Food Container Market to Reach $577.2 Billion by 2034

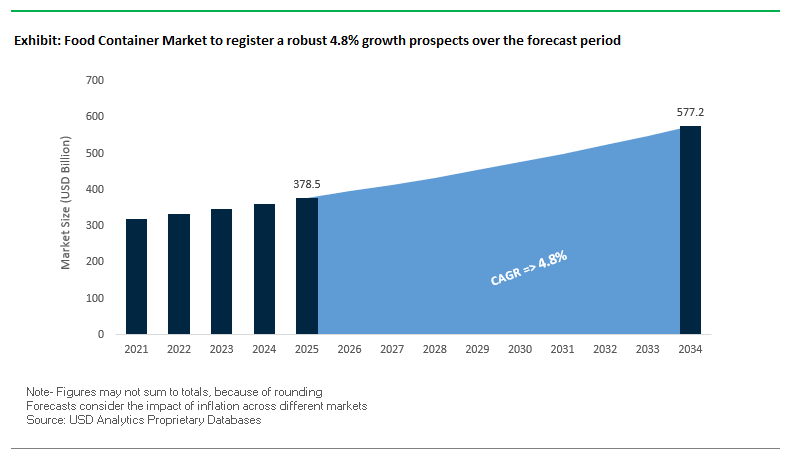

The global food container market is valued at $378.5 billion in 2025 and is expected to reach $577.2 billion by 2034, expanding at a CAGR of 4.8%. This growth is fueled by rising consumer demand for sustainable packaging, food safety, and functional design solutions.

The industry’s evolution is being shaped by the rapid adoption of eco-friendly materials, innovative functional designs, and technology-enabled packaging that improves food traceability and consumer engagement. Post-pandemic, hygiene and product integrity have also become critical purchase factors, driving innovation in antimicrobial coatings and advanced seal technologies.

Key Insights for Industry Stakeholders:

- Rise of Sustainable Materials: Transition from single-use plastics to bioplastics, plant-based fibers, and post-consumer recycled (PCR) content.

- Functional Design Priorities: Stackable, lightweight, and tamper-evident containers optimize logistics and ensure safety.

- Hygiene and Safety Emphasis: Antimicrobial coatings and improved seals improve consumer trust.

- Smart Packaging Growth: QR codes, NFC tags, and freshness indicators are enabling digital engagement and transparency.

Market Analysis: Strategic Developments Defining the Food Container Industry

The food container industry has undergone a series of high-impact corporate moves and product launches that demonstrate both consolidation and innovation.

In August 2025, Amcor reported strong Q4 earnings, reflecting the successful integration of its Berry Global acquisition earlier in the year, which significantly expanded its consumer packaging portfolio. This was followed by the July 2025 merger between Smurfit Kappa and WestRock, creating Smurfit WestRock a global packaging giant with unmatched scale in paper-based solutions. The same month, International Paper completed its $9.9 billion acquisition of DS Smith, further strengthening its European footprint.

In April 2025, WestRock partnered with Recipe Unlimited to introduce recyclable paperboard packaging expected to eliminate 31 million plastic containers from Canadian landfills, underlining the industry’s strong sustainability commitments. Similarly, Novolex launched containers with at least 10% PCR content in January 2025, reinforcing the trend toward circularity.

Meanwhile, Ball Corporation sold its aerospace division in February 2025 for $5.6 billion to sharpen focus on core packaging, while Berry Global completed the spin-off of its health division in November 2024, forming Magnera to prioritize consumer packaging. On the production front, Simak launched a canned tuna line in December 2024 in Oman with an annual output capacity exceeding 100 million cans, showing continuing investment in metal food containers.

Trends and Opportunities Transforming the Food Container Market

Unprecedented Regulatory Pressure Against Single-Use Plastics

The food container market is facing a compliance-driven transformation as governments worldwide enforce bans and restrictions on single-use plastic containers. The European Union’s Packaging and Packaging Waste Regulation (PPWR), which took effect in 2025, introduces a broad ban on plastic containers for food items such as fresh fruits, vegetables, and sauces, to be fully enforced by 2030. This regulation not only restricts plastic use but also mandates a 5% reduction in packaging volume, compelling brands to redesign food containers for sustainability and efficiency.

