Aluminum-Led Circularity, Precision Valving, and Low-GWP Propellants Push Aerosol Packaging to $10.5B (2034)

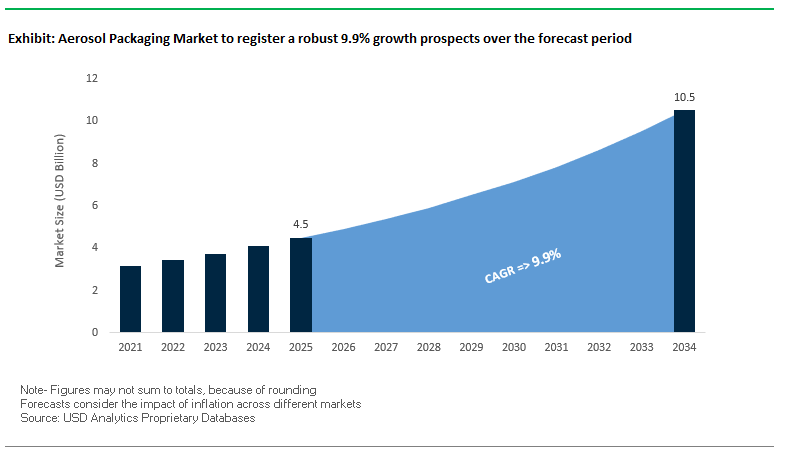

Market Value (MV) 2025: USD 4.5 Billion │ 2034: USD 10.5 Billion │ CAGR: 9.9%

The global aerosol packaging market is accelerating on three structural levers: (1) aluminum/steel dominance delivering durability, corrosion resistance, and truly circular recyclability; (2) rapid propellant transition toward compressed air, nitrogen, and lower-GWP HFAs in line with evolving regulations (e.g., the U.S. AIM Act); and (3) precision dispensing through advanced valves/actuators that minimize overuse and elevate user experience in personal care, household, and OTC use cases. With metal containers accounting for over 63% of 2024 revenue, and >75% of all aluminum ever produced still in use, procurement strategies are pivoting to recycled content sourcing, lightweighting, and mono-material compatibility to reduce total cost and carbon while protecting line speed and product integrity.

Key Insights for industry professionals:

- Material leadership: Aluminum and steel captured >63% of revenue in 2024 thanks to durability, corrosion resistance, and infinite recyclability.

- Recycling performance: >75% of historical aluminum remains in circulation; Japan’s aluminum can recycling >90% demonstrates policy + consumer impact.

- Propellants pivot: Migration from hydrocarbons toward compressed air, nitrogen, and low-GWP HFAs aligns with AIM Act trajectories.

- Dispensing science: Metered-dose valves, fine-mist sprayers, and controlled actuators curb product waste and improve dose accuracy.

- What to specify now: High-recycled aluminum, low-GWP propellants, e-commerce/ISTA compliance, and valve/actuator SKUs tuned to viscosity, droplet size, and target application.

Market Analysis: Metals Recycle at Scale, Propellant Reformulations Advance, and Dispensing/E-Commerce Readiness Tightens

Strategic refocusing and circular capacity. In September 2025, Greif announced a plan to intensify focus on core packaging after selling its Soterra land management business in August 2025 for USD 462M, followed by a July 2025 agreement to divest its Containerboard business (USD 1.8B). While not a direct aerosol supplier, this portfolio sharpening mirrors a wider industry pattern: consolidating around highest-return, regulation-resilient formats such as metal systems and dispensing components, improving capital allocation and supply reliability for brand owners.

Sustainability and performance investments. August 2025 saw Constantia Flexibles commit €100M+ to production upgrades (flexible ecosystems that increasingly co-pack with aerosols) and Aptar Beauty extend ISTA-6 capabilities in Europe relevant to e-commerce shock/vibration validation for pressurized packs and secondary packaging. In August 2025, Amcor expanded healthcare packaging in Costa Rica, strengthening sterile/quality infrastructures that often cross-pollinate with aerosol valve, liner, and laminate quality systems. July 2025 brought Huhtamaki’s fifth EcoVadis Gold, reinforcing the procurement pivot to verifiable ESG credentials across the aerosol value chain.

