Biodegradable Plastics Market Outlook: Innovation & Sustainability Trends (2025–2034)

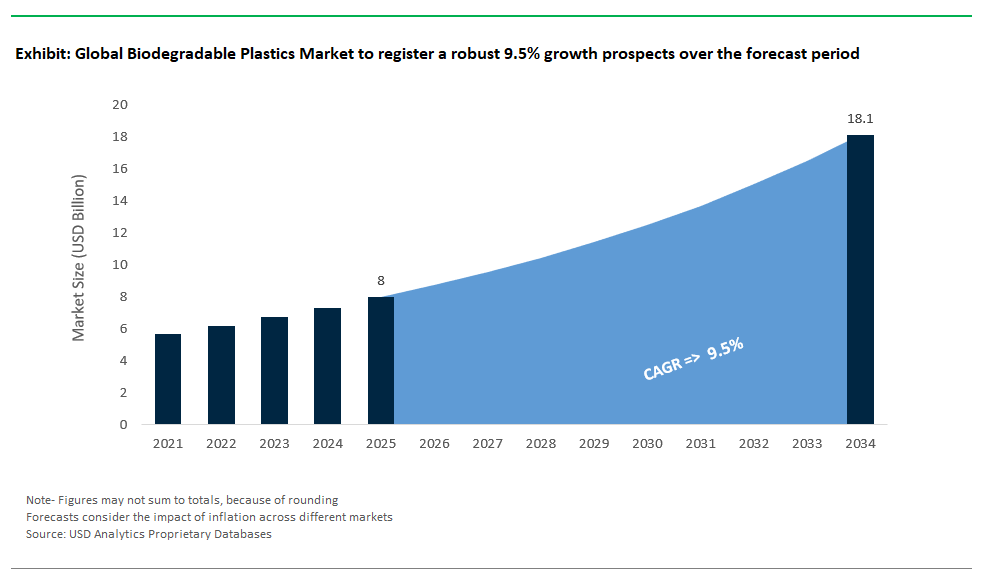

The Global Biodegradable Plastics Market is poised for steady growth from 2025 through 2034, as manufacturers, brands, and policymakers intensify efforts to replace conventional plastics with materials that support a circular, low-waste economy. The global market for biodegradable plastics is projected to expand from USD 8 billion in 2025 to USD 18.1 billion by 2034, registering a robust CAGR of 9.5%. This expansion is driven by increasingly stringent regulations against single-use plastics, rising adoption of compostable and bio-based alternatives in packaging and consumer goods, and continued advancements in polymer science and feedstock innovation.

Leveraging insights from USDAnalytics, the latest edition provides a detailed market evaluation and strategic outlook for the global biodegradable plastics market, tracking industry developments across more than 25 countries and highlighting the activities of leading players By Type (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS) & Co-Polymers (PBSA), Starch Blends / Thermoplastic Starch (TPS), Cellulose-based Plastics, Polycaprolactone (PCL), Others), By Application (Packaging (Flexible, Rigid), Agriculture & Horticulture, Consumer Goods (Disposable Tableware, Personal Care Products), Textiles (Medical & Hygiene, Apparel), Medical & Healthcare, Others), By Raw Material (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Fossil-based, Others).

This report provides a comprehensive analysis of the global biodegradable plastics market, examining the technological advances and policy shifts accelerating industry transformation through 2034. It covers the rapid growth of high-performance biopolymers like PLA and PHA, the emergence of starch and cellulose-based plastics in flexible and rigid packaging, and the integration of renewable and waste-based feedstocks into mainstream production. The study details evolving market segmentation by product type, raw material, and end-use application, and evaluates the strategies of innovators scaling up production to meet global demand. For manufacturers, suppliers, investors, and policymakers, this report delivers actionable intelligence for capturing growth opportunities and advancing the adoption of biodegradable plastics in the next era of sustainable materials.

Global Biodegradable Plastics Market Analysis: Growth Drivers & Innovations

The global biodegradable plastics market is undergoing dynamic growth, fueled by converging regulatory mandates, technological innovation, and surging brand owner commitments to sustainability. Once considered niche alternatives, biodegradable plastics are rapidly moving into mainstream applications across packaging, agriculture, consumer goods, and even marine environments. Recent developments reveal a vibrant and competitive landscape where capacity expansions, innovative product launches, and strategic alliances are reshaping the market’s trajectory.

Product Innovations: Expanding Market Horizons for Biodegradable Plastics

Product innovation is at the forefront of market momentum, as companies introduce biodegradable plastics tailored to diverse functional and environmental requirements.

- BASF’s launch of ecovio® M2351, a certified soil-biodegradable mulch film for agricultural applications, demonstrates how biodegradable materials are targeting sectors with acute environmental impacts, such as reducing persistent microplastics in agricultural soil.

- Danimer Scientific’s Nodax™ PHA-based coffee pods, home-compostable within six months, illustrate growing consumer demand for convenience products that align with circular economy principles.

- Mitsubishi Chemical’s BioPBS™ FD92 soil-biodegradable mulch films cater to agriculture’s sustainability goals, addressing both soil health and regulatory pressures to eliminate conventional plastics in farming applications.

Capacity Expansions: Underscoring Market Scalability & Future Supply

Robust capacity expansions signal rising confidence in the market’s long-term growth and highlight efforts to secure supply for increasingly large customer bases.

- TotalEnergies Corbion’s Luminy® PLA production, with significant global capacity including up to 250,000 tonnes per year, positions it as a leading global supplier for compostable applications ranging from food packaging to consumer goods.

