Biodegradable Packaging Materials Market Outlook: Sustainable Innovations & Market Expansion (2025–2034)

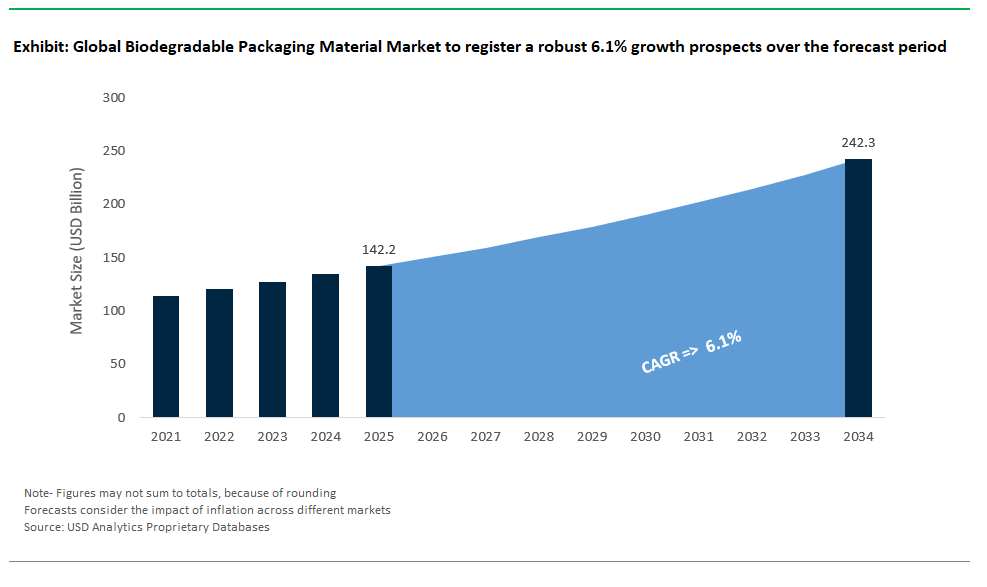

The Global Biodegradable Packaging Materials Market is set to advance steadily from 2025 through 2034, driven by regulatory mandates against plastic pollution, rising consumer preference for eco-friendly packaging, and rapid technological innovation across sustainable materials. Industry forecasts predict the market will increase from USD 142.2 billion in 2025 to USD 242.3 billion by 2034, achieving a healthy CAGR of 6.1%. Growth is powered by expanding adoption of biodegradable solutions in sectors such as food and beverages, personal care, e-commerce, and healthcare, as businesses intensify efforts to align with global sustainability goals and reduce environmental footprints.

Utilizing proprietary insights from USDAnalytics, this latest edition delivers a comprehensive analysis and forward-looking perspective on the global Biodegradable Packaging Materials Market, tracking progress in 21 countries and highlighting over 20 leading companies- By Material Type (Kraft Paper, Corrugated Board, Boxboard / Cartonboard, Molded Pulp, Specialty Papers, Recycled Paper & Paperboard, Bagasse-based Materials, Others), By Biodegradable Plastics (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Starch Blends, Polybutylene Succinate (PBS), Cellulose-based Plastics, Polycaprolactone (PCL), Others), By Emerging Biodegradable Materials (Seaweed-based Materials, Mushroom-based Materials, Alginate-based Materials, Protein-based Materials, Wood-based Materials), By Packaging (Flexible Packaging, Rigid Packaging), By End-Use Industry (Food & Beverages, Personal Care & Cosmetics, Healthcare & Pharmaceuticals, Homecare, Agriculture & Horticulture, E-commerce & Retail).

This study delivers a thorough analysis of key forces transforming the biodegradable packaging material landscape, highlighting how advances in materials such as seaweed-based films, mushroom-derived packaging, and alginate coatings are expanding sustainable options beyond traditional paper and bioplastics. It explores how manufacturers are scaling up production of innovative biodegradable plastics like PLA, PHA, and PBAT for flexible and rigid packaging, addressing both performance requirements and regulatory compliance. The report also investigates shifting end-user dynamics, rising demand from e-commerce and retail channels, and the growing role of sustainable packaging in brand differentiation and consumer loyalty. With actionable insights and validated data, this report serves as a critical resource for packaging manufacturers, converters, brand owners, investors, and policymakers aiming to navigate and capitalize on growth opportunities in the biodegradable packaging material market through 2034.

Global Biodegradable Packaging Materials Market Analysis: Regulations, Innovation, and Sustainability

The global biodegradable packaging materials market is expanding rapidly, driven by stricter regulations, technological innovations, and growing sustainability commitments from leading brands. Once considered niche, biodegradable materials are moving into mainstream packaging as consumers demand eco-friendly solutions and governments push for circular economy practices. Recent developments highlight how innovative products, capacity investments, and strategic partnerships are reshaping the market and paving the way for widespread commercial use.

Innovative Product Launches: Expanding Market Applications

New product launches show how biodegradable materials are being tailored for diverse applications, balancing performance with environmental benefits. BASF’s ecovio® M2351, a certified soil-biodegradable polymer, is designed for agricultural uses like mulch films, addressing concerns about soil microplastics and supporting sustainable farming. Danimer Scientific’s Nodax™ PHA coatings for paper cups are home-compostable and FDA-approved, offering sustainable alternatives to traditional polyethylene-coated paperboard in food-service packaging, which often poses recycling challenges. Mondi is also contributing a range of compostable paper packaging for applications like e-commerce, reflecting the shift toward fully compostable solutions that maintain durability and protection during shipping while reducing plastic use.