Propellant and component technology momentum. May 2025, Aptar was named among TIME’s World’s Most Sustainable Companies, coinciding with the market’s shift to lower-GWP propellants and precision valves (metered dose, fine mist) to enhance efficacy with less product. Earlier, in February 2025, Amcor introduced recycle-ready high-shield laminates (healthcare) that inform barrier and seal strategies in aerosol secondary/ancillary packaging. Net-net: 2025 activity supports a durable migration to circular metals, validated dispensing performance, and audit-ready supply chains capable of managing AIM-aligned propellants and omnichannel logistics.

Emerging Trends and High-Value Opportunities in the Aerosol Packaging Market

Strategic Transition to Next-Generation, Low Global Warming Potential (GWP) Propellants

The aerosol packaging industry is undergoing a significant transformation as brands and fillers adopt low-GWP propellants to comply with environmental regulations and achieve sustainability goals. Regulatory mandates, such as the U.S. Environmental Protection Agency’s (EPA) American Innovation and Manufacturing (AIM) Act, are phasing out high-GWP HFCs like HFC-152a, pushing manufacturers towards Hydrofluoroolefins (HFOs), compressed gases, and hydrocarbons. HFO-1234ze, a non-flammable, low-GWP propellant, exemplifies how next-generation formulations maintain performance while reducing environmental impact. Hydrocarbons, including blends of butane, propane, and isobutane, remain widely used due to established infrastructure, cost-effectiveness, and formulation expertise. These strategic shifts require significant reformulation, investment in new filling lines, and rigorous compatibility testing, positioning forward-looking manufacturers to capitalize on the growing demand for sustainable aerosol solutions.

Adoption of Monomaterial and Enhanced Recyclable Aluminum Cans

Sustainability concerns and consumer pressure are driving the industry toward fully recyclable aerosol solutions. Manufacturers are increasingly deploying aluminum cans with easily separable plastic overcaps or monomaterial polypropylene aerosols to enhance recyclability. Companies like Trivium Packaging emphasize that aluminum and steel aerosols are infinitely recyclable, creating a closed-loop material cycle. Design innovations ensure that plastic components can be removed easily, improving Material Recovery Facility (MRF) efficiency and increasing high-quality recycled aluminum yields. This trend aligns with both regulatory directives and consumer preferences, reinforcing the importance of sustainable design in aerosol packaging.

Development of Water-Based and Co-Solvent Formulations for Sustainable Propellant Systems

There is a substantial opportunity for R&D in water-based and compressed-gas aerosol formulations, enabling the elimination of volatile organic compounds (VOCs) and traditional liquefied gas propellants. Innovative emulsion and valve technologies allow compressed air or nitrogen to deliver consistent spray patterns, meeting performance expectations for consumer, industrial, and automotive applications. Patents for water-based aerosol sprays demonstrate technical feasibility, highlighting the potential for sustainable product lines. Advancements in actuator and valve design ensure fine, uniform sprays, overcoming previous limitations associated with compressed gas formulations. Companies investing in these technologies can gain a first-mover advantage in eco-friendly aerosol solutions.

Integration of Smart and Connected Packaging for Dosage Control and Safety

Smart aerosol packaging is emerging as a high-value opportunity for both consumer engagement and regulatory compliance. Incorporating mechanical counters, smart valves, and NFC tags enables real-time monitoring of usage, dose tracking, and enhanced anti-counterfeiting measures. In pharmaceutical applications, these innovations support medication adherence and patient safety by providing visual feedback and authenticity verification. NFC-enabled inhalers, for example, allow patients to confirm legitimacy and track remaining doses via smartphones. Additionally, connected packaging enhances supply chain visibility for high-value products, reducing risks of diversion or misuse. These technological integrations open new revenue streams while addressing critical safety and compliance requirements.

Competitive Landscape: Metal Circularity + Valve Science + Low-GWP Readiness Define the Leaders

Aerosol performance is increasingly decided by metal container quality, recycled content integration, valve/actuator precision, and compliance with evolving propellant rules. The companies below translate those vectors into differentiated offerings at global scale.

