Liquid Packaging Board Market Overview and Key Industry Insights

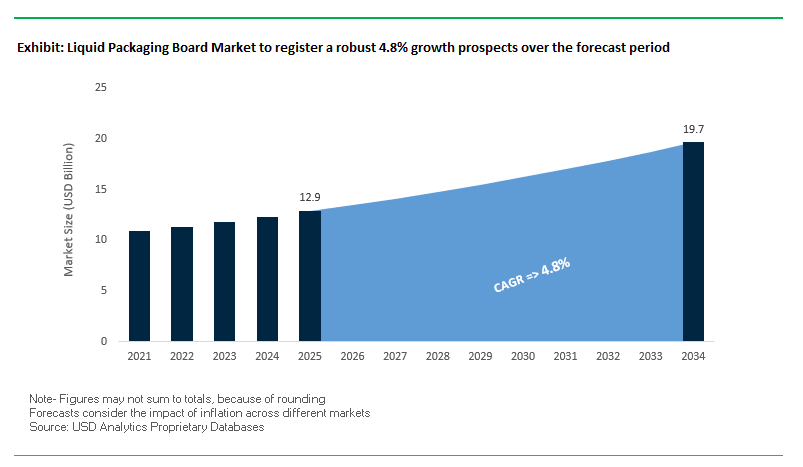

The Global Liquid Packaging Board Market is projected to expand from USD 12.9 billion in 2025 to USD 19.7 billion by 2034, reflecting a steady CAGR of 4.8%. This growth trajectory is underpinned by rising demand for sustainable food and beverage packaging solutions, especially as regulators, brand owners, and consumers push for alternatives to plastics. The sector is strategically positioned at the intersection of circular economy principles, food safety, and material innovation, making it a critical focus area for packaging manufacturers and beverage producers alike.

For industry professionals, the liquid packaging board market answers several strategic questions: How can renewable fibers compete with plastics and glass on performance? How is the industry addressing recyclability challenges? Which applications are driving the highest demand? The answers point to a market that is not only resilient but also transforming into a sustainability-driven ecosystem where innovation in barrier properties and end-of-life solutions is key.

Key Insights for Buyers and Professionals

- Circular Economy Leadership: Liquid packaging board leverages wood fiber as a renewable material, making it a sustainable choice compared to plastics and glass.

- Food Safety Advantage: The 6.5-micrometer aluminum layer provides oxygen and light barriers, enabling shelf lives of up to 18 months for products like UHT milk and juices without preservatives.

- Application Dominance: The dairy sector accounts for over 70% of global market volume, with plant-based beverages emerging as the fastest-growing segment.

- Recyclability Innovations: Investments in layer-separation technologies are enabling improved recovery of aluminum and polyethylene, enhancing recycling rates and circular value.

Market Analysis – Recent Industry Developments and Strategic Moves

The liquid packaging board market is currently shaped by aggressive investments, sustainability commitments, and expansions into high-growth regions. Companies are aligning their operations with decarbonization goals, recyclability targets, and supply chain optimization, while also tapping into emerging markets like India and North America. These developments highlight how sustainability and growth are deeply intertwined within the industry.

In August 2025, Elopak reported a 2.4% revenue increase year-on-year, fueled by growth in the Americas and the ramp-up of its new U.S. plant. During the same month, Mondi Group scaled up its FunctionalBarrier Paper Ultimate production to meet surging demand for recyclable, high-barrier packaging, and announced its plan to achieve 90% energy self-sufficiency at its Slovakian mill via a new biomass power plant—underscoring climate action priorities. Also in August, Tetra Pak earned the EcoVadis Platinum rating, the highest ESG recognition, while SIG invested USD 35 million in its Querétaro, Mexico plant, expanding capacity by 50%. These developments demonstrate the sector’s dual focus on capacity expansion and ESG leadership.

Earlier, in June 2025, Tetra Pak partnered with Fiat to incorporate recycled beverage cartons into car parts, creating a unique circular economy application in the automotive industry. In May 2025, the newly formed Smurfit Westrock published its first sustainability report, highlighting a USD 1 billion investment across paper and converting assets to accelerate innovation and efficiency. In February 2025, SIG launched its first aseptic carton plant in India, strategically targeting one of the world’s fastest-growing markets for liquid packaging.