Capacity Expansions Indicate Market Scaling and Confidence

Capacity expansions from key industry players signal strong confidence in the biodegradable packaging market and are critical for reducing costs through scale. TotalEnergies Corbion operates a 75,000-tonne-per-year PLA facility in Thailand and plans further global expansions to meet rising demand in food packaging and ensure a reliable supply for sustainability-focused brands. Kaneka, a significant producer of PHBH™ (a type of PHA), has grown its capacity to about 5,000 tonnes annually since 2019, with plans for further scale-up, targeting marine-degradable films amid increasing efforts to combat ocean plastic pollution. Meanwhile, Stora Enso is investing €10 million in advanced dispersion barrier technologies to enhance recyclable and compostable paperboard, reflecting a strong move toward paper-based solutions with biodegradable coatings in response to regulatory and consumer demand for plastic-free alternatives.

Partnerships and M&A Expand Technological Horizons

Strategic collaborations and acquisitions are increasingly shaping the market, as companies seek to integrate advanced materials and scale global distribution.

- Tetra Pak is developing paper-based barrier solutions for beverage cartons, aiming to replace aluminum layers with renewable materials to reduce carbon footprints and improve sustainable packaging options.

- Novamont’s acquisition of BioBag Group strengthens its position in compostable film applications, aligning with rising regulations targeting single-use plastic bags and foodservice packaging.

- Kuraray, through its MonoSol business, leads in PVA-based water-soluble films, expanding into applications like detergent pods, agrochemicals, and single-use soluble packaging.

Regulatory Pressure Accelerates Biodegradable Packaging Adoption

Regulatory mandates are becoming the biggest force driving the adoption of biodegradable packaging materials worldwide. The European Union’s Packaging and Packaging Waste Regulation (PPWR) requires biodegradable solutions for specific products, including tea and coffee pods, fruit stickers, and lightweight plastic bags by February 2028, creating clear market pathways for compliant materials. In North America, California’s SB 54 law sets ambitious standards, mandating that all takeout and serviceware packaging be compostable or recyclable by 2032, pushing brands and retailers to accelerate sustainable packaging efforts. Meanwhile, India’s Extended Producer Responsibility (EPR) rules incentivize producers who meet recycling and reduction targets and penalize those who don’t, spurring adoption of compostable alternatives, particularly in the fast-growing online retail sector.

Technological Innovations: Driving Performance and Sustainability

New technologies are making biodegradable packaging materials more competitive with traditional plastics, solving previous challenges related to degradation speed, performance, and cost. Researchers are exploring enzyme-triggered degradation of PLA to accelerate the breakdown of single-use products, helping reduce environmental persistence and microplastic pollution. Other innovations include biobased and nanotechnology-enhanced films incorporating materials like nanocellulose and PHA, which are being developed to improve moisture barrier performance and promote faster marine degradation. These advancements are opening up new possibilities for biodegradable packaging in applications prone to marine litter or requiring high barrier properties.

Global Brands: Accelerating Commercial Adoption

Major global brands are leading the way in commercializing biodegradable packaging, signaling strong market maturity and consumer acceptance. McDonald’s has rolled out paper straws in multiple regions, reflecting the foodservice sector’s pivot away from traditional plastics, though challenges remain with end-of-life processing. Unilever is introducing sustainable paperboard ice cream tubs for Ben & Jerry’s in Europe and the U.S., using plant-based polyethylene coatings, showing how biodegradable materials are moving into premium product categories where sustainability is a key brand differentiator. Nestlé’s launch of home-compostable, paper-based Nespresso pods with a thin biodegradable polymer lining demonstrates how companies are merging high functionality with sustainability to meet consumer expectations for convenience and environmental responsibility.

Market Dynamics: Trends & Opportunities in the Biodegradable Packaging Material Industry

Trend: Seaweed-Based Coatings Redefining Marine-Safe Packaging

The global biodegradable packaging material industry is undergoing major change as seaweed-based coatings, made from carrageenan and alginates, emerge as a leading solution for marine-safe packaging. These materials provide superior barrier properties compared to some traditional films while breaking down in seawater within just 28 days, far faster than the centuries required for conventional plastics. Notpla’s Ooho edible water pods and Huhtamaki’s plant-based coatings for sustainable fiber packaging are prominent commercial examples, gaining momentum in food service and single-use packaging markets.

Regulatory support is also boosting adoption. The European Union’s Single-Use Plastics Directive aims to reduce marine plastic litter by targeting specific single-use items and setting ambitious recycling and collection goals for 2025 and beyond. From a sustainability perspective, seaweed-based coatings offer added benefits such as carbon sequestration and a lower environmental footprint compared to plastics like LDPE, although current costs remain higher. As industry and regulation align around marine-safe standards, seaweed coatings are redefining sustainability, performance, and lifecycle impacts in the biodegradable packaging sector, sparking new waves of innovation and market growth.

Opportunity: Digital Watermarking Enhancing Circular Economy and Sorting Efficiency

A significant opportunity in the global biodegradable packaging materials market lies in digital watermarking technologies that enable better traceability and sorting for circular economy systems. Sorting and recycling biodegradable packaging often face hurdles due to difficulties in identification and processing. Digital watermarking solutions like HolyGrail 2.0 embed invisible codes directly into packaging, allowing AI-driven sorting to achieve over 90% detection rates in industrial trials. This technology enables real-time tracking of materials throughout their lifecycle, ensuring compliance with biodegradation standards from production to composting, and closing crucial gaps in traceability.

