Disposable Cutlery Market Overview: Scaling to $21.1 Billion by 2034 on Policy Bans, Bio-materials, and On-the-Go Demand (CAGR 5.2%)

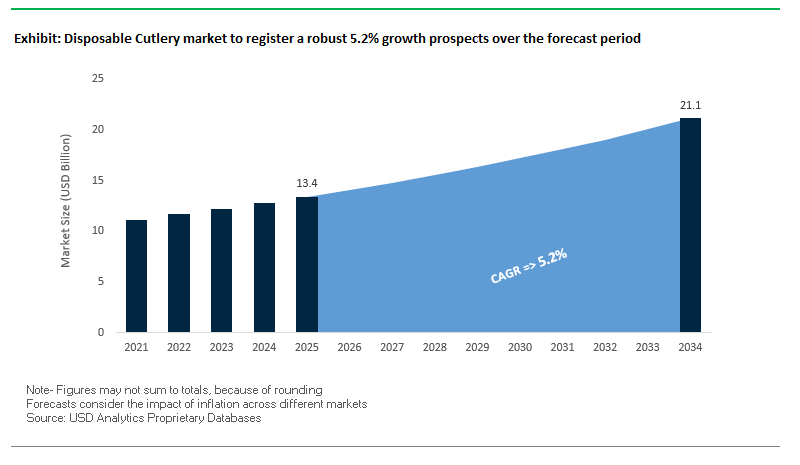

The global disposable cutlery market will grow from $13.4 billion in 2025 to $21.1 billion by 2034, posting a 5.2% CAGR. At the crossroads of convenience, compliance, and circularity, the category is being reshaped by single-use plastic restrictions, rapid food-delivery adoption, and branded sustainability. For procurement leaders and packaging engineers, the decision points are clear: which compostable or recyclable material platforms scale compliantly across regions; how to balance unit cost vs. performance for hot/greasy foods; and how to future-proof against tightening EPR and PFAS policies while keeping SKUs simple for operations.

Key Insights for buyers and specifiers

- Policy-Driven Shift: 100+ countries have enacted single-use plastic restrictions, creating mandated demand for sustainable disposable cutlery alternatives.

- Bio-based & Recycled Inputs: Next-gen SKUs leverage PLA/CPLA and agri-residue biopolymers, plus recycled content pathways, answering consumer and regulatory sustainability requirements.

- On-the-Go Acceleration: Exploding delivery/take-away with India’s cloud kitchens alone expected near $15B by 2025 keeps forks/knives/spoons mission-critical for foodservice throughput.

- Design & Aesthetics: Wood/bamboo and premium finishes provide a natural look and improved hand-feel, aligning with eco-centric brand identities and front-of-house presentation.

Market Analysis: Regulatory Momentum, Compostable Platforms, and Capacity Investments (2024–2025)

Sustainability launches and plant-fiber platforms are scaling fast. In September 2025, Sabert Europe (with Flexeserve) launched PulpUltra, a recyclable, film-sealable hot-food range that complements plant-based compostable cutlery programs across QSR and delivery. In August 2025, Hong Kong opened a public consultation to implement a full ban on plastic cutlery by 2025, underscoring Asia’s regulatory push toward fiber and bio-based utensils. One month prior (July 2025), Huhtamaki rolled out fiber-based, home & industrial-compostable ice-cream cups, highlighting end-to-end compostable serviceware ecosystems that typically bundle compostable spoons.

Compostable portfolios expand; bans tighten. In June 2025, Eco-Products, Inc. added certified-compostable foodservice items, widening SKU coverage for operators transitioning away from traditional plastics. A major white paper in March 2025 emphasized China’s 2020 policy phasing out non-degradable single-use plastics, with takeout cutlery eliminated in key cities by end-2025, accelerating supplier shifts to fiber and bioplastics. Capacity and localization also advanced: in January 2025, Genpak announced a $6.69M expansion in Scottsburg, Indiana, signaling confidence in sustained North American demand.

Technology and materials innovation reduce plastic dependence. In November 2024, Dart Container and PulPac brought dry-molded fiber production to North America high-speed cellulose conversion that cuts energy and water vs. conventional molded fiber. Earlier, May 2024, Dart’s SOLO® Bold Hold™ paperware showed how paper-first platforms pair with compostable cutlery to deliver cohesive, PFAS-free serving solutions. Net-net: 2024–2025 developments confirm a durable migration from polystyrene/PP toward CPLA, molded fiber, and wood/bamboo, with parallel investments to meet policy clocks and high-growth delivery use cases.