Emerging Trends and High-Impact Opportunities in the Liquid Packaging Board Market

Accelerated Investment in Barrier-Coated Recyclable Board to Replace Plastic Laminates

The liquid packaging board (LPB) market is undergoing a transformative shift as major food and beverage brands increasingly replace non-recyclable plastic-laminated cartons with mono-material, polyolefin-coated paperboard structures. This trend is largely driven by stricter Extended Producer Responsibility (EPR) regulations and corporate sustainability commitments, ensuring packaging is fully compatible with recycling streams. Companies like Elopak are aggressively advancing strategies such as “Repackaging Tomorrow,” promoting natural brown boards that lower carbon footprints, with over 2,200 tonnes of CO₂ savings recorded in 2024. Investment in new production lines, supported by green bonds, is expanding LPB capacity in North America and Canada to meet rising demand. Regulatory mandates, such as India’s EPR draft rules targeting 50% paper recycling by 2026-27, incentivize brands to adopt recyclable LPB solutions. Closed-loop recycling initiatives, like Tetra Pak’s partnership with Lactalis to produce cartons from certified recycled polymers, exemplify the move toward sustainable circular packaging, demonstrating the commercial viability of recycled content in food-grade LPB applications.

Development of Fiber-Based Barriers to Replace Aluminum Foil in Aseptic Cartons

Aseptic carton packaging is evolving to eliminate aluminum foil layers, which hinder recyclability in traditional paper streams. R&D investments are focusing on high-performance fiber-based barriers using silica coatings and plant-derived polymers that maintain shelf-stable protection while ensuring recyclability. Tetra Pak’s fiber-based barrier reduces carbon emissions from base material composition by up to 33% and increases renewable content, achieving around 80% FSC-certified paperboard and 90% total renewable materials with biopolymers. Dispersion coating technologies replace traditional plastic extrusion, enabling faster repulping and higher fiber recovery rates. Crucially, these innovations maintain uncompromised performance, delivering comparable oxygen and light protection as aluminum foil, ensuring product safety, and extending shelf life while meeting environmental standards.

Expansion into New Beverage Categories Beyond Dairy and Juice

The rapid growth of functional beverages, including protein drinks, plant-based milks, and cold-brew coffee, presents a white-space opportunity for LPB carton manufacturers. LPB’s strength, barrier performance, and shelf-stable properties allow packaging expansion beyond traditional dairy and juice categories. Consumers increasingly demand sustainable alternatives; research indicates that 73% of European consumers prefer fiber-based cartons over plastics, and 70% actively choose products with minimal plastic content. For instance, cold-brew coffee, traditionally packaged in plastic bottles, is now being offered in aseptic cartons, enabling ambient storage, reducing refrigeration needs, and providing environmental benefits throughout the supply chain. This trend aligns LPB with growing sustainability-conscious consumer preferences while addressing the functional beverage market’s packaging needs.

On-Pack Digital Watermarks for High-Efficiency Carton Sorting and Recycling

Improving LPB recycling efficiency remains a key opportunity through on-pack digital watermarks, which allow high-speed sorting robots to accurately separate cartons from general paper waste. Industrial trials of the HolyGrail 2.0 initiative demonstrate sorting efficiencies of up to 95.1% using digital watermarks, vastly outperforming conventional methods. This technology facilitates the differentiation of food-grade and non-food-grade packaging, enabling closed-loop recycling systems while maintaining food safety standards. Broad industry collaboration, involving over 130 companies in the packaging value chain, underscores commitment to scaling this innovation. Enhanced material purity achieved through watermark-enabled sorting ensures high-quality recycled fibers, supporting circular economy objectives and enabling LPB manufacturers to deliver fully recyclable, environmentally responsible packaging solutions.

Competitive Landscape of the Global Liquid Packaging Board Industry

The competitive landscape is defined by five global leaders—Tetra Pak, SIG Combibloc, Mondi Group, Elopak, and Smurfit Kappa (Smurfit Westrock)—that dominate through vertical integration, technological innovations, and sustainability strategies. Each company is investing heavily in recycling systems, renewable energy, and advanced barrier materials, ensuring the industry remains highly dynamic and competitive.

