Metal Packaging Market Overview: Size, CAGR, and Key Industry Insights

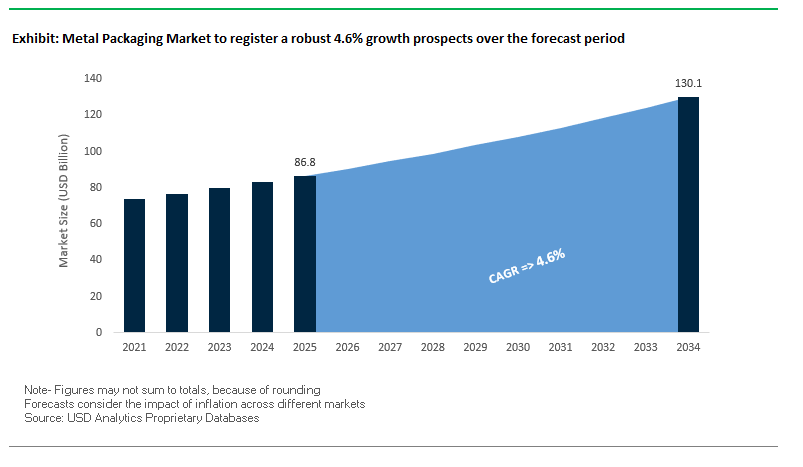

The global Metal Packaging Market is projected to grow from $86.8 billion in 2025 to $130.1 billion by 2034, registering a CAGR of 4.6%. This robust growth reflects increasing demand for sustainable, durable, and innovative packaging solutions across the food, beverage, and personal care industries. The market is driven by the growing preference for recyclable aluminum and steel packaging, lightweighting initiatives, and the integration of smart technologies that enhance consumer engagement. For industry professionals, key questions include how sustainability certifications influence purchasing decisions, the adoption rate of smart packaging, and the impact of lightweight designs on production efficiency and logistics.

Key Insights for Industry Stakeholders

- Infinite recyclability: Aluminum and steel cans can be recycled repeatedly without quality loss, supporting corporate circular economy goals.

- Sustainable certification trends: Companies increasingly pursue certifications like the Aluminum Stewardship Initiative (ASI) to demonstrate environmental responsibility.

- Lightweighting and efficiency: Thinner-walled cans and containers reduce material usage, transportation costs, and carbon footprint.

- Smart packaging adoption: QR codes and NFC-enabled metal packaging enhance customer engagement and brand storytelling.

- Broad application spectrum: Metal packaging is critical across beverages, food, aerosols, and home care products, reflecting its versatility and market penetration.

Recent Developments Driving the Global Metal Packaging Market

The metal packaging industry has experienced notable developments focused on sustainability, financial resilience, and capacity expansion. In August 2025, Ball Corporation completed the sale of 41% of its ownership in a Saudi Arabia joint venture to focus on core business operations. The same month, Crown Holdings received validation from the Science Based Targets initiative (SBTi) for its net-zero target, highlighting the increasing corporate emphasis on decarbonization and sustainability certifications.

In July 2025, Ardagh Group announced a comprehensive recapitalization transaction to significantly reduce its debt and strengthen its balance sheet, while Crown Holdings reported a 19% increase in adjusted diluted EPS for Q2 2025, driven by strong performance in its Americas beverage segment. May 2025 saw Crown expanding production with a new high-speed line in Ponta Grossa, Brazil, to meet rising regional demand.

Earlier in April 2025, Trivium Packaging released its 2024 Sustainability Report, noting a 2% reduction in Scope 1 and 2 greenhouse gas emissions. February 2025 featured Ball’s acquisition of Florida Can Manufacturing, enhancing aluminum production capacity in Florida. In January 2025, CPMC Holdings was delisted from the Hong Kong Stock Exchange following a compulsory acquisition. Looking back to November 2024, Sonoco Products Company’s acquisition of Eviosys positioned it as a leading global manufacturer of metal food and aerosol packaging.

Strategic Trends and Growth Opportunities in the Metal Packaging Market

Strategic Reshoring and Capacity Expansion for Supply Chain Resilience

The metal packaging market is experiencing a decisive push toward reshoring and regional capacity building as geopolitical disruptions, trade conflicts, and pandemic-era shortages exposed vulnerabilities in global supply chains. Governments across North America and Europe are actively supporting domestic investment to enhance resilience and ensure uninterrupted supply of essential food and beverage packaging.