Trends and Opportunities Transforming the Disposable Cutlery Market

Legislative-Driven Material Substitution Away from Conventional Plastics

One of the most powerful dynamics reshaping the disposable cutlery market is the global wave of legislation banning single-use plastic items. The European Union’s Single-Use Plastics Directive (SUPD), effective since July 2021, banned the sale and distribution of plastic cutlery, plates, and straws across member states. This has forced brand owners and suppliers to pivot to certified compostable, fiber-based, or wood-based alternatives. Similar measures in India (July 2022) and Canada (December 2022) eliminated plastic cutlery from manufacture, import, and sale, compelling suppliers to invest in alternative material development at scale. To accelerate this transition, governments have also introduced direct financial support. For instance, India pledged $67 million to back biodegradable packaging innovation, signaling a broader move to make eco-friendly cutlery economically viable. As a result, the cutlery supply chain is experiencing a non-voluntary restructuring, where compliance is no longer optional but a prerequisite for market participation.

Consumer-Led Demand for Home-Compostable and Certified Materials

Beyond regulatory compliance, consumer preference is steering the market toward home-compostable and third-party-certified products. Brands are now expected to move past the “not plastic” narrative to offer positively sustainable solutions that align with circular economy principles. Certifications such as ASTM D6400 and EN 13432 for compostability are increasingly shaping purchasing decisions. A leading brand recently launched PLA-based cutlery derived from corn starch that degrades within six months in a home composting setup, providing consumers with verifiable end-of-life sustainability. Corporate buyers are equally critical drivers, as companies seek certified compostable cutlery for internal use and large-scale events to meet waste diversion and ESG goals. This consumer and corporate pressure is positioning bio-based cutlery with credible certifications as a market differentiator, enhancing adoption across foodservice chains and quick-service restaurants.

Development of High-Performance, Marine-Degradable Biopolymers

The next frontier of growth lies in marine-degradable cutlery solutions that address the issue of plastic waste in oceans and freshwater systems. Traditional compostable plastics such as PLA degrade only in industrial composting environments, but new biopolymers like polyhydroxyalkanoates (PHAs) and cellulose-fiber composites are being engineered to degrade in marine conditions. In 2025, Panasonic Holdings Corporation announced a breakthrough cellulose-based material with durability for use and biodegradability in marine settings, underscoring corporate commitment to this innovation pathway. Academic research also validates PHAs as a promising marine-degradable solution, aligning scientific backing with commercial development. Considering that 80% of marine litter is plastic (European Commission), cutlery that naturally degrades in water environments represents not just an innovation, but a necessary solution to global marine pollution. This category has the potential to attract premium pricing and regulatory incentives, while positioning suppliers as leaders in next-generation sustainability.

Integrated Reusable System Infrastructure for Food Delivery

A transformative opportunity for the disposable cutlery industry is to evolve beyond disposability by creating closed-loop reusable systems tailored to food delivery and takeaway markets. Case studies in China demonstrate that reusable polypropylene-based packaging systems can reduce emissions by up to 63% compared to single-use alternatives. Manufacturers that invest in reverse logistics infrastructure including collection, sanitization, and redistribution can shift from a one-time product sales model to a service-based revenue model. By integrating tracking technologies, deposit-return schemes, and partnerships with washing facilities, companies can build long-term client relationships and recurring income streams. The key to scaling these systems lies in ensuring consumer convenience and trust in hygiene standards, particularly through certified sanitization processes. As food delivery continues to grow globally, this opportunity provides a pathway for manufacturers to diversify offerings and align with circular economy frameworks.

Competitive Landscape: Leaders Advancing Compostability, Scale, and Performance

The disposable cutlery market blends global scale manufacturers and sustainability specialists. Competitive edges hinge on compostability certifications, heat & rigidity performance, ban-readiness by region, and reliable supply under surging delivery volumes.

Large incumbents provide cost, scale, and distribution certainty, while innovators bring PFAS-free chemistries, dry-molded fiber throughput, and bio-resin engineering. Buyers should benchmark on ASTM/EN compostability, cut/snap strength, hot-fill tolerance, life-cycle impacts, and SKU simplicity for back-of-house operations.