Sorting efficiency is projected to rise significantly by 2030, increasing effective material recovery and lowering per-tonne costs. The potential impact on carbon emissions is substantial, as improved sorting reduces waste and contributes to climate goals. Strategic support is growing worldwide. The EU is working toward harmonized digital marking requirements under the Packaging and Packaging Waste Regulation (PPWR), backed by innovation funding. In the U.S., major retailers are testing advanced identification technologies to improve recycling and supply chain sustainability. ASEAN nations are also moving forward, supported by groups like the Asian Development Bank, focusing on sustainable infrastructure and waste management. Digital watermarking is set to become a key driver in the circular economy, helping both industry and regulators meet ambitious sustainability and waste reduction targets in the biodegradable packaging market.

Competitive Landscape of the Global Biodegradable Packaging Materials Market

The global biodegradable packaging materials market is expanding rapidly in 2024 as sustainability demands, regulatory pressures, and shifting consumer behavior push brands toward eco-friendly alternatives to conventional plastic and paper packaging. The market spans innovative bioplastics like PLA, PHA, PBAT blends, and starch-based solutions, as well as advanced biodegradable paper products featuring bio-based barriers and molded fiber designs. Leading companies are scaling production, developing new materials, and forming strategic partnerships to tap into growing demand across industries such as food and beverage, e-commerce, consumer goods, and automotive. The competitive landscape reflects a race for technological leadership and market share as biodegradable packaging transitions from niche applications to mainstream global adoption.

BASF: Strengthening the Market with Ecovio® Blends

BASF (Germany) BASF strengthens the biodegradable plastics market through its ecovio® brand, which blends PBAT and PLA for compostable packaging applications. The PBAT market was estimated at USD 1.74 billion in 2024, with Asia Pacific accounting for the largest revenue share. In February 2024, BASF launched its ChemCycling™ initiative in the US, converting plastic waste into new ISCC+ certified advanced recycled building blocks, further aligning its strategy with circular economy principles. BASF continues to demonstrate how global reach and advanced chemical innovation are propelling bioplastics into diverse and high-demand markets worldwide. Looking ahead to K 2025 (October 2025), BASF plans to showcase its commitment to #OurPlasticsJourney, highlighting a reduced Product Carbon Footprint (rPCF) portfolio and the use of biomass balance approach for biopolymers like ecovio® and ecoflex® BMB, further reinforcing its sustainable packaging solutions.

DS Smith: Innovating in Biodegradable Paper Packaging

DS Smith (UK) DS Smith is a leader in biodegradable paper packaging, particularly in molded fiber solutions designed for e-commerce and retail applications. The company highlights its focus on "Plastic Replacement" within its packaging solutions. DS Smith's research underlines the positive impact of switching to fiber-based alternatives in e-commerce clothing packaging and the potential to replace unnecessary plastics in supermarket food and drink packaging. In 2024, DS Smith received WorldStar Global Packaging Awards for innovations, including a fully recyclable corrugated cardboard packaging solution for vehicle chassis and a mono-material, plastic-free packaging for navigation systems, reinforcing its role as an innovator in sustainable paper packaging.

NatureWorks: Leading Global PLA Production

NatureWorks (USA) NatureWorks stands out as a global PLA leader, driving significant growth in biodegradable plastics. Its established global capacity is 165,000 tonnes per year from its US facility. The company's 75,000 tonnes per year Thailand plant, which made significant construction progress through Q2 2024, is anticipated to begin full production in 2025, poised to significantly boost its Asia-Pacific presence. In April 2024, NatureWorks, in partnership with IMA Coffee, announced a turn-key compostable coffee pod solution for the North American market, designed for superior brewing performance and industrial compostability, integrating Ingeo™ PLA biopolymer in the rigid capsule body, nonwoven filter, and multi-layer top lidding. Further expanding its portfolio, in February 2025, the company launched Ingeo™ 3D300 for high-quality 3D printing, and in March 2025, it introduced Ingeo™ Extend for BOPLA films. These initiatives underscore NatureWorks’ commitment to expanding PLA’s role beyond traditional single-use products into durable goods and complex packaging solutions.

Novamont: Leader in Starch-Based Biodegradable Materials

Novamont (Italy) Novamont remains a leader in starch-based biodegradable materials through its Mater-Bi® portfolio. As of October 2019, Novamont increased its Mater-Bi® compostable bioplastics production capacity by 40,000 tonnes at the Mater-Biopolymer plant in Patrica, Frosinone, complementing the existing 110,000 tonnes capacity at their Terni site. Following its acquisition of BioBag Group in 2023, Novamont significantly expanded its influence in the compostable packaging market. Novamont’s integrated approach positions it as a pivotal player in Europe’s biodegradable packaging market. However, recent developments from June 2025 indicate the Italian Competition Authority imposed fines totaling over €32 million on Novamont and its parent company Eni for abuse of a dominant position in the national markets for bioplastic raw materials used in bags.

Huhtamaki: Advancing Biodegradable Paper-Based Solutions

Huhtamaki (Finland) has cemented its reputation in the biodegradable paper packaging sector with its offerings of paper cups and lids for various beverages. In January 2025, Huhtamaki India hosted the presentation of "Design for Recyclability Guidelines for Films & Flexible Packaging" as part of the CII-India Plastics Pact's (IPP) initiative, highlighting its commitment to driving a circular economy in India's flexible packaging sector. The company also launched recyclable single-coated paper cups for dairy products in February 2025, designed to contain less than 10% plastic content and be fully recyclable in Europe. Huhtamaki’s global presence and continued investment in bio-based alternatives position it as a key supplier to the foodservice and consumer goods markets.