In the U.S., policies under the Inflation Reduction Act and CHIPS & Science Act, coupled with the findings of the 2021–2024 Quadrennial Supply Chain Review, underscore a federal commitment to strengthen critical industries like packaging. These measures align with a whole-of-government approach to safeguard national and economic security by minimizing dependence on overseas supply. Likewise, the European Union’s reindustrialization agenda, long championed by the European Economic and Social Committee (EESC), reinforces the target of restoring manufacturing’s share of GDP to above 20%.

Industry leaders are responding with concrete capital projects. In late 2024, a leading packaging company announced the development of a new state-of-the-art facility in the southern U.S., designed to ensure faster lead times and reduce reliance on imports. Beyond cost savings, domestic production plays a strategic role in food security, guaranteeing that staples like soups, vegetables, and infant formula can be canned locally without risk from global supply shocks. This trend positions reshoring as both a commercial advantage and a national imperative.

Mandatory Adoption of Non-BPA and Polymer-Based Barrier Linings

Another transformative trend is the mandatory industry-wide transition to non-BPA and polymer-based barrier linings across food, beverage, and aerosol packaging segments. Driven by tightening regulations, this shift ensures compliance with food safety mandates while aligning with consumer expectations of healthier, safer products.

The European Union’s Commission Regulation (EU) 2024/3190, effective January 2025, delivers a comprehensive ban on BPA and derivatives in food contact coatings, with a compliance deadline of July 20, 2026. Beyond BPA, the regulation sets residual content and detection limits for other hazardous bisphenols, pushing the industry to rethink coating formulations entirely. Leading manufacturers like Trivium Packaging announced proactive conversion of lacquers to BPA-NI (non-intent) formulations in late 2024, well ahead of the mandated deadlines.

In the U.S., while federal regulations are less aggressive, the Can Manufacturers Institute reported in 2020 that 95% of food cans already contained BPA-free linings, driven by consumer demand and proactive corporate policies. This momentum reflects a global shift where compliance-driven innovation is no longer optional but essential, spurring massive R&D investment into next-generation barrier technologies that balance safety, durability, and sustainability.

Development of Advanced Alloys and Lightweighting for Scope 3 Emissions Reduction

With Scope 3 emissions reduction now a critical benchmark for global brands, packaging companies face mounting pressure to lower their carbon footprint through lightweighting and advanced alloy development. The industry has already achieved substantial reductions: the average can body thickness decreased from 0.42mm in the 1970s to 0.254mm today, representing a 39.5% reduction. Similarly, lid thickness has dropped from 0.39mm to 0.24mm, and smaller end diameters further reduce raw material use.

These advances have directly improved material efficiency. Whereas one pound of aluminum historically yielded 27 cans, today’s lightweighting allows 34 cans per pound of aluminum—a 26% productivity boost. Ongoing R&D into thinner yet stronger aluminum and high-strength steels is pushing the boundaries further, enabling more aggressive reductions without compromising can integrity. For brand owners under pressure to achieve sustainability pledges, lightweight metal packaging represents a measurable solution for Scope 3 reporting while also reducing costs for manufacturers.

Integration of Digital Watermarking for Circular Economy Infrastructure

The shift to a circular economy is unlocking opportunities through the integration of digital watermarking technologies, pioneered by the HolyGrail 2.0 initiative. With the EU Packaging and Packaging Waste Regulation (PPWR), approved in December 2024, mandating recycled content targets and design-for-recycling requirements, digital watermarking provides a scalable solution to enhance recycling efficiency.

Pilot programs in Germany, completed in late 2024, demonstrated that digital watermarking achieved detection accuracies of 87.9% to 93.8%, far outperforming traditional sorting methods. These invisible codes, embedded directly into packaging, allow high-speed optical sorting cameras to classify packaging with precision at speeds up to 3 meters per second. This improves the yield and purity of recycled metal streams, enabling manufacturers to meet strict EU targets while ensuring recycled materials can be reintegrated into new packaging.

Competitive Landscape of Global Metal Packaging Industry

The global metal packaging market is dominated by leading multinational manufacturers that focus on innovation, sustainability, and global operational scale. Companies are driving growth through strategic acquisitions, advanced material technologies, and sustainable initiatives. Below is an overview of top players shaping the market.