Dart Container Corporation scales sustainable alternatives with Solo® reach

Dart’s Solo® brand spans polystyrene and sustainable alternative cutlery, giving operators broad spec flexibility during transitions. Massive vertical integration (materials, inks, equipment) underpins cost control and supply security. Recent moves include partnering with PulPac to deploy dry-molded fiber in North America (Nov 2024), enabling high-speed cellulose cutlery as bans advance. Dart’s distribution depth across foodservice, healthcare, education, and retail keeps fulfillment resilient during demand spikes.

Huhtamaki Oyj extends compostable ecosystems across global QSRs

A foodservice packaging giant, Huhtamaki complements cups/containers with compostable disposable cutlery aligned to its blueloop sustainability platform. In July 2025, its compostable fiber cups reinforced end-to-end compostable setups where spoons and stirrers must meet home/industrial standards. With 40+ production units and marquee accounts (e.g., global QSRs), Huhtamaki’s strengths are R&D, barrier science, and dependable multi-region rollouts.

Genpak LLC boosts U.S. capacity to meet delivery-led demand

Genpak’s portfolio covers polystyrene, PET, and plant-based bioplastics across tableware and cutlery. Its $6.69M capex (Scottsburg, IN; Jan 2025) expands throughput for growth categories and regional lead-time reduction. Strategically focused on operator experience, Genpak engineers cutlery and serviceware to be microwave-safe, value-optimized, and compatible with off-premise workflows.

Sabert Corporation accelerates plant-based, PFAS-free performance

Sabert’s Green Collection features CPLA compostable cutlery engineered for rigidity and heat resistance. In Sep 2025, Sabert Europe launched PulpUltra (recyclable, >95% plant-fiber hot-food boxes), and the company pioneers “no intentionally added PFAS” solutions key for regulatory compliance and brand safety. Its strength lies in design + materials science, delivering leak-resistant, durable systems for catering, grocery, and food distributors.

Eco-Products, Inc. specializes in third-party-certified compostables

A pure-play sustainability leader, Eco-Products offers plant-based disposable cutlery (e.g., CPLA, sugarcane-derived solutions) validated by independent compostability certifications. In June 2025, it broadened its compostable line to help operators replace banned plastics at scale. Core advantages: education and end-of-life guidance for customers, plus a portfolio tuned to commercial composting infrastructure and circular economy goals.

Disposable Cutlery market Share Insights

Spoons Dominate Market Share by Product Type

Spoons account for 35% of the disposable cutlery market in 2025, making them the largest product category by volume. Their dominance stems from their universal application across both liquid and semi-solid food categories, including soups, yogurts, cereals, desserts, and ice creams. Unlike forks or knives, spoon design does not require complex structural reinforcement, allowing them to transition more seamlessly from conventional plastics to sustainable alternatives like wood, bamboo, or compostable bioplastics. This ease of substitution makes spoons the preferred choice for large-scale adoption in foodservice operations where compliance with single-use plastic bans is accelerating. Forks, with a 30% share, remain the standard for solid foods such as salads, rice, and pasta. However, innovation challenges persist, as eco-materials must replicate the rigidity and tine strength of plastic without compromising user experience, positioning forks as a critical focus area for material science advancements. Knives represent a smaller but functionally significant share, especially in spreading applications and for softer foods. Their reliance on sturdier, sharper edges makes them harder to replicate with compostable materials, keeping them a niche but essential segment. Sporks are gaining traction in fast-food and takeaway environments, offering operational efficiency by reducing the number of utensils needed, while niche items like chopsticks, stirrers, and tasting spoons maintain relevance in regional and specialty dining experiences.

