Sustainability and Food Preservation Push Barrier Paper Market to USD 7.7 Billion by 2034

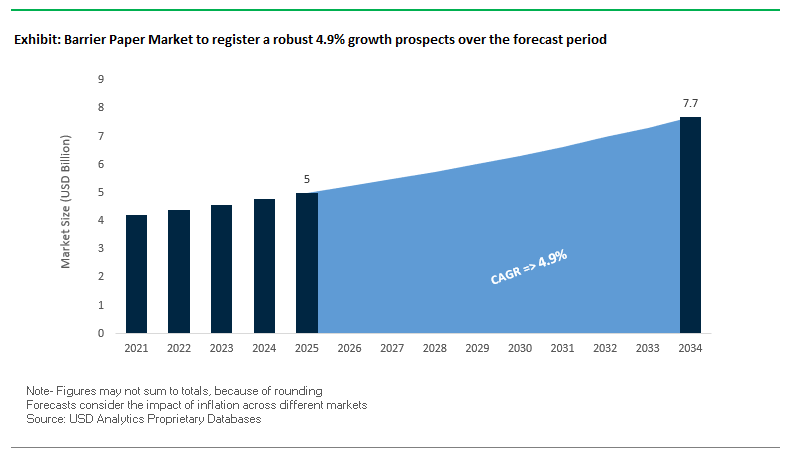

The global barrier paper market is projected to expand from USD 5 billion in 2025 to USD 7.7 billion by 2034, growing at a CAGR of 4.9%. This growth is strongly tied to the demand for sustainable alternatives to plastics, particularly in food, beverage, and consumer goods packaging. Barrier papers provide reliable protection against moisture, grease, and oxygen, making them essential for preserving food freshness while supporting brand commitments to sustainability.

Adoption is also driven by recyclability. Unlike multi-material laminates, barrier papers can often be processed within existing paper recycling streams, giving them a significant advantage for companies focused on circular economy strategies. Moreover, the versatility of barrier papers whether used in flexible pouches, wrapping materials, or corrugated applications ensures a broad end-use base across snacks, bakery products, pet food, and personal care packaging. As regulatory pressure mounts to reduce single-use plastics, barrier paper is emerging as a critical solution bridging performance with environmental compliance.

Key Insights for Industry Professionals

- Plastic substitution: Barrier papers are replacing multi-layer laminates and rigid plastics.

- Food freshness: Moisture- and oxygen-blocking properties extend shelf life.

- Circular economy fit: Compatibility with paper recycling systems boosts adoption.

- Wide applicability: Used across food, pet care, and consumer goods packaging.

Acquisitions, Conversions, and Next-generation Barrier Papers Redefine the Market

The barrier paper industry is undergoing major consolidation, facility upgrades, and product launches. In August 2025, Mondi ramped up production of its FunctionalBarrier Paper Ultimate to meet surging demand for plastic-free solutions, reinforcing its position as a global supplier of recyclable high-barrier papers. That same month, Smurfit WestRock debuted on the New York and London exchanges following its merger, expanding its footprint in corrugated and paper-based barrier solutions.

M&A reshaped the sector in July 2025 when International Paper acquired DS Smith, creating a new powerhouse in paper-based packaging. Also in July, Sappi North America began delivering products from its USD 500 million paper machine conversion, producing high-performance paperboard grades with barrier properties, particularly for frozen foods and beverages. In June 2025, Mondi expanded its sustainable portfolio with the re/cycle PaperPlus Bag Advanced, reducing reliance on plastics for humidity-sensitive goods.

Earlier innovations have also fueled the market. TOPPAN (March 2024) introduced its GL-SP mono-material barrier film in India, based on a paper substrate, while Metsä Board (October 2024) launched recyclable frozen food barrier paperboard. Meanwhile, Smurfit Kappa (November 2023) advanced in liquid packaging through its acquisition of Artemis Ltd. in Bulgaria.