- NatureWorks’ new 75,000-tonne PLA plant in Thailand strategically bolsters capacity close to high-growth Asia-Pacific markets, ensuring supply resilience and lower logistics costs.

- Kaneka’s scaling of PHBH™ production to 20,000 tonnes annually (from a 5,000 t/y pilot plant) reflects growing demand for marine-degradable materials in single-use items, aligning with emerging policies focused on mitigating ocean plastic pollution.

Strategic Partnerships & M&A: Redefining Market Leadership in Biodegradable Plastics

The market landscape is consolidating through strategic acquisitions and collaborations as companies seek to enhance technological capabilities and broaden product portfolios.

- Versalis’ acquisition of Novamont strengthens its position as a major European bioplastics producer, leveraging Novamont’s expertise in compostable materials like MATER-BI.

- Cargill’s joint venture with Helm AG to build a $300 million bio-based 1,4-butanediol (BDO) plant in Iowa signals North America’s push to develop localized supply chains and reduce reliance on imports, especially for applications like food packaging.

- Solvay’s joint development agreement with BioAmber on bio-succinic acid derivatives for plasticizers aims to expand the market’s material diversity and offer biodegradable solutions with tailored performance characteristics.

Regulatory Shifts: Driving Rapid Adoption of Biodegradable Plastics

Regulatory changes are now the biggest force driving the adoption of biodegradable plastics, turning sustainability from an option into a market necessity. The EU’s Packaging and Packaging Waste Regulation (PPWR) mandates that certain packaging types, like permeable tea and coffee bags and fruit stickers, must be compostable by February 2028, creating mandatory markets for biodegradable materials. Thailand’s plastic bag ban has sharply increased demand for PLA and PHA alternatives, especially in retail and food service, making it the world’s second-largest bioplastic producer. Meanwhile, California’s SB 54 law, requiring all fast-food and serviceware packaging to be recyclable or compostable by 2032, adds strong regulatory momentum in North America, one of the world’s key consumer markets.

Technological Advances: Solving Performance & Environmental Challenges

Innovation is rapidly addressing the traditional performance limitations of biodegradable plastics, boosting their competitiveness against conventional polymers. MIT’s research into enzyme-embedded PLA has shown significant progress in speeding up biodegradation, with some samples breaking down in home compost within a few months, a potential game-changer for single-use plastics. Fraunhofer UMSICHT has developed cellulose-starch biocomposites that degrade in marine environments within 90 days, directly tackling ocean pollution and opening new opportunities for biodegradable plastics in fishing gear, marine packaging, and coastal tourism products.

Brand Sustainability Efforts: Fueling Biodegradable Plastics Market Growth

Global brands are increasingly integrating biodegradable plastics into their sustainability strategies, driving market growth across various sectors. Nestlé has launched home-compostable, paper-based Nespresso Original pods with a thin biodegradable polymer lining, showing how companies use biodegradable materials to reduce packaging waste and strengthen their sustainability credentials in high-profile consumer products. Unilever continues to explore innovative sustainable packaging, including bio-based options, to enhance premium products like Ben & Jerry’s and appeal to environmentally conscious consumers.

Biodegradable Plastics Industry Dynamics: New Recycling Methods & Marine Safety

Trend: Enzymatic Biodegradation Revolutionizing Plastic Recycling & Adoption

The global biodegradable plastics industry is entering a new era with the rise of enzymatic biodegradation technologies, which are dramatically improving the speed, efficiency, and sustainability of plastic recycling. Carbios’ C-ZYME® enzymatic process has shown impressive results, breaking down plastics like PLA by 90% within 48 hours and progressing toward efficient PET recycling. This technology enables high monomer recovery, far surpassing the centuries-long natural degradation timeline of conventional plastics. Investments are pouring into scaling up enzymatic recycling facilities, signaling the emergence of industrial-scale, closed-loop plastics management.

Environmental benefits are substantial, as recycled plastics produced through enzymatic methods significantly cut life cycle greenhouse gas emissions compared to virgin plastic production. Research from Fraunhofer UMSICHT confirms reductions in CO₂ emissions and resource depletion through these advanced recycling processes.

Adoption is expanding across sectors. Beverage giants like PepsiCo are integrating recycled and bio-based materials into their packaging as part of their sustainability goals. The textile industry is following suit, with companies like Patagonia and Adidas using recycled and bio-based plastics in apparel. In agriculture, firms like BASF are developing biodegradable solutions for mulch films and crop protection. Together, these efforts highlight the growing commitment to closed-loop, low-carbon plastic lifecycles, driving global interest and investment in enzymatic biodegradation.

Opportunity: Marine-Degradable PHA Tackling Ocean Plastics & Transforming Fisheries

A significant growth opportunity in the global biodegradable plastics market lies in marine-degradable polyhydroxyalkanoates (PHA), especially for fisheries and coastal economies battling ocean plastic pollution. Lost fishing gear, “ghost nets” accounts for 46% of plastic waste in the North Pacific Gyre, contributing heavily to the Great Pacific Garbage Patch. Unlike traditional nylon nets, which can persist for centuries, PHA-based fishing gear certified by TÜV Austria OK Marine degrades in seawater within about 90-98 days, offering a sustainable alternative for global fisheries.

The business case for PHA is strengthening as production costs are expected to drop significantly by 2030, potentially falling 30-40% through process improvements and using alternative feedstocks like waste methane. Currently, commercial PHA prices range from $4,960 to $6,060 per tonne. The global demand for fishing gear continues to grow, and the ongoing negotiations for a UN Plastic Treaty are likely to introduce measures to address marine plastic pollution, including lost and discarded fishing gear.