Ball Corporation: Expanding Aluminum Packaging Leadership

Ball Corporation is a global leader in sustainable aluminum packaging, serving beverages, home, and personal care markets. In February 2025, Ball acquired Florida Can Manufacturing, boosting production capacity in the southeastern U.S., and in August 2025, completed a major divestment in its Saudi Arabia joint venture to focus on core operations. The company emphasizes decarbonization, aiming to cut absolute value chain emissions by 16% by 2030 and achieve 100% renewable electricity. Ball’s portfolio includes lightweight ReAl alloy cans with high recycled content, alongside advanced printing and shaping technologies that differentiate brand offerings.

Crown Holdings, Inc.: Pioneering Net-Zero Metal Packaging Solutions

Crown Holdings operates in 39 countries, producing aluminum and steel beverage cans, food containers, and aerosol packaging. In August 2025, the company’s net-zero target received SBTi validation, while its Q2 2025 segment income rose 9% YoY. Crown’s Twentyby30 program is a comprehensive sustainability initiative targeting environmental, social, and governance goals. Its expertise in lightweighting and advanced coatings ensures products are both high-performing and sustainable, catering to global brand requirements.

Ardagh Group: Financial Restructuring to Support Sustainable Growth

Ardagh Group supplies recyclable metal and glass packaging, with a diverse portfolio including beverage, food, and aerosol cans. In July 2025, Ardagh launched a major recapitalization initiative to reduce debt and strengthen financial resilience. The company focuses on material-efficient and energy-conscious innovations, supporting high-growth segments such as energy drinks, sparkling water, and ready-to-drink beverages. Its extensive global footprint enables delivery of consistent quality and sustainability standards across markets.

Trivium Packaging: Leading Circular Economy Initiatives

Trivium Packaging provides recyclable metal packaging solutions with a focus on food, beverage, and aerosol cans. Its 2024 Sustainability Report, released in April 2025, highlights 47% of total revenue derived from eco-designed products. Trivium emphasizes circularity and lightweighting, providing design and technical support to customers to optimize sustainability and product launches. The company continues to be a leading innovator in eco-efficient metal packaging solutions.

Silgan Holdings Inc.: Comprehensive Rigid Packaging Solutions

Silgan Holdings produces a wide range of metal containers for food and pet food applications across North America and Europe. In July 2025, Silgan reported strong Q2 2025 results and declared its quarterly cash dividend in August 2025, continuing a long-standing record of shareholder returns. Its strategy blends organic growth with strategic acquisitions, giving Silgan a broad product portfolio and a competitive edge in serving diverse end markets.

Metal Packaging Market Share Insights

Cans Dominate Market Share by Product Type in the Global Metal Packaging Industry

Cans represent 68% of the total global metal packaging market, reflecting their unmatched versatility and efficiency across food, beverage, and aerosol applications. Aluminum beverage cans remain one of the most widely consumed packaging formats globally due to their light weight, fast chillability, infinite recyclability, and consumer familiarity, with demand accelerating in categories such as craft beer, sparkling water, and ready-to-drink cocktails. Steel food cans continue to underpin essential packaged goods, particularly in soups, sauces, and pet food, where preservation and robustness are paramount. Aerosol cans, though a smaller subcategory, also contribute to the strong volume base. The scale of production infrastructure, combined with regulatory and consumer emphasis on circular economy solutions, ensures that cans remain the core growth engine of the broader metal packaging sector, consistently outpacing closures, tins, and bottles in both volume and value.

Food and Beverage Companies Continue to Drive End-User Share in the Metal Packaging Industry

Food and beverage companies account for 75% of metal packaging demand, underscoring their role as the industry’s primary growth engine. Within beverages, aluminum cans dominate due to their superior shelf-life protection, logistical efficiency, and consumer-driven sustainability narrative, especially as leading global brands commit to higher post-consumer recycled (PCR) content. In food, steel cans remain indispensable for preserving fruits, vegetables, seafood, and pet food, enabling safe global distribution without refrigeration and ensuring nutritional integrity over years of storage. This segment also benefits from the rise of plant-based beverages, premium canned cocktails, and functional drinks, which expand the reach of metal cans beyond traditional categories. The entrenched reliance of multinational FMCG companies on cans for both staple foods and premium beverages, combined with their alignment with circular economy goals and government recyclability mandates, guarantees that the food and beverage sector will remain the undisputed driver of metal packaging consumption worldwide.