AptarGroup, Inc.: Precision aerosol valves and bag-on-valve for hygiene and sustainability

Aptar supplies aerosol valves, actuators, and dispensing systems spanning beauty, personal care, and household. Under Future Made Better, Aptar advances reduce–reuse–recycle with all-plastic/mono-material components that simplify end-of-life streams. The Aptar Beauty range and ISTА-6 expansion (August 2025) support e-commerce durability critical for pressurized formats. Its Bag-on-Valve (BoV) architecture separates product from propellant, improving hygiene, evacuation rate, and low-GWP compatibility, while meeting diverse certification/regulatory needs. Strategically, Aptar is positioned as the valve/actuator partner of record for brands standardizing on precision dosing and sustainability.

Crown Holdings, Inc.: Global aluminum/steel aerosol can capacity with recycled-content focus

Crown manufactures aluminum and steel aerosol cans for personal care, household, and automotive applications, leveraging a broad global footprint across the Americas, Europe, and Asia. Current strategy emphasizes high-growth segments and divestment of non-core assets, channeling capex into sustainable metal packaging (higher recycled content, recyclable coatings). Crown’s competitive edge is consistent metal formability, coating integrity, and regional supply resilience key for multinational CPGs compressing lead times while meeting circularity KPIs and regional EPR obligations.

Ball Corporation: ASI-certified aluminum aerosols with higher recycled content

Ball produces aluminum aerosol cans and broader metal containers with a sustainability-first stance. In 2023, Ball became the first impact-extruded aerosol/aluminum supplier certified by the Aluminum Stewardship Initiative (ASI), underscoring responsible sourcing and manufacturing. Its portfolio includes high-recycled-content aerosols (e.g., “most sustainable” can variants) aimed at lowering embedded carbon while maintaining line speed, wall integrity, and decor fidelity. Ball’s strategy aligns brand owners with recycled aluminum supply, lightweighting, and transparent ESG reporting.

Ardagh Group S.A.: Lightweight metal systems via AMP with circular design

Through Ardagh Metal Packaging (AMP), Ardagh offers aluminum and steel aerosol containers for personal care and food. Innovation centers on lightweighting and recycled content, evidenced by the company’s Eco-Light approach (up to ~30% weight reduction in comparable metal formats), translating into lower transport emissions and improved material efficiency without sacrificing performance. Ardagh’s manufacturing discipline and global quality systems support brands navigating low-GWP propellants, valve/liner compatibility, and decor complexity at scale.

Aerosol Packaging Market Share Insights

Cans Dominate Market Share by Product Type in the Aerosol Packaging Industry

Cans hold an overwhelming 82% share, cementing their role as the undisputed standard in the aerosol packaging industry. This dominance stems from their exceptional pressure resistance, barrier performance, and cost efficiency at high volumes. Steel and aluminum cans benefit from a well-established global manufacturing and filling infrastructure that supports scale economies across personal care, household products, and automotive sprays. Bottles, typically extruded aluminum or advanced plastics, secure a niche share focused on premium personal care and cosmetics where aesthetics and tactile appeal justify higher costs. The “others” segment, though small, represents the innovation frontier with refillable formats, industrial drums, and sustainable alternatives using composite materials. This balance between volume-driven dominance of cans and innovation in premium formats underscores the industry’s dual priorities of efficiency and sustainability.

Personal Care Drives Market Share by End-Use in the Aerosol Packaging Industry

Personal care products lead the market with around 48% share, driven by massive global demand for deodorants, hair sprays, and body care products. This segment is highly dynamic, with innovation focused on reducing propellant usage, improving recyclability through lightweight aluminum, and introducing dermatologically safe spray systems. Household products account for 35% share, representing a stable yet less innovation-driven sector centered on disinfectants, air fresheners, insecticides, and starch sprays. Automotive applications maintain a specialized share for lubricants, brake cleaners, and paints where chemical resistance and safety are paramount. Healthcare aerosols, though smaller, are high-value due to their reliance on precise, sterile delivery formats for medicated foams and antiseptic sprays. The “others” category, spanning industrial sprays, food products, and animal care, is a diverse but regulated niche that reflects the expanding versatility of aerosol systems. Collectively, end-use segmentation highlights how personal care drives volume, while healthcare and food-related aerosols drive premium value.