India has set another global benchmark with its nationwide ban on single-use plastics in July 2022, targeting plates, cutlery, and food containers. The ban is reinforced by strict Extended Producer Responsibility (EPR) regulations, which shift accountability for end-of-life packaging management onto manufacturers. Similarly, in North America, state-level legislation in California, Washington, and New York has created a fragmented regulatory environment, pressuring foodservice operators and packaging producers to proactively shift towards molded fiber, paperboard, and biocomposite solutions. This wave of regulatory pressure is not optional it is a non-negotiable market driver accelerating material substitution and structural innovation in food container design.

E-commerce and Delivery-First Packaging Design

The rise of food delivery platforms (DoorDash, Uber Eats, Deliveroo) and direct-to-consumer (DTC) food shipments is reshaping container functionality. Unlike traditional in-store packaging, delivery-first designs must ensure leak resistance, thermal retention, and stackability to withstand automated logistics and last-mile delivery challenges. A logistics industry report highlights that e-commerce has amplified the need for structurally reinforced packaging that protects against vibration, compression, and spillage across multiple handling points.

Food waste caused by inadequate packaging has further spotlighted this issue. In response, a major food delivery platform partnered with a restaurant chain to introduce modular, spill-proof containers specifically engineered for transport. These containers maintain freshness, prevent leakage, and integrate stackable geometries for efficient placement in delivery bags. Simultaneously, “right-sizing” has become a regulatory and corporate imperative. The EU PPWR mandates reduced empty space and discourages filler materials like foam or air cushions, pushing brands to adopt automated packaging systems that optimize material use and minimize shipping costs. The convergence of delivery logistics and regulatory mandates is cementing performance-engineered containers as the new industry standard.

Advanced Molded Fiber Manufacturing for Hot and Oily Foods

A key opportunity lies in scaling next-generation molded fiber containers that can withstand hot, oily, and liquid-rich foods while remaining PFAS-free, compostable, and recyclable. Historically, molded fiber has struggled in these applications due to oil resistance and heat durability limitations. Companies like Solenis are commercializing water-based and biowax-based barrier coatings (TopScreen™ series), which provide grease resistance for high-temperature applications without using harmful fluorochemicals.

Innovation is accelerating through additives such as microfibrillated cellulose (MFC), developed by Borregaard, which enhances water retention, prevents cracking, and improves overall fiber strength. Parallel to this, academic and industry partnerships are producing oven-safe, PFAS-free trays capable of withstanding temperatures up to 400°F, signaling breakthroughs in bio-based coatings. These advancements unlock new application areas such as fast-food trays, take-out boxes, and liquid-rich ready meals providing manufacturers with a scalable alternative to single-use plastics that meets regulatory compliance and consumer demand for safe, compostable solutions.

Integration of Digital Watermarks for Smart Waste Management

The growing complexity of multi-material coatings and fiber composites introduces contamination risks in recycling systems. Digital watermarking technology offers a transformative solution, enabling high-precision automated sorting while providing brands and regulators with critical data for circularity compliance. The HolyGrail 2.0 initiative has proven the industrial viability of this approach, achieving over 90% detection efficiency and processing nearly 56,000 items per day in German recycling trials.

These digital watermarks embed a “digital passport” into each container, carrying data on material composition, food residue, and end-of-life pathways (compostable vs. recyclable). This enables facilities to generate clean, high-quality recycling streams that were previously impossible, particularly for food-contact fiber containers. Beyond waste management, digital watermarks create new consumer engagement channels, allowing users to scan packaging for recycling instructions, sourcing information, or loyalty rewards. The alignment with EPR reporting requirements further enhances adoption, positioning digitally enhanced food containers as a strategic convergence of compliance, consumer trust, and material innovation.

Competitive Landscape: Innovation and M&A Driving Global Food Container Leaders

The global food container market is intensely competitive, led by multinational corporations with extensive portfolios and strong R&D capabilities, alongside specialized players focusing on material innovation and sustainable solutions. Strategic acquisitions, product launches, and sustainability commitments dominate competitive positioning.

