Market Overview: Growth Outlook and Key Industry Insights

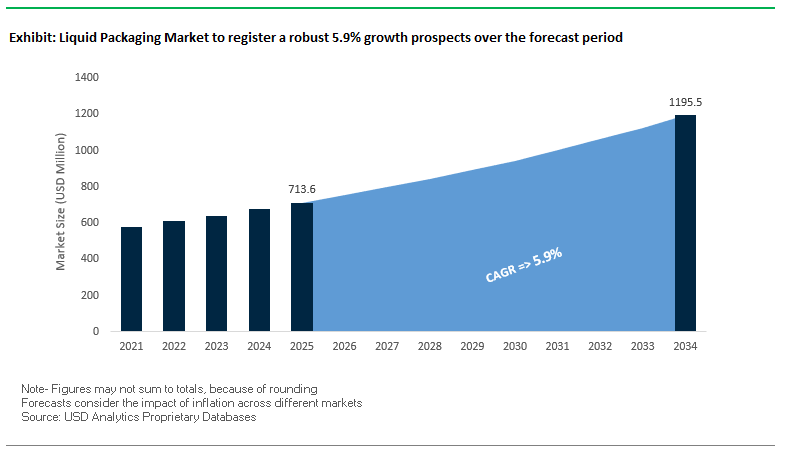

The global liquid packaging market is projected to expand from $713.6 million in 2025 to $1,195.4 million by 2034, growing at a steady CAGR of 5.9%. This growth trajectory underscores the sector’s strong reliance on aseptic packaging technologies, renewable material adoption, and e-commerce-driven logistics efficiency, while also being reshaped by the plant-based beverage boom. For industry professionals, this segment provides critical answers to where the next wave of innovation, cost-efficiency, and sustainability will come from in the packaging ecosystem.

Aseptic packaging continues to be the market cornerstone, with multi-layered formats—often including an aluminum foil barrier—extending the shelf life of milk, juices, and functional beverages for up to 18 months without refrigeration. At the same time, the industry is doubling down on recycling and renewable resource utilization, with responsibly managed forests supplying wood fiber for cartons and advanced recovery technologies enhancing recyclability rates.

The rise of e-commerce grocery platforms has further cemented the value proposition of lightweight, durable, and stackable liquid packaging formats, enabling reduced transportation costs and lower carbon emissions. Finally, the surging demand for plant-based beverages, including oat, almond, and soy milk, is fueling new product development, with specialized pouches and cartons designed to preserve integrity, nutrition, and flavor in these high-growth categories.

Key Insights for Industry Stakeholders

- Market projected to reach $1.19 billion by 2034, at 5.9% CAGR.

- Aseptic packaging enables up to 18 months of shelf life without refrigeration.

- Recycling innovation and renewable raw materials strengthen sustainability credentials.

- E-commerce logistics efficiency enhances cost savings and reduces emissions.

- Plant-based beverage demand drives specialized carton and pouch innovation.

Market Analysis: Recent Industry Developments

The liquid packaging market has experienced dynamic activity in 2024–2025, marked by strategic expansions, technological innovations, and M&A activity. In August 2025, Mondi Group unveiled its FunctionalBarrier Paper Ultimate at Fachpack 2025—a recyclable material offering ultra-high protection against oxygen and water vapor. This breakthrough underscores the trend toward high-barrier, paper-based alternatives to plastics and aluminum.

Investment-led expansion has been a defining theme. In July 2025, SIG committed $35 million to expand its Querétaro, Mexico plant, increasing capacity by 50% to serve North America. Similarly, Elopak enhanced its U.S. footprint in May 2025 by opening a carton converting facility in Little Rock, Arkansas, while SIG boosted its Asian presence in February 2025 with its first aseptic carton plant in India—both moves aligning with regional demand surges for sustainable packaging.

Circular economy initiatives are also reshaping the industry. In June 2025, Tetra Pak partnered with Fiat to transform recycled beverage cartons into car parts, showcasing the creation of high-value secondary markets for recyclables. Around the same time, Billerud launched ConFlex® HeatSeal (March 2025), a recyclable, heat-sealable paper designed to replace multi-layer plastics in liquid packaging. Meanwhile, in April 2025, Tetra Pak collaborated with a European juice brand to debut the Tetra Prisma® Aseptic 300 Edge carton with a tethered cap, enhancing renewable content while minimizing litter.