Key Trends and High-Impact Opportunities Driving the Barrier Paper Market

Development of High-Performance, Fluorochemical-Free Barrier Coatings

A transformative trend in the barrier paper market is the accelerated shift away from per- and polyfluoroalkyl substances (PFAS) in coatings toward bio-based and polymer-based alternatives. Regulatory pressure, particularly from the EU and North American markets, combined with rising consumer demand for safer and sustainable packaging, is driving this shift. Specialty chemical companies such as Kemira are spearheading innovation with solutions like FennoGuard™ dispersion barrier coatings, providing oil, grease, and moisture resistance without PFAS. Start-ups such as Earthodic have raised significant capital $6 million in seed funding to scale bio-based lignin coatings, underscoring the commercial and environmental viability of these alternatives. Certifications from FDA and BfR, as seen with Archroma's Cartaseal® OGB F10, validate these fluorochemical-free solutions for food-contact applications. The transition to sustainable coatings not only addresses health and environmental concerns but also improves the recyclability of barrier papers, reducing complexity in the recycling stream and enabling circular economy adoption. This shift positions high-performance, PFAS-free barrier coatings as a cornerstone for next-generation paper-based packaging.

Vertical Integration and Strategic Partnerships for Fiber-Based Packaging Solutions

Leading paper producers are increasingly engaging in vertical integration and strategic collaborations to deliver ready-to-use, high-performing barrier paper solutions. Partnerships with chemical companies and packaging converters allow for the creation of integrated systems that simplify supply chains for brand owners while enhancing sustainability. A notable example is the collaboration between Tetra Pak and Lactogal, which successfully deployed ultra-thin, metallized barrier papers on 25 million packages, achieving food safety and shelf-life equivalence with foil-based cartons. Similarly, SIG’s partnership with PulPac to develop paper-based barrier closures reflects a long-term commitment to achieving up to 90% paper content in cartons by 2030. These partnerships enable plug-and-play solutions that reduce sourcing complexity, accelerate innovation cycles, and ensure consistent performance. By co-developing recyclable, repulpable, and heat-sealable materials that run efficiently on high-speed packaging lines, vertical integration is emerging as a key strategic enabler in the barrier paper market.

Penetration into the Fresh Produce Sector for Plastic-Free Flow Wraps

The rising demand for plastic-free fresh produce packaging presents a major growth opportunity for barrier papers. Advanced papers are being designed to balance moisture management, which allows produce to respire naturally, with the mechanical strength required for high-speed flow-wrap machinery. Companies like Sirane have commercialized solutions such as Earthfilm, a heat-sealable, plastic-free paper providing oil, grease, and moisture barriers suitable for apples, pears, and stone fruits. Research into fine-mesh inserts within the paper allows for controlled breathability, extending shelf life and reducing food waste. Retailers benefit from the tactile and visual appeal of paper packaging, reinforcing sustainability commitments and enhancing consumer perception. This sector not only addresses regulatory and consumer pressures to reduce plastics but also offers a tangible competitive advantage in grocery and fresh produce markets globally.

Development of Functional Barriers for Dry Industrial and Food Ingredients

Beyond consumer packaging, the industrial sector presents significant opportunities for high-performance barrier papers in multi-wall sacks used for products such as flour, sugar, cement, and chemicals. These applications demand high tensile and tear strength alongside moisture, aroma, and fat resistance. Mondi’s re/cycle PaperPlus Bag Advanced exemplifies innovation in this segment, cutting plastic use by up to 60% while offering full recyclability and robust protection for humidity-sensitive powders. Developing multi-layer, functional barrier papers capable of withstanding heavy loads and transportation stress is essential to meet industrial standards. Adoption is being driven by sustainability targets among industrial firms and the critical need to preserve product integrity. Case studies from global food and agriculture sectors highlight that this trend is expanding rapidly as companies seek to reduce their environmental footprint while maintaining performance, positioning functional barrier papers as a strategic growth area.

Global Leaders Compete with High-barrier, Recyclable, and Sustainable Paper Packaging Solutions

The competitive landscape of the barrier paper market is dominated by global players investing in R&D, acquisitions, and next-generation product launches to capture growing demand for eco-friendly, recyclable packaging.