Tetra Pak: Setting the Standard in Circular Packaging Solutions

Tetra Pak leads the global market with its broad aseptic and non-aseptic carton portfolio. In June 2025, it partnered with Fiat to use recycled cartons in automotive applications, creating new circular value streams. Its strategy emphasizes sustainability, digital traceability, and renewable materials, with a stated goal of achieving 100% renewable or recycled content packaging. Flagship products like Tetra Prisma Aseptic and Tetra Rex Plant-based demonstrate its commitment to performance and eco-design.

SIG Combibloc: Expanding Global Footprint with Smart Carton Solutions

SIG is aggressively scaling in high-growth regions, investing USD 35 million in Mexico (July 2025) and opening its first aseptic plant in India (February 2025). Its strength lies in flexible, end-to-end solutions for smarter factories and connected packs, enabling rapid design changes. Products like combibloc EcoPlus highlight SIG’s role in advancing sustainable and lightweight packaging, while its diverse closures portfolio caters to convenience-focused consumers.

Mondi Group: Innovating High-Barrier Sustainable Packaging

Mondi is a key supplier of liquid packaging board and recently ramped up production of its FunctionalBarrier Paper Ultimate (August 2025). Its MAP2030 sustainability roadmap drives innovation toward fully recyclable and compostable packaging by 2025. By vertically integrating forestry, pulp, and converting operations, Mondi maintains strong quality control and sustainability across the value chain, positioning itself as a leader in barrier material innovation.

Elopak: Expanding in the Americas with Sustainable Carton Solutions

Elopak’s new U.S. facility is driving growth in the Americas, contributing to a 2.4% revenue increase in Q2 2025. Its Repackaging Tomorrow strategy aims to replace plastics with fiber-based cartons, and innovations like Pure-Fill enhance customer flexibility. Elopak’s portfolio, particularly its gable-top cartons, remains a trusted choice for fresh dairy and juice products, with its design and convenience features enhancing consumer acceptance.

Smurfit Kappa (Smurfit Westrock): Building a Global Paper Packaging Powerhouse

Formed through the merger of Smurfit Kappa and WestRock, the company published its first sustainability report in May 2025, detailing USD 1 billion in system investments. Its portfolio spans across liquid packaging board, corrugated packaging, and paper products. Smurfit Westrock’s scale and expertise in supply chain optimization and recyclability give it a strong advantage, making it one of the most influential players in the evolving global market.

Liquid Packaging Board Market Share Insights

Paperboard Leads Market Share by Material in the Liquid Packaging Board Industry

Paperboard commands the largest 74% share of the liquid packaging board (LPB) industry, cementing its role as the indispensable backbone of aseptic cartons. As the structural layer, paperboard delivers the rigidity and printable surface required for branding while being sourced from renewable forestry resources, aligning perfectly with global sustainability mandates. Its dominance is reinforced by brand strategies that leverage recyclability and renewable sourcing as key marketing claims in the competitive beverages sector. Polyethylene (PE) contributes as the essential sealing and liquid barrier layer, though its market presence is under scrutiny due to sustainability pressures, driving rapid adoption of bio-based and thinner PE coatings to reduce fossil-based content. Aluminum holds a smaller yet critical share, serving as the specialized oxygen and light barrier in UHT milk, juices, and nutritionally sensitive products, enabling extended shelf-life without refrigeration. Together, this material balance highlights how paperboard underpins sustainability leadership, PE drives functional performance, and aluminum provides the protective edge for high-value liquids.

Juices and Beverages Dominate Market Share by Application in the Liquid Packaging Board Industry

Juices and beverages account for the largest 38% share of LPB applications, reflecting their historic and ongoing role as the primary driver of aseptic carton adoption worldwide. The ability of LPB to preserve delicate flavors, vitamins, and aromas in fruit juices, nectars, and plant-based beverages without preservatives or refrigeration secures its leadership in this segment. Dairy products follow as the volume-driven core, propelled by UHT milk and flavored dairy drinks in both developed and emerging markets where shelf-stable formats are critical for distribution efficiency. Wine and spirits represent a high-value growth application, as cartons and bag-in-box solutions emerge as lightweight, sustainable alternatives to glass, gaining favor among eco-conscious consumers. Soups and sauces maintain a steady niche, supported by convenience and the ability to withstand reheating, while “other applications” such as liquid eggs and nutritional supplements form the innovation frontier. This segmentation demonstrates how juices and beverages anchor LPB adoption, while dairy and premium alcohol applications expand its reach into both mass-market and high-margin segments.