Food & Beverage Services Anchor Market Share by End-Use Industry

The food and beverage service sector commands 80% of the disposable cutlery market in 2025, making it the undisputed driver of demand and innovation. This segment, encompassing quick-service restaurants (QSRs), cafes, catering services, and institutional cafeterias, sits at the center of regulatory pressure as global bans on single-use plastics reshape procurement practices. Large-scale buyers in this category are shifting aggressively to wood, bamboo, CPLA, and molded fiber options to meet compliance requirements while also improving brand image among environmentally conscious consumers. The scale of foodservice operations makes this segment the largest testing ground for cost-effective, compostable, and recyclable solutions, with purchasing decisions heavily influenced by total cost-in-use and regulatory alignment. In contrast, the household segment remains more fragmented and price-sensitive, with traditional plastic cutlery still retaining shelf presence due to affordability and convenience for occasional use such as parties or picnics. However, the rise of eco-conscious consumerism is steadily expanding the retail footprint of compostable household cutlery. Other end-users including schools, hospitals, airlines, and emergency relief programs represent a smaller but strategically important segment. Their procurement priorities focus on bulk, cost-efficiency, and increasingly, adherence to institutional sustainability mandates. This group is becoming a key adopter of large-scale compostable cutlery solutions that balance durability with compliance, particularly in government- or NGO-driven procurement systems.

United States: Sustainability and E-Commerce Driving Disposable Cutlery Innovations

The U.S. disposable cutlery market is undergoing a major transformation, driven by a strong focus on sustainability and eco-friendly alternatives. Companies are launching innovative products made from plant-based plastics (PLA), FSC-certified wood, and compostable materials, reflecting growing consumer demand and regulatory pressures. For example, Sabert Corp.’s EcoEdge Paper Cutlery line features forks, spoons, and knives crafted from renewable resources, emphasizing biodegradability and environmental responsibility.

Rising online food delivery services are a significant market driver, as the single-use and hygienic properties of disposable cutlery make it an essential component for quick-service restaurants and delivery platforms. To meet this surge, manufacturers like Georgia-Pacific LLC are investing heavily, with a $425 million expansion of the Dixie manufacturing facility in Tennessee, aimed at increasing production capacity and ensuring a steady supply of sustainable disposable tableware. The emphasis on lightweight, compostable, and biodegradable materials continues to shape product development across the U.S., aligning with both consumer trends and evolving state-level regulations.

United Kingdom: Regulatory Push Accelerates Shift to Sustainable Alternatives

The UK disposable cutlery market is heavily influenced by government regulations, particularly the ban on single-use plastic cutlery that came into effect in England in October 2023, with Scotland and Wales following similar policies. This regulatory framework has accelerated the adoption of sustainable alternatives such as wood, sugarcane pulp, and bioplastics, driving innovation in eco-friendly and biodegradable cutlery products.

Consumer demand for environmentally responsible solutions is equally significant, prompting manufacturers to focus on compostable, renewable, and functional designs. Wooden cutlery with bio-based coatings and other innovative materials are becoming mainstream, reflecting a market that combines regulatory compliance with eco-conscious branding. The UK market is now a leading example of how policy, consumer preference, and sustainability innovation intersect to transform disposable cutlery offerings.

Germany: Circular Economy Principles Shape the Disposable Cutlery Market

Germany is at the forefront of the European disposable cutlery market’s transition to a circular economy. The industry is heavily focused on developing products with high recycled content, ensuring they are easily recyclable or compostable, in alignment with both EU directives and national environmental policies.

A significant trend is the shift from conventional plastic to plant-based materials, including wood, bamboo, and other renewable resources. German consumers and businesses place high value on quality, durability, and aesthetic appeal, especially for catering and food service applications. Companies are innovating to ensure that eco-friendly disposable cutlery not only meets functional requirements but also provides a premium feel, helping maintain competitiveness in the high-end market segment.

China: Manufacturing Powerhouse with Growing Sustainable and Edible Cutlery Trends

China’s disposable cutlery market is driven by its role as a global manufacturing hub, producing a wide range of high-volume, cost-effective cutlery products for both domestic and international markets. The country’s large domestic consumer base and rising environmental awareness are fueling demand for sustainable cutlery made from bagasse, wood, and plant-based bioplastics.

Innovations such as edible cutlery crafted from wheat, rice, and corn are gaining attention, offering a zero-waste solution to plastic pollution. These developments reflect China’s dual focus on scalable production efficiency and environmentally friendly alternatives, ensuring the market can meet growing global demand while addressing sustainability concerns.

India: Regulatory Action and Bio-Based Materials Drive Market Growth

The Indian disposable cutlery market has experienced accelerated growth following the government’s Plastic Waste Management (Amendment) Rules, effective from July 1, 2022, which banned several single-use plastic items including cutlery. This regulatory push has spurred the adoption of eco-friendly and compostable alternatives, primarily bagasse-based cutlery, contributing to a circular economy and waste reduction initiatives.