Mondi Group: Scaling High-barrier Paper with FunctionalBarrier Paper Ultimate

Mondi has emerged as a leader in plastic-free paper-based packaging, expanding its FunctionalBarrier Paper Ultimate, which combines heat-sealability, high barrier performance, and recyclability. With full vertical integration, Mondi ensures quality and innovation across forestry, paper production, and conversion, positioning itself as a key partner for brands seeking sustainable packaging transformation.

Smurfit WestRock: Leveraging Global Merger to Expand Barrier Paper Portfolio

Formed by the August 2025 merger of Smurfit Kappa and WestRock, Smurfit WestRock now operates in 42 countries with vast corrugated and specialty paper capabilities. Its portfolio includes food-grade corrugated barrier solutions and recyclable packaging designed to meet evolving consumer and regulatory sustainability demands. The company’s global scale and innovation pipeline make it a central force in advancing barrier paper packaging adoption.

Billerud Aktiebolag: Innovating with ConFlex CoatBase Met for Recyclable Solutions

Billerud continues to lead in specialty paper innovations with its ConFlex CoatBase Met technology, which applies vacuum metallization to previously non-recyclable packaging, enabling improved recyclability. With a strong global R&D network and sustainability-driven strategy, Billerud positions itself as a first-mover in high-barrier recyclable papers, especially for food and hygiene markets.

Sappi Limited: Transforming Paper Machines to Expand Barrier Paperboard Production

In July 2025, Sappi North America completed a USD 500 million mill conversion, enabling large-scale production of high-performance paperboard with barrier properties. This investment signals Sappi’s strategic pivot from declining graphic paper markets toward packaging and specialty paper, reinforcing its role as a premium supplier to the frozen food and consumer goods sectors. Its global R&D and manufacturing footprint ensure consistent quality and innovation delivery.

Barrier Paper Market Share Insights

Grease Barrier Paper Leads Market Share by Barrier Type in the Barrier Paper Industry

Grease-resistant paper accounts for the largest 35% share of the barrier paper market, underscoring its critical role in fast food, bakery, and pet food packaging. Its dominance is directly tied to the global explosion of on-the-go food consumption, where packaging must withstand oils and fats without losing structural integrity. The technology often incorporates fluorine-free coatings or bio-based alternatives to comply with PFAS restrictions, aligning with regulatory mandates in Europe and North America. While moisture and oxygen barriers support dry foods and high-value preservation, grease barrier remains the highest-volume application due to its indispensability in quick-service restaurant (QSR) chains and mass-market packaged foods. This segment exemplifies how functional performance and regulatory compliance drive adoption.

Food & Beverages Industry Holds the Largest Market Share in Barrier Paper End-Use

The food and beverages sector dominates with 65% of demand, reinforcing its position as the undisputed driver of barrier paper adoption. This dominance is fueled by the dual push for sustainability and functionality: brands are replacing plastic-based coatings and laminates with recyclable and compostable barrier papers to meet EPR mandates and corporate sustainability goals. From frozen food cartons to bakery wraps, barrier paper enables brands to deliver grease, moisture, and aroma protection without compromising recyclability. Beyond food, industrial and pharmaceutical uses represent important niches, but the scale, frequency of use, and regulatory pressures in F&B cement its role as the anchor segment for barrier paper innovation and market growth.

United States Barrier Paper Market Driven by FDA, EPA, and E-Commerce Packaging Needs

The United States barrier paper market is strongly shaped by strict regulations from the U.S. Food and Drug Administration (FDA) on food-contact materials and oversight from the Environmental Protection Agency (EPA) for environmental compliance. These agencies are pushing manufacturers toward sustainable and safe alternatives to plastics, making recyclable barrier paper a preferred choice for packaging. Corporate initiatives highlight this shift companies like Pregis are expanding their recyclable paper packaging portfolio with solutions such as White EasyPack GeoTerra, while Mondi has ramped up production of its FunctionalBarrier Paper Ultimate to meet demand for high-performance recyclable materials. Technological advancements are another driver, with innovators developing bio-based and water-based barrier coatings that enhance resistance to oxygen, grease, and moisture without compromising recyclability.