United States Liquid Packaging Board Market Expands With Sustainable Coatings and Lightweight Innovations

The U.S. liquid packaging board market is shaped by a fragmented regulatory environment, with FDA regulations ensuring the safety and integrity of food and beverage packaging. State-level Extended Producer Responsibility (EPR) laws are accelerating the adoption of recyclable and renewable packaging materials, reinforcing the shift toward sustainable liquid packaging board solutions. Technological advancements are driving innovation, including ultra-lightweight boards and bio-based high-barrier coatings, which reduce material consumption while maintaining structural integrity.

Corporate investments are significant, with Suzano acquiring Pactiv Evergreen mills, adding 420,000 metric tons of integrated paperboard production and strengthening its North American presence. The market sees strong demand in dairy, juice, plant-based beverages, and pharmaceutical packaging, where sterility and durability are paramount. Industry associations like the American Forest & Paper Association (AF&PA) promote recyclability and higher recycled content, underscoring sustainability as a key market driver for LPB.

Germany Leads Liquid Packaging Board Market Through High-Performance Coatings and Circular Economy Initiatives

Germany’s liquid packaging board industry is governed by stringent regulations under the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, mandating fully recyclable or reusable packaging by 2030. This regulatory push is driving the adoption of sustainable paper-based packaging solutions with high-performance barrier coatings that protect against oxygen and moisture. Industry 4.0 technologies are revolutionizing manufacturing processes, enhancing efficiency and product quality.

Germany’s Packaging Act (VerpackG) incentivizes companies to produce recyclable packaging, favoring LPB as a renewable and sustainable option. Corporate investments are focused on innovative, high-performance packaging solutions to meet regulatory compliance and consumer demand. The combination of regulatory pressure, technological advancement, and circular economy leadership positions Germany as a global frontrunner in eco-friendly liquid packaging board development.

China’s Liquid Packaging Board Market Grows With Domestic Manufacturing and Aseptic Innovations

China’s liquid packaging board market is being shaped by governmental initiatives under the dual carbon goal and the Action Plan for Promoting Large-Scale Equipment Updates, which encourage recycling and sustainable material use, including LPB. Regulatory reforms, such as GB/T 31268, target excessive packaging in e-commerce, driving demand for optimized, circular packaging solutions.

Technological advancements include automation, AI integration, and investments in aseptic liquid packaging board production, as demonstrated by Shandong Bohui Paper Industry, which invested over RMB 40 million to upgrade its production lines. The country’s booming e-commerce, electronics, and food & beverage sectors drive demand for high-quality LPB, while the emphasis on domestic manufacturing reduces reliance on imported solutions and strengthens local production capabilities.

India’s Liquid Packaging Board Market Accelerates With Make in India and Food Processing Growth

India’s LPB market is supported by the Make in India initiative and government incentives from the Ministry of Food Processing Industries (MoFPI), promoting domestic manufacturing and cold-chain efficiency. The adoption of advanced materials and specialized products is increasing, exemplified by UFlex commissioning a plant to produce 10 billion aseptic liquid packs annually and introducing India’s first U-shaped paper straw manufacturing line for sustainable beverage packaging.

Key applications include the dairy, beverage, and pharmaceutical sectors, with rising exports driving the need for high-performance, internationally compliant liquid packaging board solutions. The combination of technological advancements, government support, and strong domestic and export demand underscores India’s growth potential in the LPB market.

Japan’s Liquid Packaging Board Market Focuses on Specialty Coatings and High-Performance Packaging

Japan’s liquid packaging board industry is anchored in precision manufacturing and innovation, with companies like Nippon Paper Industries advancing high-performance paperboard solutions. Regulatory changes effective June 2025, introducing a “positive list” for synthetic materials in food packaging, are pushing the market toward safe, compliant coatings and environmentally responsible solutions.