Rising demand from the food service and e-commerce sectors is another key growth driver. The rapid expansion of online food delivery platforms and packaged meal services has created a need for cost-effective, hygienic, and sustainable cutlery solutions. Domestic manufacturers are investing in new production facilities and innovative technologies to meet local and export demands, positioning India as a growing hub for sustainable disposable cutlery in the Asia-Pacific region.

Disposable Cutlery Market Report Scope

Disposable Cutlery market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$13.4 Billion

|

|

Market Size (2034)

|

$21.1 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Material (Plastics, Wood, Bio-based & Compostable Materials), By Product Type (Spoons, Forks, Knives, Sporks, Other Cutlery Items), By End-Use Industry (Food & Beverage Service, Household, Other End-Users)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Huhtamaki Oyj, Dart Container Corporation, Pactiv Evergreen Inc., Genpak, LLC, Sabert Corporation, Vegware Ltd., Novolex, Georgia-Pacific LLC, BioPak, T&T Trading Company, Inc., BillerudKorsnäs AB, Fuling Global Inc., Visy Industries, Ecoware, Karat by Lollicup Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Disposable Cutlery Market Segmentation

By Material

- Plastics

- Wood

- Bio-based & Compostable Materials

By Product Type

- Spoons

- Forks

- Knives

- Sporks

- Other Cutlery Items

By End-Use Industry

- Food & Beverage Service

- Household

- Other End-Users

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Disposable Cutlery market

- Huhtamaki Oyj

- Dart Container Corporation

- Pactiv Evergreen Inc.

- Genpak, LLC

- Sabert Corporation

- Vegware Ltd.

- Novolex

- Georgia-Pacific LLC

- BioPak

- T&T Trading Company, Inc.

- BillerudKorsnäs AB

- Fuling Global Inc.

- Visy Industries

- Ecoware

- Karat by Lollicup Inc.

* List Not Exhaustive

Research Coverage

This USDAnalytics report investigates the dynamic growth and technological advancements in the global disposable cutlery market, providing a comprehensive examination of regulatory, material, and operational developments reshaping the industry. The analysis reviews market breakthroughs in bio-based, compostable, and marine-degradable materials, highlighting innovations from cellulose-based fibers, PLA/CPLA, and bamboo to edible cutlery solutions. The report also highlights market drivers such as policy bans on single-use plastics, surging demand from food delivery and e-commerce channels, and sustainability mandates influencing corporate procurement strategies. By combining historic data (2021–2024) with detailed forecasts through 2034, this report is an essential resource for packaging engineers, sustainability managers, and procurement leaders seeking insights on scaling eco-friendly cutlery solutions, mitigating regulatory risk, and aligning material performance with operational efficiency. USDAnalytics further provides in-depth company profiles, strategic developments, and regional dynamics, allowing readers to evaluate competitive positioning, emerging technologies, and future-ready solutions within the disposable cutlery ecosystem.

Scope Highlights:

- Segmentation: By Material (Plastics, Wood, Bio-based & Compostable Materials), By Product Type (Spoons, Forks, Knives, Sporks, Other Cutlery Items), By End-Use Industry (Food & Beverage Service, Household, Other End-Users)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historic & Forecast Data: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies: Analysis/profiles of 15+ leading manufacturers, including Huhtamaki Oyj, Dart Container Corporation, Pactiv Evergreen Inc., Genpak, LLC, Sabert Corporation, Vegware Ltd., Novolex, Georgia-Pacific LLC, BioPak, and others

Methodology

The research methodology integrates primary and secondary data collection, rigorous market modeling, and analytical validation to provide precise and actionable insights for industry professionals. USDAnalytics leverages interviews with key stakeholders including manufacturers, distributors, and regulatory experts while supplementing this with trade publications, corporate reports, and government policy updates. Historical consumption, production, and trade data are combined with macroeconomic indicators and regulatory milestones to construct robust market forecasts from 2025 to 2034. Quantitative methods, including CAGR calculations, market sizing, and volume-to-value conversions, underpin scenario-based projections, while qualitative analyses cover innovation trends, sustainability adoption, and strategic corporate initiatives. Competitive intelligence is further enhanced through benchmarking of operational capacities, certifications, product portfolios, and investment patterns, ensuring a holistic understanding of both global and regional market dynamics.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.