United States: State-Level EPR Laws and Recycling Initiatives Reshape the Metal Packaging Market

The U.S. metal packaging market is being reshaped by state-driven Extended Producer Responsibility (EPR) regulations, with California’s SB 54 standing out as a pivotal law that shifts the financial responsibility of packaging disposal and recycling to producers. This is accelerating the adoption of infinitely recyclable materials such as aluminum and steel, positioning metal packaging as a sustainable alternative to plastic. Alongside this regulatory momentum, the industry is witnessing rapid lightweighting innovations, where manufacturers are engineering thinner-walled aluminum and steel cans with advanced alloys. These solutions lower both production and transport costs while aligning with corporate sustainability targets.

From an investment perspective, Ball Corporation’s aluminum end facility in Kentucky exemplifies the sector’s expansion efforts to enhance North American supply chain resilience. Application growth is strongest in canned beverages, craft beer, soups, and pet foods, while rising home consumption and e-commerce logistics boost demand for durable and shelf-stable packaging. Recycling is also central to industry strategy, with the Aerosol Recycling Initiative—launched by the Can Manufacturers Institute (CMI) and HCPA—setting an ambitious 85% recycling target for aerosol cans nationwide. These combined drivers make the U.S. a global leader in sustainable and innovative metal packaging solutions.

Germany: Circular Economy Leadership and Premium Packaging Boost Market Growth

The German metal packaging market is strongly influenced by the European Union’s Circular Economy Action Plan and the Packaging and Packaging Waste Regulation (PPWR) adopted in January 2025. These policies reinforce minimum recycled content quotas and prioritize the use of high-value recyclable materials, boosting demand for aluminum and steel packaging. German manufacturers are at the forefront of can contouring innovations, producing asymmetrical and ergonomic packaging designs that enhance consumer appeal while delivering high functional performance.

Germany’s established deposit return system (DRS) and world-class recycling infrastructure support exceptionally high recycling rates for metal packaging. The country also remains a stronghold for sustainable packaging investments, with companies channeling resources into material efficiency and recyclability improvements. On the demand side, beverages and personal care products are the leading applications, supported by Germany’s high per capita consumption of canned beverages and aerosols. This combination of regulatory rigor, innovation leadership, and consumer-driven demand reinforces Germany’s role as Europe’s benchmark for circular economy practices in metal packaging.

China: Government Policy and Smart Packaging Technology Transform the Market

China’s metal packaging industry is advancing under strong government support for high-end manufacturing, with the Ministry of Industry and Information Technology’s 2025–2027 Aluminum Action Plan driving green development, technological innovation, and resource security. Additionally, the March 2025 expansion of the national Emissions Trading System (ETS) to include the aluminum and steel industries is compelling packaging producers to adopt low-carbon, energy-efficient production practices.

Chinese manufacturers are investing heavily in automation and digital printing technologies, enabling on-demand, customized can production for local and global FMCG brands. Innovations in smart packaging, such as QR-code-enabled cans, are also gaining traction, enhancing consumer engagement and traceability. Corporate investment is equally strong, with multinational FMCG companies expanding local facilities to shorten supply chains and meet growing domestic demand. These developments underscore China’s emergence as a global hub for sustainable, technologically advanced metal packaging solutions.

India: Policy Support and Rising Middle-Class Demand Drive Metal Packaging Growth

The Indian metal packaging market is gaining momentum through government-led programs such as Make in India and the Production Linked Incentive (PLI) scheme, which promote domestic manufacturing and attract investment into the packaging sector. Policymakers are also encouraging a circular economy model, where infinitely recyclable materials like aluminum and steel are prioritized. However, challenges such as compliance with the Quality Control Order (QCO) for steel products are creating transitional hurdles for producers, with the Metal Container Manufacturers’ Association (MCMA) actively engaging regulators to ensure smooth adoption of new standards.