Stora Enso: Pushing Boundaries in Biodegradable Paper Packaging

Stora Enso (Sweden) Stora Enso is pushing the boundaries of biodegradable paper packaging with advanced barrier technologies. The company is actively developing bio-based coatings that provide oil and moisture resistance, enabling paper to replace plastic in demanding applications like food packaging. Stora Enso’s partnership with Pulpex for the development of paper bottles demonstrates its commitment to innovation and sustainable packaging solutions, making it a significant player in both rigid and flexible biodegradable paper markets. Stora Enso continues to invest in renewable packaging solutions, including efforts to reduce the carbon footprint of its products and develop new fiber-based materials.

TotalEnergies Corbion: Key Innovator in High-Performance PLA

TotalEnergies Corbion (Netherlands) TotalEnergies Corbion is a key innovator in high-performance PLA, operating a 75,000 tonnes per year facility in Thailand under its Luminy® brand. The company has plans for a second 100,000 tonnes per year plant in Grandpuits, France, reflecting significant future expansion and a drive to meet growing global demand. TotalEnergies Corbion's focus on technical enhancements positions it as a pivotal supplier in applications where both sustainability and functional performance are critical.

Segmentation Analysis: Biodegradable Packaging Materials Market

By Material Type: Corrugated Board Leads Market Share, Bagasse-Based Materials Grow Fastest

In 2025, corrugated board commands a 29.7% market share, solidifying its position as the backbone of shipping and e-commerce packaging thanks to its strength, versatility, and recyclability. Bagasse-based materials are the fastest-growing segment, as they replace traditional plastics in food containers and tableware, driven by regulatory bans and rising demand for compostable alternatives. Molded pulp also continues to gain momentum, offering a sustainable, foam-free solution for electronics, eggs, and fragile items. Kraft paper, boxboard, and specialty papers serve diverse needs from shopping bags to greaseproof wraps, while recycled paperboard meets secondary and transit packaging demands.

.png)

By End-Use Industry: Food & Beverages Lead Demand, E-Commerce & Retail Drive Fastest Growth

E-commerce and retail is the fastest-growing segment with a CAGR of 6.7%, propelled by the surge in online shopping and commitments to eco-friendly shipping from retailers like Amazon. The healthcare industry is also seeing robust growth, leveraging specialty and sterile biodegradable packaging for medical devices and pharmaceuticals. Food & beverages remain the largest end-use sector in 2025, as global brands and foodservice operators prioritize sustainable packaging for prepared foods, drinks, and takeout. Personal care, cosmetics, and agriculture all contribute to market expansion, utilizing boxboard, kraft, and corrugated materials for their specific needs.

Germany Setting Technology and Policy Benchmarks in Biodegradable Packaging Materials

Germany remains at the forefront of the global biodegradable packaging material industry, blending breakthrough innovation, robust investment, and regulatory leadership. Leading the charge, BASF’s Ecovio®, a certified compostable PBAT/PLA blend, has become the gold standard for food packaging, winning widespread adoption across the European Union. The Fraunhofer Institute’s nanocellulose coatings, which extend food shelf life by 40%, are transforming both sustainability and supply chain efficiency in the perishable goods sector. In 2025, Fraunhofer is actively collaborating with major German food producers on pilot projects to integrate these nanocellulose coatings into commercial packaging lines, targeting an immediate reduction in food waste. Germany’s market progress is underpinned by €2.3 billion in bioeconomy R&D (2021–2025), funded by the federal government and channeled into next-generation bioplastics, coatings, and recycling solutions. Recent years have also seen the integration of digital technology, as Siemens partners with BASF to deploy AI-driven process optimization for bioplastic manufacturing. This partnership is expected to yield significant efficiency gains in Q3 2025, optimizing raw material usage and reducing energy consumption in biopolymer synthesis. Regulatory momentum is strong: the EU’s Packaging and Packaging Waste Regulation (PPWR), enacted in February 2025 and effective from August 2026, clarifies mandates for specific compostable packaging (e.g., sticky labels on fresh produce, very lightweight plastic carrier bags), accelerating mass adoption across supermarkets, food service, and logistics across the EU, with Germany leading in implementation. Germany’s dynamic ecosystem of policy, technology, and investment sets a global benchmark for the industry’s future direction.

China Dominating Biodegradable Packaging Production and Policy Transformation

China has solidified its position as the global production powerhouse for biodegradable packaging materials, currently supplying an estimated 65% of worldwide demand. Industrial giants such as Kingfa Science, now the world’s largest PBAT producer with capacities reportedly exceeding 800,000 tons/year and ongoing expansions aimed at 1 million tons/year by late 2025, and Sinopec, which recently launched PBS-based agricultural films, drive both output and innovation. Aggressive policy measures are a central force in China’s market transformation: by 2025, at least 30% of all packaging nationwide must be biodegradable, while major cities enforce strict bans on non-degradable single-use plastics in food service, e-commerce, and retail. This year, Chinese authorities are intensifying inspections and enforcement of these bans, particularly for online retailers and large restaurant chains, driving a massive procurement shift towards certified biodegradable alternatives. This policy push is rapidly shifting procurement and manufacturing practices, with multinational brands now sourcing sustainable alternatives from China’s cost-effective and high-capacity suppliers. Supported by the China National Development and Reform Commission, these initiatives ensure China remains a pivotal supplier, technology driver, and price leader in the global shift to biodegradable packaging.