Market leaders are emphasizing specialty and value-added products, such as self-sealing LPB with superior barrier properties, catering to the food, beverage, and pharmaceutical sectors. Japan’s strategy of leveraging total system integration and global collaboration enables manufacturers to innovate rapidly, enhancing functionality, compliance, and sustainability in the LPB segment.

Brazil’s Liquid Packaging Board Market Expands Through Sustainable Investments and Industrial Modernization

Brazil’s LPB industry is strongly influenced by the National Solid Waste Policy, promoting sustainable packaging solutions and waste reduction. Technological advancements in biodegradable, recyclable, and compostable LPB materials are being adopted to reduce environmental impact. Companies are investing heavily, exemplified by Brazil’s Forest Paper Group, which invested 60 million Reais ($12.11 million) to modernize facilities and increase production of recycled linerboard by 25%.

Demand is particularly strong in the food and beverage and agricultural sectors, fueled by the need for high-performance, sustainable packaging for processed and ready-to-eat foods. Corporate investments, coupled with trade agreements like EU-Mercosur, are enhancing Brazil’s production capabilities and attracting both domestic and international players, solidifying its position in the eco-friendly liquid packaging board market.

Liquid Packaging Board Market Report Scope

Liquid Packaging Board Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.9 Billion

|

|

Market Size (2034)

|

$19.7 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Material (Paperboard, PE, Aluminum), By Application (Dairy Products, Juices & Beverages, Wine & Spirits, Soups & Sauces, Other Applications), By Technology (Aseptic Packaging, Non-Aseptic Packaging), By Closure Type (Screw Caps, Straw Holes, Tear-off Openings, Other)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Tetra Pak International S.A., SIG Group AG, Elopak ASA, Smurfit Kappa Group, Mondi Group, Nippon Paper Industries Co., Ltd., DS Smith Plc, International Paper, Uflex Ltd., WestRock Company, BillerudKorsnäs AB, Greatview Aseptic Packaging Co., Ltd., AR Packaging Group AB, Evergreen Packaging, Lami Packaging (Kunshan) Co. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Liquid Packaging Board Market Segmentation

By Material

By Application

- Dairy Products

- Juices & Beverages

- Wine & Spirits

- Soups & Sauces

- Other Applications

By Technology

- Aseptic Packaging

- Non-Aseptic Packaging

By Closure Type

- Screw Caps

- Straw Holes

- Tear-off Openings

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Liquid Packaging Board Market

- Tetra Pak International S.A.

- SIG Group AG

- Elopak ASA

- Smurfit Kappa Group

- Mondi Group

- Nippon Paper Industries Co., Ltd.

- DS Smith Plc

- International Paper

- Uflex Ltd.

- WestRock Company

- BillerudKorsnäs AB

- Greatview Aseptic Packaging Co., Ltd.

- AR Packaging Group AB

- Evergreen Packaging

- Lami Packaging (Kunshan) Co. Ltd.

* List Not Exhaustive

Methodology

The methodology employed by USDAnalytics for analyzing the Liquid Packaging Board Market combines comprehensive primary and secondary research, designed to provide industry professionals with a precise and actionable market outlook. Primary research involved structured interviews with packaging manufacturers, beverage producers, sustainability experts, and regulatory authorities to capture firsthand insights on emerging trends, regulatory impacts, and technology adoption. Secondary research encompassed an extensive review of company reports, scientific publications, government policies, trade journals, and patents to validate market dynamics and competitive positioning. Both top-down and bottom-up approaches were used to quantify market size, factoring in regional production capacities, end-user demand across dairy, juices, and plant-based beverages, and investments in barrier technologies, recycling innovations, and aseptic processing. Forecasting models incorporated growth drivers such as sustainable packaging mandates, circular economy initiatives, and advancements in fiber-based and polyolefin-coated boards. This methodology ensures USDAnalytics delivers a robust, forward-looking analysis, enabling strategic decision-making, investment planning, and technology adoption strategies for professionals operating in the global Liquid Packaging Board Market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.