Strategic consolidation is reshaping competition. Sonoco’s acquisition of Eviosys in December 2024 positioned it as a stronger global leader in metal food and aerosol packaging, expanding its footprint beyond traditional cartons.

Transformative Trends and Strategic Opportunities in the Liquid Packaging Market

Strategic Pivot to Monomaterial Polyolefin Structures for Enhanced Recyclability

The liquid packaging market is undergoing a significant shift toward monomaterial polyolefin structures, including all-PE and all-PP pouches and films, driven by stringent Extended Producer Responsibility (EPR) regulations and corporate sustainability commitments. Major consumer goods companies are actively pursuing 100% recyclable packaging by 2030, prompting collaborations with packaging suppliers to develop high-performance monomaterial solutions. Innovations by companies like Amcor now enable monomaterial pouches to deliver equivalent shelf-life and product protection as traditional multi-laminate structures, ensuring no compromise on quality. Regulatory frameworks, particularly in the European Union, create strong financial incentives to adopt easily recyclable packaging, while compatibility with existing polyolefin recycling infrastructure ensures scalability and economic viability. This trend is central to achieving circularity in flexible packaging, making monomaterial polyolefin structures a strategic focus for sustainable packaging innovation.

Reshoring and Strategic Investment in North American Glass Container Production

Post-pandemic supply chain vulnerabilities and increasing consumer preference for premium and sustainable packaging have triggered a wave of investment in domestic glass production in North America. Major manufacturers are building new plants, such as a $123 million facility in Texas targeting spirits and ready-to-drink beverages, addressing both capacity needs and supply chain resilience. Consumers increasingly value glass for its premium feel, safety perception, and infinite recyclability—over 80% prefer glass for food and beverage products according to the Glass Packaging Institute. New facilities are designed to incorporate high percentages of recycled content, with some operations using up to 90% post-consumer recycled glass. This reshoring trend not only strengthens supply chain security but also aligns with sustainability commitments by increasing the use of recyclable and recycled materials.

Development of Integrated Digital Watermarking for Smart Sorting and Circularity

Digital watermarking represents a critical opportunity to improve recycling efficiency and traceability in liquid packaging. Through initiatives like HolyGrail 2.0, imperceptible codes embedded in packaging enable high-speed robotic sorting. Industrial trials in France demonstrated sorting efficiencies of 95.1% for two-pass sorting of watermarked materials, significantly outperforming traditional optical systems. Beyond recycling, watermarks enable granular sorting, including separation of food-grade from non-food-grade plastics, enhancing the quality and value of recycled streams. Additionally, digital watermarks provide a platform for brand engagement, allowing consumers to access product information and sustainability data via smartphones. The unique digital identity also supports traceability and anti-counterfeiting measures, helping brands monitor their products throughout the supply chain while reinforcing consumer trust.

Advanced Barrier Coatings for Paper-Based Bottles and Spouted Pouches

The shift toward paper-based alternatives to plastic and glass is driving demand for high-performance, recyclable barrier coatings. R&D is heavily focused on bio-based and recycled materials, including nanocellulose, starch, and polylactic acid (PLA), providing functional protection without compromising recyclability or compostability. Water-based dispersion coatings are replacing traditional extrusion methods, reducing plastic content and enabling easier fiber recovery in standard paper recycling mills. Specialized aqueous coatings, such as soy-protein-based barriers, are enhancing water vapor and grease resistance for liquid foods and fast-food applications. Companies like H.B. Fuller are actively commercializing these innovations, ensuring compliance with global food safety standards while enabling sustainable packaging solutions. These developments position paper-based bottles and spouted pouches as versatile, environmentally friendly alternatives in the rapidly evolving liquid packaging market.

Competitive Landscape: Leading Companies in the Liquid Packaging Industry

The global liquid packaging market is moderately consolidated, with innovation, recycling initiatives, and expansion strategies being the primary levers of competition. Key players include Tetra Pak, SIG Combibloc, Elopak, Mondi Group, and Smurfit Westrock, each driving growth with differentiated strengths.