United States Fostering Innovation and Growth in Biodegradable Packaging Markets

The United States is rapidly emerging as an innovation and growth engine for biodegradable packaging materials, combining world-class R&D, aggressive investment, and a robust commercial ecosystem. Industry leaders like NatureWorks have scaled PLA production to maintain a significant capacity (around 150,000 tons/year), with plans for global expansions, serving food packaging, service ware, and flexible films for a broad range of consumer brands. Danimer Scientific’s FDA-approved PHA is unlocking new applications in compostable and marine-degradable food packaging. Following its FDA GRAS status (Notice 1123), Danimer's PHA is seeing increased adoption in commercial trials for rigid food containers and flexible pouches for major quick-service restaurants in 2025. National policy is propelling this growth: California’s SB 54 requires all packaging to be 100% compostable or recyclable by 2032, and Amazon has already adopted biodegradable mailers for half its shipments. Public investment is accelerating, with $1.5 billion in USDA and DOE funding supporting next-generation bioplastics and sustainable supply chain infrastructure. In 2025, the USDA is set to announce additional grant recipients for projects focused on developing high-performance, cost-competitive biodegradable agricultural films and mulches, aiming to reduce plastic pollution in farming. As the sector scales, the US market is drawing global attention for its leadership in advanced formulations, regulatory ambition, and brand-driven adoption of compostable and biodegradable packaging solutions.

Italy Advancing Compostable Packaging Pioneership and Regulatory Firsts

Italy stands as a global pioneer in compostable packaging, excelling in specialty biopolymer innovation and bold regulatory adoption. Novamont’s Mater-Bi® has set a new standard for 90-day soil-degradable films, now mandated for fruit and vegetable bags in all Italian retail, while Bio-on’s PHA targets premium and luxury segments with high-performance, biodegradable cosmetics packaging. Italy was the first country to introduce a national mandate for compostable fruit and vegetable bags, sparking a wave of similar policies across Europe. In 2025, Italy is further strengthening its national composting infrastructure, with government-backed initiatives to increase the number and capacity of industrial composting facilities, crucial for the effective end-of-life management of certified compostable packaging. As a frontrunner in the EU’s circular economy initiative, Italy’s industry is backed by government support, strong consumer awareness, and partnerships with leading global brands. These advantages are propelling Italy’s leadership in certified, compostable packaging and its reputation as a regulatory trendsetter in sustainable materials.

Netherlands Leading Circular Biodegradable Packaging with Bio-Based Alternatives

The Netherlands is shaping the future of circular biodegradable packaging with a strong emphasis on plant-based alternatives, rapid commercialization, and corporate commitment. Avantium’s breakthrough PEF technology offers a renewable alternative to traditional PET, boasting superior oxygen barrier properties now being piloted in Heineken’s beer bottles for a targeted 2025 commercial launch in select markets, showcasing a critical step towards broader adoption. DSM’s bio-based polyamides are making inroads in medical packaging, while Philips’ commitment to 100% biodegradable packaging for medical devices highlights the commercial readiness of sustainable solutions in high-value sectors. In 2025, Dutch research consortia are initiating new projects focused on improving the recyclability of multi-material biodegradable packaging, aiming to develop more effective separation and processing technologies. The government is also expected to announce new tax incentives for companies investing in bio-based and biodegradable material production within the country, fostering domestic innovation and manufacturing capacity. The Netherlands’ robust ecosystem is supported by national and EU funding, open innovation platforms, and a progressive regulatory environment, cementing its position as a strategic leader in both materials development and adoption.

Japan Delivering High-Performance Biodegradable Packaging for Food and Electronics

Japan’s biodegradable packaging industry is characterized by technical sophistication, specialty materials, and rapid market adoption. Mitsubishi’s BioPBS™ leads the charge in heat-resistant, compostable food containers and trays, addressing the country’s convenience-driven food culture and stringent safety standards. Toray’s transparent PLA films are deployed in electronics packaging, serving global electronics brands that demand both sustainability and performance. Recent years have seen increased funding, with METI’s $200 million Green Fund driving R&D and commercialization across the sector. Sony’s adoption of sugarcane-based PET packaging for consumer electronics signals a growing shift among Japanese brands toward renewable, biodegradable solutions. In 2025, Japanese packaging manufacturers are increasingly focused on developing advanced barrier properties for biodegradable films, catering to the country's stringent food preservation standards and expanding into sensitive electronics packaging for moisture protection. There's also a growing trend for innovative biodegradable solutions in the medical and pharmaceutical packaging sectors, leveraging Japan's strong capabilities in precision manufacturing. Japan’s high-tech focus, combined with policy and corporate commitment, positions it as a global innovator in the next generation of biodegradable packaging materials.