Governments and institutions are supporting this transition. Thailand is investing in modernizing its fisheries, Norway offers tax incentives aligned with Ocean Panel 2030 targets, and the Asian Development Bank is funding coastal infrastructure and marine health initiatives in Southeast Asia, all of which include combating plastic pollution. These developments position marine-degradable PHA as a critical solution for ocean conservation and a key driver of growth in the biodegradable plastics market.

Competitive Landscape of the Global Biodegradable Plastics Market: Innovation, Scaling, and Strategic Growth in 2024

The global biodegradable plastics market is expanding rapidly in 2024, propelled by regulatory bans on single-use plastics, corporate sustainability goals, and consumer demand for environmentally friendly alternatives. Innovations in PLA, PHA, starch blends, and PBAT technologies are driving new applications in packaging, consumer goods, agriculture, and automotive sectors. Leading companies are scaling production capacities, securing strategic partnerships, and developing next-generation biodegradable materials to capture growing demand. The competitive landscape is defined by aggressive investment, technological breakthroughs, and the push to make biodegradable plastics economically viable on a global scale.

NatureWorks: Dominant Force in PLA Biodegradable Plastics

NatureWorks (USA) NatureWorks remains a dominant force in the PLA segment, with an established global capacity of 165,000 tonnes per year from its US facility. Its 75,000 tonnes per year Thailand plant, which made significant construction progress through Q2 2024, is anticipated to begin full production in 2025, poised to significantly strengthen its Asia-Pacific presence. In April 2024, NatureWorks, in partnership with IMA Coffee, announced a turn-key compostable coffee pod solution for the North American market, designed for superior brewing performance and industrial compostability. Further expanding its portfolio, in February 2025, the company launched Ingeo™ 3D300 for high-quality 3D printing, and in March 2025, it introduced Ingeo™ Extend for BOPLA films. These initiatives underscore NatureWorks’ commitment to expanding PLA’s role beyond traditional single-use products into durable goods and complex packaging solutions.

TotalEnergies Corbion: Major Player in PLA Production

TotalEnergies Corbion (Netherlands) TotalEnergies Corbion is a major player in PLA production, operating a 75,000 tonnes per year facility in Thailand under its Luminy® brand. The company has plans for a second 100,000 tonnes per year plant in Grandpuits, France, reflecting significant future expansion and a drive to meet growing global demand. TotalEnergies Corbion is known for its focus on enhancing PLA performance and diversifying applications, positioning it as a key force in the global biodegradable plastics market.

Kaneka Corporation: Scaling PHA Operations & Innovations

Kaneka Corporation (Japan) Kaneka Corporation is steadily scaling its PHA operations, with its proprietary PHBH™ biopolymer production capacity having increased to 20,000 tonnes annually as of January 2024. Kaneka's "Three-Year Initiatives 2025" plan (released May 2025) indicates efforts to increase production capacity and accelerate R&D on productivity-enhancing technologies for Green Planet (PHBH™), with full-scale operations at its 15,000-ton demonstration plant expected in FY2025. Kaneka's advancements signal strong momentum in PHA applications for both rigid and flexible packaging sectors.

Novamont: Leader in Starch-Based Biodegradable Plastics

Novamont (Italy) Novamont stands as a leader in starch-based biodegradable plastics with its Mater-Bi® brand, widely used for compostable bags and agricultural films. Following its acquisition of BioBag Group in 2023, Novamont significantly expanded its influence in the compostable packaging market. Novamont remains a key innovator focused on sustainable feedstock sourcing and cost efficiency to enhance its competitiveness and appeal to brands seeking sustainable yet economically viable packaging solutions. However, recent developments from June 2025 indicate the Italian Competition Authority imposed fines totaling over €32 million on Novamont and its parent company Eni for abuse of a dominant position in the national markets for bioplastic raw materials used in bags.

BASF SE: Advancing PBAT & Circular Biodegradable Solutions

BASF (Germany) BASF plays a crucial role in the PBAT sector with its ecovio® biodegradable plastic. BASF launched its ChemCycling™ initiative in the US, converting plastic waste into new ISCC+ certified advanced recycled building blocks, further aligning its strategy with circular economy principles. BASF continues to demonstrate how global reach and advanced chemical innovation are propelling bioplastics into diverse and high-demand markets worldwide. Looking ahead to K 2025 (October 2025), BASF plans to showcase its commitment to #OurPlasticsJourney, highlighting a reduced Product Carbon Footprint (rPCF) portfolio and the use of biomass balance approach for biopolymers like ecovio® and ecoflex® BMB, further reinforcing its sustainable packaging solutions.

Biodegradable Plastics Market Share Analysis

By Type: PLA Dominates Market Share, PHA Leads as Fastest-Growing Biodegradable Plastic

In 2025, polylactic acid (PLA) leads the biodegradable plastics market with a 33.1% share, reflecting widespread use in rigid packaging, food serviceware, and compostable containers. Its processability and consumer familiarity make it a mainstay for brand owners seeking sustainable solutions. Polyhydroxyalkanoates (PHA) are the fastest-growing segment, driven by superior biodegradability in marine environments and flexibility, making them ideal for single-use packaging, agricultural films, and specialty fibers. PBAT remains widely adopted for compostable films and is frequently blended with PLA to enhance flexibility and performance.

.png)

By Application: Packaging Remains Dominant, Healthcare Segment Expands Rapidly

Healthcare is the fastest-growing application with a CAGR of 11.3%, with demand surging for biodegradable sutures, drug delivery systems, and medical disposables. Textiles and agriculture are also gaining traction, especially with PHA-based fibers and mulch films for sustainable farming. Packaging dominates the biodegradable plastics market in total demand in 2025. This is supported by rapid growth in food, e-commerce, and flexible packaging films responding to regulations and consumer pressure for sustainable alternatives.

