technological innovation, and market demand for functional packaging solutions.

Brazil High Barrier Pouches Market Driven by Sustainable Packaging and Strategic Collaborations

Brazil’s high barrier pouches market is shaped by government initiatives promoting sustainable waste management, including amendments to the National Solid Waste Policy. Partnerships like iFood and XPRIZE’s $20 million global competition for flexible, biodegradable packaging are influencing innovation in high barrier pouches.

Technological advancements are creating premium and digital packaging solutions that extend shelf life while maintaining product quality. High barrier pouches are particularly in demand in the food and beverage sector, especially for processed and ready-to-eat foods. Strategic corporate collaborations, such as SIG Group’s partnership with DPA Brazil to introduce spouted pouches for yogurt, reinforce Brazil’s expanding presence in sustainable, high-performance packaging solutions.

High Barrier Pouches Market Report Scope

High Barrier Pouches Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.1 Billion

|

|

Market Size (2034)

|

$5.5 Billion

|

|

Market Growth Rate

|

6.6%

|

|

Segments

|

By Material (PE, PP, PET, EVOH, PA, Aluminum), By Pouch Type (Stand-up Pouches, Spouted Pouches, Retort Pouches, Flat Pouches), By Application (Food & Beverages, Pharmaceuticals & Healthcare, Pet Food, Cosmetics & Personal Care), By Barrier Type (Oxygen Barrier, Moisture Barrier, UV Barrier)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Huhtamaki Oyj, Berry Global Group, Inc., Sealed Air Corporation, Sonoco Products Company, ProAmpac, Constantia Flexibles Group, Klöckner Pentaplast, Toppan Inc., UFlex Ltd., Jindal Poly Films Ltd., Winpak Ltd., Novolex Holdings, LLC, TC Transcontinental

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

High Barrier Pouches Market Segmentation

By Material

- PE

- PP

- PET

- EVOH

- PA

- Aluminum

By Pouch Type

- Stand-up Pouches

- Spouted Pouches

- Retort Pouches

- Flat Pouches

By Application

- Food & Beverages

- Pharmaceuticals & Healthcare

- Pet Food

- Cosmetics & Personal Care

By Barrier Type

- Oxygen Barrier

- Moisture Barrier

- UV Barrier

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in High Barrier Pouches Market

- Amcor plc

- Mondi Group

- Huhtamaki Oyj

- Berry Global Group, Inc.

- Sealed Air Corporation

- Sonoco Products Company

- ProAmpac

- Constantia Flexibles Group

- Klöckner Pentaplast

- Toppan Inc.

- UFlex Ltd.

- Jindal Poly Films Ltd.

- Winpak Ltd.

- Novolex Holdings, LLC

- TC Transcontinental

* List Not Exhaustive

Methodology

USDAnalytics conducted an in-depth, multi-faceted research approach to deliver a comprehensive analysis of the Global High Barrier Pouches Market. Our methodology integrated primary research through interviews and consultations with key stakeholders, including packaging manufacturers, converters, brand owners, and end-users across food & beverages, pharmaceuticals, pet food, and personal care sectors. Secondary research included analysis of company reports, government regulations, patent filings, industry publications, and sustainability initiatives. Market sizing and forecasting were derived from historical data, trend extrapolation, and econometric modeling, with a focus on mono-material PE/PP pouches, bio-based films, paper-based high-barrier solutions, and smart-pack innovations (QR/NFC/TTI). Regional assessments covered key markets such as the United States, Germany, China, India, Japan, and Brazil, analyzing regulatory frameworks, technological adoption, circular economy practices, and corporate investments. Competitive analysis examined major players, including Amcor, Huhtamaki, ProAmpac, Sealed Air, Mondi, and UFlex, highlighting strategic mergers, sustainable innovation, and scale-up capabilities. This approach ensures industry professionals receive actionable insights on market growth, material innovations, recyclability trends, and high-value opportunities in the high barrier pouches landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.