Biodegradable Packaging Materials Market Report Scope

Biodegradable Packaging Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$142.2 Billion

|

|

Market Size (2034)

|

$242.3 Billion

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Material Type (Kraft Paper, Corrugated Board, Boxboard / Cartonboard, Molded Pulp, Specialty Papers, Recycled Paper & Paperboard, Bagasse-based Materials, Others), By Biodegradable Plastics (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Starch Blends, Polybutylene Succinate (PBS), Cellulose-based Plastics, Polycaprolactone (PCL), Others), By Emerging Biodegradable Materials (Seaweed-based Materials, Mushroom-based Materials, Alginate-based Materials, Protein-based Materials, Wood-based Materials), By Packaging (Flexible Packaging, Rigid Packaging), By End-Use Industry (Food & Beverages, Personal Care & Cosmetics, Healthcare & Pharmaceuticals, Homecare, Agriculture & Horticulture, E-commerce & Retail)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor Plc (Switzerland/Australia), Mondi Group (Austria/UK), International Paper Company (U.S.), Tetra Pak International SA (Switzerland), WestRock Company (U.S.), Stora Enso (Finland/Sweden), DS Smith Plc (UK), Novamont S.p.A. (Italy), BASF SE (Germany), NatureWorks LLC (U.S.), Danimer Scientific (U.S.), TotalEnergies Corbion (Netherlands), Braskem S.A. (Brazil), Huhtamaki Oyj (Finland), Smurfit Kappa Group Plc (Ireland), Sealed Air Corporation (U.S.), Alpla Group (Austria), Constantia Flexibles (Austria), Plantic Technologies Limited (Australia), Ecoware (India), Pakka Ltd. (India/Switzerland), BioPak India (Huhtamaki Oyj subsidiary) (India/Finland), Chuk (Yash Pakka Ltd.) (India), Kruger Inc. (Canada), Notpla (UK), Sulapac (Finland), Avani Eco (Indonesia), Green Dot Bioplastics (U.S.), Elevate Packaging (U.S.), and Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Biodegradable Packaging Materials Market Segmentation

By Material

- Kraft Paper

- Corrugated Board

- Boxboard / Cartonboard

- Molded Pulp

- Specialty Papers

- Recycled Paper & Paperboard

- Bagasse-based Materials

- Others

By Biodegradable Plastics

- Polylactic Acid (PLA)

- Polyhydroxyalkanoates (PHA)

- Polybutylene Adipate Terephthalate (PBAT)

- Starch Blends

- Polybutylene Succinate (PBS)

- Cellulose-based Plastics

- Polycaprolactone (PCL)

- Others

By Emerging Biodegradable Materials

- Seaweed-based Materials

- Mushroom-based Materials

- Alginate-based Materials

- Protein-based Materials

- Wood-based Materials

By Packaging

- Flexible Packaging

- Films & Wraps

- Bags

- Pouches & Sachets

- Lidding Films

- Rigid Packaging

- Boxes & Cartons

- Trays & Containers

- Bottles & Jars

- Cups & Lids

- Blister Packs & Clamshells

- Disposable Tableware & Cutlery

By End-Use Industry

- Food & Beverages

- Personal Care & Cosmetics

- Healthcare & Pharmaceuticals

- Homecare

- Agriculture & Horticulture

- E-commerce & Retail

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Biodegradable Packaging Materials Market

- Amcor Plc (Switzerland/Australia)

- Mondi Group (Austria/UK)

- International Paper Company (US)

- Tetra Pak International SA (Switzerland)

- WestRock Company (US)

- Stora Enso (Finland/Sweden)

- DS Smith Plc (UK)

- Novamont S.p.A. (Italy)

- BASF SE (Germany)

- NatureWorks LLC (US)

- Danimer Scientific (US)

- TotalEnergies Corbion (Netherlands)

- Braskem S.A. (Brazil)

- Huhtamaki Oyj (Finland)

- Smurfit Kappa Group Plc (Ireland)

- Sealed Air Corporation (US)

- Alpla Group (Austria)

- Constantia Flexibles (Austria)

- Plantic Technologies Limited (Australia)

- Ecoware (India)

- Pakka Ltd. (India/Switzerland)

- BioPak India (Huhtamaki Oyj subsidiary) (India/Finland)

- Chuk (Yash Pakka Ltd.) (India)

- Kruger Inc. (Canada)

- Notpla (UK)

- Sulapac (Finland)

- Avani Eco (Indonesia)

- Green Dot Bioplastics (US)

- Elevate Packaging (US)

* List Not Exhaustive

Methodology

The Global Biodegradable Packaging Materials Market 2025–2034 report is developed using a comprehensive and systematic research methodology that integrates both primary and secondary data sources. Primary research includes extensive interviews and discussions with senior executives of biodegradable packaging manufacturers, material scientists, converters, end-users across key industries, and regulatory authorities to capture first-hand insights on market dynamics, emerging technologies, and regional developments. Secondary research involves meticulous analysis of company filings, scientific publications, government regulations, industry reports, patent databases, and market announcements to ensure accuracy and contextual understanding. Market sizing employs a hybrid approach, combining top-down analysis of macroeconomic indicators and policy trends with bottom-up assessment of capacity expansions, material usage rates, and end-user demand across over 25 countries. All forecasts are subjected to multiple validation rounds and triangulation against proprietary intelligence from USDAnalytics, ensuring the report delivers robust and reliable insights. Scenario modeling is applied to quantify the potential impacts of regulatory shifts, technology breakthroughs, and macroeconomic fluctuations on market growth trajectories.

Research Coverage

- Geographic Scope: Global, with in-depth country-level analysis for North America, Europe, Asia Pacific, South America, and the Middle East & Africa, covering over 25 individual countries.