United States: Governmental Regulations and Sustainable Aerosol Innovations Driving Market Growth

The U.S. aerosol packaging market is being strongly shaped by evolving regulations from the Environmental Protection Agency (EPA), which impose strict guidelines on volatile organic compounds (VOCs) and propellant emissions. These policies have driven manufacturers to adopt eco-friendly formulations using low-carbon footprint alternatives, such as compressed air or nitrogen propellants. Technological advancements are further accelerating market growth, with companies like Unilever introducing nitrogen-propelled aerosol deodorants packaged in recycled aluminum cans.

Corporate initiatives also play a pivotal role. Crown Holdings, Inc. collaborates with local recycling cooperatives to enhance post-consumer aerosol can collection, while SC Johnson invests in sustainable manufacturing plants to support localized production. Consumer preference for sustainable products has fueled innovation in personal care aerosols, including premium deodorants and hairsprays with extended shelf life. Additionally, the healthcare sector continues to rely on aerosolized medications, such as asthma inhalers, emphasizing the critical regulatory compliance governed by FDA standards.

Germany: Circular Economy Leadership and Advanced Packaging Materials

Germany’s aerosol packaging market operates under a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR) effective February 2025. This regulation mandates full recyclability or reusability of packaging by 2030 and sets minimum recycled content targets. The country’s Packaging Act (VerpackG) ensures producers are accountable for the entire packaging lifecycle, driving innovation in recyclable aerosol materials.

Technological innovation is evident through lightweight aluminum cans, such as Toyo Seikan’s 6.1g beverage can launched in 2024, reducing material consumption while maintaining strength. Corporate initiatives, including Beiersdorf AG’s fully recyclable skincare aerosol line, highlight a strong commitment to sustainability. Regulatory shifts, including the EU F-Gas phase-out of fluorinated gases by 2025, are pushing a transition to eco-friendly propellants like nitrogen and carbon dioxide. Personal care remains the largest market segment, with pharmaceuticals sustaining steady demand for metered-dose inhalers supported by Germany’s advanced healthcare infrastructure.

China: Dual Carbon Goals and Smart Packaging Innovations Propel Growth

China’s aerosol packaging market is being shaped by the government’s “dual carbon” strategy, promoting carbon neutrality and peak carbon targets. The June 2025 packaging regulation encourages the use of recycled materials, reusable systems, and reduction of delivery waste. Technological advancements, including automation, AI, and “5G plus industrial internet” integration, enhance production efficiency and flexible manufacturing for aerosol packaging.

Sustainability initiatives are accelerating the shift to paper-based and eco-friendly alternatives. Multinational FMCG companies are expanding local production to meet growing consumer demand and reduce supply chain length; for instance, Unilever has launched nitrogen-propelled deodorants using 50% recycled aluminum cans. Aerosol applications in healthcare, such as disinfectants and wound care products, are also expanding. Innovative smart packaging, incorporating QR codes and pressure sensors, enables usage tracking and strengthens brand engagement, positioning China as a key market for sustainable and technologically advanced aerosol packaging solutions.

India: Local Manufacturing and Smart Packaging Drive Sustainable Aerosol Adoption

India’s aerosol packaging market benefits from initiatives like “Make in India” and “Zero Effect Zero Defect,” which encourage quality domestic production. Multinational FMCG companies, including SC Johnson, are investing in sustainable manufacturing plants to localize production and shorten supply chains. New regulations, such as the Plastic Waste Management (Amendment) Rules, are promoting eco-friendly propellants and sustainable materials adoption.

Corporate expansion is evident with Unilever and Henkel launching nitrogen-propelled aerosol products and collaborating with local partners for improved recycling. The country’s growing industrial sectors, including automotive and construction, are increasing demand for industrial aerosols like paints and lubricants. Smart packaging technologies, such as QR codes and pressure sensors, are being integrated to improve usage tracking, compliance, and consumer engagement, highlighting the convergence of sustainability, technology, and regulatory support in India’s aerosol packaging market.

Brazil: Sustainability and Robotics-Driven Efficiency Expand Market Opportunities

Brazil’s aerosol packaging market is driven by the National Solid Waste Policy, which promotes a circular economy and encourages reusable and durable packaging solutions. Technological advancements, including robotics and AI, are enhancing production efficiency and quality control, enabling sophisticated operations like automated sorting and defect detection.