By Raw Material: Sugarcane and Corn Starch Remain Primary Feedstocks, Algae and Lignin Show Highest Growth

Sugarcane and corn starch are the primary raw materials, together making up nearly half of all biodegradable plastics in 2025. Their established agricultural infrastructure and suitability for PLA and TPS production underpin their leadership. Algae is the fastest-growing feedstock, offering high sustainability and low land-use alternatives, while lignin and waste streams are gaining momentum for their role in advancing the circular economy and resource efficiency.

China: Leading Global Biodegradable Plastics Production & Market Penetration

China remains the world’s dominant producer of biodegradable plastics, with annual capacity exceeding 2.0 million metric tons in 2025, accounting for about 60% of global output. The country’s industry leadership is driven by major players such as Kingfa (the global PBAT leader, with expanded production reaching 600,000 tons per year by early 2025), Sinopec (PBS), and BBCA Biochemical (PLA). The national “Double Carbon” policy is aggressively targeting sustainability, with 2025 goals for significant biodegradable packaging penetration across consumer goods and e-commerce, driven by regional mandates and a strong push for replacing single-use plastics. China’s integrated supply chain and proactive regulatory support have made it the epicenter for scalable, cost-competitive biodegradable plastics, enabling major brands to comply with evolving global standards for compostable and marine-degradable packaging. In 2025, several new large-scale PLA and PBAT plants are expected to reach full operational capacity, further solidifying China's export capabilities. Additionally, government-backed research initiatives are focusing on developing advanced biodegradable materials for agricultural films and industrial applications, aiming to extend market penetration beyond packaging. With ongoing investments and robust state policy, China is set to maintain its leadership as the main production and export hub for the world’s biodegradable plastics industry.

United States: Advancing Biodegradable Plastics with Strategic Investments

The United States is scaling its biodegradable plastics market with a focus on advanced formulations and end-use innovation, boasting production capacity of around 450,000 tons per year in 2025, with substantial growth projected. Leading companies like NatureWorks, Danimer Scientific, and TotalEnergies Corbion are playing key roles in advancing biodegradable plastics technologies. In 2024, the U.S. Department of Energy awarded $118 million for next-generation PHA plastics that degrade safely in marine environments, underscoring America’s drive to combat ocean plastic waste. Danimer’s PHA has gained FDA GRAS status for food packaging (Notice 1123), unlocking new opportunities in foodservice and retail packaging. Regulatory momentum is strong: California’s SB 54 law will require 100% recyclable or compostable packaging by 2032, accelerating nationwide adoption of certified biodegradable solutions. In 2025, increased federal funding is being channeled into scaling up pilot projects for innovative biodegradable plastics suitable for sensitive applications like medical devices and agricultural mulches. Major U.S. food and beverage brands are launching new product lines with certified compostable packaging, driven by both consumer demand and proactive compliance strategies for upcoming state-level regulations. With a unique blend of public funding, regulatory drivers, and technical expertise, the U.S. is rapidly becoming a leader in high-performance, application-driven biodegradable plastics.

Germany: Driving Compostable Plastics Innovation & Packaging Reform

Germany is a European leader in the biodegradable plastics market, producing approximately 280,000 tons annually in 2025 with a specialization in PBAT and starch blends. Industry giants such as BASF (with its TÜV-certified Ecoflex PBAT) and Novamont (Mater-Bi) power the sector, delivering advanced compostable products for both retail and foodservice. In 2024, Germany’s market accelerated with the European Union’s PPWR (Packaging and Packaging Waste Regulation), which became legally binding in February 2025, and whose specific compostability mandates for fresh produce packaging are prompting widespread industry reform and innovation across the EU. BASF’s launch of compostable coffee capsules with TÜV certification signals the country’s ongoing commitment to both convenience and sustainability. For 2025, German material science companies are unveiling new generations of multi-layer biodegradable films with enhanced barrier properties, specifically targeting the complex fresh food and processed meat packaging segments to ensure compliance with both compostability and food safety standards. Furthermore, there's a strong push for harmonized industrial composting infrastructure development across Germany to manage the increasing volume of compostable packaging. Germany’s blend of innovation, regulation, and production strength ensures its continued leadership in Europe’s transition to certified compostable packaging and biodegradable plastics.

Italy: Expanding Compostable Bioplastics Leadership for Food & Retail

Italy has emerged as a global leader in compostable biodegradable plastics, producing about 210,000 tons per year in 2025 with a primary focus on bags, foodservice, and retail packaging. Novamont’s Mater-Bi has become the mandated standard for fruit and vegetable bags, as per national law, while Bio-on is pioneering PHA for specialty and durable goods. The Novamont-IKEA partnership for bioplastic furniture highlights the growing demand for compostable materials in non-food sectors. Italy’s strong national composting infrastructure and consumer awareness programs support high end-of-life collection rates, positioning the country as a model for successful bioplastic implementation across the EU and globally. In 2025, driven by the new EU PPWR, Italian packaging manufacturers are significantly investing in new machinery capable of processing high volumes of compostable materials for both primary and secondary packaging, particularly for the fresh food sector. There's also a noticeable increase in Italian luxury brands integrating PHA and other bio-based materials into their packaging, leveraging Italy's design expertise to create aesthetically pleasing and sustainable solutions.