Amcor: Expanding Global Reach with Berry Global Acquisition

Amcor has emerged as a powerhouse in 2025 following its acquisition of Berry Global, creating a leading packaging supplier across food, beverage, and healthcare. Its AmPrima™ recycle-ready portfolio and AmFiber™ paper-based solutions reflect its focus on sustainable, high-barrier materials. Supported by its global innovation centers and ASSET™ lifecycle assessment tools, Amcor enables customers to meet strict environmental targets while ensuring packaging performance.

Berry Global: Refocusing Portfolio with Sustainability-Driven Offerings

Berry Global, despite spinning off its health division in November 2024, remains a strong player in rigid and flexible food containers. The company emphasizes circularity, with containers developed using post-consumer recycled content. Its strong presence in foodservice and ready-meal packaging, including trays, tubs, and cups, positions it as a reliable partner for large-scale food companies.

Ardagh Group: Strengthening Glass and Metal Food Container Leadership

Ardagh Group continues to dominate the metal and glass food container segment, with products used for canned vegetables, sauces, jams, and beverages. Its lightweighting innovations reduce material costs and emissions, while specialty coatings provide shelf stability and branding flexibility. The company’s reputation for reliability and sustainability makes it a preferred partner for leading global food brands.

Huhtamaki: Pioneering Fiber-Based and Compostable Packaging

Huhtamaki is advancing fiber-based and recyclable food containers with a strong sustainability agenda. Recent innovations include recyclable ice cream packaging and egg cartons made from 100% recycled fiber, launched in the U.S. Its strategic focus on “protecting food, people, and the planet” underlines its role as a global sustainability leader in consumer and foodservice packaging.

Silgan Holdings: Specializing in Rigid Packaging and Can Innovation

Silgan Holdings is a dominant force in rigid metal and plastic food containers. Its focus on easy-open and peel-off lids enhances consumer convenience, while its BPA-NI coatings address regulatory and health concerns. Silgan’s diverse range of cans for fruits, vegetables, seafood, and pet food underscores its role as a critical supplier in both food retail and industrial supply chains.

Food Container Market Share Insights

Bags and Pouches Hold Largest Market Share by Product Type in Food Containers

In 2025, bags and pouches capture 35% of the food container market, making them the leading product type due to their unmatched sustainability, cost efficiency, and flexibility. Lightweight pouches not only reduce material use and transportation costs but also deliver superior barrier properties that extend shelf life across snacks, frozen foods, and dry goods. Their dominance is reinforced by their role in meeting FMCG sustainability commitments and their branding advantage through high-quality digital and flexographic printing. Trays and containers, at 25%, remain critical for ready meals, fresh produce, and proteins where rigidity and leak prevention are non-negotiable, particularly with modified atmosphere packaging (MAP). Bottles and jars continue to provide premium appeal in sauces, oils, and baby food, while cups, bowls, and cans serve important niches in on-the-go consumption and shelf-stable categories. Together, these insights highlight how bags and pouches drive flexible, sustainable growth, while rigid trays and bottles protect high-value perishables and premium-positioned products.

Ready Meals and Convenience Foods Lead Market Share by Application in Food Containers

By application, ready meals and convenience foods hold the largest share at 30% of the food container market in 2025, underscoring how changing consumer lifestyles are reshaping packaging demand. Microwave-safe trays, dual-ovenable fiber-based containers, and portion-controlled packs dominate this segment, meeting consumer preference for speed, portability, and safety. The segment’s growth is amplified by meal kit subscriptions, supermarket-ready heat-and-eat formats, and the rising adoption of recyclable and compostable trays. Fruits and vegetables follow with 25%, where the transition away from plastic clamshells to molded fiber and cardboard trays is accelerating under retailer and regulatory pressure. Meat, poultry, and seafood remain highly protective applications, with absorbent pad-lined trays ensuring safety and hygiene. Bakery and confectionery leverage containers for branding and freshness, while dairy continues to rely on tubs, bottles, and coated paperboard. Collectively, the end-use distribution reflects how ready meals shape convenience-driven innovation, fresh produce accelerates plastic-free transitions, and proteins anchor safety-focused packaging.