Sustainability remains a key focus, with eco-friendly aerosol materials gaining traction following the January 2025 law banning imported solid waste, including plastics. Strategic investments by industry bodies and NGOs, such as ABRE, are fostering sustainable design practices. The cosmetics and household products sectors are major growth drivers, while the expanding food processing industry increases demand for aerosol packaging solutions like cooking sprays and food preservation products, positioning Brazil as a critical market for sustainable and technologically advanced aerosol innovations.

Japan: Advanced Technologies and Bio-Based Materials Fuel Market Expansion

Japan’s aerosol packaging market benefits from advanced technologies and precision manufacturing, with AI-driven processes enhancing design efficiency and production accuracy. Regulatory updates from May 2025 by the Ministry of Health, Labour and Welfare (MHLW) introduce stricter food-contact packaging requirements under the Food Sanitation Act, emphasizing safety and compliance.

A shift toward bio-based materials is evident, highlighted by LyondellBasell’s partial incorporation of bio-based polypropylene into Shiseido’s aerosol packaging in September 2025. Continuous innovation in functionality, including high dimensional stability and resistance to deformation, caters to high-performance applications. Demographic drivers, such as the aging population, sustain demand for aerosol-based medical devices for respiratory treatments, solidifying the healthcare sector’s importance. The rapid growth of e-commerce further boosts demand for durable, reliable, and customizable aerosol packaging solutions across Japan.

Aerosol Packaging Market Report Scope

Aerosol Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.5 Billion

|

|

Market Size (2034)

|

$10.5 Billion

|

|

Market Growth Rate

|

9.9%

|

|

Segments

|

By Product Type (Cans, Bottles, Others), By Material (Aluminum, Tin-plated Steel, Glass, Plastic), By Propellant Type (Compressed Gas, Liquefied Gas), By End-Use Industry (Personal Care, Household Products, Automotive, Healthcare, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ball Corporation, Crown Holdings Inc., Trivium Packaging, Mauser Packaging Solutions, CCL Industries Inc., Toyo Seikan Group Holdings Ltd., Ardagh Group S.A., Colep Packaging, Nampak Ltd., CPMC Holdings Ltd., Aerosol-Service AG, Exal Corporation, Lindal Group, Nussbaum Matzingen AG, Tecnocap S.p.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Aerosol Packaging Market Segmentation

By Product Type

By Material

- Aluminum

- Tin-plated Steel

- Glass

- Plastic

By Propellant Type

- Compressed Gas

- Liquefied Gas

By End-Use Industry

- Personal Care

- Household Products

- Automotive

- Healthcare

- Others

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Aerosol Packaging Market

- Ball Corporation

- Crown Holdings Inc.

- Trivium Packaging

- Mauser Packaging Solutions

- CCL Industries Inc.

- Toyo Seikan Group Holdings Ltd.

- Ardagh Group S.A.

- Colep Packaging

- Nampak Ltd.

- CPMC Holdings Ltd.

- Aerosol-Service AG

- Exal Corporation

- Lindal Group

- Nussbaum Matzingen AG

- Tecnocap S.p.A.

* List Not Exhaustive

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous, data-driven methodology to deliver actionable insights into the global Aerosol Packaging Market. Our research combines primary data from interviews with packaging engineers, supply chain managers, brand owners, and regulatory experts, with secondary sources such as corporate filings, sustainability reports, trade journals, and regulatory databases. Market sizing, spanning USD 4.5 billion in 2025 to USD 10.5 billion by 2034 at a CAGR of 9.9%, is estimated through top-down and bottom-up approaches, considering product types (cans, bottles, others), materials (aluminum, tin-plated steel, glass, plastic), propellant types (compressed and liquefied gases), and end-use industries (personal care, household, automotive, healthcare). USDAnalytics also evaluates technological trends, including precision valves, low-GWP propellants, water-based formulations, and smart/connected packaging, alongside sustainability initiatives like high-recycled-content metals and monomaterial design. Regional insights cover the U.S., Germany, China, India, Brazil, and Japan, analyzing regulatory influence, circular economy mandates, and local manufacturing strategies. Competitive benchmarking assesses leaders such as Ball Corporation, Crown Holdings, AptarGroup, and Ardagh Group, highlighting capabilities in valve science, low-GWP readiness, and metal circularity. This methodology ensures industry professionals receive accurate, forward-looking intelligence for decision-making, sustainable design, and optimized product performance.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.