Netherlands: Innovating in Plant-Based Alternatives & Circular Solutions

The Netherlands has solidified its reputation as an innovation hub for biodegradable plastics, with a focus on advanced bio-based PET alternatives and circular business models. Avantium’s world-first 5,000-ton PEF plant, which completed construction in 2024 and is targeting first commercial production in 2025, enables the production of renewable Coca-Cola bottles with superior barrier properties. The country benefits from significant EU Horizon Europe grants (e.g., the HORIZON-JU-CBE-2025-IAFlag-03 call for Circular-by-design fibre-based packaging with improved properties) dedicated to circular packaging, accelerating R&D and commercialization. The Netherlands continues to attract global attention as a site for piloting and scaling sustainable materials, making it an essential player in Europe’s transition to plant-based and compostable plastics. For 2025, Dutch research institutes are leading new collaborations with major FMCG companies to develop pilot programs for chemical recycling of advanced bioplastics like PEF, aiming for truly circular material streams. The government is also expected to announce further incentives for companies investing in bio-based and biodegradable plastic production facilities, reinforcing the Netherlands' position as a hub for sustainable chemistry.

Thailand: Leading Biodegradable Plastics Export & Regional Adoption

Thailand is Southeast Asia’s top producer and exporter of biodegradable plastics, with a capacity of approximately 380,000 tons per year in 2025, focused on PLA and PBS grades. Key players like PTT MCC Biochem and Total Corbion PLA drive technology and exports, supplying packaging for global consumer brands such as Unilever. Government incentives under the Bio-Circular-Green (BCG) Economy initiative are propelling rapid investment in capacity and infrastructure. PTT’s PLA is now used in a variety of branded packaging, positioning Thailand as a regional hub for affordable, high-quality biodegradable plastics. In 2025, Thailand is actively expanding its bioplastics industrial parks, attracting foreign direct investment, particularly from Japanese and European firms, to establish new production facilities for advanced biodegradable polymers. Furthermore, the government is initiating programs to promote the use of biodegradable plastics in the domestic agricultural sector, aiming to reduce plastic pollution from conventional mulch films and packaging in farming.

Brazil: Advancing Sugarcane-Based Bioplastics & Eco-Friendly Packaging

Brazil is a leading supplier of sugarcane-based biodegradable plastics, producing about 130,000 tons annually in 2025. Braskem’s bio-PE, already used in L’Oréal’s sustainable cosmetic packaging, exemplifies the country’s ability to commercialize renewables for mainstream brands. Brazil’s “Plastic Free Amazon” initiative is driving the adoption of biodegradable alternatives across the region, helping to protect biodiversity and address environmental challenges. In 2025, Braskem is expected to announce further capacity expansions for its bio-PE and potentially bio-PP lines, driven by increasing global demand for carbon-negative polymers. There's also a growing focus on developing biodegradable packaging solutions for the booming e-commerce sector within Brazil, leveraging the country's abundant renewable resources. With continued investment and robust cooperation between industry and government, Brazil is set to strengthen its position in the global biodegradable plastics market, particularly in food, retail, and personal care packaging.

India: Accelerating Biodegradable Plastics Growth for Packaging & Infrastructure

India’s biodegradable plastics market is growing at a rapid pace, with production reaching about 90,000 tons per year in 2025 and strong momentum in starch- and PLA-based grades. Major players such as Reliance (bio-PET pilot plant) and Tata Chemicals are scaling up operations to meet rising demand for compostable packaging, foodservice ware, and retail bags. The government’s EPR (Extended Producer Responsibility) rules are providing financial incentives for brands adopting biodegradable solutions. New investments, such as the Zhejiang Hisun and Indian Oil joint venture for a 50,000-ton/year PLA plant slated to begin operations in late 2025, are set to further boost local supply and lower costs. For 2025, the Indian government is set to introduce clearer guidelines for the labeling and certification of biodegradable plastics, aiming to build consumer trust and prevent greenwashing. Additionally, there's a significant push to integrate biodegradable plastics into municipal solid waste management systems, particularly for organic waste collection, to enhance composting efforts in major cities. India’s combination of policy support, growing consumer awareness, and infrastructure investment positions it as a rising force in Asia’s biodegradable plastics supply chain.

Biodegradable Plastics Market Report Scope

Biodegradable Plastics Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8 Billion

|

|

Market Size (2034)

|

$18.1 Billion

|

|

Market Growth Rate

|

9.5%

|

|

Segments

|

By Type (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS) & Co-Polymers (PBSA), Starch Blends / Thermoplastic Starch (TPS), Cellulose-based Plastics, Polycaprolactone (PCL), Others), By Application (Packaging (Flexible, Rigid), Agriculture & Horticulture, Consumer Goods (Disposable Tableware, Personal Care Products), Textiles (Medical & Hygiene, Apparel), Medical & Healthcare, Others), By Raw Material (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Fossil-based, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

NatureWorks LLC, Novamont S.p.A., BASF SE, TotalEnergies Corbion, Danimer Scientific, Mitsubishi Chemical Group Corporation, CJ Biomaterials Inc., Biome Bioplastics, FKuR Kunststoff GmbH, Plantic Technologies Limited, Green Dot Bioplastics, Biotec Biologische Naturverpackungen GmbH & Co. KG, KANEKA Corporation, Polymateria Ltd., Avani Eco, and Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Biodegradable Plastics Market Segmentation

By Type

- Polylactic Acid (PLA)

- Polyhydroxyalkanoates (PHA)

- Polybutylene Adipate Terephthalate (PBAT)

- Polybutylene Succinate (PBS) & Co-Polymers (PBSA)

- Starch Blends / Thermoplastic Starch (TPS)

- Cellulose-based Plastics

- Polycaprolactone (PCL)

- Others

By Application

- Packaging (Flexible, Rigid)

- Agriculture & Horticulture

- Consumer Goods (Disposable Tableware, Personal Care Products)

- Textiles (Medical & Hygiene, Apparel)

- Medical & Healthcare

- Others

By Raw Material

- Sugarcane

- Corn Starch

- Cellulose

- Vegetable Oils

- Lignin

- Algae

- Waste Streams

- Fossil-based

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Biodegradable Plastics Market

- NatureWorks LLC

- Novamont S.p.A.