United States: Driving Sustainability and PFAS-Free Food Containers for E-Commerce

The U.S. food container market is increasingly focused on sustainability and the use of post-consumer recycled (PCR) content. Companies like Pactiv Evergreen are introducing Recycleware Reduced-Density Polypropylene meat trays as sustainable alternatives to foam polystyrene, addressing environmental concerns while appealing to eco-conscious consumers. There is also a strong industry-wide push to eliminate per- and polyfluoroalkyl substances (PFAS) from food containers, with new lines of molded fiber packaging designed to comply with state-level regulations and meet consumer demand for safe, PFAS-free options. The rapid growth of e-commerce and food delivery platforms is fueling demand for durable, lightweight containers that maintain product integrity during shipping. Additionally, technological advancements, including QR codes and RFID tags, are being integrated into containers to provide transparency on origin, nutritional content, and recycling instructions, enhancing consumer engagement and trust.

Germany: Leading Circular Economy Practices and Innovative Sustainable Materials

Germany’s food container market is at the forefront of Europe’s circular economy, driven by high recycling rates and regulations such as the German Packaging Act (VerpackG) and the EU Packaging and Packaging Waste Regulation (PPWR). The market is innovating with sustainable and reusable materials, exemplified by collaborations between companies like Alpla and German start-ups to produce fully recyclable PET containers for personal care products, a trend that reflects cross-industry application potential for sustainable packaging. The industry is also focused on advanced functionality, including the development of paper-based trays for sensitive foods, providing high barrier properties while reducing environmental impact. Germany’s strong regulatory framework, commitment to sustainability, and technological investments make it a leader in eco-friendly food container solutions.

China: Governmental Regulations and Innovative Solutions for Sustainable Containers

China’s food container market is shaped by robust governmental policies promoting sustainability, including plastic bans and waste management regulations, which encourage the adoption of reusable containers made from durable materials such as polypropylene. National standards like GB 4806.8-2022 for food-contact paper and paperboard ensure product safety and regulatory compliance, supporting high-quality production. Companies are also addressing waste from online food delivery, with initiatives such as Meituan’s “opt-out for disposable cutlery” feature, which over 70% of orders in Shanghai currently use. The combination of regulatory compliance, governmental sustainability initiatives, and environmental responsibility is accelerating innovation in China’s food container industry.

India: Make in India and Technological Advancements Fuel Market Growth

India’s food container industry is benefiting from the “Make in India” initiative and liberal FDI policies, attracting global players and driving growth in local manufacturing. Technological advancements, including AI-based automation and smart packaging, are enhancing product functionality and positioning India as a potential global hub for food and packaging materials. Government support through initiatives like Mega Food Parks and Agro-Processing Clusters by the Ministry of Food Processing Industries (MoFPI) provides a strong foundation for market expansion. Additionally, the rapid rise of organic and healthy food consumption is fueling demand for containers that align with consumer preferences for sustainable and premium-quality packaging.

Brazil: Regulatory Standards and Bioplastic Innovation Driving Sustainable Containers

Brazil’s food container market is experiencing growth due to regulatory updates by the Brazilian Health Regulatory Agency (Anvisa), with a new framework implemented in 2024 to ensure food safety and uniform packaging standards. The industry is also pioneering the development of bioplastics, such as green polyethylene derived from sugarcane ethanol, reducing reliance on fossil fuels and improving environmental sustainability. Strong e-commerce growth is creating demand for lightweight, durable packaging that lowers shipping costs and material use. Furthermore, the adoption of innovative packaging solutions supports new product launches, including plant-based foods, highlighting Brazil’s focus on sustainability and technological innovation.

Japan: Bio-Based Packaging, Quality Focus, and Updated Food Contact Standards

Japan’s food container market is increasingly adopting bio-polypropylene (bio-PP) to meet sustainability goals and reduce greenhouse gas emissions. Companies are leveraging bio-based raw materials to produce food packaging that addresses environmental concerns while maintaining product quality. The market places high importance on premium aesthetics and functional design, encouraging brands to utilize high-quality materials and decorative printing techniques. Additionally, revisions to Japan’s food contact material standards, including updated requirements for synthetic resin, glass, and metal containers, ensure improved product safety and compliance. The combination of sustainability initiatives, quality-driven innovation, and regulatory oversight positions Japan as a key leader in the global food container market.