From a technology standpoint, the market is shifting toward two-piece aluminum cans with lightweight and safety-enhanced features. A key example was Ball Corporation’s 2024 partnership with CavinKare, introducing retort aluminum cans for milkshake packaging. Applications are flourishing across the food and beverage sector, especially for ready-to-eat meals, supported by India’s rising disposable incomes and expanding middle class. Together, these factors make India one of the fastest-growing and most promising markets for metal packaging in Asia.

Brazil: Food Labeling Reforms and Strategic Investments Expand Market Opportunities

The Brazilian metal packaging market is being shaped by regulatory action from Anvisa, particularly RDC #

429/2020, which mandates front-of-pack warning labels on certain food products. This reform has pushed companies to redesign labels and packaging formats to align with new consumer transparency standards. Technological innovation is also adapting to Brazil’s unique logistics and climate challenges, with steel cans valued for their rigidity and resistance to internal pressure during transportation.

Corporate investments are significantly expanding capacity. JBS’s BRL 70 million investment in Zempack is increasing production of luncheon meat and aerosol cans, while CANPACK’s BRL 710 million aluminum beverage can plant in Poços de Caldas highlights global players’ confidence in Brazil’s growth potential. Market demand is strong in both food and beverage packaging and in the aerosol segment for personal care and household products, underscoring Brazil’s position as a strategic growth hub for Latin America’s metal packaging sector.

Metal Packaging Market Report Scope

Metal Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$86.8 Billion

|

|

Market Size (2034)

|

$130.1 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Material (Aluminum, Steel & Tinplate, Other Materials), By Product Type (Cans, Bottles, Drums & Barrels, Tins, Caps & Closures), By Application (Food & Beverage, Personal Care & Cosmetics, Automotive & Industrial, Pharmaceuticals & Healthcare, Others), By End-User (Food & Beverage Companies, Pharmaceutical Companies, Personal Care Product Manufacturers, Chemical & Industrial Product Manufacturers)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ball Corporation, Crown Holdings, Inc., Ardagh Group S.A., Trivium Packaging, Silgan Holdings Inc., Toyo Seikan Group Holdings, Ltd., Can-Pack S.A., ORG Technology Co., Ltd., Nampak Ltd., Sonoco Products Company, CPMC Holdings Limited, Mauser Packaging Solutions, Greif, Inc., Exal Corporation, Hindustan Tin Works Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Metal Packaging Market Segmentation

By Material

- Aluminum

- Steel & Tinplate

- Other Materials

By Product Type

- Cans

- Bottles

- Drums & Barrels

- Tins

- Caps & Closures

By Application

- Food & Beverage

- Personal Care & Cosmetics

- Automotive & Industrial

- Pharmaceuticals & Healthcare

- Others

By End-User

- Food & Beverage Companies

- Pharmaceutical Companies

- Personal Care Product Manufacturers

- Chemical & Industrial Product Manufacturers

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Metal Packaging Market

- Ball Corporation

- Crown Holdings, Inc.

- Ardagh Group S.A.

- Trivium Packaging

- Silgan Holdings Inc.

- Toyo Seikan Group Holdings, Ltd.

- Can-Pack S.A.

- ORG Technology Co., Ltd.

- Nampak Ltd.

- Sonoco Products Company

- CPMC Holdings Limited

- Mauser Packaging Solutions

- Greif, Inc.

- Exal Corporation

- Hindustan Tin Works Ltd.

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive, multi-faceted research methodology to provide actionable insights into the global Metal Packaging Market. The analysis combines primary research, including consultations with leading industry stakeholders such as manufacturers, distributors, and regulatory authorities, with secondary research from verified sources such as corporate filings, sustainability reports, industry journals, and government databases. Key market drivers—including sustainability certifications, non-BPA and polymer-based barrier adoption, lightweighting innovations, and smart packaging trends—are analyzed alongside macroeconomic, geopolitical, and regulatory factors impacting regional growth. Advanced modeling techniques, including CAGR projections, material- and product-type segmentation, and end-user demand analysis, are applied to forecast market size, value, and emerging opportunities. Corporate developments, including mergers and acquisitions, capacity expansions, and financial restructuring, are closely monitored for their impact on competitive positioning, while regional market evaluations covering the U.S., Europe, China, India, Brazil, and Japan provide nuanced perspectives on localized trends and technological adoption. This robust methodology ensures USDAnalytics delivers precise, industry-relevant intelligence for professionals seeking to navigate the evolving metal packaging ecosystem with confidence.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.