- Segmentation: Detailed segmentation by Material Type (Kraft Paper, Corrugated Board, Boxboard/Cartonboard, Molded Pulp, Specialty Papers, Recycled Paper & Paperboard, Bagasse-based Materials, Others), Biodegradable Plastics (PLA, PHA, PBAT, Starch Blends, PBS, Cellulose-based Plastics, PCL, Others), Emerging Biodegradable Materials (Seaweed-based Materials, Mushroom-based Materials, Alginate-based Materials, Protein-based Materials, Wood-based Materials), Packaging Format (Flexible Packaging, Rigid Packaging), and End-Use Industry (Food & Beverages, Personal Care & Cosmetics, Healthcare & Pharmaceuticals, Homecare, Agriculture & Horticulture, E-commerce & Retail).

- Competitive Analysis: Extensive profiling and strategic assessments of over 25 leading global and regional companies engaged in biodegradable packaging material development, manufacturing, and commercialization.

- Key Themes: Exploration of sustainable material innovations, regulatory drivers (e.g., EU PPWR, US SB 54), digital watermarking, circular economy strategies, cost trends, and emerging applications in sectors like e-commerce, healthcare, and premium consumer goods.

- Market Dynamics: In-depth analysis of growth drivers, restraints, regulatory frameworks, technological advances, investment trends, and consumer behavior shaping the biodegradable packaging materials market through 2034.

- Data Horizon: Historical data from 2021–2024 and forecasts from 2025–2034.

Deliverables

- Comprehensive Market Report (PDF & Excel): In-depth market analysis, segmented data tables, visuals, and expert commentary.

- Country-Level Market Forecasts & Insights

- Segment-Level Revenue and Volume Projections (2025–2034)

- Detailed Company Profiles and Competitive Benchmarking

- Regulatory Landscape Review and Emerging Policy Tracker

- Executive Summary with Analyst Insights and Strategic Recommendations

- Post-Purchase Analyst Support for Customized Inquiries

Table of Contents: Biodegradable Packaging Materials Market Outlook: Sustainable Innovations & Market Expansion (2025–2034)

Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

Biodegradable Packaging Materials Market Landscape & Outlook (2025-2034)

2.1. Introduction to Biodegradable Packaging Materials

2.2. Market Valuation and Growth Projections (2025-2034)

2.2.1. Historical Market Size (2020-2024)

2.2.2. Current Market Size (2025): USD 142.2 Billion

2.2.3. Forecasted Market Size and CAGR (2025-2034): USD 242.3 Billion at 6.1% CAGR

2.3. Key Market Drivers

2.3.1. Increasing Regulatory Mandates Against Plastic Pollution

2.3.2. Rising Consumer Demand for Eco-Friendly Packaging

2.3.3. Significant Technological Advancements in Sustainable Materials

2.3.4. Expanding Adoption in Key Sectors (Food and Beverages, Personal Care, E-commerce, Healthcare)

2.4. Market Challenges and Restraints

2.4.1. High Production Costs and Scalability Challenges

2.4.2. Performance Limitations Compared to Traditional Plastics (e.g., barrier properties, shelf-life)

2.4.3. Complexities in Waste Management and Recycling Infrastructure for Biodegradables

2.4.4. Consumer Confusion and Lack of Awareness Regarding Proper Disposal

Market Analysis: Biodegradable Packaging Innovations & Commercialization (2024–2025)

3.1. Overview of Sustainable Innovation and Commercialization Trends

3.2. Material Advancements & New Product Development

3.2.1. Developments in Paper-Based Solutions (Kraft Paper, Corrugated Board, Molded Pulp)

3.2.2. Innovations in Biodegradable Plastics (PLA, PHA, PBAT)

3.2.3. Emergence of Seaweed-Based and Mushroom-Based Packaging

3.3. Strategic Initiatives Driving Market Growth

3.3.1. Innovative Product Launches

3.3.2. Capacity Expansions by Major Players (e.g., TotalEnergies Corbion, Kaneka)

3.3.3. Strategic Partnerships and Collaborations

3.4. Accelerating Role of Regulatory Pressures

3.4.1. Impact of EU's Packaging and Packaging Waste Regulation

3.4.2. Influence of California's SB 54 Law and Other Regional Mandates

3.5. Increasing Commercial Adoption by Global Brands

3.5.1. Case Studies: McDonald's, Unilever, Nestlé and others

Competitive Landscape of the Biodegradable Packaging Materials Market

4.1. Key Players and Market Competition Overview

4.2. BASF: Strengthening the Market with Ecovio® Blends

4.3. DS Smith: Innovating in Biodegradable Paper Packaging

4.4. NatureWorks: Leading Global PLA Production

4.5. Novamont: Leader in Starch-Based Biodegradable Materials

4.6. Huhtamaki: Advancing Biodegradable Paper-Based Solutions

4.7. Stora Enso: Pushing Boundaries in Biodegradable Paper Packaging

4.8. TotalEnergies Corbion: Key Innovator in High-Performance PLA

4.9. Other Key Players

Market Dynamics – Biodegradable Packaging Materials Industry: Key Trends & Opportunities (2025–2034)

5.1. Trend: Rise of Seaweed-Based Coatings for Marine-Safe Packaging

5.1.1. Superior Barrier Properties

5.1.2. Rapid Degradation in Marine Environments

5.2. Opportunity: Digital Watermarking for Improved Circular Economy and Sorting Efficiency

5.2.1. Enhanced Traceability and Material Recovery

5.2.2. Reduced Carbon Emissions

5.3. Trend: Growth in Sustainable Packaging for E-commerce

5.4. Opportunity: Development of Home Compostable Packaging Solutions

Biodegradable Packaging Materials Market Share and Segmentation Analysis (2021-2034)