Tetra Pak: Pioneering Sustainability and Digital Innovation

Tetra Pak remains the industry leader, offering aseptic and non-aseptic cartons for dairy, juices, and other beverages. In June 2025, it partnered with Fiat to repurpose recycled carton material into car parts, advancing circular value chains. The company is focused on achieving 100% renewable or recycled material packaging, supported by digital solutions for track-and-trace and consumer engagement. With flagship products like Tetra Rex Plant-based and Tetra Prisma Aseptic, Tetra Pak demonstrates unmatched integration across processing, packaging, and recycling.

SIG Combibloc: Scaling Across North America and Asia

SIG is rapidly expanding to capture high-growth regions. Its $35 million investment in Mexico (July 2025) and its new aseptic plant in India (February 2025) highlight its global strategy. SIG’s strength lies in end-to-end solutions for flexible packaging, offering products like combibloc EcoPlus and combibloc NNP, which minimize environmental impact. Its smarter factory systems enable quick design and volume changeovers, giving customers flexibility in a competitive market.

Elopak: Strengthening North American Market Reach

Elopak has prioritized North America with the Little Rock, Arkansas plant opening in May 2025, driving growth in its Americas segment, which posted 2.4% YoY revenue growth in Q2 2025. Its “Repackaging Tomorrow” strategy focuses on replacing plastic with fiber-based cartons, supported by innovations like the Pure-Fill platform. Known for its gable-top cartons for fresh milk and juices, Elopak emphasizes consumer convenience through a range of closures and openings.

Mondi Group: Advancing Barrier Paper Solutions

Mondi is recognized for pioneering paper-based barrier technologies. Its FunctionalBarrier Paper Ultimate, showcased in August 2025, provides a recyclable solution with high resistance to oxygen and moisture. Through its MAP2030 commitments, Mondi is targeting 100% reusable, recyclable, or compostable packaging by 2025. With a vertically integrated model from forestry to finished packaging, Mondi maintains strong supply chain control, ensuring high-quality, sustainable products.

Smurfit Westrock: Leveraging Scale After Merger

Formed through the 2024 merger of Smurfit Kappa and WestRock, Smurfit Westrock is now a global powerhouse in paper-based packaging. In May 2025, it published its first sustainability report, highlighting efforts to reduce carbon emissions and water usage. The company has invested $1 billion across paper and converting assets to improve efficiency and innovation. With its diversified portfolio and global reach, Smurfit Westrock is well-positioned to lead on recyclability and supply chain optimization in the liquid packaging segment.

Liquid Packaging Market Share Insights

Rigid Packaging Dominates Market Share by Packaging Type in the Liquid Packaging Industry

Rigid packaging holds a commanding 65% share of the global liquid packaging industry, underscoring its entrenched dominance in beverages and liquid foods. PET and HDPE bottles produced via blow molding are the central force behind this leadership, supported by their structural integrity, stackability, and consumer familiarity. Bottled water and carbonated soft drinks remain the largest contributors, while brand owners leverage rigid packaging’s wide decoration capabilities to reinforce recognition in crowded retail environments. Cartons, jars, and jugs extend the dominance of rigid formats by meeting product safety and shelf-display needs. By contrast, flexible packaging, while smaller in overall share, is the industry’s fastest-growing segment. Lightweight pouches, sachets, and bag-in-box formats offer significant material reductions, lower transport emissions, and enhanced convenience, particularly for sauces, soups, detergents, and premium wines. This dynamic illustrates how rigid packaging maintains volume leadership through scale and reliability, while flexible formats accelerate adoption through sustainability and logistics efficiency.

Blow Molding Leads Market Share by Technology in the Liquid Packaging Industry

Blow molding represents the largest 48% share of the liquid packaging technology landscape, cementing its position as the backbone of global beverage packaging. The technology’s ability to produce high-speed, cost-effective PET and HDPE bottles makes it indispensable for bottled water, carbonated soft drinks, and sports beverages—categories that collectively dominate global liquid consumption. Aseptic packaging follows as the premium enabler, driving the growth of shelf-stable cartons and bottles that eliminate preservatives while safeguarding taste, aroma, and nutrients, thus facilitating long-distance distribution without refrigeration. Form-Fill-Seal (FFS) technology secures a growing share as the efficiency engine of flexible packaging, delivering lightweight, space-saving pouches in a single integrated process that reduces material use and optimizes supply chains. Other technologies such as injection molding, thermoforming, and glass blowing sustain relevance in niche and specialized applications, including closures, tubs, and premium glass packaging. This segmentation highlights how blow molding anchors mass-volume efficiency, aseptic packaging ensures premium product preservation, and FFS drives the rapid rise of flexible solutions.