The rapid growth of e-commerce is further fueling the adoption of barrier paper in the U.S. packaging industry. Companies are replacing traditional non-sustainable packaging with recyclable, durable solutions designed for shipping resilience. High-value applications in food and beverage such as coffee sticks, cereal bars, and dried foods benefit significantly from barrier paper’s shelf-life extending properties. Federal and state-level plastic reduction initiatives are accelerating innovation in recyclable packaging technologies, positioning the United States as a leader in adopting sustainable barrier paper for large-scale food and e-commerce applications.

Germany Barrier Paper Market Strengthened by EU PPWR and VerpackG Regulations

Germany’s barrier paper market operates under one of the most stringent frameworks in the world, shaped by the EU Packaging and Packaging Waste Regulation (PPWR), which mandates that all packaging must be recyclable or reusable by 2030. Complementing this, Germany’s Packaging Act (VerpackG) places responsibility for the entire packaging lifecycle on producers, pushing companies to design recyclable and circular-ready packaging materials. This leadership in circular economy practices has positioned Germany as a hub for sustainable barrier paper innovation.

Technological advancements are at the forefront, with companies like Sappi Europe launching high-barrier Guard Pro OHS and Guard Pro OMH papers at FachPack 2025. These mono-material papers are designed to replace multilayer foils and plastics while offering high moisture and oxygen barrier performance. The barrier paper market in Germany is especially strong in food and beverage, pharmaceutical, and hygiene applications, including snacks, dry foods, and flow wraps for ice cream and hygiene products. With significant investment in R&D and strategic partnerships, Germany is emerging as a center for sustainable packaging solutions that align with both EU mandates and consumer demand for eco-friendly alternatives.

China Barrier Paper Market Accelerated by Dual Carbon Goals and Domestic Substitution

China’s barrier paper market is undergoing a rapid transformation under the government’s “dual carbon” goal, which mandates a green shift in industrial production. Policies restricting non-degradable plastics are driving demand for paper-based alternatives, while the “Made in China 2025” plan boosts domestic production of high-value goods, including food and pharmaceutical packaging. Regulatory reforms from the State Administration for Market Regulation (SAMR) continue to update “GB” standards, aligning Chinese barrier paper with global food-contact and consumer protection standards.

Technological advancements are also shaping the market, with manufacturers deploying AI, automation, and “5G plus industrial internet” to optimize efficiency and improve flexible production capacity. A key trend is domestic substitution, with local companies scaling up to replace imported technology and serve booming demand from the food and beverage industry. China’s ban on imported waste paper has shifted focus toward domestic recycling and the production of high-quality virgin pulp critical for barrier paper manufacturing. With e-commerce and food packaging driving massive consumption, China’s barrier paper market is positioned to expand as both local and global brands seek cost-effective, recyclable, and high-barrier solutions for mass packaging needs.

India Barrier Paper Market Supported by Government Initiatives and Plastic Ban

The barrier paper market in India is propelled by national initiatives like “Make in India” and “Zero Effect Zero Defect,” which emphasize sustainable, high-quality domestic production. The Council of Scientific and Industrial Research (CSIR) has also launched the National Mission on Sustainable Packaging Solutions to develop recyclable materials and testing facilities, further accelerating market adoption. Regulatory oversight from the Food Safety and Standards Authority of India (FSSAI) and the Ministry of Environment, Forest, and Climate Change (MoEFCC) ensures barrier paper meets stringent food safety and sustainability requirements, making it an attractive substitute for plastic packaging.

Technological adoption is rising, with automated packaging systems, advanced barrier coatings, and customized solutions designed to protect food from oxygen and moisture. The government’s ban on single-use plastics has created significant opportunities for barrier paper in food processing, snacks, dairy, and ready-to-eat meals packaging. Corporate investments are also notable, with Huhtamaki establishing a recycling plant in Maharashtra as part of its CloseTheLoop initiative, strengthening India’s role in the circular economy. As India emerges as a major food processing hub with expanding exports, barrier paper is positioned as a critical sustainable packaging solution for both domestic and global markets.