- BASF SE

- TotalEnergies Corbion

- Danimer Scientific

- Mitsubishi Chemical Group Corporation

- CJ Biomaterials Inc.

- Biome Bioplastics

- FKuR Kunststoff GmbH

- Plantic Technologies Limited

- Green Dot Bioplastics

- Biotec Biologische Naturverpackungen GmbH & Co. KG

- KANEKA Corporation

- Polymateria Ltd.

- Avani Eco

* List Not Exhaustive

Methodology

The Global Biodegradable Plastics Market 2025–2034 report is developed through a rigorous blend of primary and secondary research methodologies. Primary research includes detailed interviews and discussions with biodegradable plastics manufacturers, technology developers, brand sustainability leaders, policymakers, and industry experts to gain firsthand insights into market trends, production expansions, regulatory shifts, and emerging applications. Secondary research draws from scientific publications, patent databases, industry journals, sustainability reports, regulatory documents, trade statistics, and company financial disclosures to validate and refine primary insights. Market sizing and forecasts were conducted using top-down and bottom-up approaches, integrating production capacities, consumption trends, technology penetration rates, and regulatory adoption across over 25 countries. Data was meticulously cross-verified and triangulated to ensure reliability and precision. Proprietary analytics from USDAnalytics further enhance the analysis, delivering advanced insights into competitive dynamics, technological innovations, and scenario-driven forecasts that equip stakeholders with a robust understanding of the biodegradable plastics market landscape.

Research Coverage:

- Geographic Scope: Analysis covers 25+ countries across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

- Segmentation: Detailed segmentation by Type (PLA, PHA, PBAT, PBS & Co-Polymers, TPS, Cellulose-based Plastics, PCL, Others), Application (Packaging (Flexible, Rigid), Agriculture & Horticulture, Consumer Goods, Textiles, Medical & Healthcare, Others), and Raw Material (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Fossil-based, Others).

- Competitive Landscape: Profiles and strategies of 15+ leading manufacturers, technology innovators, and material suppliers shaping the global biodegradable plastics market.

- Trends & Disruptions: In-depth analysis of regulatory mandates, technological breakthroughs (e.g., enzymatic biodegradation), new end-use applications, marine-degradable plastics, and circular economy initiatives.

- Industry Dynamics: Evaluation of market drivers, restraints, investment trends, raw material developments, policy evolution, and supply chain innovations shaping market growth through 2034.

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034

Deliverables:

- Full Market Research Report (PDF, Excel): Comprehensive narrative insights, data tables, charts, and market visualizations.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & Company Profiles

- Regulatory Landscape & Emerging Policy Tracker

- Executive Summary & Analyst Insights

- Custom Queries/Analyst Support Post Sale

Table of Contents

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Biodegradable Plastics Market Overview: Innovation & Sustainability Trends (2025–2034)