United States Liquid Packaging Market Driven by Sustainability and Technological Innovation

The U.S. liquid packaging market is heavily shaped by a fragmented regulatory environment. FDA regulations ensure product safety across the food and beverage industry, while state-level Extended Producer Responsibility (EPR) laws incentivize renewable and recyclable packaging adoption, particularly paperboard and metal-based solutions. Collaborative investments, such as the USD 100 million initiative by the American Beverage Association, are advancing PET bottle recycling and reducing reliance on virgin plastics, strengthening sustainability across the sector.

Technological innovation is a key growth driver, with the development of ultra-lightweight glass and plastic bottles, flexible packaging formats like pouches and bag-in-box systems, and advanced sealing technologies. Strategic corporate moves, such as Sealed Air’s acquisition of Liquibox and Canpack’s new aluminum can plant in Indiana, are expanding production capabilities to meet rising demand across dairy, juice, plant-based beverages, and spirits-based ready-to-drink (RTD) markets. Sustainability trends, including mono-material packaging and bio-based resins, are further enhancing recyclability, operational efficiency, and environmental performance.

Germany Emerges as a Global Leader in Sustainable Liquid Packaging

Germany’s liquid packaging industry operates under stringent regulations, including the Packaging Act (VerpackG) and the EU Packaging and Packaging Waste Regulation (PPWR) effective February 2025, mandating full recyclability or reuse of packaging by 2030. This legislative push accelerates adoption of sustainable paperboard and aseptic cartons. Innovations such as Elopak’s Pure-Pak® eSense, which removes the aluminum layer for easier recycling, illustrate Germany’s leadership in high-performance, eco-friendly packaging solutions.

Germany’s focus on the circular economy promotes innovations in sorting and recycling systems, rewarding packaging designed for recyclability. Strategic investments by domestic companies aim to enhance production efficiency and develop sustainable liquid packaging solutions to meet growing regulatory and consumer expectations. This positions Germany as a benchmark for renewable, recyclable, and high-performance liquid packaging technologies.

China’s Liquid Packaging Market Expands With Green Manufacturing and Automation

China’s liquid packaging sector is strongly influenced by governmental initiatives under the dual carbon goal and the Action Plan for Large-Scale Equipment Updates, encouraging sustainable materials and reduced excessive packaging. Regulatory reforms like GB/T 31268, which limit excess packaging in e-commerce, are directly shaping demand for efficient liquid packaging solutions.

Technological advancements, including AI-driven production and 5G-enabled industrial processes, are optimizing efficiency and scalability. Investments such as Shandong Bohui Paper Industry’s RMB 40 million upgrade to produce aseptic liquid packaging board highlight the emphasis on high-quality, food-safe materials. Local manufacturing growth and booming e-commerce, food, and beverage sectors are major demand drivers, positioning China as a leading hub for high-performance, circular liquid packaging solutions.

India’s Liquid Packaging Market Accelerates With Make in India and Infrastructure Programs

India’s liquid packaging industry benefits from the Make in India initiative and infrastructure programs like the Jal Jeevan Mission, which enhances water supply access and strengthens demand for aseptic and sustainable packaging. Incentives from the Ministry of Food Processing Industries (MoFPI) further support technological upgrading and domestic production expansion.

Technological adoption is increasing with initiatives such as UFlex’s U-shaped paper straw line and a plant producing 10 billion aseptic liquid packs annually, supporting sustainability and international compliance. Key applications include dairy, beverage, and pharmaceutical sectors, with rising exports demanding high-performance packaging that meets global safety standards. India is emerging as a critical market for eco-friendly, innovative liquid packaging solutions.