6.1. By Material Type

6.1.1. Paper-Based Solutions

6.1.1.1. Kraft Paper

6.1.1.2. Corrugated Board

6.1.1.3. Molded Pulp

6.1.2. Biodegradable Plastics

6.1.2.1. Polylactic Acid (PLA)

6.1.2.2. Polyhydroxyalkanoates (PHA)

6.1.2.3. Polybutylene Adipate Terephthalate (PBAT)

6.1.3. Emerging Biodegradable Materials

6.1.3.1. Seaweed-Based Materials

6.1.3.2. Mushroom-Based Materials

6.1.3.3. Bagasse-Based Materials

6.2. By Packaging Type

6.2.1. Flexible Packaging

6.2.2. Rigid Packaging

6.3. By End-Use Industry

6.3.1. Food & Beverages

6.3.2. Personal Care & Cosmetics

6.3.3. Healthcare & Pharmaceuticals

6.3.4. Homecare

6.3.5. Agriculture & Horticulture

6.3.6. E-commerce & Retail

6.3.7. Others

7. Country Analysis and Outlook of Biodegradable Packaging Materials Market, 2021- 2034

7.1. United States: Fostering innovation and growth in biodegradable packaging.

7.2. Canada: Growing in biodegradable plastics and sustainable solutions.

7.3. Mexico: Seeing growth in compostable packaging from global and national drives.

7.4. Germany: Setting technology and policy benchmarks.

7.5. United Kingdom: Investing in smart sustainable packaging and bio-based materials.

7.6. France: A key player in eco-friendly flexible and bio-based packaging.

7.8. Spain: Promoting compostable packaging and supporting infrastructure.

7.9. Italy: Advancing compostable packaging and regulatory firsts.

7.10. Netherlands: Leading circular biodegradable packaging with bio-based alternatives.

7.11. Russia: Developing innovative biodegradable films and smart packaging.

7.12. Rest of Europe: Experiencing robust growth driven by demand and regulations.

7.13. China: Dominating biodegradable packaging production and policy.

7.14. India: Driven by environmental awareness and plastic bans.

7.15. Japan: Delivering high-performance biodegradable packaging for various sectors.

7.16. South Korea: Moving towards plastic-free with strong policies.

7.17. Australia: Strong growth in sustainable packaging, supported by research.

7.18. South East Asia: Significant growth from awareness and biopolymer innovation.

7.19. Rest of Asia: Fast-growing due to environmental acts and urbanization.

7.20. Brazil: Advancing sustainable practices with legal mandates.

7.21. Argentina: Poised for growth in compostable packaging.

7.22. Middle East and Africa: Increasing adoption of biodegradable packaging due to urbanization and industrialization.

8. Biodegradable Packaging Materials Market Size Outlook by Region (2025-2034)

8.1. North America Biodegradable Packaging Materials Market Size Outlook to 2034

8.1.1. By Material Type

8.1.2. By Packaging Type

8.1.3. By End-Use Industry

8.2. Europe Biodegradable Packaging Materials Market Size Outlook to 2034

8.2.1. By Material Type

8.2.2. By Packaging Type

8.2.3. By End-Use Industry

8.3. Asia Pacific Biodegradable Packaging Materials Market Size Outlook to 2034

8.3.1. By Material Type

8.3.2. By Packaging Type

8.3.3. By End-Use Industry

8.4. South America Biodegradable Packaging Materials Market Size Outlook to 2034

8.4.1. By Material Type

8.4.2. By Packaging Type

8.4.3. By End-Use Industry

8.5. Middle East and Africa Biodegradable Packaging Materials Market Size Outlook to 2034

8.5.1. By Material Type

8.5.2. By Packaging Type

8.5.3. By End-Use Industry

9. Company Profiles: Leading Players in Biodegradable Packaging Materials Market

9.1. Amcor Plc

9.2. Mondi Group

9.3. International Paper Company

9.4. Tetra Pak International SA

9.5. WestRock Company

9.6. Stora Enso

9.7. DS Smith Plc

9.8. Novamont S.p.A.

9.9. BASF SE

9.10. NatureWorks LLC

9.11. Danimer Scientific

9.12. TotalEnergies Corbion

9.13. Braskem S.A.

9.14. Huhtamaki Oyj

9.15. Smurfit Kappa Group Plc

9.16. Sealed Air Corporation

9.17. Alpla Group

9.18. Constantia Flexibles

9.19. Plantic Technologies Limited

9.20. Ecoware

9.21. Pakka Ltd.

9.22. BioPak India

9.23. Chuk (Yash Pakka Ltd.)

9.24. Kruger Inc.

9.25. Notpla

9.26. Sulapac

9.27. Avani Eco

9.28. Green Dot Bioplastics

9.29. Elevate Packaging

9.30. Additional Prominent Players

10. Methodology

10.1. Research Scope

10.1.1. Market Definition

10.1.2. Key Market Segments Covered

10.1.3. Geographic Coverage

10.1.4. Years Covered (Historical, Current, Forecast)

10.2. Market Research Approach

10.2.1. Primary Research

10.2.2. Secondary Research

10.2.3. Data Triangulation

10.3. Data Sources (Primary and Secondary)

10.3.1. Primary Data Sources

10.3.2. Secondary Data Sources

10.4. Market Estimation and Forecasting Model

10.4.1. Market Sizing Approaches

10.4.2. Forecasting Techniques

10.4.3. Assumptions for Market Modeling

10.5. Assumptions and Limitations

11. Appendix

11.1. Acronyms and Abbreviations

11.2. List of Tables

11.3. List of Figures