2.1. Introduction to Biodegradable Plastics

2.2. Market Valuation and Growth Projections (2025-2034)

2.2.1. Historical Market Size (2021-2024)

2.2.2. Current Market Size (2025)

2.2.3. Forecasted Market Size and CAGR (2025-2034)

2.3. Key Market Drivers

2.3.1. Increasingly Stringent Regulations Against Single-Use Plastics

2.3.2. Rising Adoption of Compostable and Bio-Based Alternatives

2.3.3. Continued Advancements in Polymer Science and Feedstock Innovation

2.4. Market Challenges and Restraints

3. Global Biodegradable Plastics Market Analysis: Growth Drivers & Innovations

3.1. Product Innovations: Expanding Market Horizons for Biodegradable Plastics

3.1.1. Soil-Biodegradable Mulch Film for Agriculture (BASF ecovio® M2351)

3.1.2. PHA-Based Home-Compostable Coffee Pods (Danimer Scientific Nodax™)

3.1.3. Soil-Biodegradable Mulch Films for Agriculture (Mitsubishi Chemical BioPBS™ FD92)

3.2. Capacity Expansions: Underscoring Market Scalability & Future Supply

3.2.1. TotalEnergies Corbion: Luminy® PLA Production Expansion

3.2.2. NatureWorks: New PLA Plant in Thailand

3.2.3. Kaneka: Scaling PHBH™ Production

3.3. Strategic Partnerships & M&A: Redefining Market Leadership in Biodegradable Plastics

3.3.1. Versalis’ Acquisition of Novamont

3.3.2. Cargill’s Joint Venture with Helm AG for Bio-Based 1,4-Butanediol (BDO)

3.3.3. Solvay’s Joint Development with BioAmber on Bio-Succinic Acid Derivatives

3.4. Regulatory Shifts: Driving Rapid Adoption of Biodegradable Plastics

3.4.1. EU Packaging and Packaging Waste Regulation (PPWR) Mandates

3.4.2. Thailand’s Plastic Bag Ban

3.4.3. California’s SB 54 Law for Serviceware Packaging

3.5. Technological Advances: Solving Performance & Environmental Challenges

3.5.1. Enzyme-Embedded PLA for Accelerated Biodegradation (MIT)

3.5.2. Cellulose-Starch Biocomposites for Marine Degradation (Fraunhofer UMSICHT)

3.6. Brand Sustainability Efforts: Fueling Biodegradable Plastics Market Growth

3.6.1. Nestlé’s Home-Compostable, Paper-Based Nespresso Pods

3.6.2. Unilever’s Exploration of Innovative Sustainable Packaging (Ben & Jerry’s)

4. Biodegradable Plastics Industry Dynamics: New Recycling Methods & Marine Safety

4.1. Trend: Enzymatic Biodegradation Revolutionizing Plastic Recycling & Adoption

4.1.1. Carbios’ C-ZYME® Enzymatic Process for Plastic Breakdown

4.1.2. Investments in Scaling Enzymatic Recycling Facilities

4.1.3. Environmental Benefits: Reduced GHG Emissions and Resource Depletion

4.1.4. Expanding Adoption Across Beverage, Textile, and Agriculture Sectors

4.2. Opportunity: Marine-Degradable PHA Tackling Ocean Plastics & Transforming Fisheries

4.2.1. Lost Fishing Gear as a Major Contributor to Ocean Plastic Waste

4.2.2. PHA-Based Fishing Gear: Certified Marine Degradability and Performance

4.2.3. Strengthening Business Case: Production Cost Reduction and Growing Demand

4.2.4. Government and Institutional Support for Transition (Thailand, Norway, ADB)

5. Competitive Landscape of the Global Biodegradable Plastics Market: Innovation, Scaling, and Strategic Growth in 2024

5.1. Key Players and Market Competition Overview

5.2. Company Profiles & Strategies (Overview)

5.2.1. NatureWorks: Dominant Force in PLA Biodegradable Plastics

5.2.2. TotalEnergies Corbion: Major Player in PLA Production

5.2.3. Kaneka Corporation: Scaling PHA Operations & Innovations

5.2.4. Novamont: Leader in Starch-Based Biodegradable Plastics

5.2.5. BASF SE: Advancing PBAT & Circular Biodegradable Solutions

5.2.6. Other Key Players (Detailed profiles in Chapter 9)

6. Biodegradable Plastics Market Share Analysis

6.1. By Type

6.1.1. Polylactic Acid (PLA)

6.1.2. Polyhydroxyalkanoates (PHA)

6.1.3. Polybutylene Adipate Terephthalate (PBAT)

6.1.4. Polybutylene Succinate (PBS) & Co-Polymers (PBSA)

6.1.5. Starch Blends / Thermoplastic Starch (TPS)

6.1.6. Cellulose-based Plastics

6.1.7. Polycaprolactone (PCL)

6.1.8. Others

6.2. By Application

6.2.1. Packaging

6.2.1.1. Flexible Packaging

6.2.1.2. Rigid Packaging

6.2.2. Agriculture & Horticulture

6.2.3. Consumer Goods

6.2.3.1. Disposable Tableware

6.2.3.2. Personal Care Products

6.2.4. Textiles

6.2.4.1. Medical & Hygiene

6.2.4.2. Apparel

6.2.5. Medical & Healthcare

6.2.6. Others

6.3. By Raw Material

6.3.1. Sugarcane

6.3.2. Corn Starch

6.3.3. Cellulose

6.3.4. Vegetable Oils

6.3.5. Lignin

6.3.6. Algae

6.3.7. Waste Streams

6.3.8. Fossil-based

6.3.9. Others

7. Geographic Analysis: Biodegradable Plastics Market Outlook by Country (2021- 2034)

7.1. North America

7.1.1. United States: Advancing Biodegradable Plastics with Strategic Investments

7.1.2. Canada: Steady Growth Driven by Sustainable Packaging Demand and Polysaccharide Dominance

7.1.3. Mexico: Rapid Expansion Fueled by Sustainable Packaging and F&B Sector Demand

7.2. Europe

7.2.1. Germany: Driving Compostable Plastics Innovation & Packaging Reform

7.2.2. UK: Strong Growth Driven by Packaging Sector and Environmental Awareness

7.2.3. France: Increasing Adoption Driven by Stringent Regulations and Innovative Material Development

7.2.4. Spain: Significant Market Expansion Led by Polysaccharide and PLA Adoption

7.2.5. Italy: Expanding Compostable Bioplastics Leadership for Food & Retail

7.2.6. Russia: Emerging Market with Growing Awareness and Demand for Eco-friendly Alternatives

7.2.7. Rest of Europe: Broad Adoption of Bio-based Biodegradables and Flexible Packaging Amidst Policy Shifts

7.2.8. Netherlands: Innovating in Plant-Based Alternatives & Circular Solutions

7.3. Asia Pacific

7.3.1. China: Leading Global Biodegradable Plastics Production & Market Penetration

7.3.2. Japan: Developing High-Performance Biopolymer Films for Packaging & Electronics