Japan’s Liquid Packaging Market Focuses on Advanced Materials and Regulatory Compliance

Japan’s liquid packaging market is driven by innovation in precision manufacturing and bio-based materials. Companies like LyondellBasell and Japanese cosmetic brands are incorporating bio-polypropylene (bio-PP) to enhance sustainability. Regulatory changes effective June 2025, including the “positive list” for synthetic materials in food containers, are driving safer and more compliant packaging solutions.

The market is emphasizing high-performance, specialty liquid packaging products, such as self-sealing cartons and high-barrier containers. Innovations recognized by the Japan Packaging Contest 2023, including 100% plant-based biodegradable biopolymers, highlight the sector’s commitment to functional, sustainable, and aesthetically superior packaging solutions across food, beverage, and cosmetic industries.

Brazil’s Liquid Packaging Market Advances With Sustainable Investments and Bio-Based Packaging

Brazil’s liquid packaging industry is shaped by the National Solid Waste Policy, which promotes sustainable packaging and waste management modernization. Technological developments include biodegradable, recyclable, and compostable solutions, with suppliers integrating bio-based polyethylene derived from sugarcane to reduce fossil fuel use and support carbon neutrality.

Corporate investments are driving capacity expansion and modernization, such as Forest Paper Group’s R$60 million project and Ardagh Group’s first Brazilian glass production facility, targeting growing demand in food, beverage, and agricultural sectors. Urbanization, sustainability awareness, and health-conscious consumer trends are shifting packaging toward reusable and recyclable liquid packaging solutions, attracting both domestic and international players.

Liquid Packaging Market Report Scope

Liquid Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$713.6 Million

|

|

Market Size (2034)

|

$1195.4 Million

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Packaging Type (Rigid Packaging, Flexible Packaging), By Material (Plastic, Paper & Paperboard, Glass, Metal), By Technology (Aseptic Packaging, Blow Molding, Form-Fill-Seal, Others), By End-User (Food & Beverages, Pharmaceuticals, Personal Care & Cosmetics, Household Care Products, Industrial Liquids, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Tetra Pak International S.A., SIG Group AG, Elopak ASA, Amcor Plc, Ball Corporation, Smurfit Kappa Group, Mondi Group, Nippon Paper Industries Co., Ltd., DS Smith Plc, International Paper, Uflex Ltd., WestRock Company, BillerudKorsnäs AB, Greatview Aseptic Packaging Co., Ltd., Berry Global Group, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Liquid Packaging Market Segmentation

By Packaging Type

- Rigid Packaging

- Flexible Packaging

By Material

- Plastic

- Paper & Paperboard

- Glass

- Metal

By Technology

- Aseptic Packaging

- Blow Molding

- Form-Fill-Seal

- Others

By End-User

- Food & Beverages

- Pharmaceuticals

- Personal Care & Cosmetics

- Household Care Products

- Industrial Liquids

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Liquid Packaging Market

- Tetra Pak International S.A.

- SIG Group AG

- Elopak ASA

- Amcor Plc

- Ball Corporation

- Smurfit Kappa Group

- Mondi Group

- Nippon Paper Industries Co., Ltd.

- DS Smith Plc

- International Paper

- Uflex Ltd.

- WestRock Company

- BillerudKorsnäs AB

- Greatview Aseptic Packaging Co., Ltd.

- Berry Global Group, Inc.

* List Not Exhaustive

Methodology

The research methodology for the Liquid Packaging Market integrates both primary and secondary approaches to ensure precise, actionable insights for industry professionals. Primary research included interviews with packaging engineers, sustainability experts, supply chain stakeholders, and senior executives across key regions, capturing firsthand perspectives on technological adoption, regulatory impacts, and market dynamics. Secondary research involved a thorough review of annual reports, patents, industry journals, regulatory databases, and verified sustainability disclosures to validate market trends and competitive landscapes. Advanced data triangulation techniques were applied to confirm market sizing, growth forecasts, and investment patterns, factoring in macroeconomic indicators, raw material pricing trends, and innovations in aseptic, blow molding, and flexible packaging technologies. Both top-down and bottom-up forecasting models were employed, while regional insights were contextualized against policy frameworks, consumer behavior, and trade flows. This comprehensive, multi-layered methodology ensures that USDAnalytics delivers reliable, fact-based, and professionally relevant intelligence on the global Liquid Packaging Market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.