Food Container Market Report Scope

Food Container Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$378.5 Billion

|

|

Market Size (2034)

|

$577.2 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Material (Plastics, Glass, Metal, Paper and Paperboard, Bioplastics), By Product Type (Bags & Pouches, Trays & Containers, Bottles & Jars, Cans, Cups & Bowls, Other Containers), By Application (Fruits & Vegetables, Meat, Poultry & Seafood, Dairy & Dairy Products, Bakery & Confectionery, Ready Meals & Convenience Foods, Other Applications), By End-Use (Food Service, Retail, Households)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global Group, Inc., Silgan Holdings Inc., Ball Corporation, Crown Holdings Inc., Ardagh Group S.A., Sonoco Products Company, Pactiv Evergreen Inc., Huhtamaki Oyj, WestRock Company, Graphic Packaging Holding Company, TC Transcontinental Inc., Greif, Inc., Mondi Group, DS Smith Plc

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Food Container Market Segmentation

By Material

- Plastics

- Glass

- Metal

- Paper and Paperboard

- Bioplastics

By Product Type

- Bags & Pouches

- Trays & Containers

- Bottles & Jars

- Cans

- Cups & Bowls

- Other Containers

By Application

- Fruits & Vegetables

- Meat

- Poultry & Seafood

- Dairy & Dairy Products

- Bakery & Confectionery

- Ready Meals & Convenience Foods

- Other Applications

By End-Use

- Food Service

- Retail

- Households

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Food Container Market

- Amcor plc

- Berry Global Group, Inc.

- Silgan Holdings Inc.

- Ball Corporation

- Crown Holdings Inc.

- Ardagh Group S.A.

- Sonoco Products Company

- Pactiv Evergreen Inc.

- Huhtamaki Oyj

- WestRock Company

- Graphic Packaging Holding Company

- TC Transcontinental Inc.

- Greif, Inc.

- Mondi Group

- DS Smith Plc

*List not Exhaustive

Research Coverage

This USDAnalytics report investigates the global Food Container Market, focusing on innovations, sustainability initiatives, and regulatory drivers that are transforming the industry. The analysis reviews breakthroughs in eco-friendly materials, advanced molded fiber, bioplastics, and technology-enabled containers that enhance food safety, hygiene, and consumer engagement. The report highlights strategic corporate developments, including mergers, acquisitions, capacity expansions, and product launches that are reshaping the competitive landscape. This report is an essential resource for packaging manufacturers, brand owners, foodservice operators, and investors seeking insights into material substitution, smart packaging trends, and regulatory compliance. By connecting historical performance from 2021 to 2024 with forecast projections for 2025 to 2034, USDAnalytics provides actionable intelligence on emerging opportunities, market segmentation dynamics, and global growth patterns.

Scope Highlights

- Segmentation: By Material (Plastics, Glass, Metal, Paper and Paperboard, Bioplastics), By Product Type (Bags & Pouches, Trays & Containers, Bottles & Jars, Cans, Cups & Bowls, Other Containers), By Application (Fruits & Vegetables, Meat, Poultry & Seafood, Dairy & Dairy Products, Bakery & Confectionery, Ready Meals & Convenience Foods, Other Applications), By End-Use (Food Service, Retail, Households)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic and Forecast Data: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies: Analysis/profiles of 15+ leading companies including Amcor, Berry Global, Silgan Holdings, Ball Corporation, Crown Holdings, Ardagh Group, Sonoco, Pactiv Evergreen, Huhtamaki, WestRock, and others.

Methodology

USDAnalytics applies a comprehensive research methodology combining primary and secondary data collection to deliver precise, actionable insights for the Food Container Market. Primary research involved interviews with packaging manufacturers, foodservice operators, regulatory experts, and sustainability consultants to capture firsthand perspectives on innovation, material adoption, and compliance strategies. Secondary research included detailed reviews of company reports, investor presentations, patent filings, regulatory documents, and trade publications to validate market trends and benchmark performance. Market sizing and forecasts were determined using a blend of top-down and bottom-up approaches, considering production capacities, consumption trends, and adoption rates across product types, materials, applications, and end-uses. Triangulation and scenario modeling were applied to reconcile historical data (2021–2024) with forward-looking projections (2025–2034), ensuring reliability and strategic relevance for industry stakeholders.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.