Japan Barrier Paper Market Powered by Advanced Coatings, Smart Packaging, and Bioplastic Roadmap

Japan’s barrier paper market is driven by its leadership in advanced manufacturing and its bioplastic roadmap, which targets mass bioplastic adoption by 2030. Companies like Oji Holdings and Toppan are innovating barrier coatings that provide high-performance moisture resistance while maintaining recyclability. Regulatory updates from the Ministry of Health, Labour and Welfare (MHLW) continue to tighten requirements for food-contact packaging, pushing companies toward safer, more sustainable materials.

Sustainability and functionality are key trends, with barrier paper increasingly developed for specialized applications requiring high dimensional stability and resistance to deformation. Strategic collaborations are central to market growth Toppan and partners are advancing high-barrier coated papers that serve food, cosmetics, and pharmaceutical packaging. Japan’s focus on smart packaging, integrating sensors to track freshness and safety, is also creating opportunities for advanced barrier paper with multi-functional properties. With universities actively researching biopolymers and natural agents for packaging, Japan stands at the forefront of combining sustainability, innovation, and precision manufacturing in the global barrier paper industry.

Barrier Paper Market Report Scope

Barrier Paper Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5 Billion

|

|

Market Size (2034)

|

$7.7 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Material Type (Paper & Paperboard, Coatings, Laminations), By Barrier Type (Oxygen Barrier, Moisture Barrier, Grease Barrier, Aroma Barrier), By End-Use Industry (Food & Beverages, Pharmaceuticals & Medical, Cosmetics & Personal Care, Industrial & Building, Others), By Application (Wraps & Liners, Bags & Pouches, Labels, Cups & Bowls, Corrugated Boxes)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Smurfit Kappa Group, Mondi Group, DS Smith Plc, WestRock Company, International Paper Company, Nefab AB, Sonoco Products Company, Pregis LLC, Sealed Air Corporation, Huhtamäki Oyj, Menasha Corporation, Amcor plc, Greif, Inc., Sappi Limited, Ahlstrom-Munksjö

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Barrier Paper Market Segmentation

By Material Type

- Paper & Paperboard

- Coatings

- Laminations

By Barrier Type

- Oxygen Barrier

- Moisture Barrier

- Grease Barrier

- Aroma Barrier

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Medical

- Cosmetics & Personal Care

- Industrial & Building

- Others

By Application

- Wraps & Liners

- Bags & Pouches

- Labels

- Cups & Bowls

- Corrugated Boxes

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Barrier Paper Market

- Smurfit Kappa Group

- Mondi Group

- DS Smith Plc

- WestRock Company

- International Paper Company

- Nefab AB

- Sonoco Products Company

- Pregis LLC

- Sealed Air Corporation

- Huhtamäki Oyj

- Menasha Corporation

- Amcor plc

- Greif, Inc.

- Sappi Limited

- Ahlstrom-Munksjö

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive research methodology to analyze the global barrier paper market, combining primary and secondary sources to ensure high-quality, actionable insights. Primary research includes interviews with packaging manufacturers, chemical coating suppliers, converters, and end-users across food, beverage, pharmaceutical, and industrial sectors. Secondary research leverages corporate reports, regulatory publications, and trade journals to assess market trends, sustainability initiatives, and technological innovations. Market sizing and forecasts are calculated using proprietary quantitative models incorporating growth drivers such as PFAS-free coating adoption, mono-material paper solutions, recyclability, plastic substitution, and functional barrier performance for moisture, grease, and oxygen protection. Competitive landscape analysis evaluates mergers, acquisitions, capacity expansions, and product launches from global leaders such as Mondi, Smurfit WestRock, Billerud, and Sappi, while regional trends in the U.S., Germany, China, India, and Japan are factored in. Regulatory compliance including FDA, EU PPWR, VerpackG, MHLW, and local sustainability mandates is considered to determine adoption patterns, investment potential, and technological priorities. By triangulating verified data with expert insights, USDAnalytics provides industry professionals with precise, forward-looking intelligence on barrier paper opportunities, innovations, and market dynamics.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.