7.3.3. India: Accelerating Biodegradable Plastics Growth for Packaging & Infrastructure

7.3.4. South Korea: Advancing Sustainable Biopolymer Market with Focus on Packaging and Biomedical Applications

7.3.5. Australia: Accelerating Adoption in Packaging and Agriculture with Focus on Polysaccharides and PLA

7.3.6. Southeast Asia: Rising Demand in Flexible Packaging and Electronics, Bolstered by Government Initiatives

7.3.7. Rest of Asia: Significant Market Share and Fastest Growth Driven by Demand for Bio-based Packaging

7.4. South America

7.4.1. Brazil: Advancing Sugarcane-Based Bioplastics & Eco-Friendly Packaging

7.4.2. Argentina: Emerging Market with Potential in Electrical & Electronics and Biodegradable Applications

7.4.3. Rest of South America: Increasing Adoption of PLA and PHA in Sustainable Packaging Solutions

7.5. Middle East and Africa

7.5.1. Saudi Arabia: Developing Market for Lignin-based Biopolymers in Construction and Agriculture

7.5.2. UAE: Rapidly Growing Demand for Sustainable Packaging and Consumer Goods

7.5.3. Rest of Middle East: Expanding Market for Bioplastics in Packaging and Electrical & Electronics Sectors

7.5.4. South Africa: Growing Adoption of Biopolymers in Electrical & Electronics and Packaging

7.5.5. Egypt: Increasing Focus on Bioplastic Multi-Layer Films for Food Packaging and Delivery Services

7.5.6. Rest of Africa: Rising Demand for Eco-Friendly Plastics, Particularly in Packaging Industry

8. Biodegradable Plastics Market Size Outlook by Region (2025-2034)

8.1. North America Biodegradable Plastics Market Size Outlook to 2034

8.1.1. By Type (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS) & Co-Polymers (PBSA), Starch Blends / Thermoplastic Starch (TPS), Cellulose-based Plastics, Polycaprolactone (PCL), Others)

8.1.2. By Application (Packaging (Flexible, Rigid), Agriculture & Horticulture, Consumer Goods (Disposable Tableware, Personal Care Products), Textiles (Medical & Hygiene, Apparel), Medical & Healthcare, Others)

8.1.3. By Raw Material (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Fossil-based, Others)

8.2. Europe Biodegradable Plastics Market Size Outlook to 2034

8.2.1. By Type (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS) & Co-Polymers (PBSA), Starch Blends / Thermoplastic Starch (TPS), Cellulose-based Plastics, Polycaprolactone (PCL), Others)

8.2.2. By Application (Packaging (Flexible, Rigid), Agriculture & Horticulture, Consumer Goods (Disposable Tableware, Personal Care Products), Textiles (Medical & Hygiene, Apparel), Medical & Healthcare, Others)

8.2.3. By Raw Material (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Fossil-based, Others)

8.3. Asia Pacific Biodegradable Plastics Market Size Outlook to 2034

8.3.1. By Type (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS) & Co-Polymers (PBSA), Starch Blends / Thermoplastic Starch (TPS), Cellulose-based Plastics, Polycaprolactone (PCL), Others)

8.3.2. By Application (Packaging (Flexible, Rigid), Agriculture & Horticulture, Consumer Goods (Disposable Tableware, Personal Care Products), Textiles (Medical & Hygiene, Apparel), Medical & Healthcare, Others)

8.3.3. By Raw Material (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Fossil-based, Others)

8.4. South America Biodegradable Plastics Market Size Outlook to 2034

8.4.1. By Type (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS) & Co-Polymers (PBSA), Starch Blends / Thermoplastic Starch (TPS), Cellulose-based Plastics, Polycaprolactone (PCL), Others)

8.4.2. By Application (Packaging (Flexible, Rigid), Agriculture & Horticulture, Consumer Goods (Disposable Tableware, Personal Care Products), Textiles (Medical & Hygiene, Apparel), Medical & Healthcare, Others)

8.4.3. By Raw Material (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Fossil-based, Others)

8.5. Middle East and Africa Biodegradable Plastics Market Size Outlook to 2034

8.5.1. By Type (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS) & Co-Polymers (PBSA), Starch Blends / Thermoplastic Starch (TPS), Cellulose-based Plastics, Polycaprolactone (PCL), Others)

8.5.2. By Application (Packaging (Flexible, Rigid), Agriculture & Horticulture, Consumer Goods (Disposable Tableware, Personal Care Products), Textiles (Medical & Hygiene, Apparel), Medical & Healthcare, Others)

8.5.3. By Raw Material (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Fossil-based, Others)

9. Company Profiles: Leading Players in the Biodegradable Plastics Market

9.1. NatureWorks LLC

9.2. Novamont S.p.A.

9.3. BASF SE

9.4. TotalEnergies Corbion

9.5. Danimer Scientific

9.6. Mitsubishi Chemical Group Corporation

9.7. CJ Biomaterials Inc.

9.8. Biome Bioplastics

9.9. FKuR Kunststoff GmbH

9.10. Plantic Technologies Limited

9.11. Green Dot Bioplastics

9.12. Biotec Biologische Naturverpackungen GmbH & Co. KG

9.13. KANEKA Corporation

9.14. Polymateria Ltd.

9.15. Avani Eco

10. Research Methodology

10.1. Data Collection Approach (Primary & Secondary Research)

10.2. Market Sizing and Forecasting Model

10.3. Data Validation and Triangulation

10.4. Proprietary Intelligence & Tools (USDAnalytics)

11. Report Scope & Deliverables

11.1. Report Scope

11.1.1. Geographic Coverage

11.1.2. Market Segmentation

11.1.3. Competitive Landscape Assessment

11.1.4. Key Trends & Disruptions

11.1.5. Industry Dynamics

11.1.6. Historic and Forecast Data Range

11.2. Deliverables

11.2.1. Full Market Research Report (PDF, Excel)

11.2.2. Country-Level Forecasts & Analysis

11.2.3. Segment-wise Revenue Projections

11.2.4. Competitive Benchmarking & Company Profiles

11.2.5. Regulatory Landscape & Emerging Policy Tracker

11.2.6. Executive Summary & Key Analyst Insights

11.2.7. Custom Queries/Analyst Support Post Sale

12. Disclaimer